Bitcoin Accumulation Strategy and BTC Price Outlook to 2030: How Long-Term Investors Can Build Exposure With Discipline

2026/06/22 17:02:00

Introduction

Every Bitcoin cycle creates the same illusion: investors believe the most important decision is finding the perfect entry price. In reality, the investors who historically benefited most from Bitcoin's long-term appreciation were often not those who bought at the absolute bottom, but those who developed a repeatable accumulation framework and remained invested through multiple market environments.

As Bitcoin moves further into institutional adoption and broader capital market integration, the investment discussion is changing. The question is no longer whether Bitcoin can reach a certain number in the next few months. Instead, long-term investors increasingly want to understand how much Bitcoin they should accumulate, how to manage downside risk during accumulation, and what realistic price expectations may look like by 2030.

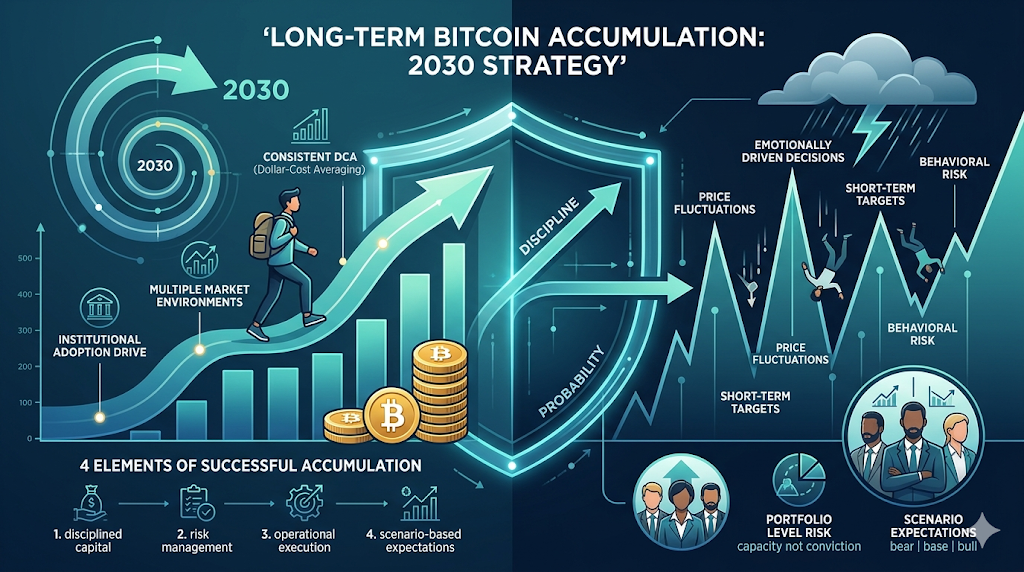

A successful Bitcoin accumulation strategy combines four elements: disciplined capital deployment, portfolio-level risk management, operational execution, and scenario-based expectations rather than relying on a single price target. Investors who approach Bitcoin through this framework are often better positioned to participate in long-term upside while reducing the probability of making emotionally driven decisions during volatility.

Practical Accumulation Strategies: DCA, Lump-Sum, and Tranche Plans

For most investors, the most effective Bitcoin accumulation strategy is not maximizing entry precision but maximizing consistency over time. Because Bitcoin remains a highly volatile asset, accumulation methods should focus on controlling behavioral risk rather than predicting short-term price movements.

Dollar-cost averaging (DCA), lump-sum investing, and tranche-based deployment each serve different objectives and risk profiles. The optimal approach depends less on market forecasts and more on available capital, investment horizon, and tolerance for drawdowns.

Dollar-cost averaging remains the most broadly applicable approach because it transforms market uncertainty into a fixed investment process. Under DCA, investors commit predefined amounts at fixed intervals regardless of price. This approach reduces decision fatigue and prevents overexposure during periods of market enthusiasm.

Below is a practical framework investors can immediately apply:

| Risk Profile | Monthly Capital | Deployment Method | Position Build Timeline |

| Conservative | $300-$800 | Monthly DCA | 18-24 months |

| Neutral | $1,000-$3,000 | Weekly DCA + tactical adds | 12-18 months |

| Aggressive | $5,000+ | Multi-tranche entry | 6-12 months |

For example, a conservative investor may allocate $500 on the first trading day of every month and review position sizing only once every six months. A neutral investor may split capital into weekly purchases while reserving approximately 20%-30% for volatility opportunities. An aggressive investor may divide target exposure into ten tranches and deploy additional capital only when objective conditions are met.

Execution rules become particularly important when tranche investing is used. Instead of buying based on emotions, investors can predefine accumulation triggers such as:

-

Add one tranche if Bitcoin remains above the 200-day moving average and declines more than 15%.

-

Increase deployment size if 30-day volatility compresses below historical norms.

-

Deploy accelerated capital only after ATR-normalized pullbacks.

Compared with DCA, lump-sum investing historically performs well when entered early in prolonged bull markets because full capital becomes productive immediately. However, the cost of being wrong is significantly higher. Investors entering with full exposure shortly before a major correction may experience drawdowns large enough to abandon the strategy altogether.

Transaction costs should also be incorporated into planning. Frequent small purchases reduce timing risk but may increase cumulative trading fees and settlement costs. Extremely large orders may generate slippage depending on venue liquidity.

For U.S. investors, accumulation should include tax-aware execution from the beginning. Maintaining lot-by-lot accounting can materially improve future flexibility. Specific Identification accounting may provide more efficient tax outcomes than FIFO because investors retain greater control over cost basis selection when reducing positions later.

The key advantage of structured accumulation is not superior forecasting. It is reducing the probability that emotions determine investment decisions.

Portfolio Allocation and Risk Management for Long-Term BTC Exposure

Bitcoin accumulation becomes significantly more effective when viewed as part of a broader portfolio instead of an isolated investment thesis.

One of the most common mistakes among long-term investors is determining position size based on conviction rather than risk capacity. Strong conviction does not eliminate volatility, and concentration risk remains one of the largest threats to long-term compounding.

A more practical approach is to determine Bitcoin exposure according to investment objectives, expected return requirements, and maximum acceptable portfolio drawdown. The following allocation ranges provide a starting framework:

| Investor Profile | Suggested BTC Allocation |

| Conservative | 1%-3% |

| Balanced | 3%-8% |

| Growth-Oriented | 8%-20% |

These ranges are not forecasts of future performance. They are risk management tools designed to preserve portfolio survivability across different market conditions. Position increases should also follow predefined rules.

For example, investors may decide to increase Bitcoin exposure only after total portfolio value exceeds predetermined milestones or after quarterly review periods. This approach avoids a common behavioral trap in which investors continuously increase allocation simply because prices are rising.

Rebalancing frequency matters as well. Quarterly rebalancing remains a practical default because it balances responsiveness with transaction efficiency. Investors may additionally apply volatility-triggered rebalancing if Bitcoin grows beyond 125% of its intended portfolio allocation.

Risk management should include explicit drawdown planning rather than relying on subjective judgment during periods of market stress.

A practical framework could look like this:

-

Portfolio drawdown below 20%: maintain schedule.

-

Drawdown between 20%-35%: continue DCA but pause accelerated buys.

-

Drawdown above 35%: reassess assumptions before adding exposure.

When discussing Bitcoin's outlook to 2030, investors should avoid relying on single-number predictions. Probability-based scenario construction generally creates more robust decisions.

| Scenario | Probability | BTC Price Range | Expected Portfolio Effect |

| Bear Case | 30% | $80,000-$180,000 | Moderate contribution |

| Base Case | 50% | $180,000-$350,000 | Meaningful growth |

| Bull Case | 20% | $350,000-$700,000+ | Dominant return source |

This framework shifts the conversation from “Will Bitcoin reach a target?” to “How does my portfolio perform across multiple outcomes?” That distinction often determines whether investors remain disciplined through the full market cycle.

Bitcoin Price Scenarios to 2030: Probabilistic Ranges and Key Drivers

Forecasting Bitcoin with a single target price is attractive for headlines but rarely useful for portfolio decisions. A more practical approach is to build probability-weighted scenarios and understand which variables would need to occur for each scenario to materialize.

Bitcoin's long-term valuation remains driven by a combination of supply constraints, demand expansion, macroeconomic conditions, and institutional adoption. None of these variables operate independently, which is why identical price targets can emerge from completely different market structures.

On the supply side, Bitcoin continues to operate under a declining issuance schedule. The most recent halving reduced the pace of newly created supply, and historically the full effects of supply compression have tended to emerge gradually rather than immediately.

However, total circulating supply is not equivalent to liquid supply. A meaningful portion of existing Bitcoin is estimated to be permanently inaccessible due to lost private keys, inactive wallets, and long-term storage behavior. At the same time, exchange balances have trended lower over multiple cycles as more coins move into long-term custody structures.

Miner behavior also remains an important variable. During expansion periods, miners may reduce selling pressure and retain larger portions of mined inventory. During periods of stress, miner distribution can temporarily increase available supply and create local market pressure.

Demand-side developments may become even more influential by 2030. Institutional allocation remains one of the most closely watched variables because relatively small portfolio allocations from traditional capital pools can generate disproportionately large effects due to Bitcoin's comparatively limited liquid market.

Additional drivers include:

-

ETF adoption and net inflows,

-

sovereign and corporate treasury participation,

-

retirement platform integration,

-

global liquidity conditions,

-

long-term holder accumulation,

-

active address expansion.

These variables create a range of plausible outcomes rather than a single destination.

| Scenario | Estimated Probability | BTC Range by 2030 | Core Assumptions |

| Bear Case | 25% | $90,000-$180,000 | Slower adoption, restrictive liquidity |

| Base Case | 50% | $180,000-$400,000 | Continued institutional participation |

| Bull Case | 25% | $400,000-$800,000+ | Accelerated capital inflows and supply tightening |

Investors should interpret these scenarios as frameworks rather than predictions. Several commonly referenced valuation models may provide context but should not be treated as forecasting tools.

Stock-to-flow models emphasize scarcity and issuance reduction but historically struggle when macro conditions dominate liquidity.

Network-effect frameworks attempt to connect value creation to adoption growth but often underestimate cyclical sentiment. Institutional allocation models evaluate Bitcoin as an emerging portfolio asset but remain highly sensitive to assumptions around capital rotation.

Ultimately, no model consistently predicts Bitcoin's exact future price. What investors can control is whether their portfolio remains resilient across multiple outcomes.

Hedging, Yield, and Execution Tactics During Accumulation

Accumulation does not necessarily require investors to remain fully exposed to downside volatility. Long-term positioning and risk management can coexist if implemented with clear rules and realistic expectations. For investors seeking downside protection, options strategies remain among the most direct tools.

Protective put structures allow investors to maintain spot exposure while defining maximum downside over a given period. The trade-off is explicit premium cost, which reduces net returns if protection expires unused.

A collar structure lowers hedging cost by financing downside protection through capped upside participation. This approach may appeal to investors who prioritize capital preservation over capturing every phase of market expansion.

Futures-based approaches can also serve accumulation goals. Instead of directional speculation, investors may use calendar structures or temporary overlays to reduce portfolio volatility while continuing scheduled spot purchases.

Hedging should remain proportional. Attempting to fully hedge long-term Bitcoin exposure often introduces excessive complexity and cost. Partial protection during periods of elevated uncertainty is generally more sustainable.

Some investors also attempt to improve portfolio efficiency through yield generation. Yield opportunities broadly fall into three categories:

-

centralized lending platforms,

-

decentralized lending protocols,

-

regulated yield-oriented structures.

Each introduces trade-offs between accessibility, return potential, compliance requirements, and counterparty exposure. Investors should evaluate yield opportunities cautiously because additional percentage returns rarely compensate for significant custody risk.

Execution quality during accumulation also deserves attention. Large market orders frequently create unnecessary slippage, especially during periods of reduced liquidity. More efficient execution methods include:

-

staged limit orders,

-

iceberg execution,

-

OTC block settlement,

-

time-based order splitting.

Investors transferring assets across venues should additionally account for withdrawal costs, confirmation timing, transfer verification procedures, and operational security. Tax-aware execution may further improve long-term outcomes.

Realizing losses intentionally during drawdowns can create future flexibility, while maintaining complete transaction histories simplifies reporting obligations. The objective of accumulation is not maximizing every source of return. It is preserving the ability to remain invested through uncertainty.

How to Accumulate Bitcoin on KuCoin for a Long-Term 2030 Strategy

Investors preparing for a multi-year Bitcoin thesis should focus on process quality rather than short-term forecasting. A practical implementation framework may include:

Step 1: Define a target portfolio allocation rather than a target number of coins.

Step 2: Select an accumulation schedule using DCA, tranche execution, or a hybrid model.

Step 3: Establish custody rules before position size becomes meaningful.

Step 4: Track cost basis and maintain records continuously.

Step 5: Revisit probability assumptions periodically rather than reacting to headlines.

New users can now register at KuCoin and Get Up to 11,000 USDT in New User Rewards.

Conclusion

Bitcoin accumulation is ultimately a portfolio construction decision rather than a price prediction exercise. Although long-term forecasts toward 2030 remain uncertain, investors do not need certainty to build a rational strategy. What matters more is defining how capital will be deployed, how risk will be managed, and how decisions will be maintained across changing market conditions.

A disciplined accumulation plan combines structured entries, explicit allocation rules, operational security, and realistic expectations around both upside and downside outcomes.

Investors who attempt to predict every cycle often underestimate execution risk. Investors who build systems around consistency and probability may be better positioned to remain invested long enough for compounding to work.

The central question therefore may not be whether Bitcoin reaches a specific target by 2030. It may be whether investors can maintain discipline long enough to participate if it does.

FAQs

What realistic price range should investors expect for Bitcoin by 2030, and how likely are different scenarios?

A practical expectation framework is approximately $90,000-$180,000 under bearish conditions, $180,000-$400,000 in a baseline environment, and $400,000-$800,000 or higher in an aggressive expansion scenario. The probability distribution behind each outcome is generally more important than selecting a single target.

What is Michael Saylor's Bitcoin prediction for 2030, and how should investors evaluate its credibility?

Michael Saylor has publicly maintained extremely bullish long-term expectations for Bitcoin. Investors should treat these projections as directional viewpoints rather than valuation anchors and compare them against adoption assumptions, liquidity conditions, and portfolio objectives.

How much Bitcoin would I need to hold today to reach $1 million by 2030 under conservative, baseline, and bullish scenarios?

At a future BTC price of $200,000, approximately 5 BTC would represent $1 million. At $400,000, approximately 2.5 BTC would be required. At $800,000, approximately 1.25 BTC would achieve the same outcome. Actual allocation decisions should remain portfolio-driven.

How can investors hedge downside risk while continuing a long-term accumulation plan?

Partial hedging approaches such as protective puts, collars, and measured futures overlays may reduce volatility without abandoning accumulation schedules. Hedging should support long-term ownership rather than replace it.

Are ETF approvals and institutional flows likely to materially affect Bitcoin's price trajectory before 2030?

Institutional flows may become one of the most influential variables because incremental allocations from large capital pools can materially affect a limited liquid supply base. However, flows should be evaluated alongside macro liquidity and long-term holder behavior rather than in isolation.