Kelly Criterion Explained: How Professional Traders Use Math to Maximize Growth

Modern trading is no longer just about finding good entries and exits. Position sizing has become one of the most important factors in determining long-term success. Many traders fail not because their strategy is wrong, but because they risk too much or too little on each trade. This is where mathematical frameworks like the Kelly Criterion come into play. Originally developed in information theory, the Kelly Criterion has found strong application in finance and trading. It provides a formula to determine the optimal percentage of capital to risk on a trade based on probability and expected returns.

While the concept may appear technical, its goal is simple: maximize long-term capital growth while minimizing the risk of ruin. Professional traders and quantitative funds use variations of this model to manage risk more effectively. In a market where uncertainty is constant, having a structured approach to position sizing offers a significant advantage. The Kelly Criterion stands out because it is grounded in probability rather than intuition, making it a powerful tool for disciplined trading.

Thesis statement

The Kelly Criterion remains one of the most effective mathematical tools for traders because it systematically determines optimal position sizing based on probability, balancing growth and risk in uncertain markets.

The Origin Story: From Information Theory to Trading Floors

The Kelly Criterion was first introduced in 1956 by John L. Kelly Jr., a researcher working at Bell Labs. His work was not initially intended for financial markets but for improving signal transmission over noisy communication channels. The core idea was to maximize the rate at which information could be transmitted efficiently. Over time, mathematicians and economists realized that the same principle could be applied to capital growth. The concept was later adopted by gamblers and investors who recognized its potential in optimizing bet sizes. By the 1980s and 1990s, hedge funds and professional traders began integrating Kelly-based models into their risk management systems. The appeal of the Kelly Criterion lies in its scientific foundation. It does not rely on guesswork or subjective judgment.

Instead, it uses probability and expected outcomes to determine how much capital should be allocated to a given opportunity. This makes it particularly valuable in modern trading, where decisions must be made quickly and consistently. Today, the Kelly Criterion is widely discussed in quantitative finance and is considered a cornerstone of optimal betting theory.

Breaking Down the Formula Behind the Kelly Criterion

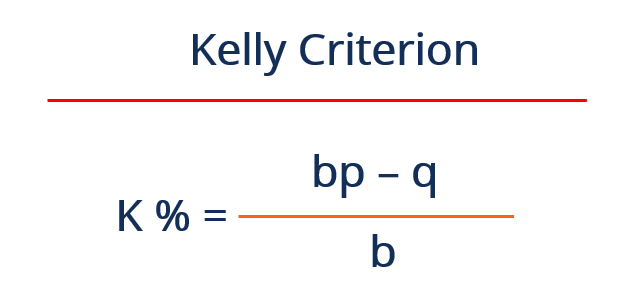

The Kelly Criterion is expressed through a simple formula that determines the optimal fraction of capital to risk on a trade. The formula takes into account the probability of winning, the probability of losing, and the payoff ratio. It can be written as: f = (bp − q) / b, where f represents the fraction of capital to risk, b is the ratio of profit to loss, p is the probability of winning, and q is the probability of losing. While the equation may seem straightforward, its implications are powerful. It provides a precise answer to a question that many traders struggle with: how much should I risk on this trade?

By incorporating both probability and payoff, the formula ensures that position sizing is aligned with the quality of the opportunity. A trade with a higher probability of success or a better reward-to-risk ratio will justify a larger allocation of capital. Conversely, weaker setups result in smaller positions. This dynamic adjustment is what makes the Kelly Criterion so effective. It ensures that capital is deployed efficiently, maximizing growth potential while controlling risk.

Why Position Sizing Matters More Than Entry Timing

Many traders focus heavily on finding the perfect entry point. While timing is important, position sizing often has a greater impact on long-term performance. Even a profitable strategy can fail if position sizes are too large or inconsistent. The Kelly Criterion addresses this issue by providing a structured approach to sizing trades. It ensures that risk is proportional to the quality of the opportunity. This reduces the likelihood of significant losses that can damage a trading account. Professional traders understand that preserving capital is just as important as generating returns.

By using a mathematical framework, they can avoid the common pitfalls of overconfidence and emotional decision-making. The Kelly Criterion also helps maintain consistency. Instead of adjusting position sizes based on intuition, traders rely on calculated values. This leads to more stable performance over time. In volatile markets, where conditions can change rapidly, having a reliable method for position sizing becomes essential. The Kelly Criterion provides that reliability, making it a valuable tool for both individual traders and institutional investors.

Calculating a Real Trade Using the Kelly Formula

Understanding the Kelly Criterion becomes clearer when applied to a real example. Consider a trader who has a strategy with a 60 percent win rate. For each winning trade, the trader gains twice the amount risked, resulting in a payoff ratio of 2:1. Using the Kelly formula, the calculation becomes: f = (2 × 0.6 − 0.4) / 2. This simplifies to f = (1.2 − 0.4) / 2, which equals 0.4. This means the trader should risk 40 percent of their capital on each trade according to the full Kelly strategy.

While this may seem aggressive, it reflects the strength of the trading edge. In practice, most traders use a fraction of the Kelly value to reduce risk. For example, using half-Kelly would result in risking 20 percent of capital per trade. This adjustment helps manage drawdowns while still benefiting from the strategy’s edge. This example highlights how the Kelly Criterion translates theoretical probabilities into actionable decisions. It bridges the gap between analysis and execution, providing a clear guideline for capital allocation. By applying this method, traders can align their risk-taking with the statistical strength of their strategy.

The Growth Advantage: Maximizing Capital Over Time

One of the key benefits of the Kelly Criterion is its focus on long-term capital growth. The formula is designed to maximize the geometric growth rate of an investment portfolio. This means it prioritizes consistent compounding rather than short-term gains. Over time, this approach can lead to significantly higher returns compared to fixed position sizing methods. The reason lies in how capital is allocated.

By increasing position sizes when the edge is strong and reducing them when the edge is weak, the Kelly Criterion ensures that capital is used efficiently. This dynamic allocation allows traders to take full advantage of favorable conditions while protecting against losses. Studies in portfolio theory have shown that strategies based on Kelly principles can outperform traditional approaches in terms of growth rate.

However, this comes with increased volatility, which is why many traders adjust the formula to suit their risk tolerance. Despite this, the underlying principle remains powerful. By focusing on maximizing growth over time, the Kelly Criterion provides a framework for sustainable success in trading.

The Hidden Risk: Why Full Kelly Can Be Dangerous

While the Kelly Criterion offers a mathematically optimal solution, it is not without risks. One of the main concerns is the volatility associated with full Kelly position sizing. Risking the full recommended fraction can lead to significant drawdowns, especially during losing streaks. This is because the formula assumes that probabilities and outcomes are known with certainty. In reality, market conditions can change, and estimates may not always be accurate. Professional traders are aware of this limitation and often use a more conservative approach. By applying a fraction of the Kelly value, such as half or quarter Kelly, they reduce the impact of volatility.

This adjustment helps balance growth and risk, making the strategy more practical for real-world trading. The concept of “risk of ruin” is also important. Even with a positive edge, large position sizes can lead to substantial losses if the market behaves unexpectedly. Understanding these risks is essential for using the Kelly Criterion effectively. It is not a one-size-fits-all solution but a tool that must be adapted to individual circumstances.

Why Professional Traders Rarely Use Full Kelly

In theory, the full Kelly strategy maximizes growth. In practice, most professional traders avoid using it. The reason lies in the trade-off between growth and stability. Full Kelly can produce the highest returns over time, but it also introduces significant volatility. Large drawdowns can be psychologically challenging and difficult to recover from. Professional traders prioritize consistency and capital preservation.

By using a fraction of the Kelly value, they can achieve a more stable performance. This approach reduces the likelihood of large losses while still capturing the benefits of the strategy. It also allows for greater flexibility in managing risk. Traders can adjust their position sizes based on market conditions and confidence in their edge. This pragmatic approach reflects the realities of trading, where uncertainty is always present. The goal is not just to maximize returns but to survive and thrive over the long term. By scaling down the Kelly allocation, traders strike a balance between growth and risk management.

Comparing Kelly Criterion to Fixed Risk Strategies

Fixed risk strategies involve risking a constant percentage of capital on each trade, regardless of the setup. While this approach is simple and easy to implement, it does not account for variations in trade quality. The Kelly Criterion offers a more dynamic alternative. By adjusting position sizes based on probability and payoff, it ensures that capital is allocated more efficiently. This leads to better utilization of trading opportunities. Fixed risk strategies can be effective in maintaining consistency, but they may limit growth potential.

The Kelly Criterion, on the other hand, adapts to changing conditions. It increases exposure when the edge is strong and reduces it when the edge is weak. This flexibility can result in higher overall returns. However, it also requires accurate estimation of probabilities, which can be challenging. Each approach has its advantages and limitations. Professional traders often combine elements of both, using Kelly-based calculations to inform their risk management while maintaining a level of consistency in execution.

The Psychology Behind Trusting a Mathematical Model

Relying on a mathematical model for decision-making requires a shift in mindset. Many traders struggle to trust formulas over intuition. The Kelly Criterion challenges this by providing a clear, logical framework for position sizing. It removes the need for guesswork and replaces it with calculated decisions. This can be difficult at first, especially for traders who are used to discretionary approaches. However, those who adopt the model often find that it improves their discipline.

By following a structured system, they reduce the influence of emotions. This leads to more consistent performance over time. The psychological benefit of having a clear plan cannot be overstated. It provides confidence and reduces stress, particularly during periods of market volatility.

Trusting the Kelly Criterion requires understanding its principles and limitations. It is not about blindly following a formula but about using it as a guide. When combined with sound judgment, it becomes a powerful tool for managing risk and optimizing performance.

Applications Beyond Trading

The Kelly Criterion is not limited to financial markets. Its principles are used in various fields where decision-making under uncertainty is required. In sports betting, it helps determine optimal bet sizes based on probabilities and odds. In portfolio management, it guides asset allocation decisions. Even in business, similar concepts are applied to investment strategies and risk assessment.

The versatility of the Kelly Criterion lies in its foundation in probability theory. It can be adapted to different contexts where outcomes are uncertain. This broad applicability highlights its importance as a decision-making tool. In trading, it serves as a bridge between theory and practice.

By applying mathematical principles to real-world scenarios, it helps traders make more informed decisions. This cross-disciplinary relevance underscores the value of the Kelly Criterion. It is not just a trading strategy but a framework for optimizing outcomes in uncertain environments.

The Future of Kelly Criterion in Algorithmic Trading

As trading becomes increasingly automated, the role of mathematical models like the Kelly Criterion is expected to grow. Algorithmic trading systems rely on precise calculations to make decisions. The Kelly Criterion fits naturally into this framework. It provides a clear method for determining position sizes based on statistical inputs. Advances in data analysis and machine learning are enhancing the accuracy of these inputs. This allows for more precise estimation of probabilities and outcomes.

As a result, Kelly-based strategies are becoming more effective. Some trading systems now incorporate adaptive versions of the Kelly Criterion that adjust parameters in real time. This enables them to respond to changing market conditions more efficiently. The integration of technology is expanding the potential of the Kelly Criterion.

It is growing from a theoretical concept into a practical tool for modern trading. As markets continue to develop, the importance of structured, data-driven approaches is likely to increase. The Kelly Criterion is well positioned to remain a key component of this evolution.

FAQs

1. What is the Kelly Criterion in simple terms?

The Kelly Criterion is a mathematical formula used to determine how much of your capital to risk on a trade based on your probability of winning and the potential reward.

2. Why is the Kelly Criterion important for traders?

It helps traders maximize long-term growth while managing risk by adjusting position sizes according to the strength of their trading edge.

3. Is it safe to use the full Kelly percentage?

Using the full Kelly value can be risky due to high volatility. Most traders prefer using a fraction of it to reduce drawdowns.

4. Can beginners use the Kelly Criterion?

Yes, but it requires understanding probabilities and maintaining discipline. Many beginners start with simplified or fractional versions.

5. How do you calculate the Kelly percentage?

It is calculated using the formula f = (bp − q) / b, where variables represent probability and payoff ratios.

6. Does the Kelly Criterion guarantee profits?

No, it does not guarantee profits. It optimizes position sizing based on probabilities, but outcomes still depend on market conditions.

Disclaimer

This content is for informational purposes only and does not constitute investment advice. Cryptocurrency investments carry risk. Please do your own research (DYOR).