SpaceX Pre-IPO Crash Explained: Why Hyperliquid's Perp Fell 45% and Bitget's preSPCX Dropped 80% Before the IPO

2026/06/01 11:37:00

Introduction

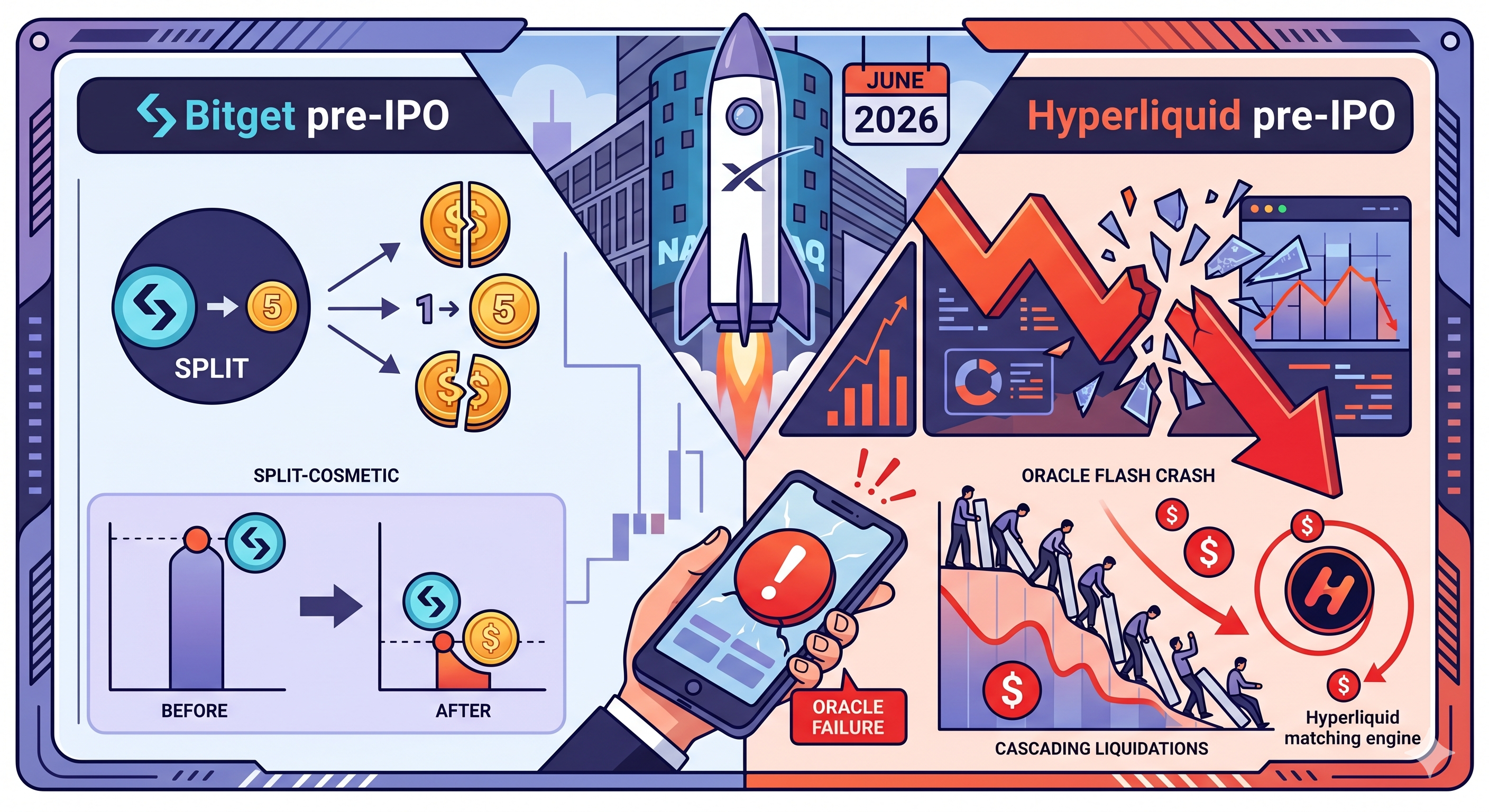

Less than two weeks before SpaceX's expected Nasdaq debut, its pre-IPO synthetic markets convulsed in a single overnight session — and over 400 retail traders paid the price. On May 28, 2026, Hyperliquid's SPACEX-USDH perpetual contract plunged from an open of $2,277 to a low of $1,254, a near-45% collapse within 30 minutes, liquidating 405 users across 1,393 positions and wiping $1.51 million in notional value. Hours earlier, the preSPCX/USDT spot pair on Bitget displayed a sudden 80% drop — a nominal price adjustment caused by a pre-announced 1:5 token split, not a fundamental crash.

The two events — one a technical adjustment, the other a real oracle failure — both expose how fragile pre-IPO synthetic markets become when leverage, thin liquidity, and off-chain data feeds collide right before a high-profile listing.

What Exactly Happened to SpaceX Pre-IPO Tokens on May 28, 2026?

Two unrelated incidents hit SpaceX pre-IPO products on the same day, but only one caused real losses. The Bitget preSPCX event was a mechanical token split, while the Hyperliquid SPACEX-USDH event was a genuine oracle-driven flash crash that liquidated retail traders.

According to PANews, on May 28, less than a month before SpaceX's anticipated Nasdaq listing, its pre-IPO assets experienced a series of "cliff-like crashes" overnight. The market read both moves as evidence of fragility, but the mechanics behind each were completely different.

The Bitget preSPCX 80% Drop: A Token Split, Not a Crash

The Bitget "crash" was a cosmetic price adjustment tied to SpaceX's own corporate action. According to Bitget's official announcement, the exchange rebranded preSPAX to preSPCX and implemented a 1:5 token split to align with SpaceX's official stock split, with each preSPAX token converting into five preSPCX tokens and the price per token adjusted accordingly — leaving the total value of user holdings unchanged except for market fluctuations.

A 1:5 split means the number of tokens held by an investor is multiplied by 5, so assuming total value remains constant, the price per token drops to one-fifth of the original — translating to a nominal 80% drop on the trading screen. No retail investor actually lost money from the split itself.

The Hyperliquid SPACEX-USDH 45% Flash Crash: An Oracle Disaster

The Hyperliquid event was the real disaster. According to Unchained, the SPACEX-USDH perpetual on Hyperliquid's Ventuals market crashed 45% after Notice.co's oracle mishandled SpaceX's 5-for-1 stock split, triggering liquidations across 405 users and 1,393 trades.

In effect, the same corporate action that Bitget handled cleanly through a planned token split was fed into Hyperliquid's pricing engine incorrectly — and the system responded by treating the apparent 80% drop as a real market move.

Why Did the Hyperliquid SPACEX Perpetual Fall 45% in 30 Minutes?

The Hyperliquid SPACEX-USDH contract fell 45% because a single faulty off-chain data point entered an oracle feed with no public reference price to correct it. The result was a cascading liquidation in a market that lacked the depth to absorb the move.

According to Ventuals' own statement, "the offchain data provider used as a component of the oracle price returned incorrect data, which caused the market's oracle and mark price to move dramatically".

The Oracle Failure Explained

Ventuals does not pull pricing from a public market — because there isn't one. According to Cryptonews.net, Ventuals lists the SpaceX token under HIP-3, Hyperliquid's builder-deployed perpetuals standard where third parties can spin up new perp tokens on its matching engine; because SpaceX is privately held and has no public price, Ventuals constructs its own oracle that blends a feed from private-markets vendor Notice with a two-hour moving average of the contract's mark price — with Notice's feed earning one-third weight and the Exponential Moving Average of Hyperliquid trading prices earning two-thirds weight.

When the Notice feed returned a bad number, both the oracle and mark price jolted lower, the contract collapsed inside the 20% downward price band Ventuals enforces relative to the oracle, then collapsed again as the oracle itself kept moving.

Hyperliquid's Safeguards Were Not Enough

Hyperliquid does have circuit-breaker logic, but it was overwhelmed. According to FinanceFeeds, Hyperliquid restricts mark price movements to a maximum 1% change per three-second update interval, but that safeguard did not prevent the cascading liquidation cycle once the faulty data entered the feed.

Why Do Pre-IPO Perpetual Contracts Have Structural Liquidity Problems?

Pre-IPO perpetuals are structurally fragile because they lack a public spot market anchor — meaning there is no deep, transparent reference price to stabilize them during shocks. This makes them fundamentally different from BTC or ETH perpetuals.

According to CoinDesk, unlike perpetual futures on Bitcoin or Ethereum, which anchor to deep, liquid spot markets, the SPACEX contract has no public price benchmark, with SpaceX shares trading only through private secondary markets gated to accredited investors.

What Does the SpaceX IPO Timeline Mean for These Markets?

The SpaceX IPO will eliminate the oracle problem for SPACEX synthetics but won't fix it for other pre-IPO products. SpaceX publicly filed its S-1 with the SEC last week, revealing an 18,712 bitcoin position worth roughly $1.45 billion and targeting a public offering valuation above $1.75 trillion, with pricing expected on June 11 and trading on Nasdaq as early as June 12 under the ticker SPCX.

Once SPCX prints a live Nasdaq price, oracle dependency collapses to a solved problem for SpaceX specifically. The availability of a public reference price should reduce oracle risk specifically for SpaceX synthetics; however, the broader question of how to safely price pre-IPO perpetuals for other private companies without public price feeds remains unresolved, and Ventuals currently lists markets for several pre-IPO firms each facing similar oracle dependency risks until those companies pursue public listings.

Conclusion

The May 28, 2026 events around SpaceX pre-IPO assets were a stress test that neither retail traders nor synthetic infrastructure passed cleanly. The Bitget preSPCX 80% display drop was a cosmetic 1:5 token split that left holders' total value intact — a classic case of headline panic without actual loss. The Hyperliquid SPACEX-USDH 45% flash crash was the real damage: 405 users and 1,393 positions liquidated for $1.51 million in notional value, triggered by a faulty Notice.co oracle feed mishandling SpaceX's 5-for-1 stock split.

The structural lesson is bigger than one bad data point. Pre-IPO perpetuals depend on single off-chain oracles, lack public reference prices, and trade in thin markets where one large order can collapse the book. Hyperliquid's 1%-per-3-second mark price cap was no match for a cascading oracle move. With SpaceX's June 11 pricing and June 12 Nasdaq debut imminent, SPACEX-specific oracle risk will fade — but the broader pre-IPO synthetic category remains structurally fragile until better redundancy emerges.

FAQs

1. Will Hyperliquid SPACEX-USDH traders be made whole after the crash?

Yes, partially. Ventuals — the HIP-3 builder behind the contract — announced it would compensate affected users within 48 hours of the May 28 incident, though the exact compensation amount and methodology have not been publicly disclosed. Traders should monitor Ventuals' official channels for distribution details.

2. Is the Bitget preSPCX token a security or actual SpaceX equity?

Neither. According to Bitget's own disclosures, preSPCX (formerly preSPAX) is a debt instrument issued by Republic International Cayman that mirrors SpaceX's economic performance. It carries no voting rights, no dividend rights, no shareholder rights, and is not affiliated with or endorsed by SpaceX.

3. What leverage was used by traders who got liquidated on Hyperliquid?

Most liquidated traders were using approximately 3x leverage — modest by crypto standards. The problem wasn't aggressive leverage; it was that a 45% adverse move in 30 minutes will liquidate almost any leveraged long position regardless of leverage tier, especially with thin margin cushions averaging $31.

4. Are other pre-IPO perpetual contracts on Ventuals at similar risk?

Yes. Ventuals also lists pre-IPO perpetuals for Anthropic and OpenAI, both of which rely on the same off-chain oracle architecture. Until these private companies establish public reference prices through their own IPOs, they carry the same single-oracle dependency that caused the SPACEX-USDH flash crash.