Will MU Stock Price Rise or Plunge After June 24 Earnings?

2026/06/22 15:32:00

Introduction

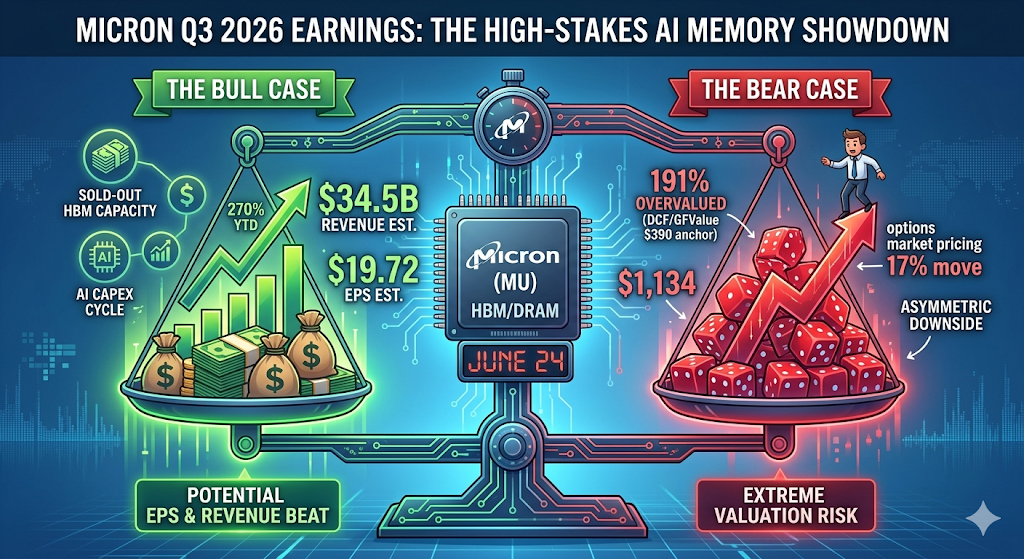

Micron Technology (MU) heads into its June 24, 2026 fiscal Q3 earnings release sitting at a record $1,133.99 — up more than 270% year-to-date — with the options market pricing a 17% one-day move in either direction.

Yet MU's stock has already run far past most Wall Street targets, meaning the real question is not whether Micron beats — it almost certainly will — but whether the beat is large enough to justify a valuation that traditional DCF models peg closer to $300 in fair value. This article breaks down the bull case, the bear case, the key technical levels, and what traders should actually watch on June 24.

What Are Analysts Expecting From Micron's June 24 Earnings?

Wall Street is bracing for a record quarter, but estimates vary widely. Micron Technology reports fiscal third-quarter 2026 results after the close on June 24, with analysts forecasting earnings of $19.72 per share on revenue of $34.52 billion, with EPS estimates spanning a wide range from $7.53 to $24.08 and revenue projections stretching from $19.68 billion to $40.07 billion.

That spread is unusual. According to Alphastreet, the EPS consensus has climbed 3.1% over the past 30 days from $19.13, and the 90-day trajectory reveals even more dramatic optimism, with the consensus rising 68.1% from $11.73 three months ago. In other words, the bar has been raised — repeatedly — in the weeks leading up to the print.

For context, Micron's last quarter set the tone. Q2 beat expectations with $23.86 billion in revenue and $12.20 non-GAAP EPS, up 196% year-over-year. The company has now strung together multiple consecutive beats, and management's own Q3 guidance is even more aggressive than the Street's: company guidance points to $33.5 billion ± $750 million in revenue, with gross margins near 81% and non-GAAP EPS of $19.15 ± $0.40.

Why Has MU Stock Surged to $1,134?

Micron's rally is entirely an HBM (High-Bandwidth Memory) story, layered on top of a broader AI infrastructure capex cycle. According to TradingKey, Micron is transitioning from a commodity provider to a pivotal AI infrastructure player, benefiting from its HBM oligopoly and strong demand from hyperscalers.

Three forces have driven the parabolic move:

1. HBM capacity is sold out. High-bandwidth memory capacity is sold out through calendar year 2026, and the company has guided to an HBM annualized revenue run-rate of roughly $8 billion.

2. Price targets are being lifted aggressively. RBC Capital elevated its target from $525 to $1,200 on June 15 based on AI demand, while C.J. Muse at Cantor Fitzgerald sits at $1,500 as the Street's most aggressive target.

3. The full-year earnings ramp is staggering. For full fiscal 2026, analysts project EPS of $57.71, up 651% from $7.68 in fiscal 2025, with further growth to $97.77 expected in fiscal 2027.

The result: Micron has crossed the US$1 trillion market cap mark, with AI-driven demand for its HBM, DRAM and NAND products and record Q2 2026 results that included revenue of US$24 billion and sharply higher net income and margins.

Is Micron Priced for Perfection Heading Into June 24?

Yes — and that is the single most important risk factor for traders right now. Even with a likely beat, MU's valuation leaves almost no margin of safety. According to TradingKey, Micron trades near record highs at $1,133.99 with a trailing P/E ratio above 50x, which is significantly higher than its 5-year median of 20.72x, and is estimated by GuruFocus to be 191% overvalued compared to its GF Value of $389.69, while aggressive consensus expectations of $34.38 billion in revenue and $19.72 EPS leave no margin of safety, meaning any in-line results or slightly cautious guidance could trigger a sharp post-earnings selloff.

That GF Value figure — roughly $390 — aligns closely with traditional DCF models, which place Micron's fair value near $300–$400 per share. The current price already embeds multiple years of flawless execution.

What Does "Priced for Perfection" Mean for Traders?

It means good news is already in the stock. Per Phemex's analysis, Micron closed at an all-time high of $1,133 on June 18, a fresh record after a +11% run, and the company reports fiscal Q3 results on June 24 covering the March-May 2026 quarter. The options market is pricing a roughly 17% move in either direction off the print. A stock sitting at a record high with that much implied volatility has almost no room to disappoint.

Seeking Alpha goes further, warning of asymmetric downside: Micron faces asymmetric downside risk ahead of June 24 earnings due to extreme bullish call option positioning. Options premiums are highly elevated, with 10-day implied volatility near 120%, making both calls and puts expensive and hard to profit from. MU's call wall at $1,200 creates significant resistance; failure to break above could trigger rapid value loss for call holders. Implied volatility is likely to collapse post-earnings, potentially causing sharp declines in option values and exposing MU to 12–21% downside toward $970–$900 support.

What Are the Key Price Levels to Watch After Earnings?

Based on options positioning, gamma exposure, and recent technical structure, traders should monitor a clearly defined set of levels.

|

Scenario

|

Price Target

|

Driver

|

|

Bullish beat + raised guidance

|

~$1,200

|

Call wall resistance breakout

|

|

Mild beat / in-line guidance

|

$1,100

|

First technical support

|

|

Cautious guidance / supply concerns

|

$1,050

|

Second support, prior gamma flip zone

|

|

"Sell-the-news" capitulation

|

$970–$900

|

Implied vol collapse, post-earnings unwind

|

The options-derived structure is unusually concentrated. According to moomoo's options desk analysis, Micron's gamma profile for the June 26 weekly expiry has the stock trading deep in positive gamma territory at $1,133.99, comfortably above the $984.40 gamma flip with a towering Call Wall at $1050 already breached, leaving dealers long gamma in a stabilizing posture that should dampen volatility but cap explosive upside as market makers sell into strength.

Translation: dealers are positioned to suppress upside above $1,200 while providing only limited cushion below $1,050. The $984 gamma flip is the line where dealer behavior reverses and selling can accelerate.

What Should Investors Actually Listen For on the Call?

The numbers will likely beat. What matters is forward guidance and HBM commentary. According to Goldman Sachs research summarized by TradingKey, tight DRAM supply and better visibility of margins are the two important themes for Q3.

Three specific items will move the stock:

1. HBM4 allocation and pricing. Key monitorables include forward-looking HBM4 allocations, fiscal 2026 guidance, and sustainability of gross margins amid rising CAPEX and intensifying competition from SK Hynix and Samsung.

2. Capex trajectory. Per moomoo, last quarter Micron projected fiscal 2026 capex above $25 billion and fiscal Q3 capex of approximately $7 billion, while also saying fiscal 2027 capex should step up meaningfully to support HBM and DRAM investments. That is the right move if demand remains structurally above supply, but it is also the classic risk in memory cycles — tight supply leads to high margins, high margins trigger spending, and spending eventually creates new supply.

3. Pricing commentary. As Phemex notes, listen for explicit remarks on HBM, DRAM, and NAND contract pricing — sold-out capacity only matters if prices hold, so direct confirmation that pricing is firm or rising is what separates a structural story from a volume story.

How Strong Is Micron's Competitive Position vs. SK Hynix and Samsung?

Micron is the smallest of the HBM "Big Three," and the competitive picture is shifting quickly. According to a May 2026 snapshot from Presenc AI, HBM market share in 2026 splits roughly SK hynix 50-62%, Samsung 25-40%, Micron 5-20%, with HBM3E dominating shipments and HBM4 ramping.

On Nvidia's next-generation platform specifically, on NVIDIA's HBM4 allocation, SK hynix gets mid-50%, Samsung mid-20%, Micron about 20%. Notably, Nvidia has certified Micron, Samsung and SK Hynix to supply HBM4 for its Vera Rubin AI platform, reinforcing Micron's role in high-end AI memory even as Nvidia also deepens collaboration with SK Hynix.

Are Competitors Catching Up?

Yes, and aggressively. SK hynix has completed development of HBM4, claiming a 40% improvement in power efficiency and data rates of 10 Gbps, with mass production to follow once qualification is complete. Micron meanwhile has begun shipping HBM4 samples rated at up to 11 Gbps and is working with foundry partners on future HBM4E products.

Historically, memory remains a cyclical commodity business. The key tension for investors is the contrast between very strong current fundamentals backed by long-term contracts and a memory market that still has a history of sharp cycles, rising competition from SK Hynix and Samsung, and concerns that demand could cool after 2027. Memory stocks have historically peaked 3–8 months before pricing peaks — a cycle-timing risk that no amount of AI narrative can eliminate.

What Are the Biggest Risks if Earnings Disappoint?

Three risks dominate the bear case.

Demand normalization. If hyperscalers continue to purchase less or train AI models more efficiently than anticipated, HBM demand may weaken before Micron's new capacity is available.

Capex-driven oversupply. DRAM capacity additions are now increasingly visible, including first wafer output from the first Idaho fab in mid-calendar 2027. Once new fabs come online, the supply tightness that drove margins to 81% will inevitably ease.

Valuation reset. The stock's $1 trillion valuation reflects expectations that the market has reached a new era in which demand for AI has ended the memorable up-and-down run of memory. If that assumption breaks even slightly, the multiple compression alone could drive a 20%+ correction independent of fundamentals.

How to Trade US Stocks and Bitcoin on KuCoin

KuCoin also offers exposure to trading US stock perps — meaning you can rebalance between crypto and US equity narratives without leaving the platform. Combined with the security infrastructure of a tier-one global exchange, KuCoin is positioned for investors who want flexibility across both asset classes.

Conclusion

Micron's June 24 earnings release sits at the intersection of a near-certain beat and a near-impossible valuation. The numbers themselves are almost a foregone conclusion: consensus calls for roughly $19.72 EPS on $34.5 billion in revenue, with management's own guide pointing to record gross margins above 80%. Yet the stock at $1,134 has already absorbed every visible positive, leaving forward guidance and HBM commentary as the true catalysts.

The most likely outcomes split into two paths. A bullish print with raised HBM4 framework and confirmed pricing strength can push MU toward the $1,200 call wall, though dealer positioning may cap further upside. A merely in-line result, or any cautious guidance language, opens the door to a "sell-the-news" decline toward $1,100, then $1,050, with worst-case implied-vol-collapse scenarios extending toward $970–$900. For traders, the asymmetry currently favors caution: the upside is gated by positioning, while the downside is gated only by sentiment. Watch the guide, not the headline.

FAQs

1. When exactly does Micron report Q3 fiscal 2026 earnings?

Micron Technology will release earnings on June 24, 2026, after the close (confirmed). The conference call typically follows about 30 minutes after the press release.

2. What is the options market's implied move for MU around earnings?

The options market is pricing roughly a 17% move in either direction. With the market pricing roughly 17%, an at-the-money straddle bought before the print needs MU to move more than that 17% to break even.

3. Why do some analysts think MU is overvalued despite strong earnings growth?

Traditional valuation models — DCF, P/E reversion to historical memory cycle multiples, and asset-based approaches — place Micron's fair value between roughly $300 and $400. GuruFocus pegs the GF Value at $389.69, implying the stock is trading more than 190% above that anchor. The premium reflects an assumption that AI demand has structurally broken the historic memory cycle, which remains unproven.