What Is LFI on Base Chain? How It Tokenizes US Property Tax Liens for Onchain Yield

2026/05/19 10:33:01

Introduction

The US property tax lien market generates an estimated $21 billion in delinquent tax obligations annually, yet retail investors have historically been locked out by county-level auctions, paperwork barriers, and minimum capital requirements often exceeding $10,000 per lien. LFI is changing that. LFI is a Base chain RWA (real-world asset) protocol that tokenizes US county property tax liens, allowing anyone with a wallet to access yield streams previously monopolized by institutional buyers and specialized funds.

As of mid-May 2026, LFI's FDV broke past $27 million with a 24-hour gain exceeding 23%, according to onchain market trackers — making it one of the standout movers in Base's accelerating RWA sector. This article breaks down what LFI does, how the tax-lien tokenization model works, the bull and bear case, and the risks investors should weigh before participating.

What Is LFI on Base Chain?

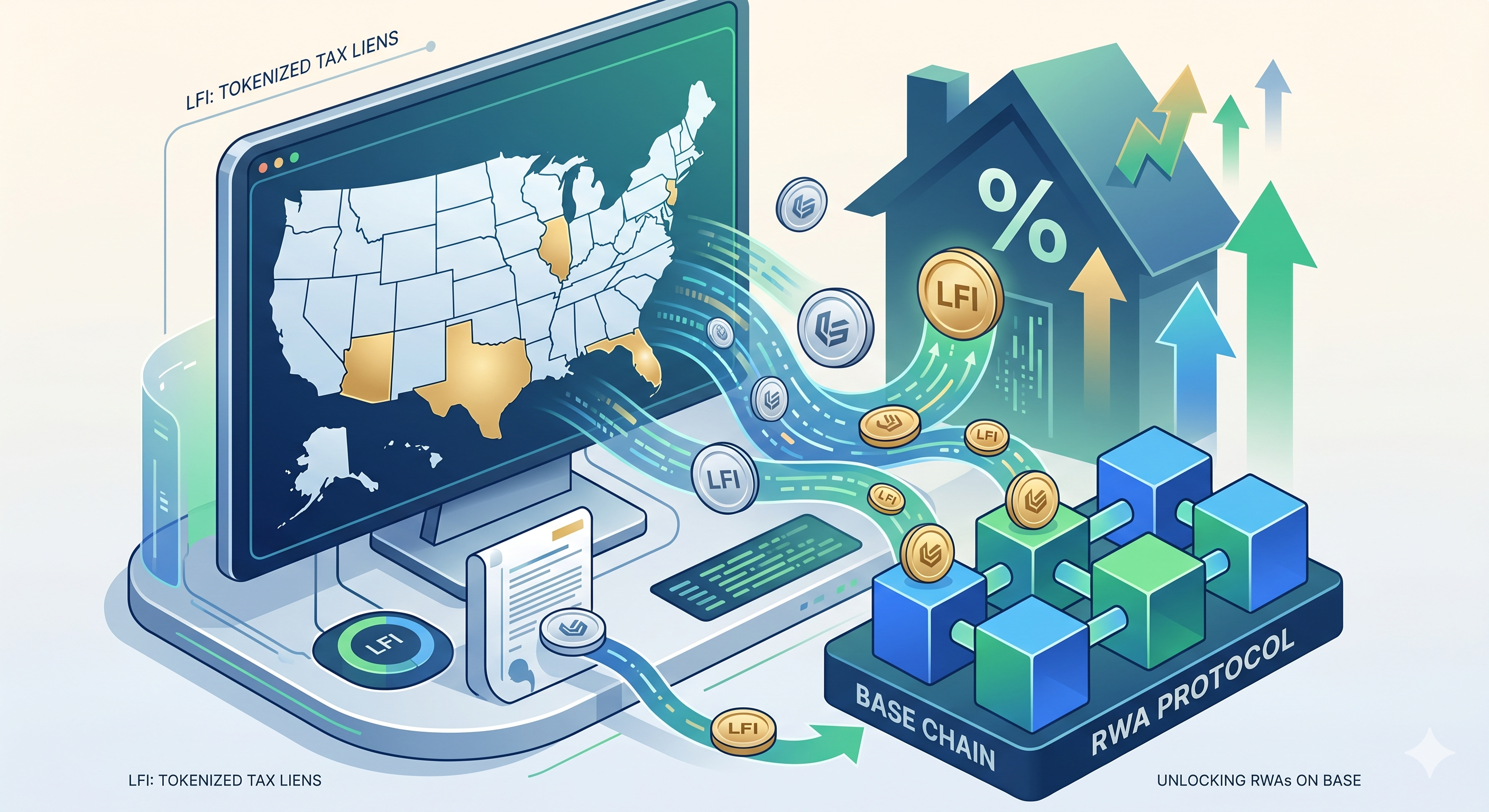

LFI is a real-world asset (RWA) protocol built on Coinbase's Base Layer-2 network that tokenizes US property tax liens into onchain, yield-bearing assets. Rather than buying a single physical lien certificate at a county auction, holders gain fractional exposure to a portfolio of tax-lien claims that generate statutory interest payments from delinquent property owners.

The protocol sits at the intersection of two of 2026's strongest narratives — Base chain growth and tokenized real-world assets. Base's total RWA TVL has expanded sharply since May 2026, and LFI has emerged as a flagship project pulling capital and attention into the segment.

Why Property Tax Liens?

Property tax liens are one of the most legally protected cash-flow instruments in the United States. When a homeowner fails to pay property taxes, the county issues a lien — a senior claim on the property that must be settled before any mortgage. Investors who buy these liens earn statutory interest rates that, depending on the state, can range from 8% to 36% annually until the homeowner redeems the debt.

This asset class is attractive because:

-

Senior legal claim — tax liens sit ahead of mortgages in priority

-

Government-enforced interest rates — yields are set by state law, not market negotiation

-

Collateralized by real estate — recovery is backed by a tangible property

-

Counter-cyclical demand — delinquencies often rise during economic stress

Historically, accessing this market required attending physical county auctions, navigating 50 different state legal frameworks, and tying up capital for 1-3 years. LFI abstracts all of that into a single onchain token.

How Does LFI Tokenize US Property Tax Liens?

LFI tokenizes property tax liens by acquiring them through licensed entities, packaging them into a pooled structure, and issuing onchain tokens that represent claims on the underlying yield. The process bridges off-chain legal ownership with on-chain liquidity and transparency.

The Acquisition Layer

The protocol's off-chain partners participate in county tax-lien auctions across qualifying US states — primarily Florida, Arizona, New Jersey, Illinois, and Texas, which together account for the bulk of investor-friendly lien markets. Each acquired lien is held in a special-purpose legal vehicle that serves as the bankruptcy-remote custodian.

The Tokenization Layer

Once liens are custodied, the protocol mints corresponding tokens on Base. The token holder is not buying the lien certificate directly but rather a claim on the cash flows produced by the lien pool. When homeowners redeem their delinquent taxes (paying principal plus statutory interest), proceeds flow back through the smart contracts and are distributed to token holders or used to acquire new liens.

The Yield Distribution Layer

Yield is generated from two sources:

-

Statutory interest — fixed by state law, paid by the delinquent property owner upon redemption

-

Property foreclosure proceeds — in the rare case where the homeowner never redeems, the lien holder can foreclose and take ownership of the property at a deep discount

This dual-track structure means the protocol earns whether homeowners pay or not — a feature that has made tax liens a favored institutional product for decades.

What Are the Bull and Bear Cases for LFI?

The bull case rests on real yield delivery, while the bear case centers on tokenomics transparency and unlock risk. Investors should weigh both before sizing a position.

The Bull Case

Real-yield catalyst potential. If LFI's tax-lien revenue model demonstrably distributes statutory interest to token holders onchain, it would validate one of the most credible RWA designs in the Base ecosystem. Verifiable cash flow is the single hardest thing for RWA tokens to deliver, and it is also the single largest re-rating event when delivered.

First-mover advantage. No major competitor on Base is currently focused specifically on property tax liens. If LFI captures the category before larger DeFi or RWA platforms enter, it could become the default ticker for this exposure.

Macro tailwind. US property tax delinquencies tend to rise with cost-of-living stress. In a higher-for-longer rate environment, more liens become available at attractive yields.

The Bear Case

Opaque tokenomics. Public information on LFI's full token supply, vesting schedule, and team/investor allocations remains limited. Without transparent unlock schedules, holders face unknown future sell pressure.

Unverified smart-contract mechanics. Marketing materials describe how tax-lien yield should flow to holders, but the on-chain mechanism for converting off-chain lien redemptions into on-chain distributions has not been independently audited or widely documented.

Speculative premium. A 23% single-day move suggests the price is currently driven more by narrative momentum and KOL flows than by underlying yield accrual. Mean reversion is a real risk once the FOMO subsides.

How Does LFI Compare to Other Base Chain RWAs?

LFI differentiates from other Base RWA tokens by targeting a unique underlying asset — county tax liens — rather than the more crowded categories of tokenized Treasuries or private credit. The table below outlines the high-level positioning.

|

RWA Category on Base

|

Underlying Asset

|

Typical Yield Source

|

LFI Comparison

|

|

Tokenized Treasuries

|

Short-term US T-Bills

|

Fed-driven risk-free rate

|

LFI yield is higher but credit-exposed

|

|

Tokenized Private Credit

|

Corporate loans

|

Loan interest spreads

|

LFI is government-enforced rates, not negotiated

|

|

Tokenized Real Estate

|

Property equity

|

Rental cash flows

|

LFI is a senior debt claim, not equity

|

|

LFI (Tax Liens)

|

Delinquent property tax claims

|

Statutory interest 8-36%

|

Unique senior-secured claim, high yield

|

The takeaway: LFI is not directly competitive with most existing Base RWA tokens — it occupies a niche of its own, which is both an opportunity and a reason for caution given the lack of comparable benchmarks.

Conclusion

LFI represents one of the more creative real-world asset experiments to emerge from the Base ecosystem in 2026 — tokenizing US property tax liens to bring a historically institutional cash-flow market onchain for retail participants. The protocol's $27 million FDV, 23%+ single-day rally, and growing smart-money interest reflect strong narrative alignment with the broader RWA wave sweeping Base.

The bull case is compelling: senior-secured claims on real estate, statutory yields between 8% and 36%, and a first-mover position in a niche RWA category. But the bear case is equally real — opaque tokenomics, unverified smart-contract distribution mechanics, regulatory uncertainty around tokenized lien securities, and the small-cap volatility that comes with a sub-$30 million token.

For traders, LFI is best treated as a high-conviction but high-variance position. Verify the project's official documentation, monitor on-chain contract activity, and watch for the eventual publication of a full tokenomics breakdown before committing meaningful capital. The story is promising, but the proof must come from delivered yield, not just price action.

FAQs

1. Is LFI a security under US law?

LFI's classification has not been confirmed by the SEC. Because the token represents a claim on yield generated by underlying tax-lien instruments, it has features that could be viewed through the lens of US securities law. Investors in restricted jurisdictions should consult legal counsel.

2. Can I redeem LFI tokens for the underlying property tax liens?

No. Token holders hold a claim on the yield stream and pooled performance of the lien portfolio — not direct ownership of any specific lien certificate. The underlying liens remain held by the protocol's licensed off-chain custodian.

3. What states does LFI operate tax-lien acquisition in?

LFI's off-chain partners primarily target investor-friendly tax-lien states such as Florida, Arizona, New Jersey, Illinois, and Texas. Each state has different statutory interest rates and redemption periods, which the protocol blends into its overall portfolio yield.

4. How often is yield distributed to LFI holders?

Distribution cadence depends on when underlying homeowners redeem their delinquent taxes, which is irregular by nature. The protocol's documentation should be consulted for specific distribution schedules, smart-contract mechanics, and any auto-compounding features.

5. What happens to LFI's price if Base chain RWA narrative cools?

LFI would likely face material drawdown pressure if the broader Base RWA sector rotation reverses, given that recent price action has been driven heavily by narrative flows and KOL momentum. Tokens with small market caps and limited float typically experience amplified moves in both directions during sector rotations.