Circle Reports Q1 2026 Earnings: USDC Volume Surges 263%, Arc Blockchain Unveiled

2026/05/12 06:42:02

Introduction

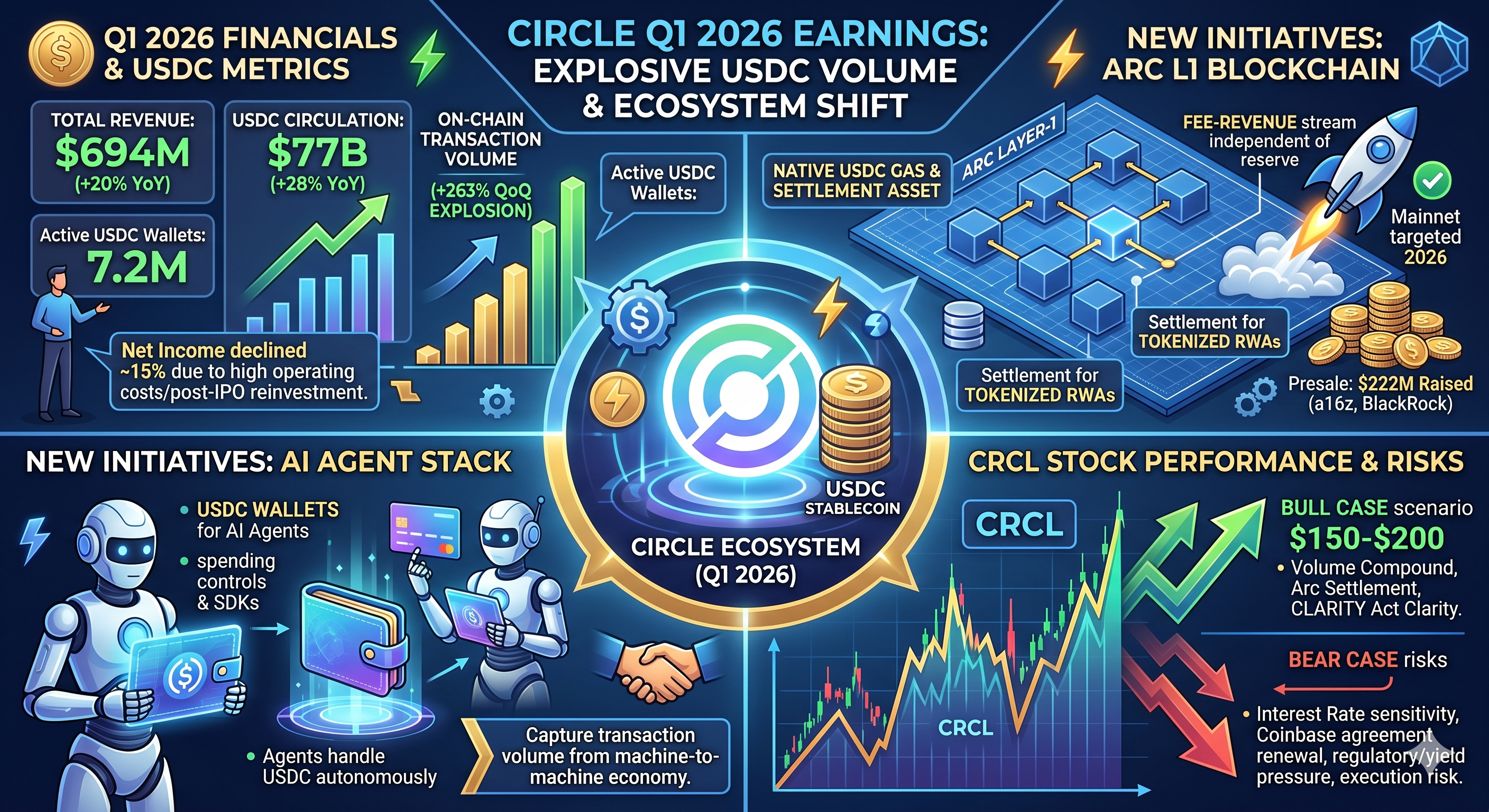

Circle's USDC on-chain transaction volume exploded 263% quarter-over-quarter in Q1 2026, while circulation climbed 28% year-over-year to $77 billion — a signal that stablecoin adoption is accelerating far beyond what most analysts modeled at the start of the year. According to Circle's Q1 2026 earnings release published on its pressroom, revenue grew 20% YoY to $694 million, even as net income dipped 15% due to elevated post-IPO operating expenses. The company simultaneously unveiled its Arc Layer-1 blockchain whitepaper and an AI-focused Agent Stack, repositioning itself well beyond a pure stablecoin issuer.

To understand the full context, the recommended readings are as below:

-

CRCL Stock Comparison benchmarks Circle against other listed crypto equities,

-

CLARITY Act Impact examines how the stablecoin yield ban reshapes CRCL's earnings power,

-

and CRCL Price Targets explores upside scenarios tied to final regulatory passage.

What Did Circle Report in Q1 2026 Earnings?

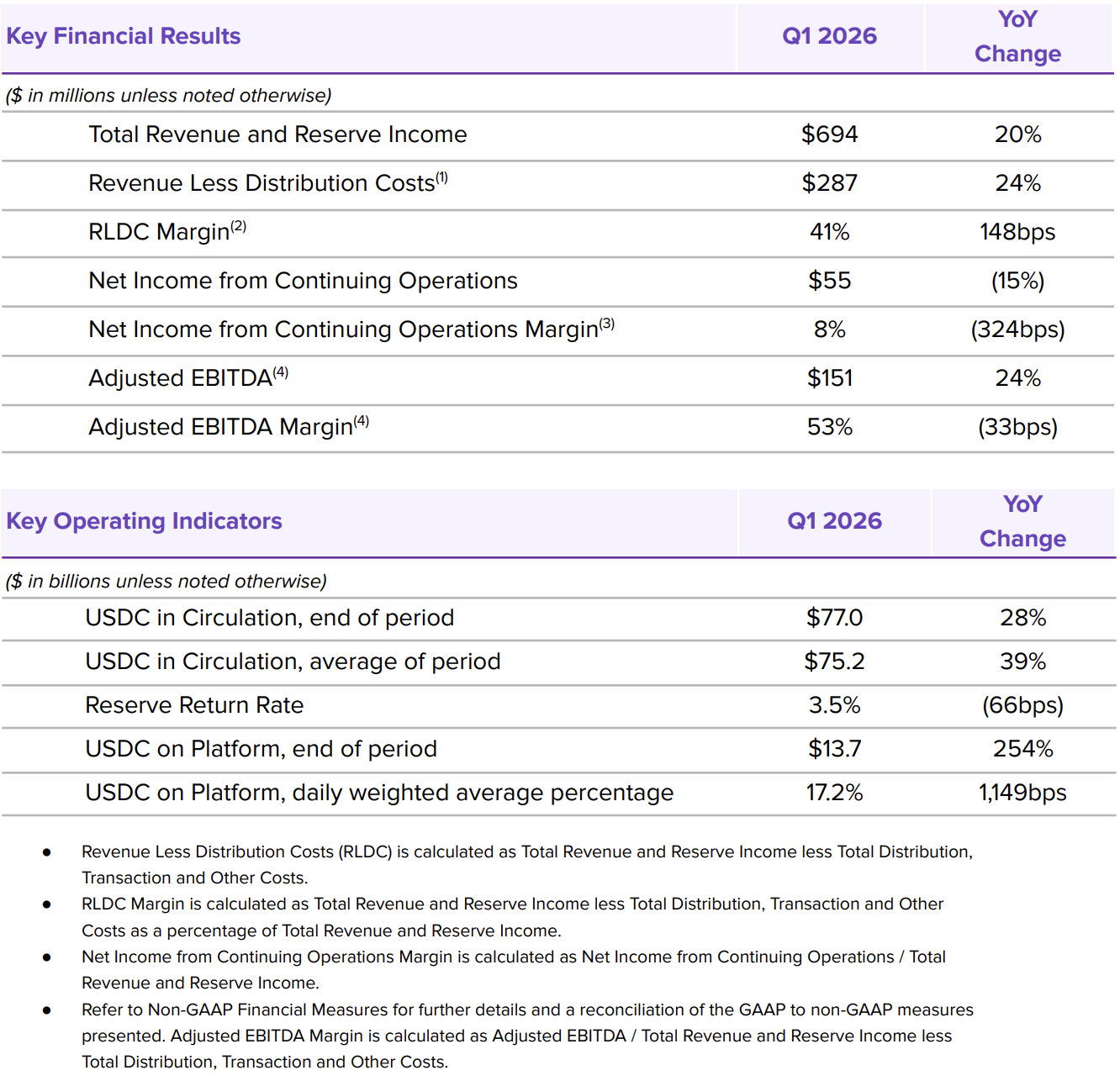

Circle reported $694 million in total revenue for Q1 2026, up 20% year-over-year, but net income declined approximately 15% as the company absorbed higher public-company operating costs. According to Circle's Q1 2026 press release, the headline mix shows a business growing aggressively on the top line while reinvesting heavily into infrastructure, distribution, and the new Arc ecosystem.

USDC in circulation reached $77 billion at quarter-end, a 28% YoY increase. On-chain USDC transaction volume jumped 263% sequentially — the largest single-quarter acceleration since Circle went public. Active USDC wallets rose to 7.2 million, reflecting both retail expansion and institutional onboarding through Circle Mint partners.

Revenue Breakdown and Margin Pressure

Reserve income remained the dominant revenue line, contributing the majority of the $694 million figure. Subscription and services revenue — covering Circle Mint, CCTP cross-chain transfers, and the new payments stack — grew faster on a percentage basis but from a smaller base.

Operating expenses rose materially. Compensation, compliance, and product investment all expanded as Circle scaled its global footprint following its 2025 listing. The 15% net income decline reflects deliberate reinvestment rather than core business deterioration, according to management commentary accompanying the release.

Key Operating Metrics

|

Metric

|

Q1 2026

|

YoY Change

|

|

Total Revenue

|

$694M

|

+20%

|

|

USDC Circulation

|

$77B

|

+28%

|

|

On-Chain Volume (QoQ)

|

—

|

+263%

|

|

Active Wallets

|

7.2M

|

Growing

|

Why Did USDC On-Chain Volume Surge 263%?

USDC on-chain volume surged 263% quarter-over-quarter primarily because of expanding cross-chain deployment, growing DeFi integration, and rising institutional settlement activity. The data point is the standout figure of the entire Q1 release and the single biggest reason CRCL bulls remain constructive into mid-2026.

Three forces drove the move. First, Circle's Cross-Chain Transfer Protocol (CCTP V2) saw native USDC availability extended across more than 20 chains by quarter-end, removing friction for wrapped-asset users migrating to canonical USDC. Second, tokenized money market funds — including products linked to Circle's reserve infrastructure — recycled increasing volume on-chain. Third, payments corridors in Latin America and Asia-Pacific saw sharp growth as merchants and remittance providers adopted USDC rails.

The Verification Caveat

The 263% figure deserves a caveat. On-chain volume metrics can be inflated by bot activity, MEV transactions, and routing through aggregators. Independent verification across block explorers is partial, and Circle has not yet published the full methodology behind the figure in granular form. Traders should weight the trend direction over the precise magnitude when modeling the stock.

How Does the Arc Blockchain Change Circle's Long-Term Story?

Circle's Arc blockchain, unveiled via whitepaper alongside Q1 earnings, transforms the company from a stablecoin issuer into a vertically integrated settlement infrastructure provider. Mainnet is targeted for 2026, with a presale that raised $222 million from investors reportedly including a16z and BlackRock, according to Circle's official announcement.

Arc is purpose-built around USDC as the native gas and settlement asset. That design eliminates the gas-token volatility problem for enterprises and creates a captive economic loop: every transaction on Arc generates fees denominated in USDC, capturing value Circle previously surrendered to external Layer-1s like Ethereum and Solana.

Strategic Implications

Arc gives Circle three things it lacked. It provides a fee-revenue stream independent of reserve interest, hedging the interest-rate risk that dominates the current P&L. It creates a settlement layer optimized for tokenized real-world assets — a market Boston Consulting Group and others have repeatedly projected into the trillions by 2030. And it positions Circle as the issuer-and-rails counterpart to traditional financial market infrastructure providers.

Competitive Positioning

The Arc rollout puts Circle into direct competition with general-purpose Layer-1s and with stablecoin-native chains. Execution risk is real: launching a new L1 in 2026 means competing for liquidity, developers, and validator decentralization against incumbents with multi-year head starts. The $222 million presale and tier-one backers materially de-risk the launch, but adoption is the gating variable.

What Is Circle's AI Agent Stack and Why Does It Matter?

Circle's Agent Stack is a developer toolkit that lets AI agents hold, send, and receive USDC autonomously — and it matters because it positions Circle to capture transaction volume from the emerging machine-to-machine economy. The Agent Stack was launched alongside the Q1 earnings release.

The product set includes AI agent wallets with programmable spending controls, identity and compliance primitives so agents can transact under issuer-grade KYC frameworks, and SDKs that integrate with major AI agent frameworks. The thesis is straightforward: if autonomous AI agents become significant economic actors over the next three to five years, the payments rail they default to will accrue enormous transaction volume.

USDC's regulatory clarity in the US — particularly under the evolving CLARITY Act framework — gives Circle a credibility edge over algorithmic and offshore alternatives when AI builders evaluate which stablecoin to integrate. Whether agent-driven volume becomes material within Circle's 2026-2027 reporting horizon is uncertain, but the optionality is genuine.

How Did CRCL Stock React to the Q1 2026 Earnings Report?

CRCL stock reacted with sharp two-way volatility after the Q1 print, initially selling off on the revenue miss against consensus before recovering as the market digested the Arc whitepaper, the Agent Stack launch, and the 263% on-chain volume growth. The intraday range exceeded 10% in the session following the release, according to public market data.

The bear reaction focused on three points: revenue came in slightly below the highest sell-side estimates, net income declined year-over-year, and reserve income remains hostage to Federal Reserve policy. The bull reaction centered on the explosive USDC volume growth, the strategic depth added by Arc, and the strength of the institutional presale.

Sell-Side Sentiment Shift

Sentiment among crypto-equity analysts shifted notably more constructive following the call. Several research desks raised price targets based on Arc's optionality and the trajectory of stablecoin circulation. Skeptics remain focused on the structural risk that yield-bearing stablecoin competitors — including Ethena's USDe — could erode USDC's market share if regulation eventually permits yield pass-through.

What Are the Key Risks Facing Circle After Q1 2026?

The key risks facing Circle are interest rate sensitivity, the Coinbase distribution agreement renewal, regulatory drift on yield, and competition from yield-bearing stablecoins. Each materially affects the forward earnings model.

Interest Rate Sensitivity

Reserve income — interest earned on Treasury bills backing USDC — remains the dominant revenue driver. With the Federal Reserve in a balance-sheet runoff phase and rate-cut expectations building into the second half of 2026, the yield Circle earns per dollar of circulation is likely to compress. Volume growth has so far offset rate pressure; whether that continues depends on circulation scaling faster than spreads compress.

Coinbase Agreement Renewal

The economic split with Coinbase under the existing distribution agreement is due for renewal in August. The terms of any renegotiation will materially affect Circle's net retained reserve income, and the outcome is one of the most-watched catalysts on the calendar.

Regulatory and Competitive Pressure

The CLARITY Act's stablecoin yield ban — discussed in detail in the spoke coverage — is a double-edged sword. It protects incumbents like Circle from yield-based competition domestically, but it also caps Circle's ability to defend share if offshore yield-bearing alternatives gain enterprise traction. Regional expansion into Europe, Asia-Pacific, and Latin America carries its own compliance overhead.

What Is the Bull Case for CRCL Stock in 2026?

The bull case for CRCL rests on stablecoin demand continuing to compound at 25%+ annually, Arc capturing meaningful settlement share, and regulatory clarity in the US locking in Circle's competitive moat. If all three play out, the current valuation looks reasonable rather than stretched.

The 263% quarterly volume surge supports the demand leg directly. The $222 million Arc presale and tier-one backer list support the infrastructure leg. The pending CLARITY Act, if passed in its current form, supports the regulatory leg — and several scenarios analyzed in the spoke content sketch upside paths to $150 and even $200 per share under favorable outcomes.

Diversification matters. Tokenized funds, cross-chain bridges, payments infrastructure, and the Agent Stack all reduce dependence on the interest-rate cycle. The more revenue migrates toward subscription and services, the more durable the earnings multiple becomes.

What Is the Bear Case for CRCL Stock in 2026?

The bear case is that Circle is structurally a Treasury-yield play dressed up as a fintech, and that the yield is about to compress while competition intensifies. Net income already declined 15% YoY despite 20% revenue growth — a warning that operating leverage is currently working in reverse.

If the Fed cuts more aggressively than the market expects, if the Coinbase renegotiation tilts unfavorably, or if Ethena-style yield-bearing competitors capture share in jurisdictions that permit them, the consensus 2027 earnings estimate could prove materially too high. Arc and the Agent Stack are interesting optionality but contribute negligibly to near-term P&L. Execution risk on Arc mainnet — slated for 2026 — adds another potential disappointment vector.

Conclusion

Circle's Q1 2026 earnings tell a story of a business compounding aggressively on volume while reinvesting earnings into infrastructure that could redefine its long-term margin profile. The 263% surge in on-chain USDC transactions and 28% YoY growth in circulation to $77 billion confirm that stablecoin adoption is in a structural uptrend, even as the 15% net income decline reminds investors that reserve income remains hostage to Federal Reserve policy.

The Arc blockchain and Agent Stack are the most strategically important announcements of the quarter. If Arc captures meaningful settlement share and AI agents adopt USDC as their default rail, Circle's revenue mix could rebalance away from interest-rate dependence within two to three years. If they underperform, the bear case on margin compression hardens.

Catalysts to watch include the August Coinbase agreement renewal, CLARITY Act passage, Arc mainnet launch, and Q2 2026 print. For traders, KuCoin offers the most direct way to express views on the stablecoin themes embedded in Circle's results.

FAQs

1. When did Circle go public and what was the IPO price?

Circle listed on the NYSE in mid-2025 under the ticker CRCL. The IPO priced above the initial range due to strong demand, and the stock traded materially higher in its opening sessions before settling into a wider range driven by quarterly earnings and regulatory headlines.

2. How is USDC different from Tether's USDT?

USDC is issued by Circle under US state money transmitter licenses and provides monthly attestation reports on its reserves, which are held in cash and short-duration US Treasuries. USDT, issued by Tether, is larger by market cap but historically less transparent on reserve composition and faces a different regulatory posture.

3. Does Circle pay a dividend on CRCL stock?

Circle does not currently pay a dividend on CRCL shares. Capital is being reinvested into Arc, the Agent Stack, international expansion, and product development, consistent with a growth-stage public company profile.

4. What chains does USDC currently support?

Native USDC is available on more than 20 blockchains as of Q1 2026, including Ethereum, Solana, Base, Arbitrum, Optimism, Polygon, Avalanche, and several others. Cross-chain transfers between supported networks use Circle's CCTP V2 protocol.

5. How does the CLARITY Act affect Circle's business model?

The CLARITY Act establishes a federal framework for stablecoin issuers and includes provisions restricting yield payments on payment stablecoins. For Circle, this is broadly protective domestically — it limits yield-based competition — but it also constrains Circle's own ability to share reserve income directly with USDC holders.