$300B and Counting: New Money Inflow or Crypto Natives Playing Defense?

2026/03/31 13:11:52

The digital asset ecosystem has officially entered a new epoch. In March 2026, the aggregate market capitalization of stablecoins breached the $300 billion milestone, a figure that was once dismissed as a generational peak but now appears to be a structural floor. This achievement is not merely a quantitative win for "crypto"; it is a qualitative shift in how the world perceives the US Dollar as a programmable, global utility.

The digital asset ecosystem has officially entered a new epoch. In March 2026, the aggregate market capitalization of stablecoins breached the $300 billion milestone, a figure that was once dismissed as a generational peak but now appears to be a structural floor. This achievement is not merely a quantitative win for "crypto"; it is a qualitative shift in how the world perceives the US Dollar as a programmable, global utility.When the market last saw significant growth in 2021 and early 2024, stablecoins were largely viewed as "casino chips"—temporary placeholders used by traders to jump in and out of volatile assets like Bitcoin and Ethereum. Today, the landscape is fundamentally different. The breach of $300 billion occurs against a backdrop of sophisticated regulation, the rise of tokenized Real-World Assets (RWA), and a global economy that is increasingly looking for "Digital Dollars" to bypass legacy banking inefficiencies.

The central tension in the current market revolves around the origin of this capital. Is the $300 billion a signal of a massive "New Money" on-ramp fueled by institutional adoption and the GENIUS Act of 2025? Or is it a defensive posture by "Old Money"—crypto natives who have sold their bags at local tops and are now sitting on a mountain of dry powder, waiting for a macro correction? To understand the future of the bull market, we must first deconstruct the anatomy of this $300 billion liquid wall.

Key Takeaways

-

A New Regulatory Era: The GENIUS Act of 2025 has provided the legal "green light" for U.S. institutions to hold and settle in stablecoins, transforming them from speculative tools into regulated financial instruments.

-

Institutional Domination: A significant portion of the recent $50B+ inflow is "New Money" from corporate treasuries and fintech integrations (Stripe, PayPal, Visa) rather than just retail trading.

-

The RWA Engine: Stablecoins are no longer just sitting idle; they are the primary currency for purchasing Tokenized Treasury Bills, which currently offer competitive yields compared to traditional high-yield savings accounts.

-

Strategic Defense: Large "whales" from the 2023-2024 cycle are increasingly rotating into stablecoins to capture yield and hedge against volatility, keeping the total market cap high even when BTC price action stalls.

-

Market Implications: A $300B stablecoin supply represents the largest "buy wall" in financial history, suggesting that any significant dip in BTC or ETH will be aggressively met by sidelined liquidity.

Breaking Down the $300B: The Hierarchy of Digital Dollars

To analyze whether this is new or old money, we must first look at the distribution of the assets themselves. The stablecoin market is no longer a monolith; it has bifurcated into "offshore liquidity" and "onshore regulated" sectors.

Tether (USDT) continues to hold the lion's share of the market, currently hovering around $185 billion. Tether remains the undisputed king of global liquidity, particularly in emerging markets and offshore exchanges. Its growth in 2025 and early 2026 has been driven by its role as the "Eurodollar of the 21st century." In regions dealing with high inflation or restricted access to USD, USDT has become the primary medium of exchange for small businesses and cross-border remittances. Platforms that prioritize global accessibility, such as KuCoin, have become central hubs for this liquidity, providing the deep order books and diverse trading pairs necessary for these international participants to move seamlessly between stablecoins and a wide array of altcoins.

USD Coin (USDC), issued by Circle, has seen a resurgence following the implementation of the GENIUS Act. Now sitting at approximately $80 billion, USDC’s growth is the clearest indicator of institutional "New Money." Because USDC is compliant with the latest federal audit requirements, it has become the preferred vehicle for BlackRock, Fidelity, and other major asset managers who are moving into the tokenization space. When we see USDC supply expansion, it is almost always a signal of fresh capital entering the ecosystem from the traditional financial (TradFi) sector.

Finally, we see the rise of decentralized and yield-bearing stables like USDS (formerly DAI) and Ethena’s USDe. These assets represent the "Native" side of the equation. Their growth is often tied to "Old Money" crypto natives who want to stay on-chain but earn a "risk-free" rate that rivals or exceeds the Federal Reserve’s overnight repo rate. By analyzing the growth of these three distinct buckets, we can see that the $300 billion mark is a hybrid achievement—a mix of global retail necessity, institutional on-ramping, and sophisticated DeFi yield-seeking.

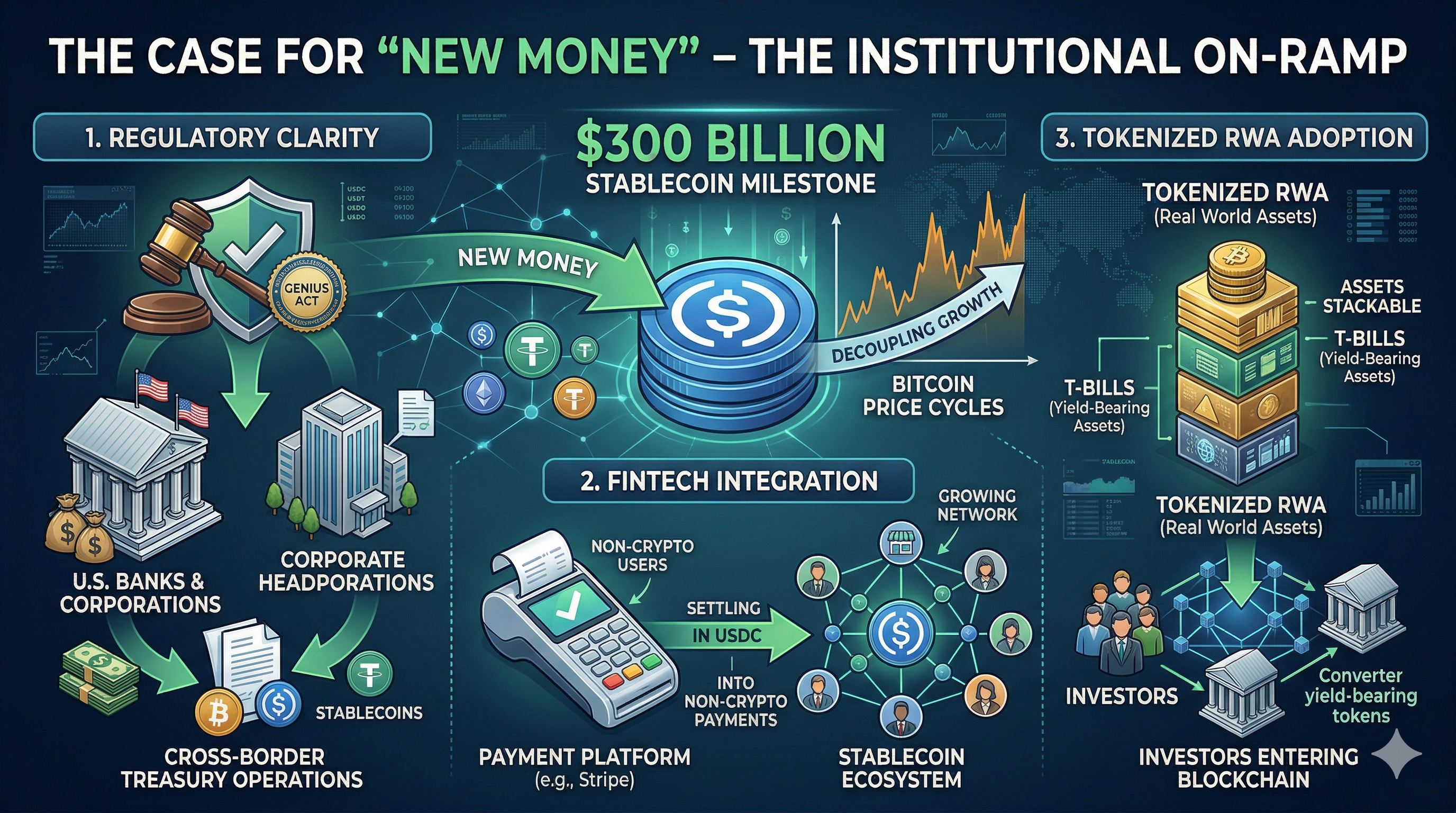

The Case for “New Money” – The Institutional On-Ramp

The most compelling argument for the $300 billion milestone being "New Money" is the tectonic shift in the regulatory landscape. Prior to 2025, many institutional CFOs were hesitant to touch stablecoins due to a "gray area" in accounting and legal status. The passage of the GENIUS Act (Generating Enhanced National Infrastructure for United Stables) changed the calculus.

For the first time, U.S. banks were given a clear pathway to issue their own stablecoins or custody third-party ones. This led to a massive influx of corporate treasury funds. Large multinational corporations began using stablecoins for intra-company transfers, finding that they could settle millions of dollars across borders in seconds for a fraction of the cost of a SWIFT wire. This is capital that was never in the crypto market before; it is "New Money" that views the blockchain purely as a superior settlement rail.

Furthermore, the integration of stablecoins into the fintech stack has brought in millions of non-crypto users. When a small business owner accepts a payment via Stripe that is settled in USDC, that liquidity contributes to the $300 billion market cap. These users don't consider themselves "crypto investors"; they are simply using a faster, cheaper dollar. This "invisible" adoption is perhaps the most bullish long-term indicator, as it decouples stablecoin growth from the boom-and-bust cycles of Bitcoin's price.

For many entering this space for the first time, user-friendly exchanges like KuCoin provide a gateway to put this new liquidity to work, offering products like "KuCoin Earn" where users can find competitive flexible savings options for their idle stablecoins while they navigate the broader market.

The Case for “Old Money” – The Strategic Flight to Safety

While the institutional narrative is strong, we cannot ignore the behavior of the "Crypto Natives"—the whales and early adopters who have survived multiple cycles. For this group, the $300 billion market cap is a sign of a "Risk-Off" rotation.

Historically, when Bitcoin approaches or breaks previous all-time highs (as it did in late 2025), savvy investors begin to "ladder out" of their positions. Instead of exiting to fiat—which involves bank delays, high fees, and potential tax reporting friction—they move into stablecoins. This allows them to stay "on-chain" and ready to "buy the dip" at a moment's notice. The fact that the stablecoin market cap remains at an all-time high while Bitcoin's price experiences a sideways consolidation suggests that the "Old Money" isn't leaving the ecosystem—it is simply waiting for a better entry point.

This defensive posture is further incentivized by the evolution of on-chain yield. In previous cycles, sitting in stablecoins meant earning 0% or taking high risks in unproven DeFi protocols. In 2026, stablecoin holders can earn a "natural yield" derived from the underlying Treasury reserves held by the issuers. When a whale holds $100 million in a yield-passing stablecoin, they are essentially holding a digital version of a sovereign bond. This makes the "Safe Haven" play highly profitable, reducing the urgency to rotate back into volatile "Risk-On" assets like altcoins.

We also see a "Defensive" trend in the rise of algorithmic and delta-neutral strategies. Protocols like Ethena allow investors to hold a "synthetic dollar" while earning a yield from the basis trade. This has attracted billions of dollars from crypto-native hedge funds that want to hedge their market exposure without exiting to the traditional banking system. This capital is "Old Money" that has become more sophisticated, contributing to the $300 billion total without necessarily representing a new buyer in the market.

Beyond the Narrative: Analyzing On-Chain Data

To settle the debate between "New" and "Old" money, we must look at the hard data provided by the blockchain. On-chain metrics in 2026 provide a granular view of how these $300 billion are actually being used.

First, let’s look at Address Growth vs. Transaction Volume. If the market cap growth was purely "Old Money" playing defense, we would see a stagnant number of unique wallets but a high concentration of wealth in large addresses. However, data from early 2026 shows a 40% year-over-year increase in active stablecoin addresses with balances between $1,000 and $10,000. This suggests a "middle-class" adoption phase that is characteristic of "New Money" entering the space for payments and savings.

Second, the Exchange Reserve vs. Private Wallet metric is telling. In 2021, over 50% of the stablecoin supply was sitting on centralized exchanges, ready to be traded. Today, that number has dropped to less than 25%. The majority of the $300 billion is now held in self-custody wallets or locked in smart contracts for RWA yields. This indicates that stablecoins are being used as a Store of Value (SoV) rather than just a medium for speculation. When money moves off an exchange and into a long-term yield protocol, it behaves more like "Old Money" seeking a safe haven or "New Money" using the chain as a bank account.

Third, we must examine the Velocity of Money. Velocity measures how often a single dollar is moved within a specific timeframe. Interestingly, while the market cap has hit record highs, the velocity of stablecoins on Layer 2 networks like Base, Arbitrum, and Polygon has increased by 300% since 2024. This high velocity is a hallmark of "New Money" utility. It means people are actually using these digital dollars to buy goods, pay for AI-agent services, and settle debts, rather than just letting them sit in a trading account.

What Does This Mean for Altcoins and BTC?

The implications of a $300 billion stablecoin floor for the rest of the market are profoundly bullish, though they require a bit of nuance. In the short term, a high stablecoin market cap often acts as a "drag" on price action because it represents capital that has been pulled out of BTC and ETH. However, in the medium to long term, this is the most significant indicator of future price appreciation.

The "Spring" Effect: Think of the $300 billion as a compressed spring. In previous cycles, the total stablecoin supply was often less than 10% of the total crypto market cap. As we head into mid-2026, that ratio has shifted. There is now more "ready-to-deploy" cash on the sidelines than ever before. If a catalyst—such as a further interest rate cut by the Fed or a major technological breakthrough in Layer 2 scaling—triggers a "Risk-On" sentiment, the rotation from stables back into BTC could be the most violent upward move in the history of the asset class.

The Altcoin "Quality" Filter: For altcoins, the $300 billion milestone is a double-edged sword. While there is more liquidity available to pump small-cap tokens, the "New Money" entering via the GENIUS Act is generally more conservative. Institutional investors are unlikely to rotate their USDC into speculative meme coins. Instead, they are looking for "Blue Chip" altcoins with clear revenue models and regulatory compliance. Consequently, we may see a "divergence" where high-utility altcoins thrive while purely speculative tokens struggle to attract this new class of capital.

Market Stability: Perhaps the most underrated benefit of the $300 billion market cap is the added stability it brings to the ecosystem. Deep stablecoin liquidity acts as a buffer during flash crashes. When Bitcoin's price drops, the presence of billions of dollars in sidelined stables allows for faster "dip buying," which prevents the "death spirals" that were common in the 2018 and 2022 bear markets. We are moving toward a more mature, liquid market that behaves more like the S&P 500 and less like a volatile penny stock.

Conclusion: A Bullish Signal with a Caveat

The breach of the $300 billion stablecoin market cap is a watershed moment for the digital asset industry. It is the clearest evidence yet that the "Digital Dollar" has won the race to become the internet’s native currency.

Through our analysis, it becomes clear that the "New Money vs. Old Money" debate isn't a zero-sum game. The $300 billion is a hybrid monument. It is built on the foundation of "Old Money" natives who have matured into sophisticated on-chain treasurers, but it is being propelled into the stratosphere by "New Money" institutions that are finally comfortable with the regulatory clarity provided by the GENIUS Act.

However, the caveat remains: with great liquidity comes great scrutiny. As stablecoins become a systemic part of the global financial plumbing, the risks of centralized "kill switches," regulatory overreach, and reserve transparency will only intensify. The $300 billion mark is not just a celebration of growth; it is a call for the industry to maintain the highest standards of integrity.

For investors, the message is clear: the "dry powder" is at an all-time high. The infrastructure is ready. The world is on-boarded. Whether this capital is playing defense today or preparing for an offensive tomorrow, the digital asset market has never been more liquid, more regulated, or more ready for the next leg of global adoption.

FAQs

What triggered the sudden growth to $300 billion in 2026?

The primary triggers were the GENIUS Act of 2025, which provided a federal framework for stablecoin issuers in the U.S., and the rapid expansion of Tokenized Real-World Assets (RWA). These developments allowed institutional capital to enter the market legally and earn yields from U.S. Treasuries directly on the blockchain.

Is USDT or USDC a better indicator of "New Money"?

While both are growing, USDC is generally considered a better indicator of "New Money" from Western institutions and regulated entities due to its strict adherence to U.S. compliance standards. USDT growth typically reflects "New Money" in global emerging markets and offshore trading liquidity.

Does a high stablecoin market cap mean Bitcoin’s price will go up?

Not necessarily in the immediate term, but it is a strong long-term indicator. A high stablecoin market cap represents "sidelined liquidity." While it can mean people are selling BTC (pushing price down), it also means there is a massive amount of cash ready to buy BTC as soon as the market sentiment turns bullish.

How do stablecoins earn yield in 2026?

In 2026, many stablecoins are "yield-bearing" or "yield-passing." Because the issuers hold their reserves in interest-bearing assets like U.S. Treasury bills, they can pass a portion of that yield back to the holders via decentralized finance (DeFi) protocols or through direct programmatic updates to the token's value.

What is the risk of the stablecoin market getting too large?

The main risk is systemic importance. If a stablecoin issuer holding $100B+ in Treasuries were to fail or face a regulatory freeze, it could cause a liquidity crisis not just in crypto, but in the traditional bond markets as well. This is why the 2025-2026 regulatory push has focused so heavily on "stress testing" stablecoin reserves.