Why SpaceX's Valuation Could Reach $3 Trillion — And Whether Investors Should Worry About a Bubble

2026/06/16 17:07:00

Introduction

Can a company generating less than $20 billion in annual revenue realistically justify a multi-trillion-dollar valuation?

That question is at the center of the debate surrounding SpaceX in 2026. Following its record-setting public debut and rapid post-listing rally, market discussions have shifted from whether SpaceX deserves a trillion-dollar valuation to whether it could eventually approach $3 trillion. According to Reuters reporting published in June 2026, SpaceX's IPO ultimately raised approximately $85.7 billion after underwriters exercised additional allocation rights, while post-listing trading briefly pushed the company above the $2 trillion threshold.

Many observers initially dismissed the rally as speculative enthusiasm. But institutional capital appears to be pricing SpaceX differently. Rather than valuing a traditional aerospace company, markets increasingly view SpaceX as a combination of communications infrastructure, government-backed strategic capability, orbital logistics, and long-duration technology optionality.

So, could SpaceX really reach $3 trillion? And more importantly — would that valuation represent rational expectations or a speculative bubble?

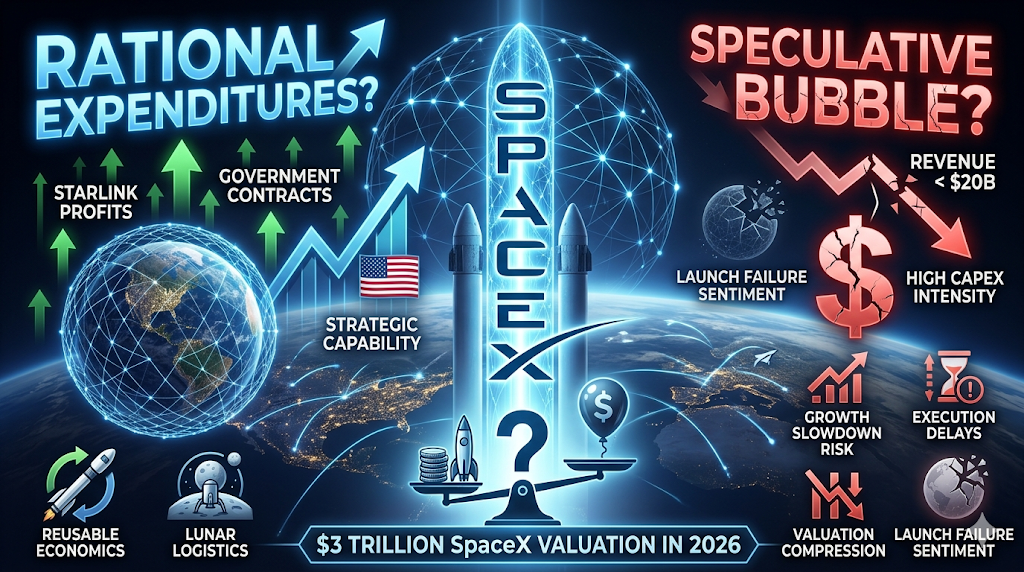

What Is Driving SpaceX Toward a Potential $3 Trillion Valuation?

The short answer is that investors are no longer valuing SpaceX as a rocket company.

Traditional aerospace businesses typically trade based on manufacturing output and contract pipelines. SpaceX is increasingly being valued as a platform business with multiple overlapping revenue engines.

According to Reuters and recent market disclosures, SpaceX generated approximately $18.7 billion in 2025 revenue but achieved a market valuation above $2 trillion shortly after listing. That gap looks extreme on traditional valuation metrics, yet supporters argue that current revenue understates future monetization opportunities.

Three major valuation narratives dominate institutional discussions.

Starlink Is Becoming the Core Profit Engine

Starlink has evolved from a supporting business into the centerpiece of the SpaceX investment thesis.

Recent market analysis estimates that Starlink contributed the majority of SpaceX operating profitability and represented a substantial portion of consolidated revenue entering 2026. Subscriber growth and geographic expansion transformed the business from experimental infrastructure into a global communications network.

Unlike launch services, satellite broadband creates recurring cash flow. Investors see three characteristics that support premium valuation multiples:

-

Subscription revenue instead of one-off contracts

-

Global addressable market expansion

-

Infrastructure advantages that become stronger as scale increases

Satellite internet also serves customer groups that terrestrial providers struggle to reach — maritime operations, remote regions, emergency communications, military deployments, and underserved geographies.

Supporters argue that if cloud infrastructure created companies worth trillions, orbital communications infrastructure could follow a similar path.

Government Contracts Reduce Commercial Risk

SpaceX's relationship with public-sector customers significantly changes how investors evaluate downside risk. Government aerospace contracts are not new, but SpaceX occupies an unusually strategic position.

NASA missions, defense programs, launch operations, satellite deployment, and national infrastructure initiatives increasingly rely on SpaceX capabilities.

Institutional investors often interpret this differently from typical enterprise revenue. Instead of asking whether SpaceX can acquire customers, markets ask whether governments can realistically replace SpaceX at scale.

That distinction matters because strategic infrastructure businesses historically command valuation premiums. This does not eliminate risk, but it changes the nature of the risk from demand uncertainty to execution uncertainty.

Starship and Long-Term Space Infrastructure Function as Embedded Options

The third driver is optionality. Markets rarely assign full present value to projects that may not mature for decades. However, they frequently assign probability-weighted value to transformational opportunities.

For SpaceX, that optionality includes:

-

Fully reusable heavy launch economics

-

Orbital manufacturing

-

Space computing infrastructure

-

Lunar logistics

-

Interplanetary transportation

-

Long-duration communications networks

Importantly, investors are not necessarily paying for Mars colonization itself. They may be paying for the possibility that SpaceX becomes foundational infrastructure for entirely new industries.

That distinction explains why valuation models appear disconnected from current earnings.

Does SpaceX's Current Valuation Actually Make Financial Sense?

The answer depends entirely on which framework investors use. If SpaceX is evaluated as an aerospace contractor, current valuation appears extremely expensive.

If investors treat SpaceX as infrastructure plus communications plus AI exposure plus long-term optionality, valuation assumptions become more flexible. The comparison below illustrates the challenge.

| Company | Approximate Valuation Framework | Core Growth Driver |

| Apple | Consumer ecosystem | Devices and services |

| Microsoft | Software and cloud | Enterprise infrastructure |

| Amazon | Commerce and cloud | Network effects |

| SpaceX | Communications + space infrastructure | Platform expansion |

Supporters argue that historical market leaders often appeared expensive before monetization matured. Critics counter that even dominant companies eventually needed revenue growth to justify market capitalization.

According to recent IPO analysis published in 2026, implied valuation multiples placed SpaceX near or above 90x annual sales depending on methodology. That level requires extraordinary execution.

To justify $3 trillion mathematically, investors likely need to assume:

-

sustained double-digit annual growth,

-

continued Starlink expansion,

-

successful Starship deployment,

-

stable government demand,

-

and entirely new revenue categories.

Is SpaceX a Bubble or a Rational Repricing?

Calling every expensive asset a bubble oversimplifies market behavior. A bubble occurs when price disconnects permanently from realistic future cash generation. A repricing occurs when markets update assumptions about future economics.

Today, both interpretations exist.

The Bubble Argument

The bear case is straightforward. Revenue remains small relative to valuation. Profitability remains inconsistent. Capital expenditure requirements continue rising. Recent reporting indicated substantial investment intensity across growth initiatives despite expanding revenue.

Critics argue investors may be extrapolating too much success from a limited number of proven businesses. Several concerns stand out:

-

Revenue scale remains modest relative to valuation

-

Expansion assumptions extend many years forward

-

Competitive threats remain possible

-

Launch failures could damage sentiment quickly

Under this framework, valuation is borrowing heavily from future execution.

The Repricing Argument

The bullish case argues that traditional valuation methods underestimate platform transitions. Supporters point out that markets repeatedly underestimated companies during major infrastructure shifts.

Examples often include:

-

cloud computing,

-

smartphones,

-

internet commerce,

-

and AI infrastructure.

The argument is not that SpaceX deserves $3 trillion today. The argument is that ownership of strategic infrastructure becomes increasingly valuable as ecosystems consolidate.

If space becomes a major economic layer over the next twenty years, investors may prefer paying aggressively early rather than missing exposure entirely.

What Risks Could Break the $3 Trillion Investment Thesis?

The strongest bull markets still depend on assumptions staying intact. SpaceX's valuation case becomes weaker if one or more foundational assumptions fail.

Risk 1: Starlink Growth Slows

Subscription businesses depend on expansion. If customer acquisition slows or pricing compresses, valuation expectations could reset.

Risk 2: Starship Execution Delays

Much of the future narrative depends on dramatically lower launch costs. Technical setbacks would reduce confidence in long-duration projections.

Risk 3: Government Concentration Risk

Strategic relationships create stability but also concentration. Policy shifts or competitive procurement could affect growth assumptions.

Risk 4: Valuation Compression Across Growth Markets

Even if execution remains strong, macroeconomic conditions may reduce acceptable valuation multiples. History shows that excellent companies can still experience severe repricing.

How to Trade SpaceX and US Stocks on KuCoin

KuCoin gives you streamlined access to SPCX and a growing range of crypto-equity products, making it one of the most efficient platforms for building a blended portfolio.

KuCoin also offers exposure to trading US stock perps — meaning you can rebalance between crypto and US equity narratives without leaving the platform. Combined with the security infrastructure of a tier-one global exchange, KuCoin is positioned for investors who want flexibility across both asset classes.

Conclusion

SpaceX approaching a $3 trillion valuation sounds extraordinary, but markets are not pricing the company as a rocket manufacturer anymore.

Investors increasingly view SpaceX as a combination of global communications infrastructure, strategic government capability, launch economics, and long-term technological optionality. That framework explains why traditional valuation comparisons often appear disconnected.

At the same time, skepticism remains justified.

Current revenue still represents only a fraction of what would normally support multi-trillion-dollar market capitalization. Much of today's valuation depends on execution years into the future. Starlink must continue scaling, Starship must deliver, and new business models must emerge.

The most balanced interpretation may be that this is neither pure speculation nor fully proven economics. Markets are effectively placing a long-duration bet that space becomes the next foundational platform layer for the global economy.

If that happens, $3 trillion may eventually look conservative. If it does not, today's valuation could become a case study in future expectations moving too far ahead of financial reality.

FAQs

-

What business contributes most to SpaceX valuation today?

Starlink appears to be the largest contributor because of recurring revenue and stronger profitability characteristics.

-

Is SpaceX profitable?

Reported revenue has grown significantly, but consolidated profitability remains affected by investment intensity and expansion spending.

-

Why do investors compare SpaceX to technology companies instead of aerospace companies?

Because investors increasingly view SpaceX as infrastructure and platform exposure rather than manufacturing output.