Summary

This paper systematically examines the four leading RWA projects in the United States: real estate RWA (RealT), fixed-income RWA (Ondo Finance), supply chain finance RWA (Centrifuge), and pre-IPO equity RWA. The study aims to uncover the institutional logic and technological foundations of RWA in the global financial restructuring wave of 2025 through case analysis, compliance structure breakdown, and comparative yield modeling.

1. Asset structure level: RealT breaks down real estate investment barriers through SPV ownership and Reg D/S compliant issuance, enabling fractional small-scale investments; Ondo leverages U.S. Treasuries as underlying assets and integrates BlackRock and Coinbase custody mechanisms to deliver on-chain money market fund functionality; Centrifuge uses its Tinlake mechanism to tokenize supply chain receivables, with MakerDAO providing collateralized DAI liquidity, establishing a new paradigm for on-chain factoring.

2. Regulatory Compliance Perspective: Research shows that the U.S. SEC’s primary regulatory pathways for RWA structures are Regulation D, Regulation S, Regulation CF, and Regulation A+, with core principles centered on investor eligibility, disclosure obligations, and liquidity restrictions.

3. Technical Support Layer: Technically, the Aave module provides a funding bridge for institutions and ensures efficient fund flow, while Chainlink oracles guarantee the reliability of asset valuation, collateralization ratios, and yield settlements.

4. Risks and Outlook: The future development of RWA will be constrained by three key bottlenecks: compliance and disclosure costs, cross-border custody compliance, and stablecoin pegging risks. However, based on institutional adoption trends and the alignment of returns with risk, RWA is regarded as one of the most sustainable asset classes in on-chain finance.

Keywords: RWA, Tokenization, Digital Securities, Asset Tokenization, Supply Chain Finance

01 Real Estate RWA (RealT): Asset Ownership Verification, Fractionalization, and Lowering Investor Entry Barriers

1.1 Development Logic of U.S. Real Estate RWA

Real estate is one of the earliest asset classes to be tokenized and represents the segment within the RWA space most deeply integrated with the traditional financial system. Its core logic lies in fundamentally transforming the high barriers to entry and low liquidity of traditional real estate through on-chain ownership verification, fractional governance, and smart contract-based distribution mechanisms. RealT, as the most representative platform in the United States, has built a compliant tokenized real estate system on Ethereum and Gnosis since 2019, serving as a model for asset tokenization and regulatory integration.

Compared to traditional REITs (Real Estate Investment Trusts), the innovation of the RealT model lies in:

1) An SPV (Special Purpose Vehicle) token issuance structure based on specific real estate properties enables independent governance for each property;

2) Rent distribution based on stablecoins (USDC/DAI) enhances the traceability and immediacy of earnings;

3) After completing KYC/AML verification, investors can participate in overseas property income distributions with a very low capital threshold (typically starting at $50).

1.2 Asset Ownership Verification and SPV Structure Design

In the RealT system, the title verification process is the most critical regulatory step. Before any property is tokenized, it must undergo title review, valuation certification, and SPV registration. This SPV is typically established in Michigan or Delaware, USA, in the form of an LLC (Limited Liability Company), with RealT responsible for property management and income distribution. The table below outlines RealT’s standardized asset title verification process.

Note: RealT employs a two-layer structure of SPV + Token, which does not avoid the classification of the Token as a security—in fact, RealT’s Tokens are explicitly considered securities; they are issued through Reg D / Reg S exemption pathways, thus avoiding public registration (Non-Public Offering).

1.3 Share Split and Overcoming Investor Thresholds

RealT's success lies in lowering barriers and increasing participation. Traditional real estate investment typically requires capital in the millions, but RealT enables fractional ownership through tokenization. Investors can choose to invest in individual properties, with earnings automatically distributed according to their token holdings.

Note: RealT's token liquidity primarily relies on its own marketplace, with occasional integration with DEXs such as Uniswap. Its advantages include instant liquidity and global participation, but regulatory barriers limit its investor base primarily to accredited investors who have completed KYC verification.

1.4 Economic Benefit Model and On-Chain Revenue Distribution

RealT platform returns primarily come from rental distributions and secondary market price spreads. [4] Based on public data (2025), RealT properties have an average net rental yield of 10%, maintaining high returns even after deducting property management and maintenance fees.

Note: RealT's value lies not only in its cash flow stability but also in transforming real estate into quasi-monetary assets. During the Federal Reserve's high-interest-rate cycle, its stable returns and asset preservation characteristics make it a secure yield source within the USDC stablecoin ecosystem, with some DeFi protocols already integrating RealT tokens as collateral.

1.5 Regulatory Challenges and Future Outlook

The advantages of the RealT model are accompanied by risks: first, regulatory gray areas—although the project adheres to the Reg D/Reg S framework, legal uncertainties remain regarding whether secondary market trading of its tokens constitutes unregistered securities distribution. Second, compliance expansion bottlenecks—variations in state laws governing real estate transactions and SPV formation make asset standardization difficult. Third, oracle and on-chain valuation issues—RealT currently employs a fixed valuation method, lacking a dynamic market pricing mechanism.

However, from a macro perspective, real estate RWA is gradually integrating with the traditional financial system. Institutions such as BlackRock and Franklin Templeton are exploring structured portfolios combining on-chain funds with physical assets; meanwhile, the open regulatory environments in markets like Hong Kong and the UAE provide fertile ground for the international replication of the RealT model.

1.6 Case Study

1.6.1 Detroit Rental Housing Project (2024)

Detroit is a key focus city for RealT, offering low property prices and stable rental income, making it an ideal asset for high returns with low volatility. For example, a residential property listed on-chain in 2024[5]:

- Property value: USD 72,500

- Token issuance: 1,450 tokens ($50 each)

- Annual net rental income: USD 7,400

- Investor Return Rate: 10.2%

- Payment Method: Weekly automatic distribution of USDC

- Investor sources: Primarily KYC-verified investors from the European Union, Canada, and Singapore.

Success factor: The project’s success lies in the integration of real-world assets with on-chain smart contracts. Rental income is distributed in real time via stablecoins, allowing investors to directly verify receipt of payments through a blockchain explorer; property management data and lease agreements are uploaded as hashes, enabling immutable audit trails.

Risk points: Operations (property management, taxation, tenant disputes) remain off-chain determinants; tokenization cannot replace on-site management. Feedback from RealT’s expansion has highlighted weak operational coordination, indicating that on-site KPIs should be routinely integrated with on-chain disclosures. During due diligence,务必 obtain on-site due diligence reports, custody/insurance terms, and property management agreements.

1.6.2 St. Regis Aspen or Aspen Coin

In 2018, Elevated Returns tokenized a portion of the St. Regis Aspen Resort in Colorado (Aspen Coin), [6] offering it as a security token to accredited investors and raising approximately $18M. This case is often regarded as a representative example of legal compliance preceding technological implementation.

- Property value: Approximately $18M raised, representing nearly 18% equity in the hotel, implying a total hotel valuation of approximately $95M–$100M+ at the time.

- Token Issuance: Issued at a price of $1/coin, totaling 18,000,000 Aspen Coins.

- Annual net rental yield: This product distributes returns based on hotel revenue, with the annualized return dependent on the hotel’s operational performance, as publicly disclosed through dividend payments to shareholders.

- Investor Return: As an equity product, returns come from hotel operating profits and capital gains; this project does not guarantee a fixed return.

- Payment methods: Available for purchase using publicly accessible USD, BTC, ETH, etc.; dividends and distributions are executed through traditional payment or custodial procedures within legal and custodial frameworks, with on-chain tokens serving to record and transfer ownership.

- Investor sourcing: Primarily targeted at qualified, institutional, and restricted investors, with a minimum purchase requirement of 10,000 tokens to align with compliant investor criteria [7].

Success point: Prioritized resolving legal and custody issues (SPV, trustee, securities registration), treating tokens as digitized securities, thereby providing a compliant pathway for institutions and qualified investors and reducing regulatory barriers.

Risks: High compliance costs and limited liquidity in the secondary market; suitable for high-value, low-frequency trading assets. For offerings targeted at institutions or family offices, compliance prioritization is typically more important.

1.6.3 Roofstock onChain (Single Property NFT or LLC Structure)

Roofstock onChain enables on-chain trading and coordination with off-chain property transfers by converting single residential properties—often rental units—into NFTs representing ownership equity of a single-member LLC. The platform also integrates on-chain financing and compliant KYC processes.

- Real estate value: Public transaction examples include $175,000 (a property in South Carolina, purchased with USDC in 2022)

- Token issuance: Roofstock On Chain typically represents an entire property with a single NFT (ERC-721).

- Annual net rental yield: For a property priced at $175k–$180k, the typical rental yield varies with market conditions and generally falls within a net rental return range of 4–8%[8].

- Investor Return: For full property buyers, the return consists of net rental income plus capital appreciation; for Fractional Holders (if subdivided), returns are distributed proportionally according to share ownership.

- Payment Methods: Pay with USDC (a stablecoin) combined with on-chain loans (Teller or USDC Homes), or use fiat pathways (the platform supports multi-channel settlement).

- Investor base: Targeted at retail investors, real estate investors, and the blockchain community; counterparties are typically property buyers or investors, and the platform usually integrates KYC or compliance procedures.

Success point: Standardized the commercial process for transferring ownership (LLC and NFT), resolving the integration point between on-chain transactions and traditional land registration, improving transaction efficiency, and enabling on-chain financing.

Risk point: If the original mortgage or lien is not clearly resolved, or if the lender does not consent to the on-chain transfer, legal validity may be compromised. The mortgage or lien must be settled or written consent obtained prior to on-chain registration. Ensure that all mortgages/claims are cleared or written approval is secured before on-chain registration.

1.6.4 Harbor (A Case Study of Failure in a Student Housing Project)

Harbor's early 2019 initiative to tokenize real estate projects such as student dormitories, like The Hub at Co

Lumbia), but the corresponding tokenization plan was forced to be canceled or restructured due to conflicts with existing lender terms and collateral/priority issues, serving as a cautionary case in the implementation of tokenization.

- Real estate value [9]: $20M

- Token Issuance: Due to the cancellation of the plan, there is no final issuance amount or actual circulating supply of tokens.

- Annual net rental income: Project incomplete; no publicly available actual distribution data

- Investor Return Rate: Not yet issued; no historical return data available

- Payment Method: A tokenized REIT was planned, expected to combine fiat and on-chain settlement, but the proposal was withdrawn before implementation, and details have not been fully disclosed.

- Investor sourcing: Originally planned for qualified or institutional investors and platform users; however, as the offering was not completed, no actual investor composition data is available.

Lessons learned: Before proceeding with real estate tokenization, you must first obtain consent from all existing creditors, restructure debt, or legally establish a clear priority order; otherwise, even the best technical solution may be invalidated by creditor laws or security interest priorities.

02 Fixed Income RWA (Ondo Finance): Product Design, Risk Management, and Institutional Investor Engagement Logic

2.1 Background and Industry Positioning

In the RWA (Real-World Assets) sector, fixed-income assets—particularly U.S. Treasuries and short-term government securities—are regarded as on-chain safe havens due to their high credit ratings and low yield volatility, compared to real estate, private equity, or supply chain finance. Ondo Finance is one of the pioneers in this space, with its flagship products USDY and OUSG catering respectively to broader investor access and a qualified investor-only channel. In June 2025, media reports revealed that OUSG had reached approximately $6.93 billion in volume on the ONDO platform, demonstrating the scalability potential of fixed-income RWA[1].

The core value of this model lies in taking highly standardized, credit-grade government bonds off-chain, structuring and tokenizing them via an SPV and smart contracts, and connecting them to on-chain liquidity pools—thereby achieving three key benefits: enhanced liquidity, lowered investment barriers, and access to compliant assets.

2.2 Product Design Structure

2.2.1 Product Categories and Target Audience

- USDY: Designed for non-accredited investors and global users, backed by U.S. Treasury bills and bank deposits, with a variable annualized yield.

- OUSG: Designed for qualified purchasers in the United States, focusing on U.S. government short-term bonds with an emphasis on extremely high credit ratings and low risk [10].

2.2.2 Structural Diagram

Select the following structure:

- Underlying asset → U.S. Treasuries or short-term government securities (such as T-Bills)

- Custodian and audit institution (underlying entity, such as BlackRock’s BUIDL fund in traditional asset management)

- SPV / Trust structure established to hold underlying assets

- On-chain issuance of tokens (USDY or OUSG)—token holders have rights to the underlying asset's returns but do not hold direct ownership.

- Smart contract configuration for minting/redemption mechanism + yield distribution mechanism (e.g., daily or weekly interest accrual)

- Secondary market or platform market-making mechanisms enhance liquidity.

2.2.3 Institutional Participation Logic

Institutional drivers for participating in fixed-income RWA include: first, traditional capital seeks to maintain on-chain allocations without sacrificing low-risk returns; second, asset managers gain access to transparent, traceable, and low-friction issuance channels on-chain. For Ondo, its compliance background, custody arrangements, and partnerships with prominent asset managers such as BlackRock and Franklin Templeton enhance institutional trust. [2] Additionally, tokenized government bonds can serve as collateral in the DeFi ecosystem, improving capital efficiency.

2.3 Risk Management and Compliance Mechanisms

In fixed-income RWA products, risk control and compliance mechanisms fundamentally form the core prerequisite for institutional investor acceptance. Based on current U.S. practices, these products typically use U.S. government short-term securities as underlying assets, resulting in extremely low credit risk—a key advantage distinguishing them from on-chain native assets. Meanwhile, the yield settlement mechanism is automatically executed via smart contracts, reducing operational risks while significantly enhancing transparency and auditability. Combined with custodial banking and third-party audit protocols, this ensures a one-to-one correspondence between underlying assets and tokens, establishing a dual layer of assurance at the institutional level: authentic asset existence paired with trustworthy on-chain representation.

From a structured risk management perspective, its core is not a single measure, but a dual-track system combining on-chain trigger mechanisms with traditional financial regulation. Specifically, regarding asset coverage, a rigid requirement ensures that the ratio of underlying assets to tokens is no less than 1:1, complemented by a Proof-of-Reserve mechanism for on-chain verifiability, backed by audits from custodial banks. For liquidity management, it relies on 24/7 minting and redemption mechanisms alongside market maker commitments, with all processes recorded on-chain to ensure full traceability. In investor eligibility control, it integrates KYC/AML protocols with accredited investor frameworks alongside a whitelist system to align on-chain access management with U.S. securities regulations (e.g., SEC frameworks). On the technical level, risks at the protocol layer are mitigated through smart contract audits, multi-signature governance, and the on-chain publication of audit reports. Additionally, in all collateral and liquidity usage scenarios, every collateralization action is transparently recorded on-chain and disclosed by the platform to prevent the accumulation of hidden leverage risk.

From a compliance perspective, such token issuances typically rely on the Reg D and Reg S frameworks under U.S. securities law, using private placement exemptions to avoid registration requirements for public offerings, while strictly limiting the investor base and disclosure obligations; underlying asset custody must comply with banking regulatory standards and be verified through regular audits to ensure asset authenticity and independence; in designing trading and exit mechanisms, on-chain transfers are not entirely unrestricted but incorporate investor eligibility checks and compliance restrictions, thereby achieving a dynamic balance between liquidity and regulatory requirements.

Looking at the big picture, the essence of the current RWA risk management system is to transform the credit intermediation and audit trust mechanisms from traditional finance into an on-chain, verifiable structure with automated rule enforcement. This model does not weaken regulation; rather, it enhances regulatory enforcement at the technological level. However, it is important to note that risks have not disappeared—they have shifted from being primarily credit-related to being dominated by structural and compliance execution risks, such as custodian failure, discrepancies between on-chain data and real-world assets, or uncertainties arising from changes in regulatory policies. Therefore, whether RWA can achieve large-scale institutional adoption in the future depends not on technological maturity, but on the long-term stability and regulatory feasibility of this integrated on-chain and off-chain risk management framework.

2.4 Yield Model and Quantitative Analysis

In the fixed-income RWA framework, the core logic of the yield model remains rooted in traditional finance but achieves higher efficiency in yield redistribution and liquidity enhancement through on-chain structures. RWA products such as Ondo Finance’s Treasury-backed offerings derive their returns primarily from underlying U.S. Treasury interest, supplemented by structural premiums generated from pool operational efficiency and liquidity premiums enabled by on-chain secondary markets. Actual data shows that in 2024, the annualized yields for USDY and OUSG products ranged between 4.6% and 5.4%[3], a level that significantly exceeds most traditional money market funds under current interest rate conditions and highlights the cost compression and distribution efficiency advantages of on-chain assets. More importantly, by tokenizing these previously institutionally confined yield-generating assets, such products repackage them to serve both retail and accredited investors, thereby creating additional market expansion value beyond their yield structure.

From a cost and structural perspective, on-chain notes exhibit a distinctly lightweight profile compared to traditional MMFs or bond funds. On one hand, management fees are significantly reduced, reflecting the compression of intermediary layers; on the other, the on-chain minting-redemption-trading mechanism substantially improves capital turnover efficiency, allowing investors to unlock liquidity via secondary markets without relying entirely on fund redemption windows. This quasi-real-time liquidity represents a structural transformation of traditional assets by DeFi mechanisms—its significance lies not in higher yields, but in enhanced capital efficiency and asset composability. In other words, the competitiveness of RWA is shifting from delivering higher returns to offering superior efficiency under comparable risk.

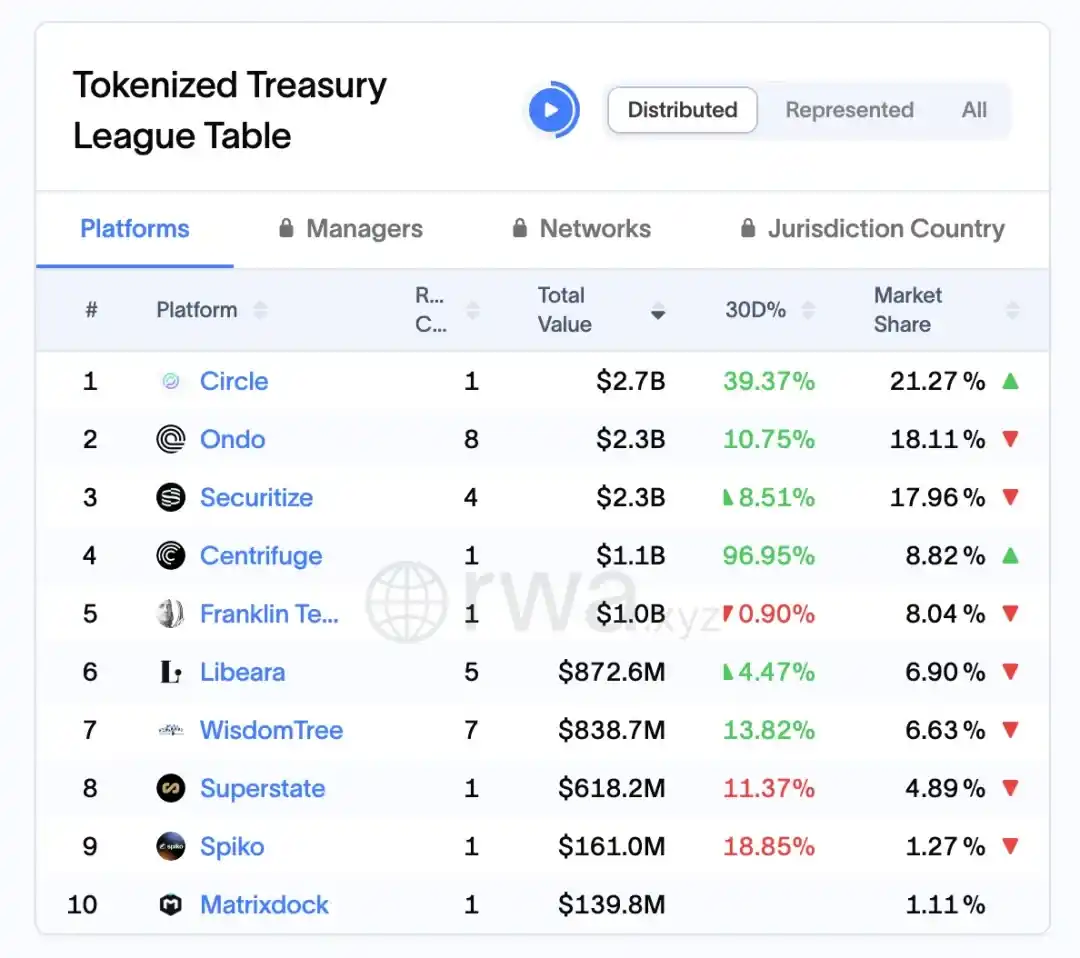

According to data from the RWA.xyz platform, as of April 1, 2026, Ondo had approximately $2.3 billion in assets locked in the U.S. Treasury RWA market, holding a market share of about 18.11%, making it one of the leading players in this niche segment.

Figure 7: Market Capitalization and Market Share of the Top 10 Global RWA Issuance Protocols (as of April 1, 2026)

Source: rwa.xyz/treasuries, Pharos Research

2.5 Institutional Participation and Secondary Mechanisms

As the fixed-income RWA ecosystem gradually matures, the participation pathways for institutional investors and the construction of secondary market mechanisms have become critical variables determining product scale and liquidity. Drawing from Ondo Finance’s practice, its core strategy is not merely to inject institutional capital, but rather to design a structure that bridges offline asset management with on-chain liquidity expression, effectively connecting traditional asset managers and custodian banks with on-chain investors—thereby enabling dual expansion of funding sources and asset supply. In this model, institutions primarily assume responsibilities such as underlying asset selection, portfolio management, and compliant custody, while the on-chain layer handles share fragmentation, liquidity release, and investor distribution, forming a new type of collaborative relationship characterized by functional decoupling yet risk interdependence. This structure allows RWA products to meet institutional demands for security and compliance while accommodating on-chain users’ needs for flexibility and tradability.

Looking further, the secondary market mechanism is the core driver behind the transformation of RWA from fund-like products into tradable asset classes. Secondary trading mechanisms enhance token liquidity and improve asset fundraising effectiveness. Ondo’s Nexus platform, for instance, enables a mint-and-redeem mechanism that boosts liquidity[2]. This mechanism fundamentally reshapes the traditional fund model, where liquidity is driven by subscription and redemption, allowing investors to transfer shares on-chain through order matching rather than relying entirely on issuers to provide liquidity exit routes, thereby significantly shortening the capital exit cycle. Meanwhile, the introduction of market-making mechanisms and liquidity pools has also mitigated, to some extent, the liquidity discount caused by price volatility, enabling RWA assets to gradually develop trading characteristics similar to bond ETFs.

On a deeper level, there is a clear positive feedback loop between institutional participation and secondary market mechanisms: institutional entry enhances the quality and stability of underlying assets, thereby boosting market confidence; in turn, more efficient secondary liquidity increases institutional allocation intent and capital turnover efficiency. Once this cycle is established, it will propel the RWA market into a phase of scalable growth. However, it is important to note that this model still depends on strict regulatory boundaries and investor access mechanisms—particularly under the U.S. regulatory framework, where secondary trading is often constrained by transfer restrictions and accredited investor rules, limiting the realization of fully unrestricted liquidity.

The secondary mechanism currently built by Ondo is essentially an attempt to create on-chain infrastructure for a fixed-income market. Its significance lies not only in enhancing the liquidity of individual products but also in providing a unified trading and pricing framework for diverse RWA assets. If this mechanism continues to evolve and gradually incorporates more market makers, structured products, and interest rate derivatives, the RWA market could transform from a passive yield asset pool into a fully-fledged on-chain bond market with a complete yield curve and risk stratification. At that point, institutional participation will no longer be an incremental factor but will become a core component of market operations.

2.6 Challenges, Trends, and Implications for the Hong Kong Market

From a broader perspective, although the RWA sector in the United States has validated feasible pathways for asset tokenization, its development still faces multiple structural constraints, including an incomplete regulatory framework, complex legal alignment between on-chain and off-chain ownership, dependence on a limited number of platforms for liquidity, and inconsistent transparency of underlying assets. Meanwhile, the market is gradually forming clear trends: first, asset types are expanding from standardized instruments like short-term Treasuries to more complex categories such as credit assets and private fund shares; second, compliance infrastructure—including KYC/AML, custody, and auditing—is continuously strengthening; third, leading institutions are accelerating their entry to drive scalable growth. Against this backdrop, if China and Hong Kong aim to seize the opportunities in RWA development, they should focus on two fronts: institutional support and practical use case implementation. For instance, leveraging Hong Kong’s strengths in international finance and regulatory coordination, they could pioneer compliant tokenized issuance and cross-border circulation mechanisms, while establishing higher standards in asset selection, disclosure, and investor protection to achieve innovative breakthroughs under controlled risk.

03 Supply Chain Finance RWA (Centrifuge): Core Enterprise Authentication, Improved Financing Efficiency for SMEs, and Risk Mitigation

3.1 Overview: Structural Innovations of RWA in Supply Chain Finance

Among existing RWA practices, supply chain finance represents a scenario with greater real-world complexity, presenting significantly higher challenges for transformation than real estate or government bond assets—yet this very complexity lends it greater structural innovation potential. From my observations, the core issues in traditional supply chain finance consistently revolve around three key terms: information asymmetry, broken credit transmission, and low financing efficiency—even when small and medium-sized enterprises hold genuine accounts receivable, they still struggle to secure low-cost funding. The introduction of RWA is not merely about tokenizing receivables on-chain; rather, it involves a comprehensive structural reconfiguration that dismantles the bank-dominated credit intermediary system into an on-chain combination of asset ownership verification, risk tranching, and liquidity matching. In this process, models like Centrifuge offer a relatively clear pathway: on one hand, receivables are standardized and encapsulated via SPVs or legal agreements, endowing them with verifiable, transferable underlying asset characteristics; on the other hand, layered financing structures such as Tinlake are introduced to divide the asset pool into different risk tiers (e.g., Senior/Junior Tranches), thereby attracting capital with varying risk appetites. This design essentially replicates and optimizes the traditional ABS (asset-backed securities) logic on-chain, but its key distinction lies in blockchain’s ability to provide more frequent and transparent asset status updates, enabling capital providers to assess risk more dynamically rather than relying solely on periodic disclosures. Furthermore, the integration of DeFi liquidity (e.g., stablecoin financing provided by MakerDAO) further transforms the funding structure, moving supply chain financing beyond the confines of bank balance sheets and connecting it to global on-chain capital pools. In essence, RWA’s true innovation in this space is not merely improving financing efficiency—it is attempting to reshape the fundamental mechanisms by which credit is disaggregated, priced, and circulated. This is precisely what makes this sector more noteworthy than other RWA verticals.

3.2 Centrifuge Platform Design Logic: Tinlake Model and SPV Mechanism

Centrifuge’s Tinlake model is structured around off-chain SPVs holding real-world assets, with on-chain tokens representing beneficial ownership. Its key innovation lies in a dual-token structure that enables risk tranching: TIN tokens absorb junior risk, while DROP tokens provide senior investors with stable returns.

This structure creates credit tranches similar to traditional asset securitization, but with greater on-chain transparency in liquidity and audit mechanisms.

Chart description: This structure ensures full compliance throughout the process, from offline ownership verification of RWA assets to their on-chain liquidity. The SPV legally isolates risk, the NFT ownership mechanism prevents double pledging, and the layered token design enables investors with varying risk appetites to participate.

3.3 Cooperation Mechanism with MakerDAO: Stablecoin Liquidity Injection

Within the entire RWA supply chain ecosystem, if Centrifuge addresses the question of how assets are tokenized and layered, then its integration with MakerDAO further answers a more critical question—how these assets can truly secure a continuous, scalable source of funding. In practice, this collaboration is not merely a simple protocol integration, but rather a systematic effort to migrate traditional factoring finance logic onto the blockchain.

Specifically, Centrifuge enables assets representing low-risk senior cash flows, generated as DROP tokens on Tinlake, to be directly used as collateral in MakerDAO’s collateralization system for minting stablecoins. The core significance of this design lies in establishing a direct conversion pathway between real-world assets and on-chain credit money (DAI), allowing supply chain finance to move away from reliance on banks or private credit funding and instead connect to a more open on-chain liquidity pool. In other words, asset owners are not merely gaining an additional financing channel—they are experiencing a fundamental transformation in their source of capital.

From a structural perspective, this mechanism can be understood as a progressive path of abstraction and enhanced liquidity: real assets → DROP → DAI → secondary market. Each transformation step involves standardization of asset form and increased liquidity: receivables are first tokenized as NFTs to establish ownership, then converted via a layered structure into tradable ERC-20 tokens (DROP/TIN), subsequently unlocked as the stablecoin DAI through the MakerDAO system, and finally circulated and reallocated across the broader DeFi market. It is through this process that traditionally closed credit assets in conventional finance gain composability for the first time, enabling integration into more complex on-chain financial structures.

Of course, the viability of this mechanism relies on the combined effect of multiple risk mitigation measures. On one hand, Centrifuge prioritizes risk allocation to TIN holders through a layered structure, providing a credit buffer for DROP; on the other hand, MakerDAO enforces a high collateralization ratio for DROP and complements it with a liquidation mechanism to control systemic risk. Additionally, the underlying assets still depend on SPV structures, audits, and legal constraints to ensure actual repayments, meaning that on-chain credit remains tied to the real-world legal system, forming a hybrid model of combined on-chain and off-chain enforcement.

From my perspective, the true innovation of this collaboration lies not merely in introducing stablecoin liquidity to RWA, but in fundamentally attempting to build a new pathway for credit transmission: credit is no longer entirely dependent on bank balance sheets, but is gradually segmented and repriced on-chain through asset tranching, protocol-backed collateral, and market pricing. Once mature, this mechanism could extend beyond supply chain finance to a broader range of real-world assets.

3.4 Case Study: New Silver and HarborTrade

(1) New Silver Case: Real Estate Renovation Loan RWA New Silver is a U.S.-based short-term real estate financing institution that tokenizes home renovation loans as NFTs via the Centrifuge platform, with an average loan amount of $100,000–$250,000 per transaction. Once assets are deposited into the Tinlake pool, DROP investors can earn a stable annualized return of 6–9%. Project data[11] shows that, as of the end of 2024, cumulative disbursements exceeded $50 million, with an extremely low default rate (historically ranging from 0–2%; for precise figures, refer to the issuer’s loan-level default schedule or third-party audit report).

(2) HarborTrade Case: RWA Tokenization of International Trade Accounts Receivable HarborTrade integrates an RWA structure into trade finance, with the core asset being the exporter’s accounts receivable. [12] After generating NFT certificates via the Centrifuge system, DROP investor funds flow directly to the exporter through an SPV, reducing the financing disbursement cycle from weeks to a single week or less (specific projects can achieve 1–2 weeks, subject to project-specific cash flow verification).

3.5 Asset Ownership Verification, Risk Control, and On-Chain Monitoring Logic

Centrifuge employs a dual-track mechanism combining on-chain real-time monitoring with off-chain legal verification. The foundational documents for each asset—contracts, invoices, and payment records—are verified by third-party audit institutions and hashed onto the blockchain. The system includes an Oracle monitoring module that automatically triggers liquidation procedures in the event of asset default, delayed payments, or collateral depreciation.

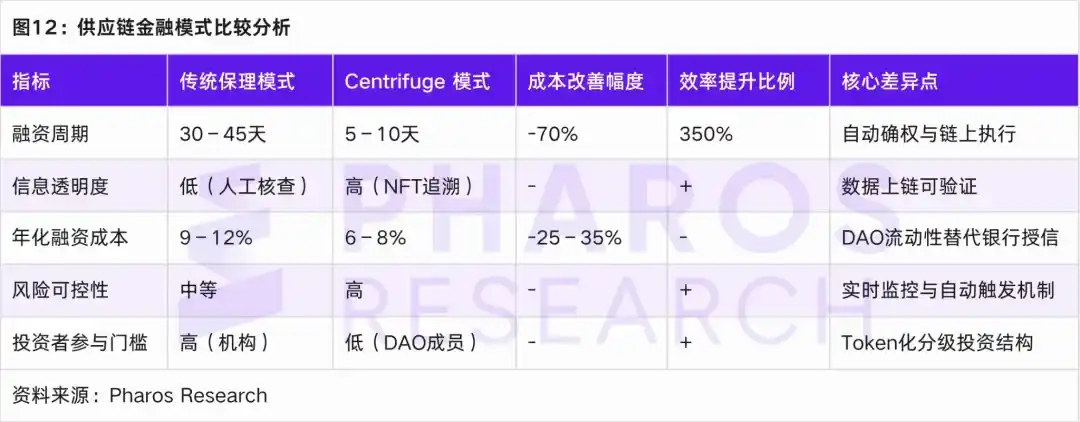

3.6 Comparison of Efficiency and Cost with Traditional Supply Chain Finance

Compared to traditional factoring models, RWA demonstrates significant advantages in financing cycles, information transparency, funding costs, and default control through the Centrifuge model.

04 Pre-IPO Equity RWA: Asset Compliance, Transfer Restrictions, and Valuation Pricing Mechanism

4.1 Market Context and Institutional Logic of Pre-IPO Equity RWA

In the previous analysis of real estate, fixed income, and supply chain finance RWA, a common underlying logic is evident: transforming traditionally illiquid real-world assets into financial products with separable, tradable, and programmable features through asset ownership verification, structural packaging, and on-chain circulation. RWA in the form of pre-IPO equity follows this same logic, but with significantly greater complexity and regulatory constraints; its core challenge is no longer merely putting assets on-chain, but rather achieving compliant digital representation and limited liquidity release of private equity within the strict framework of U.S. securities regulation.

From a market perspective, with the rise of compliant tokenization platforms such as Securitize, Arca Labs, and Republic, traditionally illiquid equity holdings held by conventional VC/PE firms are now gaining a technological pathway to fractionalization and securitization via blockchain—essentially structuring and splitting primary-market equity interests while introducing secondary-market-like mechanisms within a regulated environment. However, unlike assets such as RealT or Ondo, Pre-IPO equity faces stricter risk pricing, disclosure requirements, and transfer restrictions, making its institutional design heavily reliant on the U.S. securities law exemption framework. In terms of practical implementation, the market has gradually evolved into a compliance triad centered on Reg D, Reg A+, and Reg CF: Reg D (Rule 506(c)) targets accredited high-net-worth investors and serves as the primary channel for large-scale financing and institutional participation, characterized by high issuance efficiency but limited liquidity (typically requiring a one-year lock-up period); Reg A+ (Tier 2) partially opens participation to retail investors, balancing fundraising scale with compliance disclosure obligations and enabling limited tradability on Alternative Trading Systems (ATS); Reg CF emphasizes decentralized participation and risk control—not merely lowering entry barriers, but dynamically constraining annual investment limits per investor, positioning it as a user engagement layer or community equity pool, a logic somewhat analogous to the subordinated capital mechanism in supply chain finance RWA. From case studies, mainstream Pre-IPO RWA projects typically adopt a two-tier structure: upper-tier fundraising via Reg D/Reg S combined with lower-tier user participation via Reg CF, effectively balancing fundraising efficiency with community expansion—an approach highly consistent with the structural layering trend mentioned earlier. Thus, Pre-IPO equity RWA is not a simple replication of the on-chain pathways used for real estate or bond assets; rather, it represents an institutional correction to the liquidity challenges of traditional private equity under stricter regulatory constraints. Its core value lies in enhancing asset accessibility and liquidity efficiency through on-chain technology without violating the fundamental boundaries of securities law—its developmental boundaries remain firmly defined by the regulatory framework.

4.2 Case Studies of Representative Platforms: Securitize, Arca Labs, and Republic

From a practical perspective, three representative platforms—Securitize, Arca Labs, and Republic—correspond to three distinct paradigms: infrastructure-driven, fund-structure-restructured, and crowdfunding-inclusive models. First, Securitize functions more like the underlying operating system of the digital securities era, integrating issuance, registration, compliance, and trading (ATS) into a unified system, thereby modularizing and on-chainizing the traditionally fragmented private equity process, enabling Pre-IPO equity to become programmatically tradable. Its Pre-IPO Equity Token Program essentially allows companies to unlock partial liquidity prior to their IPO, while strictly limiting investor eligibility through frameworks such as Regulation D, achieving a balance between efficiency and compliance. Second, Arca Labs restructures assets at the structural level by embedding Pre-IPO equity within a fund vehicle, using NAV (net asset value) mechanisms to create a quasi-public fund-like expression. The key advantage of this model lies not in the liquidity of individual assets but in portfolio-level risk diversification and valuation smoothing—effectively mirroring traditional asset management logic on-chain. Finally, Republic represents an alternative path: leveraging the Regulation CF framework to lower participation barriers and extend Pre-IPO investment access from high-net-worth individuals to retail investors. By utilizing blockchain for automated equity registration and dividend distribution, Republic enables feasible, small-scale, diversified, and decentralized investment structures—though it inherently faces greater liquidity constraints and heightened disclosure obligations.

From the author’s perspective, these three models are not in competition but collectively form a layered market structure for Pre-IPO equity RWA: Securitize addresses the question of regulatory compliance for trading, Arca Labs optimizes pricing and holding mechanisms, and Republic explores the boundaries of participant eligibility. Together, they point to a central proposition: how to gently restructure traditional equity liquidity through technological means without crossing the boundaries of securities regulation. This restructuring does not eliminate illiquidity entirely but achieves controlled liquidity through lock-up periods, investor tiering, and secondary market access mechanisms—this controlled liquidity is the defining characteristic that distinguishes Pre-IPO RWA from other asset classes.

4.3 Valuation Pricing and Holding Period Mechanism

The greatest challenge in valuing pre-IPO equity stems from its inherent illiquidity and information asymmetry. To effectively address these challenges, RWA tokenization projects employ dynamic net asset value (NAV) models and verifiable reporting mechanisms for valuation and risk mitigation. In this space, leading platforms commonly adopt three valuation approaches to accommodate diverse market demands and valuation scenarios.

First, milestone valuation is a common valuation method that dynamically adjusts valuation based on a company’s growth stage, such as funding rounds and revenue growth. This approach is particularly suitable for early-stage growth companies, as it accurately reflects evolving valuations over time. Second, the comparable companies method determines a relatively reasonable market valuation for a Pre-IPO company by comparing valuation multiples of publicly traded peers in the same industry. This method emphasizes market-driven factors and can flexibly reflect the impact of changing market conditions. Finally, the on-chain NAV oracle method involves independent audit institutions periodically recording a company’s net asset value on the blockchain, ensuring transparency and traceability of valuation. This method is applicable to valuation updates throughout a company’s entire lifecycle and can reflect asset changes in real time, although it entails higher audit costs.

These valuation approaches do not operate in isolation but are combined based on project characteristics and market demand. For example, stage-based valuation and comparable company analysis are often used for early- and mid-stage projects, offering flexible and market-driven valuations. Meanwhile, blockchain net asset value synchronization provides transparent and reliable valuation support for mature, illiquid assets.

By combining these valuation methods, RWA platforms can not only enhance the accuracy of valuations but also increase investor confidence in projects, thereby promoting healthy market development. Additionally, these valuation models provide investors with multi-dimensional risk assessment criteria, enabling them to better understand the risk-return profile of projects in complex investment environments.

4.4 Liquidity Mechanism and Transfer Restrictions

In the previous analysis, we examined the core structures and compliance pathways of different asset types, such as real estate RWA (RealT), fixed-income RWA (Ondo Finance), and supply chain finance RWA (Centrifuge). In comparison, the liquidity mechanisms and transfer restrictions for Pre-IPO equity RWA are more complex, primarily constrained by lock-up periods, investor accreditation requirements, and regulatory exemption conditions. For example, with Securitize, tokenized shares must observe a minimum 12-month lock-up period before they can be transferred on a corresponding regulated ATS. This process reflects the stringent regulations that Pre-IPO equity RWA must follow in the release of liquidity.

To enhance liquidity, the key to Pre-IPO equity RWA lies in establishing a compliant and efficient transfer mechanism. First, a regulatory-recognized token registration system enables asset circulation across platforms while ensuring compliance. Second, cross-platform identity verification (KYC Passporting) allows investors’ identities to be validated across platforms, ensuring regulatory adherence. Finally, an on-chain compliance routing mechanism (Compliance Layer Smart Contract) automatically enforces all compliance requirements during transfers, reducing the risk of human error.

Combining the above mechanisms, the process for Pre-IPO equity RWA from private placement to compliant trading typically follows this path:

(1) During the lock-up period, tokens are non-transferable; investors must complete KYC verification but cannot trade on any market, resulting in complete liquidity freeze.

(2) After the lock-up period, tokens can be traded on regulated ATS markets such as Securitize Markets and tZERO, still requiring KYC and AML reviews to ensure buyer compliance. However, liquidity remains somewhat constrained due to insufficient market depth and a limited pool of buyers.

(3) During the public offering conversion phase, tokens may be converted into public market assets after meeting SEC disclosure requirements and obtaining Reg A+ approval, making them available to a broader investor base; however, this process often results in delayed liquidity release due to approval delays.

Through these layered compliance measures, Pre-IPO equity RWA can gradually unlock liquidity while ensuring compliance. However, this process also highlights the complexity and cyclical nature of liquidity release for assets within a regulatory framework.

Through the design of this liquidity mechanism and transfer restrictions, the market development of Pre-IPO equity RWA will gradually enhance asset liquidity while meeting regulatory requirements, advancing its marketization process.

4.5 Investment Returns and Holding Period Analysis

In pre-IPO equity RWA, the investment horizon typically ranges from 3 to 7 years. Based on historical data from the Securitize and Republic platforms [14], investors' internal rate of return (IRR) has ranged between 12% and 25%, albeit with significant volatility. With the emergence of on-chain structured products, yield tranching designs are now being widely adopted:

(1) Senior Layer (Priority Tokens): Tokens in this layer typically offer stable dividends and are suitable for institutional investors with low risk tolerance, with a typical holding period of 2 to 3 years [15] and an annualized yield between 8% and 12%.

(2) Mezzanine Layer (Mezzanine Tokens): Assumes moderate risk, suitable for investors with medium risk tolerance, offering an annualized yield of 15% to 20%[16], with a typical holding period of 3 to 5 years.

(3) Equity Layer (Equity Tokens): Tokens at this layer carry higher investment risk and are primarily targeted at risk-tolerant investors, with annualized returns exceeding 25%[17] and typical holding periods of 5 to 7 years.

This hierarchical design not only attracts institutional investors with varying risk appetites but also provides a more flexible product structure for the tokenized secondary market, better meeting diverse market demands.

This structured design not only optimizes the alignment of risk and return for different types of investors but also effectively enhances asset liquidity, paving the way for diversified development in capital markets.

05 Conclusion

Based on research into early U.S. RWA case studies, RWA as an on-chain asset class is continuously breaking down the boundaries between traditional finance and blockchain, demonstrating profound innovative potential across multiple domains. RealT, a real estate RWA, enables fractional ownership of traditional real estate assets through SPV structuring and tokenization, significantly lowering investment barriers while ensuring market legitimacy through a compliant framework. Ondo Finance tokenizes U.S. Treasury bonds as underlying assets, leveraging smart contracts and SPV architecture to bring fixed-income products on-chain, allowing investors to participate in the fixed-income market with low risk and high liquidity. Centrifuge transforms the traditional bank-dependent credit system into a blockchain-based decentralized structure through its supply chain finance RWA project, enhancing financing efficiency and reducing costs.

However, despite providing valuable insights and innovative pathways for the development of the RWA market, these projects face numerous challenges. For instance, high costs of regulatory disclosure, cross-border custody compliance issues, and stablecoin peg risks remain key bottlenecks to the continued growth of RWA. Particularly in terms of regulation, although all major platforms have designed their offerings with compliance in mind, stringent requirements under U.S. securities law still limit the liquidity of certain products. For example, liquidity mechanisms and transfer restrictions for Pre-IPO equity RWA must strike a balance between regulatory compliance and market demand, especially under lock-up periods and secondary market constraints, making full liquidity liberalization difficult to achieve.

Although the technical framework and compliance design for RWA have made certain progress in the United States, China and Hong Kong, as international financial centers, possess distinct advantages. China’s flexibility in financial technology and innovative regulation can be leveraged to strengthen the integration of blockchain with traditional finance, exploring RWA pathways better suited to its domestic market. As an international financial center, Hong Kong can leverage its mature financial markets and global investor base to facilitate compliant cross-border RWA流通, serving as a vital bridge for the expansion of the global RWA market. Particularly in terms of cross-border liquidity and international investor access, Hong Kong is well-positioned to become a key testing ground and driving force for this emerging asset class.

Overall, although the United States has taken a leading position in the development of RWA, its future scaling faces significant challenges in compliance, liquidity, and other areas. Meanwhile, the openness and innovative capabilities of China and Hong Kong markets may offer new opportunities and perspectives for the further expansion of the global RWA market.

06 Reference Source

[1] Coindesk: Ondo Finance Launches $693M Treasury Token on the XRP Ledger Amid Surging RWA Trend

[2] Ondo.finance: Introducing Ondo Nexus — Delivering Instant Liquidity for Third-Party Tokenized Treasuries, Leveraging Assets from BlackRock, Franklin Templeton, Wellington Management, and WisdomTree

[3] Plume.org: Plume Network Partners with Ondo Finance to Expand Its RWAfi Ecosystem with Tokenized U.S. Treasuries

[4] outliermedia.org: The real estate scheme consuming Detroit, one digital token at a time

https://outliermedia.org/crypto-real-estate-realt-cryptocurrency-detroit/

[5] RealT White Paper - https://realt.co/wp-content/uploads/2019/05/RealToken_White_Paper_US_v03.pdf

[6] Aspentime - https://www.aspentimes.com/trending/in-18-million-deal-nearly-one-fifth-of-st-regis-aspen-sells-through-digital-tokens

[7] Pwco - https://www.pwco.com.sg/insights/blockchain-real-estate-part-iii/

[8] Nftnow - https://nftnow.com/news/roofstock-onchain-origin-story-sell-third-property-via-nft-marketplace/

[9] Harbor Cancels Tokenized REIT of University Dorm 'The Hub at Columbia'

https://tokenist.com/harbor-cancels-tokenized-reit-of-university-dorm-the-hub-at-columbia/

[10] RWA.xyz: https://app.rwa.xyz/assets/OUSG

[11] Gov.centrifuge: https://gov.centrifuge.io/t/cp95-pop-new-silver-ns3/5603

[12] Gov.centrifuge: https://gov.centrifuge.io/t/issuer-harbor-trade-credit/141

[13] U.S. Securities and Exchange Commission: https://www.sec.gov/resources-small-businesses/regulation-crowdfunding-guidance-issuers

[14] State of the Pre-IPO Market -

https://www.hiive.com/market-reports/state-of-the-pre-ipo-market-2026-annual-report

[15] https://www.blueowlcapitalcorporation.com/investors/sec-filings

[16] https://app.rwa.xyz/credit

[17] https://dune.com/discover/content/trending