Will Trump Accounts Sustain the Bullish Trend in the US Stock Market in 2026 and Beyond?

2026/07/06 11:51:00

Introduction

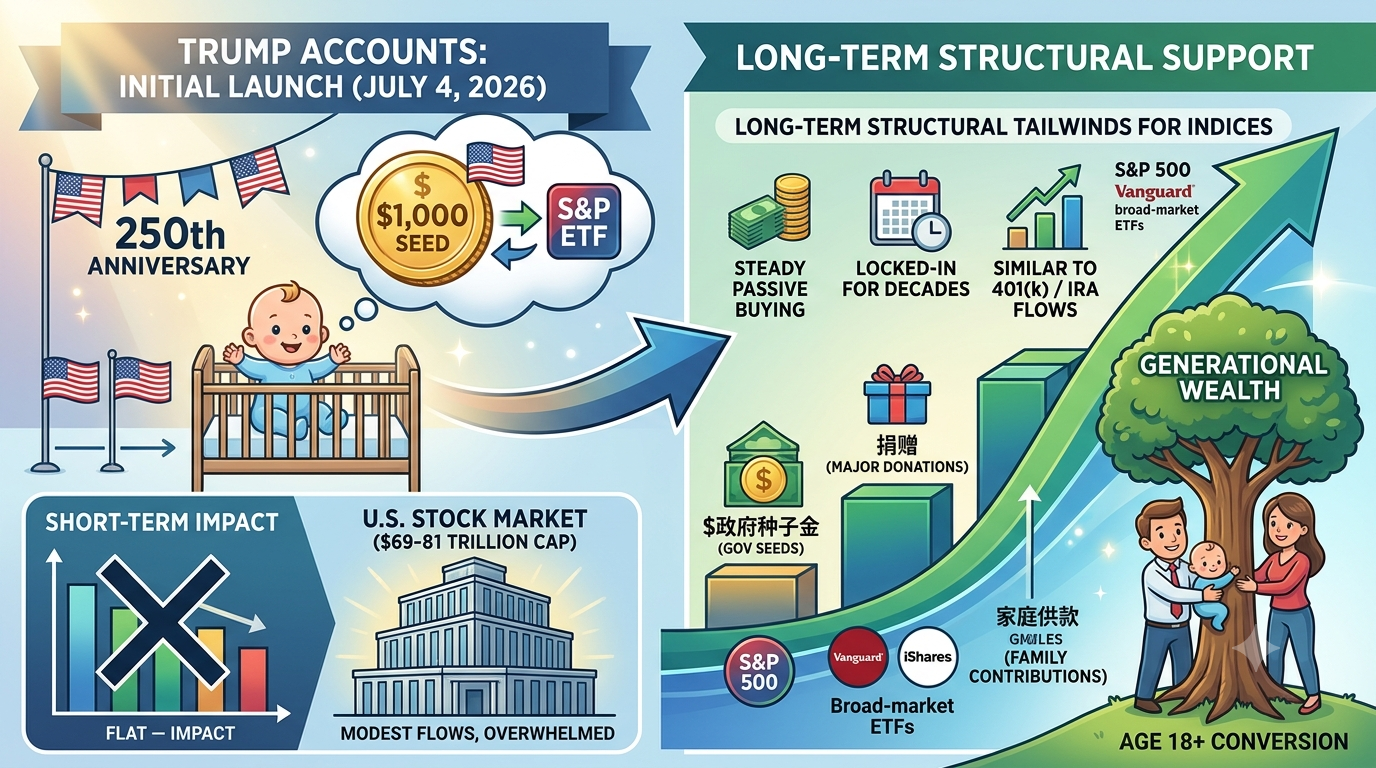

On July 4, 2026—America’s 250th anniversary—the U.S. Treasury launched Trump Accounts, depositing $1,000 seed funding into eligible newborns’ accounts and automatically investing it in low-cost S&P 500 ETFs. Over 6 million accounts have already been opened nationwide.

Trump Accounts will not drive a significant new bullish surge in the US stock market in the short term. Their scale remains modest relative to the $50–80 trillion U.S. equity market capitalization. Long-term, however, they introduce steady, locked-in passive buying pressure on broad indices, offering mild structural support similar to 401(k) and IRA flows.

What Are Trump Accounts and How Do They Invest?

Trump Accounts function as tax-advantaged, IRA-like vehicles (officially 530A accounts) for children under 18. Key rules, per Treasury and IRS details as of July 2026:

-

Eligibility: Any U.S. child under 18 with a Social Security number can have an account. A $1,000 government seed applies only to those born 2025–2028.

-

Contributions: Up to $5,000 annually total from parents, relatives, and others; employers can add up to $2,500 (tax-advantaged). Funds lock until age 18.

-

Investments: Restricted to low-cost U.S. equity index ETFs (expense ratio ≤0.1%). Default is State Street SPDR Portfolio S&P 500 ETF (SPYM, ~0.02% fee). Other options include Vanguard and iShares broad-market funds.

-

Growth Projection: Treasury cites historical S&P 500 ~10.5% annualized returns, projecting the $1,000 seed could grow substantially by retirement.

Accounts opened rapidly, exceeding 6 million by early July 2026, with initial seed money targeting ~1.4 million newborns for roughly $1.4 billion in immediate inflows.

Estimating Capital Inflows from Trump Accounts

Initial and short-term inflows remain small relative to market scale. Government seeds total ~$1.4 billion for qualifying newborns. Philanthropic donations, such as the Dell family’s $6.25 billion pledge (distributing ~$250 per qualifying child in targeted groups), add tens of billions more over time.

Analysts estimate first-year inflows (seeds + initial contributions + major donations) in the $20–80 billion range conservatively, potentially reaching $300–500 billion optimistically with high participation. Annual ongoing contributions could add $100–300 billion if half of accounts receive average $2,000–3,000 yearly, though actual uptake will vary.

These figures pale against U.S. market size. S&P 500 market cap exceeds $58–67 trillion as of mid-2026, with total U.S. equity market capitalization around $69–81 trillion. Daily trading volume often reaches hundreds of billions, dwarfing incremental Trump Account flows.

Funds buy broad indices passively and gradually, avoiding concentrated impact on individual stocks.

Short-Term Market Impact: Minimal and Overwhelmed by Other Factors

Trump Accounts will not meaningfully alter near-term US stock market direction. The $14 billion seed plus early additions represent a tiny fraction of market cap—comparable to routine ETF rebalancing or single-day volatility.

Near-term sentiment hinges more on macroeconomic drivers. The June 2026 CPI release (due July 14) and Fed Chair Warsh’s semi-annual testimony will dominate. Warsh has emphasized price stability as the Fed’s top priority, with rates held at 3.5–3.75% in June amid sticky inflation above 3%. Higher-than-expected CPI could raise hike risks; lower readings might ease pressure.

Corporate earnings, tariffs, geopolitical events, and consumer spending continue to outweigh this new program’s influence in 2026.

Long-Term Structural Support for Indices

Over years and decades, Trump Accounts provide mild positive tailwinds for broad U.S. equities. Locked funds create consistent, long-horizon buying—mirroring how automatic retirement contributions have supported bull markets by adding durable demand during dips.

This “buy-and-hold” demand benefits S&P 500 and total-market ETFs disproportionately. It fosters a “stakeholder generation” tied to market performance, potentially increasing overall equity ownership culture. However, realization depends on sustained participation rates, contribution levels, and additional philanthropy.

Limitations include:

-

Sub-maximal contributions from many families.

-

Gradual deployment rather than lump sums.

-

Dominance of larger forces like Fed policy and earnings growth.

Should You Trade US Stocks on KuCoin?

KuCoin provides access to a broad range of not only crypto markets, but also stock markets. Now users can also participate in KuCoin's Campaign of Trading US Stock Perps:

-

After complete simple trading missions, users may unlock 100,000 USDT prize pool rewards in TSLA, AAPL, or GOOGL.

Conclusion

Trump Accounts launched with fanfare on July 4, 2026, channeling initial billions into S&P 500 ETFs and promising generational wealth through market participation. However, their immediate capital impact stays negligible against the multi-trillion-dollar U.S. stock market. Short-term bullish continuation depends far more on Fed decisions, inflation data, and corporate fundamentals than on these new accounts.

Longer-term, they add steady passive demand and promote equity ownership from a young age, delivering mild structural support—especially valuable in downturns. Success hinges on high participation and supplementary donations. This initiative blends policy innovation with capitalist incentives, binding future generations to stock market outcomes without guaranteeing outsized returns or market dominance.

Investors should monitor actual contribution rates and flows in coming quarters. Trump Accounts represent a positive but incremental development in a market driven primarily by macro forces, earnings, and policy. They enhance the investment landscape without fundamentally reshaping near-term trends.

FAQs

Can non-U.S. citizens open Trump Accounts?

No. Eligibility requires U.S. citizenship or qualifying status with a valid Social Security number for the child.

What happens to a Trump Account when the child turns 18?

It converts to a traditional IRA, with standard rules applying thereafter and funds becoming accessible per IRA guidelines.

Are contributions to Trump Accounts tax-deductible?

Generally no for individuals, though employer contributions offer tax advantages. Growth is tax-deferred.

Can money be withdrawn early from a Trump Account?

No, funds are locked until age 18, with penalties likely applying for early access similar to retirement accounts.

How do Trump Accounts compare to 529 college savings plans?

Trump Accounts focus on long-term retirement-style equity investing with lock-up, while 529 plans target education expenses with different tax benefits and withdrawal rules.