Author: Dune

Compiled by: Felix, PANews

Recently, Dune partnered with Steakhouse Financial to launch a stablecoin dataset. This dataset covers dimensions such as holder composition, fund flows, on-chain behavior categorization, and velocity, providing a foundation for institutional-grade analysis, research reports, compliance monitoring, and high-level decision-making. Through analysis of the dataset, Dune published insights revealing aspects of the true current state of the stablecoin market. Below are the details.

Everyone is citing stablecoin supply data. It appears in every report, every earnings call, and every policy hearing. But beyond the figure that “supply exceeds $300 billion,” how much do we really know about stablecoins?

Who holds them? How concentrated is ownership? What is their velocity? On which blockchains do they operate? What are their actual use cases? Are they used for DeFi liquidity, payments, or merely as idle capital?

As Meta announces plans to integrate third-party stablecoin payments on its platform; Bridge receives approval from the U.S. Office of the Comptroller of the Currency (OCC) to establish a national trust bank; Payoneer enables stablecoin functionality for 2 million merchants; and Anchorage Digital launches compliant stablecoin services for non-U.S. banks. Institutions and regulators are entering en masse, and what they need goes far deeper than a simple supply figure.

We used Dune’s newly released stablecoin dataset to answer these questions. Here’s what the data reveals:

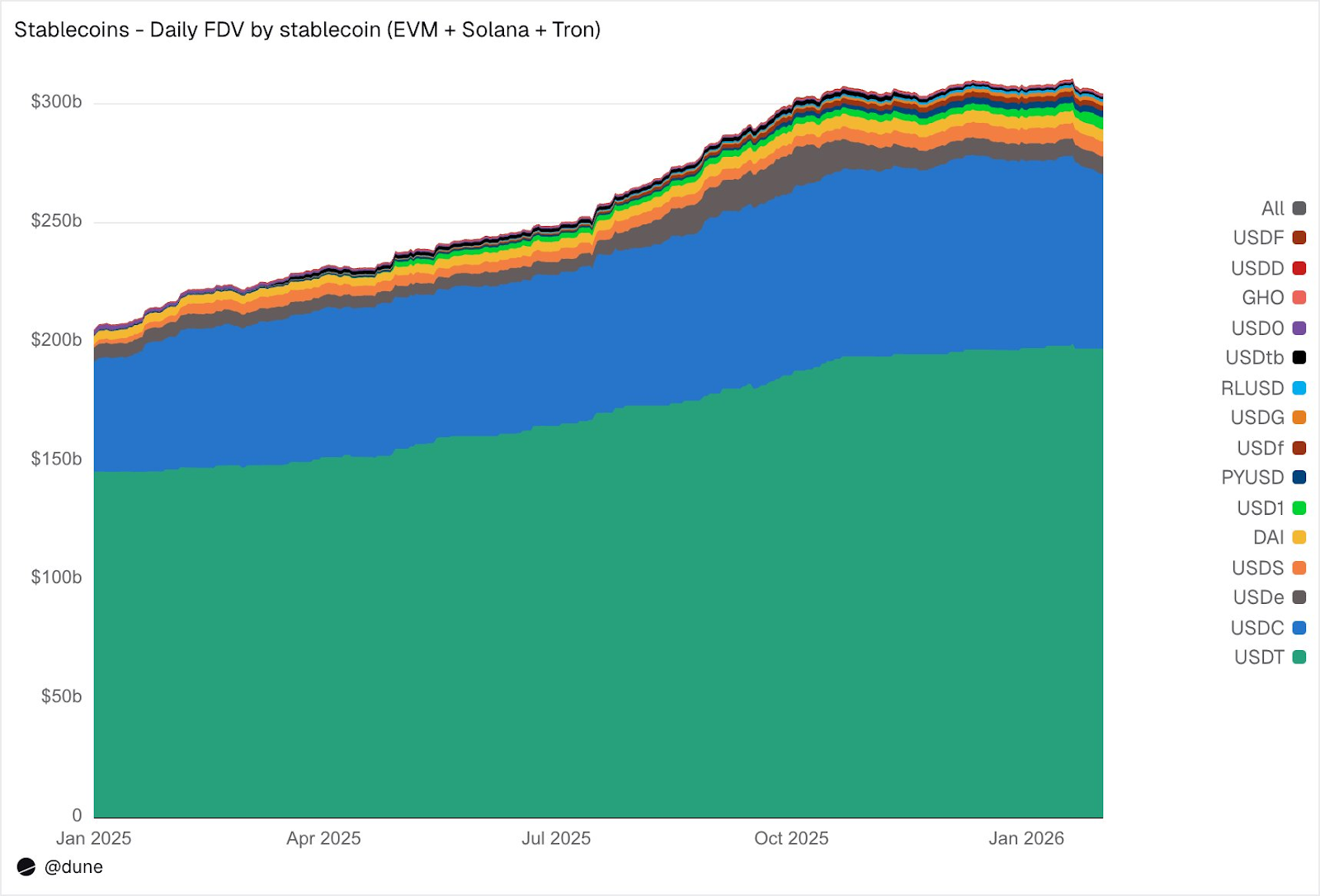

Overview of Supply

As of January 2026, the fully diluted supply of the 15 largest stablecoins on EVM-compatible chains, Solana, and Tron reached $304 billion, a 49% year-over-year increase. Tether’s USDT ($197 billion) and Circle’s USDC ($73 billion) still account for 89% of the market share.

By chain, Ethereum reached $176 billion (58%); Tron reached $84 billion (28%); Solana reached $15 billion (5%); BNB Chain reached $13 billion (4%). Despite the total supply nearly doubling, the distribution across chains has remained nearly unchanged over the past year.

Source: Dune

But beyond the two major stablecoins, 2025 is the "Year of the Challengers." USDS (Sky Ecosystem) saw its market cap grow 376% to $6.3 billion. PYUSD (PayPal) surged 753% to $2.8 billion. RLUSD (Ripple) skyrocketed from $580 million to $1.1 billion, a massive 1,803% increase. USDG's market cap grew 52-fold. And USD1 jumped from zero to $5.1 billion.

But not all challengers achieved growth. USD0 fell 66%, while Ethena’s USDe peaked in October (nearly tripling) and ended the year up 23%. Even so, the group of competitors beneath USDT and USDC still expanded significantly.

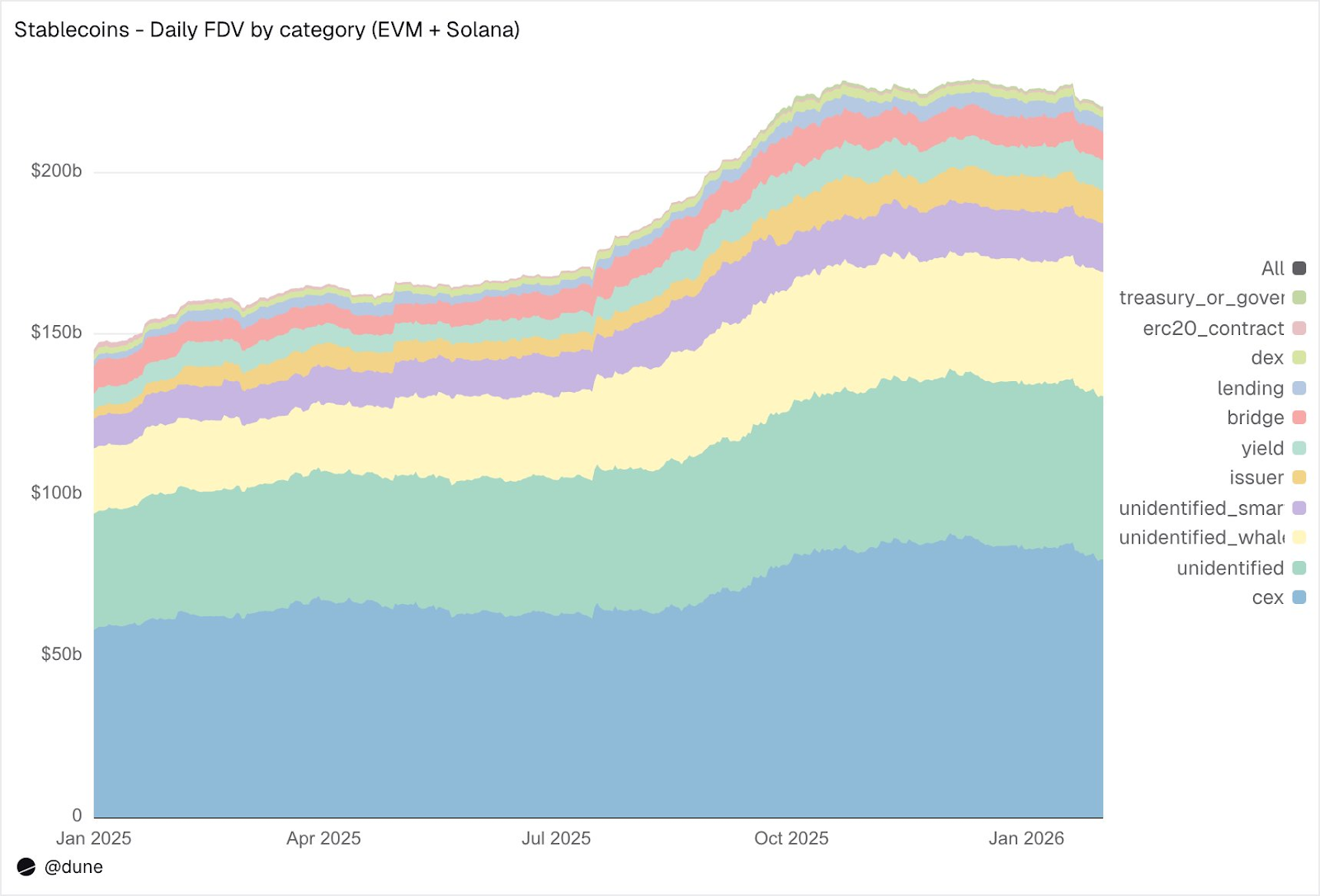

Who holds stablecoins?

Most stablecoin datasets can only tell you the total supply. Because our dataset tracks wallet-level balances and address labels, it can tell you who holds these stablecoins.

Source: Dune

On EVM and Solana, CEXs are the largest known holding category, totaling $80 billion (up from $58 billion last year). The primary function of stablecoins remains as trading and settlement infrastructure for exchanges. Whale wallets hold $39 billion. Yield protocol holdings nearly doubled to $9.3 billion, reflecting growth in on-chain yield strategies. Issuer addresses (treasuries and mint/burn contracts) surged 4.6-fold from $2.2 billion to $10.2 billion, directly reflecting the scale of new supply entering the market.

Regarding label quality: Only 23% of the supply is held in completely unidentifiable addresses. This is an exceptionally high identification rate for on-chain data, and it is crucial for understanding the true sources of risk associated with stablecoins.

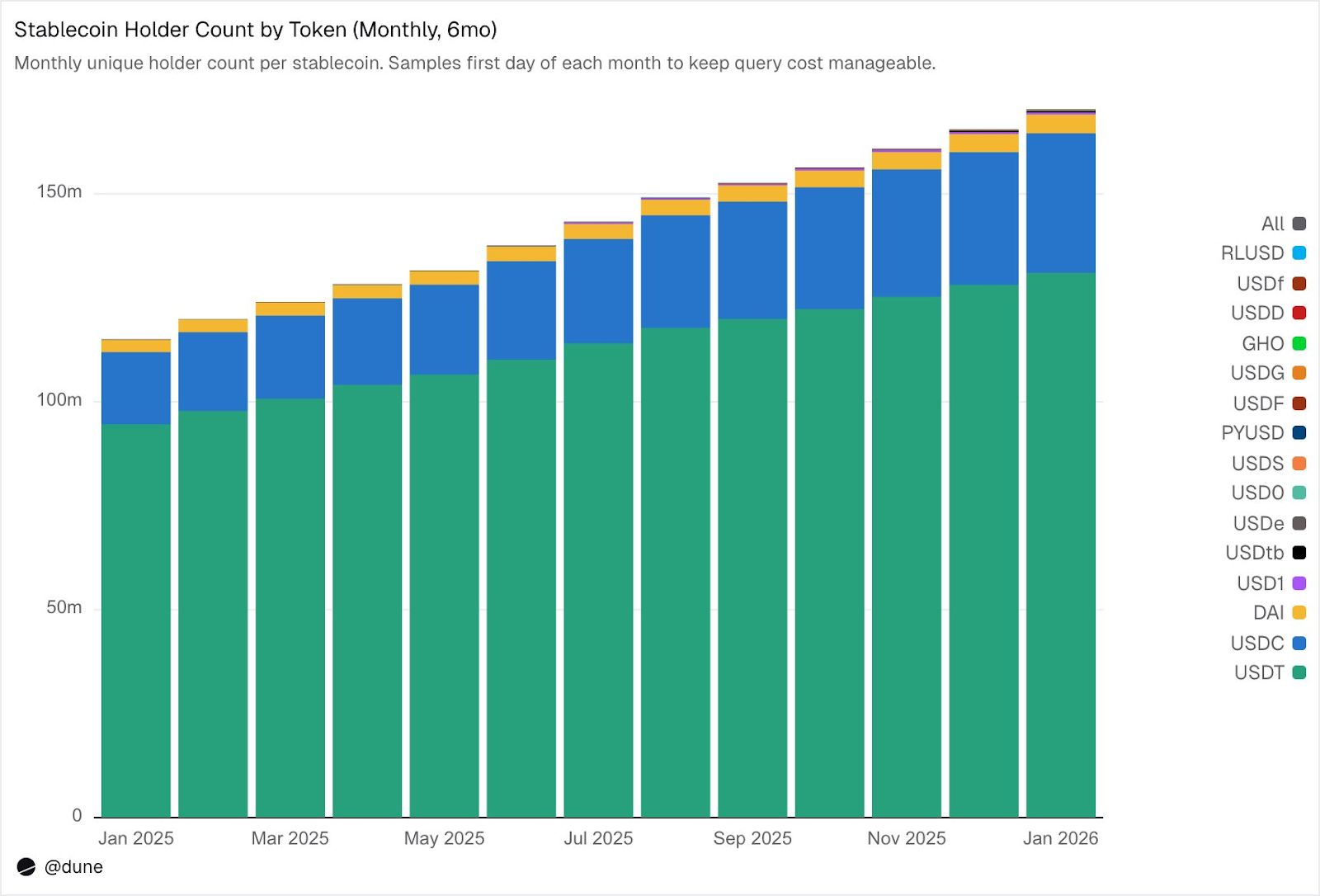

Held by 172 million addresses, but with extremely high concentration

As of February 2026, 172 million unique addresses hold at least one of these 15 stablecoins. Of these, USDT accounts for 136 million, USDC for 36 million, and DAI for 4.7 million. The distribution of these three stablecoins is highly widespread: their top 10 wallets hold only 23–26% of the supply, with HHI (Herfindahl-Hirschman Index, a standard economic measure of concentration, where 0 indicates perfect dispersion and 1.0 indicates a single holder) below 0.03.

Source: Dune

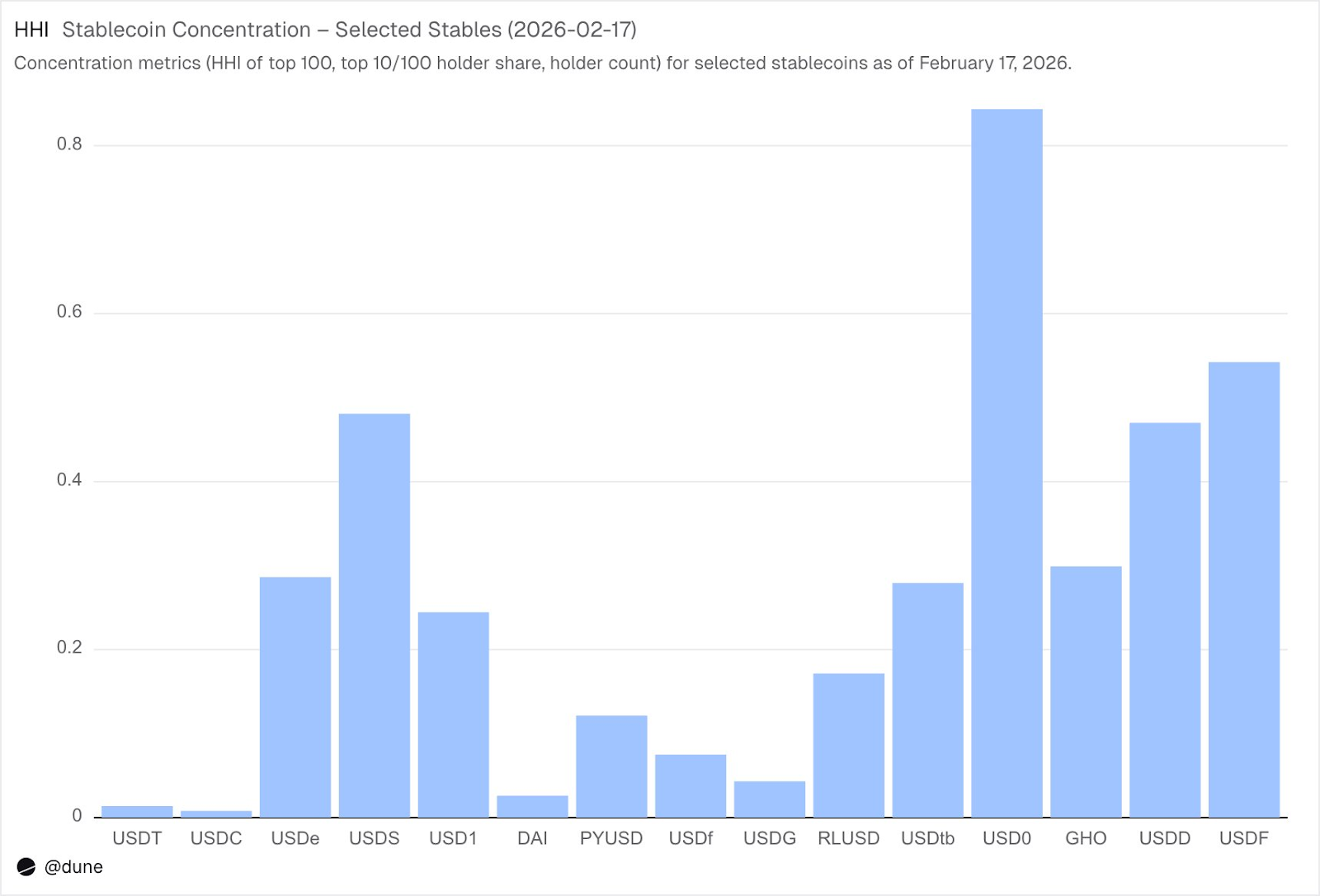

However, the situation is entirely different for other stablecoins. The top 10 wallets hold 60–99% of the supply. USDS, despite a circulating supply of $6.9 billion, has 90% concentrated in just 10 wallets (HHI 0.48); USDF has 99% concentrated in the top 10 (HHI 0.54); and USD0 is the most extreme, with 99% concentrated in the top 10 (HHI 0.84), meaning that even among these large holders, the supply is dominated by one or two wallets.

Source: Dune

This does not mean these stablecoins have issues—some are newer, and others are intentionally structured by institutions. But it does mean their supply data should be treated differently from that of USDT or USDC. Concentration affects de-pegging risk, liquidity depth, and whether supply reflects genuine demand or demand from a small number of large participants. Such analysis is only possible when you have access to the balances of all holders, not just aggregated minting and burning data.

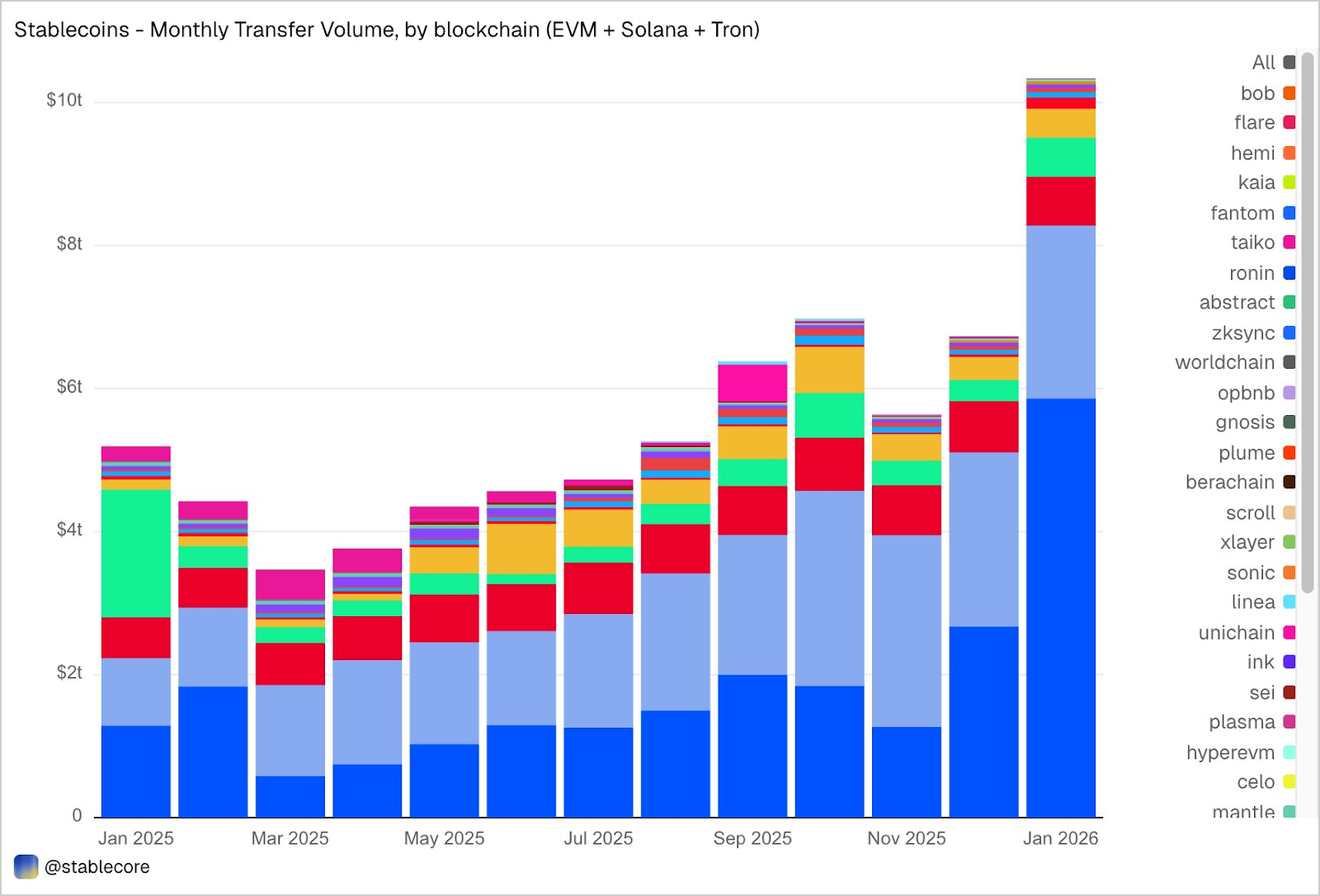

Total transfer volume reached $10.3 trillion in January.

In January, stablecoin transfer volumes on EVM, Solana, and Tron reached $10.3 trillion, more than double the amount in January 2025. The distribution of on-chain transaction volumes is striking and differs significantly from supply shares: Base, with only $4.4 billion in supply, led with $5.9 trillion in transaction volume; Ethereum recorded $2.4 trillion; Tron $682 billion; Solana $544 billion; and BNB Chain $406 billion.

Source: Dune

By token, USDC dominates with $8.3 trillion, nearly five times that of USDT ($1.7 trillion), despite having 2.7 times less supply. USDC clearly has higher transfer volume and frequency than USDT. DAI’s trading volume is $138 billion, USDS is $92 billion, and USD1 is $43 billion.

Importantly, this data is objective and neutral. The dataset does not pre-filter transfers based on a fixed interpretation of what constitutes “real” economic activity, so the total may include traffic related to arbitrage, bots, internal routing, or other automated behaviors. Our goal is to present an objective, comprehensive view of on-chain activity, allowing users to apply their own filtering criteria—such as removing bot-driven volume, isolating organic usage, or defining more accurate metrics for measuring transaction activity.

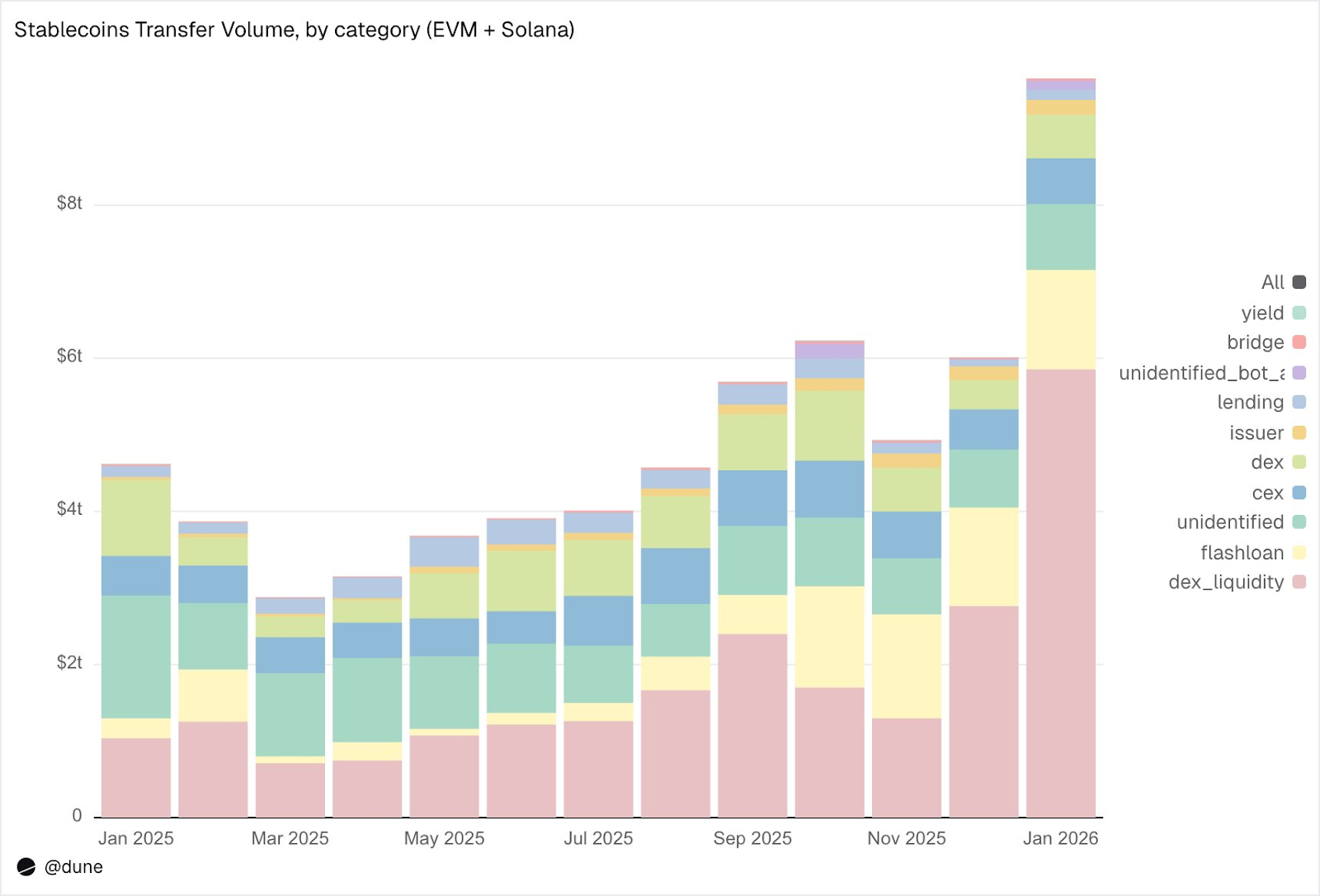

What exactly are stablecoins doing?

Transfers in this dataset are not only labeled as "volume" but also categorized as specific on-chain activities:

January breakdown:

1. Market Infrastructure (DEX Trading and Liquidity):

DEX liquidity provision and withdrawal: $5.9 trillion. This is the largest single use case, reflecting the role of stablecoins as on-chain base assets for market making.

DEX Swaps: $376 billion. Direct trading activity conducted through automated market makers.

Together, these two types of data indicate that stablecoins primarily function as collateral and liquidity infrastructure. Notably, trading volume is concentrated in incentive-driven activities, such as yield farming and active capital optimization, rather than pure trading demand.

2. Leverage and Capital Efficiency (Borrowing + Flash Loans)

Flash loans (borrowing and repayment): $1.3 trillion. Automated arbitrage and liquidation cycles.

Lending activities: supply, borrow, repay, withdraw, $137 billion. Represents on-chain short-term capital efficiency and structured credit.

3. Access Channels (CEX and Bridges)

CEX traffic: deposits ($224 billion), withdrawals ($224 billion), internal transfers ($151 billion), totaling $599 billion

Cross-chain bridge deposits and withdrawals: $28 billion. This volume highlights the critical role stablecoins play in transfers between CEXs and cross-chain settlement.

4. Issuance Layer (Currency Operations)

Issuer activity: Minting ($280B), burning ($200B), de-pegging adjustments ($230B), and other activities, totaling $1060B—nearly five times the $420B recorded in the same period last year.

5. Yield Protocol

Yield protocol activity: $2.7 billion. This is a smaller but structurally significant segment closely tied to structured strategies and on-chain asset management.

Overall, 90% of transfer volume flows through identified activity categories, enabling detailed insight into how stablecoins move across every layer of the on-chain technology stack.

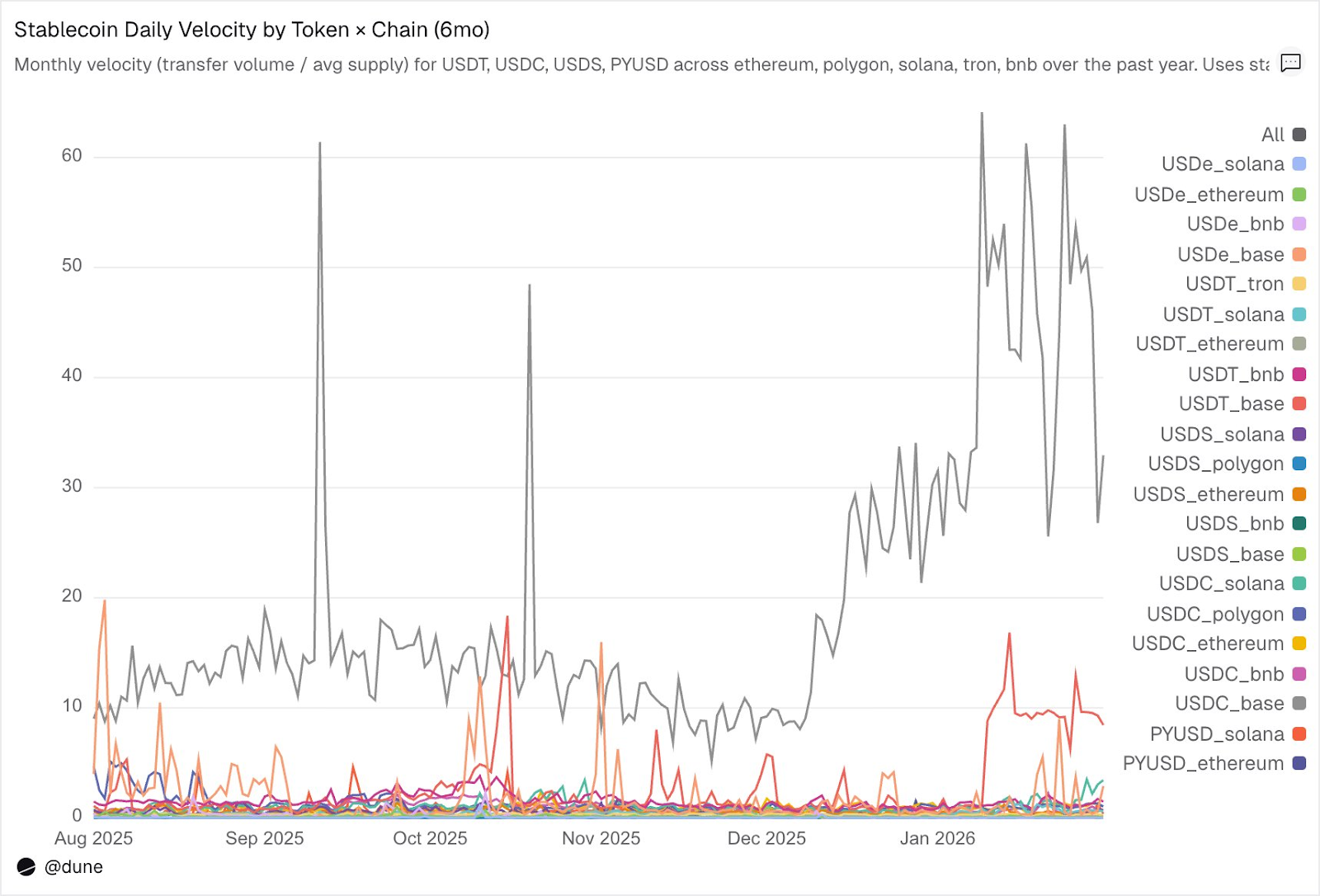

Velocity: The same token, different worlds

The daily turnover rate (transfer volume divided by supply) may be the most underappreciated metric in stablecoin analysis. It reflects how actively a stablecoin is used as a medium of exchange, not just how much is held.

Among the tokens we analyzed, USDC and USDT once again stand out, despite their differences.

Source: Dune

USDC has the highest velocity on L2s and Solana. On Base, USDC’s daily velocity reaches as high as 14x, primarily driven by high-frequency DeFi trading activity. On Solana and Polygon, it’s around 1x; on Ethereum, it reaches 0.9x, with nearly its entire supply traded daily.

USDT is fastest on BNB and Tron. The daily velocity on BNB Chain is 1.4x, reflecting its active trading activity; on Tron, the daily velocity is 0.3x, with lower transaction volumes but exceptional stability, consistent with its role as a primary channel for cross-border payments. On Ethereum, USDT’s daily velocity is only 0.2x, with the majority of its $100 billion+ supply remaining idle.

The trading velocity of USDe and USDS is intentionally slow. On Ethereum, USDe has an average daily velocity of just 0.09x, while USDS has an average daily velocity of 0.5x. Both are designed as yield-bearing stablecoins: USDe is typically staked as sUSDe to capture the returns from Ethena’s delta-neutral strategy, while USDS is deposited into the Sky Savings Rate to earn protocol-sponsored yields. As a result, a significant portion of the supply remains idle in savings contracts, lending markets like Aave, or structured yield cycles. The low velocity is not a disadvantage—it’s a feature: these assets are designed to accumulate yield, not to circulate.

Chains matter more than tokens. On Solana, PYUSD has a daily velocity of 0.6x, four times that of Ethereum (0.1x). The same token exhibits vastly different usage patterns across different ecosystems.

Supply and volume each reflect part of the picture. Velocity connects the two, measuring as a single metric whether stablecoins on a specific chain are functioning as active infrastructure or sitting as idle funds.

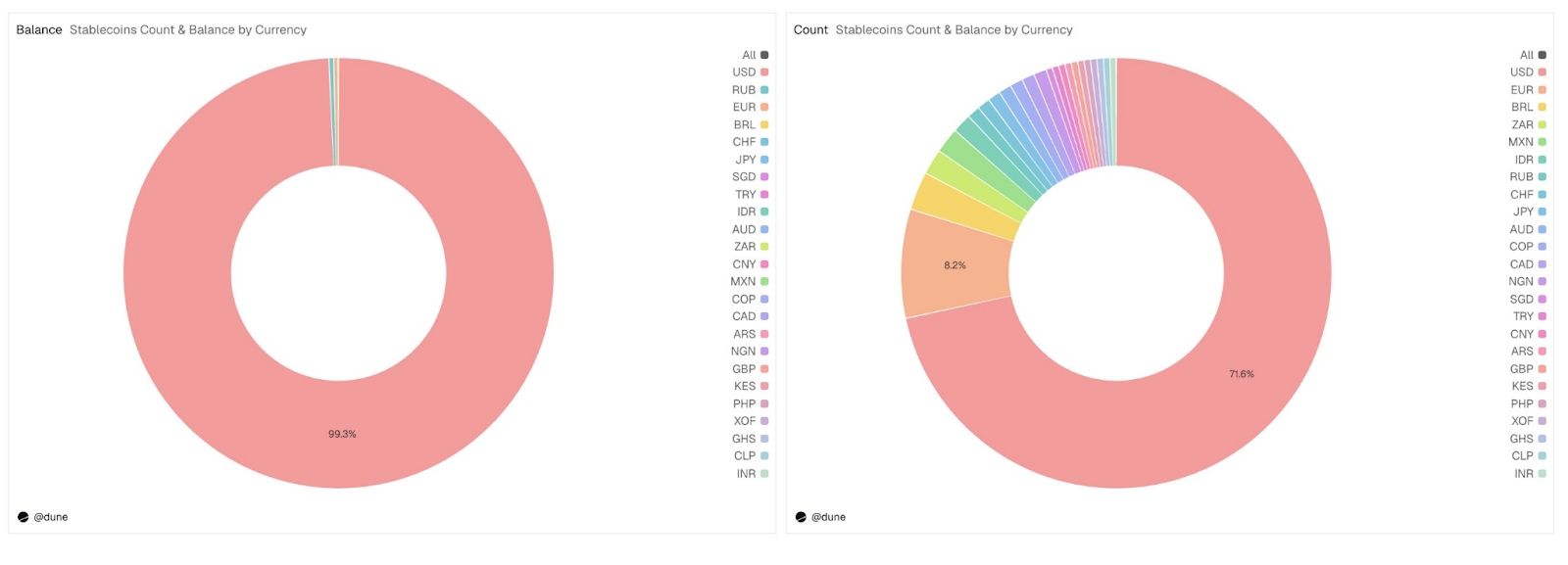

Beyond the US Dollar

This analysis focuses on 15 USD-pegged stablecoins, but the full dataset covers a broader range. It tracks over 200 stablecoins representing more than 20 currencies: the euro (17 tokens, $990 million supply), the Brazilian real ($141 million), the Japanese yen ($13 million), as well as tokens denominated in the Nigerian naira, Kenyan shilling, South African rand, Turkish lira, Indonesian rupiah, Singapore dollar, and others.

Source: Dune

The supply of non-U.S. dollar stablecoins currently stands at just $1.2 billion, yet 59 different tokens are already distributed across six continents, accounting for nearly 30% of the total tokens in the dataset. Infrastructure for local currency stablecoins is being built on-chain, and data to track their development is already available.

Related reading: The Secret War Behind Stablecoins: Who Will Be the “Biggest Winner” Among Issuers, Applications, and Users?