The Future of RWAs: How Ripple and JPMorgan Just Revolutionized Treasury Redemptions

2026/05/08 17:48:02

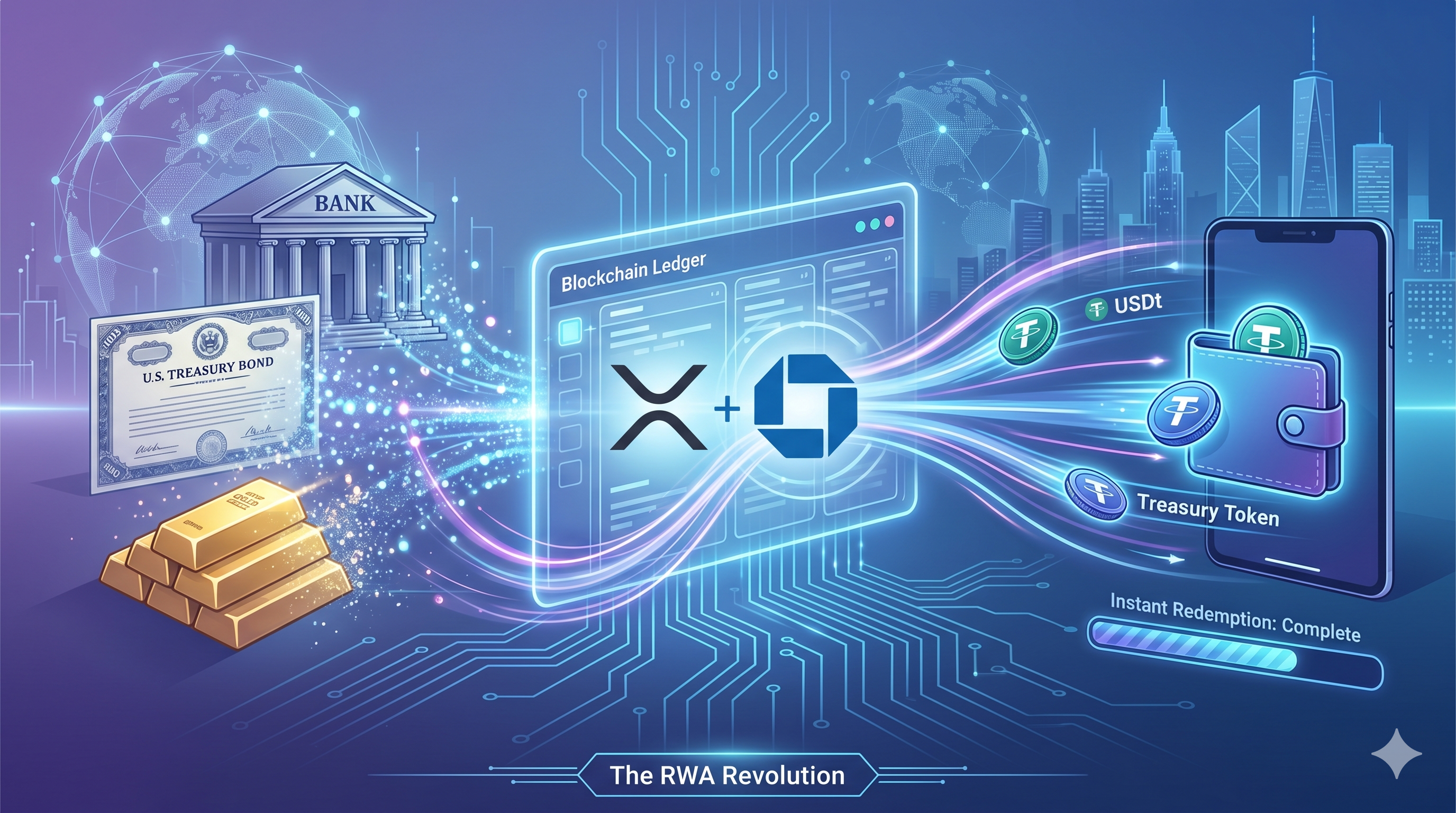

Did you know that settling a cross-border transaction involving U.S. Treasuries typically takes one to three business days? As of May 6, 2026, that traditional "T+2" model was effectively dismantled in under five seconds. Ripple, JPMorgan (via its Kinexys platform), Mastercard, and Ondo Finance have successfully executed the first-ever cross-border, interbank redemption of a tokenized U.S. Treasury fund using both public and private blockchain rails.

This isn't just another pilot; it is the birth of a 24/7 global financial system where billion-dollar liquidity moves at the speed of the internet. By integrating the XRP Ledger (XRPL) with JPMorgan’s regulated settlement infrastructure, these giants have proven that public blockchains can handle institutional-grade finance without sacrificing regulatory compliance. This breakthrough solves the "redemption bottleneck" that has long plagued Real World Assets (RWAs), allowing for near-instant conversion of tokenized assets into fiat currency across international borders, even when traditional banks are closed.

Key Takeaways

-

Instant Liquidity: The pilot settled tokenized U.S. Treasury redemptions in under five seconds, eliminating the standard multi-day waiting period.

-

Hybrid Infrastructure: The transaction successfully linked the public XRP Ledger with JPMorgan’s Kinexys (formerly Onyx) and Mastercard’s Multi-Token Network (MTN).

-

24/7 Operations: This milestone marks the first time cross-border interbank settlements for tokenized assets occurred outside traditional banking hours.

-

Market Growth: The tokenized RWA market (excluding stablecoins) has surged to over $31.1 billion as of May 2026, a massive leap from $14.1 billion at the start of the year.

-

Institutional Credibility: The participation of the world’s largest bank (JPMorgan) and a global payment leader (Mastercard) validates the XRPL as a premier venue for RWA issuance and settlement.

The 5-Second Settlement: How the Ripple-JPMorgan Collaboration Works

The Ripple and JPMorgan pilot successfully bridged the gap between decentralized ledgers and regulated banking by creating a unified transaction flow. Traditionally, tokenized assets existed in "silos"—you could trade them on-chain, but moving the resulting fiat to a bank account required manual intervention and traditional wire systems. This new model automates the entire sequence, ensuring that the asset leg and the cash leg of a trade happen almost simultaneously.

The Anatomy of a Modern Redemption

The process begins on the XRP Ledger, where Ripple initiates a redemption of its holdings in Ondo Finance’s OUSG (tokenized short-term U.S. Treasuries).

-

The Asset Leg: The XRPL processes the token transfer in approximately three to five seconds, notifying Ondo Finance of the redemption.

-

The Messaging Layer: Mastercard’s Multi-Token Network (MTN) acts as the bridge, transmitting payment instructions from the blockchain to the banking world.

-

The Cash Leg: JPMorgan’s Kinexys platform receives the instruction and immediately debits Ondo’s blockchain deposit account, delivering U.S. Dollars to Ripple’s bank account in Singapore.

Breaking the "Banking Hours" Barrier

One of the most significant aspects of this 2026 breakthrough is its independence from the legacy financial calendar. Because the XRP Ledger and Kinexys operate 24/7, the parties were able to settle the transaction during hours when the Federal Reserve’s Fedwire and other correspondent banking systems were offline. For institutional treasurers, this means no longer having to maintain massive "nostro/vostro" liquidity buffers in different time zones to cover settlement delays.

RWA Market Snapshot: The $31 Billion Milestone

The RWA sector is no longer a "niche" experiment; it is the fastest-growing segment in the cryptocurrency market in 2026. According to data from RWA.xyz and DeFiLlama as of early May 2026, the total value of tokenized real-world assets has eclipsed $31.1 billion. This represents a staggering 120% increase in just five months, driven by institutional hunger for yield-bearing assets on-chain.

Dominance of Tokenized Treasuries

Tokenized U.S. Treasury products, such as Ondo's OUSG and BlackRock’s BUIDL, now account for roughly $15.24 billion of the total market. These assets serve as a "risk-free" yield source for DAOs, hedge funds, and corporate treasuries. The Ripple-JPMorgan pilot is particularly vital here because it addresses the number one concern of these investors: exit liquidity. If you can't get your cash back instantly when the market moves, the asset is less valuable. By proving sub-5-second redemptions, these firms have effectively made tokenized Treasuries as liquid as cash.

The Rise of Commodity and Equity Tokenization

While Treasuries lead the pack, other asset classes are following suit. Tokenized gold and commodities have reached $7.3 billion in market capitalization as of April 2026, while tokenized stocks are approaching the $1 billion mark. The trend is clear: institutions are systematically moving the global ledger of ownership onto the blockchain.

| Asset Class | Market Cap (May 2026) | Growth Since Jan 2026 |

| Tokenized U.S. Treasuries | $15.24 Billion | 0.58 |

| Tokenized Commodities (Gold) | $7.30 Billion | 0.42 |

| Private Credit | $4.20 Billion | 0.15 |

| Tokenized Equities | $0.96 Billion | 1.26 |

| Total RWA (excl. Stablecoins) | $31.10 Billion | 1.2 |

Why Ripple and the XRP Ledger are Winning the RWA Race

The XRP Ledger has emerged as a primary infrastructure layer for RWAs in 2026 because of its native support for asset issuance and high throughput. While Ethereum still holds the majority of RWA liquidity, the XRPL has captured approximately 63% of the tokenized Treasury supply in certain institutional categories. This shift is due to the ledger's "Institutional-First" design, which includes built-in compliance tools like "freeze" and "clawback" capabilities that banks require.

Historically, Ripple was known primarily for XRP-based cross-border payments. However, the senior leadership, including RippleX SVP Markus Infanger, has pivoted the company to focus on "Unified Flows." The goal is to ensure that a tokenized asset transfer and its fiat settlement are no longer two separate events. The 2026 pilot with JPMorgan proves that Ripple's infrastructure can serve as the "settlement rail" for the world's most valuable assets, not just for moving money, but for redeeming it.

JPMorgan's rebranding of Onyx to Kinexys in late 2025 signaled a new era where the bank is comfortable interfacing with public chains. Kinexys provides the "Regulatory Wrapper" that allows a bank to interact with the XRP Ledger without violating KYC (Know Your Customer) or AML (Anti-Money Laundering) rules. This hybrid approach—public ledger for speed, private ledger for compliance—is becoming the industry standard.

Future Outlook: The Death of T+2?

The successful pilot between Ripple and JPMorgan suggests that the traditional "T+2" settlement model is entering its final days. In a world where the New York Stock Exchange and Nasdaq are both building 24/7 tokenized securities platforms, the expectation for "instant" is becoming universal.

By eliminating the two-day settlement delay, trillions of dollars in "settlement risk" capital can be freed up. Banks will no longer need to keep billions of dollars sitting idle in accounts across the globe to facilitate trades. Instead, that capital can be deployed back into the market, potentially lowering costs for consumers and increasing efficiency for enterprises.

Despite the success of the 2026 pilot, challenges remain. The International Monetary Fund (IMF) recently warned that tokenization could shift risks from traditional banking systems to smart contract code. Furthermore, "Shark Tank" investor Kevin O'Leary noted at Consensus Miami 2026 that while the tech is ready, massive institutional capital is still waiting for comprehensive U.S. market structure legislation to be finalized.

Exploring the Next Wave of RWAs on KuCoin

As the bridge between traditional finance and blockchain becomes seamless, the opportunity to participate in this $31 billion revolution is no longer reserved for banking giants like JPMorgan. Platforms like KuCoin are at the forefront of this shift, offering users a front-row seat to the tokenization of everything. Whether you are looking to trade the tokens powering these new settlement rails or exploring emerging RWA projects, the landscape is evolving faster than ever. Are you ready to move beyond traditional market hours and explore a 24/7 financial future? The tools to navigate this high-speed market are already here, and the next breakthrough could be just a trade away.

💡Tips: New to crypto? KuCoin's Knowledge Base has everything you need to get started.

Conclusion

The collaboration between Ripple, JPMorgan, Mastercard, and Ondo Finance in May 2026 represents a tectonic shift in the global financial landscape. By settling tokenized U.S. Treasury redemptions in under five seconds across international borders, these institutions have effectively proven that the "T+2" settlement model is obsolete. The fusion of the public XRP Ledger with regulated interbank rails like Kinexys demonstrates a viable path forward for institutional blockchain adoption—one that balances the transparency and speed of decentralized tech with the rigorous standards of global banking.

As the RWA market soars toward a $31.1 billion valuation, the focus is shifting from simple tokenization to the complex plumbing of redemptions and liquidity. The ability to move value instantly, 24/7, and across different currencies without manual delays is the ultimate "holy grail" of finance. While regulatory hurdles still exist, the 2026 pilot has laid the groundwork for a future where every asset—from government bonds to real estate—is tradeable and redeemable with a single click. We are witnessing the transition from a world of "siloed" money to a truly unified, global internet of value.

FAQs

What is the "redemption bottleneck" in RWA tokenization?

The redemption bottleneck refers to the delay and complexity of converting a tokenized asset (like a digital Treasury bill) back into fiat currency (like USD in a bank account). While the blockchain part happens instantly, the "off-ramp" into the traditional banking system usually takes days due to limited banking hours and manual wire transfers.

Why did JPMorgan change Onyx to Kinexys?

JPMorgan rebranded Onyx to Kinexys to reflect its evolution from a private research project into a functional, interbank settlement platform. Kinexys is designed to provide the regulated infrastructure needed for the bank to safely interact with public blockchains and external financial networks.

Is the XRP Ledger (XRPL) a private or public blockchain?

The XRP Ledger is a public, decentralized blockchain. In the 2026 pilot, it was used as the public "asset leg" of the transaction, where the tokenized Treasuries were held and redeemed, proving that institutions can use public ledgers for high-value transactions.

What role did Mastercard play in the Treasury redemption pilot?

Mastercard provided the Multi-Token Network (MTN), which served as the "messaging layer." It transmitted the data and settlement instructions from the XRP Ledger to JPMorgan’s banking system, ensuring that the blockchain and the bank were "speaking the same language."

How does 24/7 settlement reduce "settlement risk"?

Settlement risk is the danger that one party in a trade fails to deliver the asset or the cash during the multi-day "T+2" waiting period. By settling the entire transaction in five seconds, the window of time for something to go wrong—such as a bank failure or market crash—is almost entirely eliminated.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency investments carry significant risk. Always conduct your own research before trading.