Written by: Will A Wang

Receive payments in USDT, with funds arriving in ten seconds and chargebacks eliminated—that’s the real experience many digital entertainment merchants have when first using stablecoin payment processing. But getting the money is just the simplest part of it.

In traditional payment systems, the issuer, acquirer, and card network collectively handle all the unseen tasks: identity verification, risk screening, suspicious transaction reporting, and dispute resolution. Stablecoins eliminate every intermediary in this mechanism. At the moment a on-chain transfer is completed, none of these four tasks are being performed by any party.

This article addresses the gap: who will fill it, how to fill it, and to what extent it must be filled to remain compliant. For platforms building stablecoin payment processing services and merchants evaluating whether to integrate, this is not a theoretical regulatory issue—it is an existing compliance risk in your current business architecture.

One, receiving payments and processing payments are not the same thing.

At the end of 2023, a Southeast Asian digital entertainment merchant’s Stripe account was permanently suspended due to an excessive chargeback rate. Within three weeks, they integrated with a stablecoin payment platform registered in Saint Vincent, and USDT payments began arriving—chargebacks disappeared. However, two years later, a compliance audit revealed that none of the transactions over those 24 months had undergone on-chain risk screening.

The funds have arrived. The compliance documentation has not.

This is the real problem that stablecoin payment processing aims to solve.

Stablecoins are inherently about "receiving payments," not "processing payments"—money moves from Wallet A to Wallet B, confirmed on-chain, and that’s all. We use the term "processing payments" because it more accurately points to the real issue: merchants don’t just need to receive money; they need a complete, legitimate, secure, and auditable service system to support it.

In the traditional banking card system, this framework is shared among three parties: the issuing bank verifies the cardholder’s identity, the acquiring bank processes each transaction and assumes the risk exposure, and the card network handles clearing in between. When a merchant swipes a card, an entire mechanism of responsibility allocation operates silently behind the scenes—KYC is handled by someone, risks are borne by someone, chargebacks are managed by someone, and reports are submitted by someone. Merchants are completely unaware of it and need not concern themselves with any of it.

Stablecoins have eliminated all intermediate layers in this system. The funds have arrived, but:

- Neither party has completed the payer's identity verification (KYC).

- Neither party performed risk screening (KYT) on this transaction.

- Neither party reported a suspicious transaction report (STR) to the regulatory authority.

- Neither party can process incorrect payments or disputes.

These four missing elements represent the entire gap between receiving stablecoins and true "payment processing." Who will fill them, how to fill them, and to what extent they must be filled to be compliant—these are the only questions this article aims to address.

Technically, stablecoin merchant acquiring is a peer-to-peer transfer. Commercially, it must deliver everything that traditional merchant acquirers provide. The value of stablecoin merchant acquiring lies off-chain, not on-chain.

II. Demand-Driven: Why Merchants Have Reached This Point

What drives merchants to adopt stablecoin payments is never enthusiasm for new technology. Their core reasons for adoption are only three.

Requirement One: Eliminate Chargebacks

Chargebacks are not an incidental risk of online payments—they are a structural feature. All online transactions lack physical card swiping, signatures, or in-person verification, placing the full cost and difficulty of dispute resolution on the merchant.

The numbers illustrate the scale of the problem. Chargeflow data shows that global e-commerce chargeback losses are projected to reach $33.8 billion in 2025 and rise to $41.7 billion by 2028. Sift’s Q4 2024 Digital Trust Index breaks this down into two layers: in terms of scale, the average overall chargeback amount in Q1 2024 surged 59% year-over-year to $374; structurally, chargeback rates for online travel and accommodation spiked 816%, e-commerce rose 222%, and digital goods and services increased 59%. Digital entertainment and financial services together account for 30% of all high-risk merchant disputes.

The root cause lies in the reversible design of the credit card system. Friendly fraud—where users initiate chargebacks after making purchases by claiming “unauthorized transactions”—is a persistent issue for digital entertainment platforms. More seriously, account suspension: if the chargeback rate exceeds the threshold, Stripe or Adyen will immediately freeze the account, preventing fund collection for 2–4 weeks, causing existing users to churn upon seeing “payment failed.”

Blockchain has no "dispute and reversal" mechanism. The immutability of the chain fundamentally eliminates this issue.

NOWPayments’ data confirms the scale of this demand: its iGaming transaction volume increased by 40% year-over-year, accounting for approximately 15% of the industry’s transaction market share. In 2025, stablecoins (USDT/USDC) already accounted for over 50% of on-chain transaction volume in global crypto iGaming. It should be noted that the shift toward stablecoins in iGaming is driven by multiple factors—elimination of chargebacks is one, but regulatory arbitrage and low entry barriers are also significant. The outcome has already occurred: the market has migrated.

Irreversibility eliminates chargebacks, but also removes the consumer safety net—a issue we'll revisit in Chapter 3.

Requirement 2: Reduce online payment processing costs

The cost of online payment processing is not a single number—it's a stack of layered fees.

Stripe’s standard rate for U.S. merchants is 2.9% + $0.30 per transaction, plus an additional 1% for international cards and another 1% for currency conversion—meaning a $100 order from an overseas customer incurs nearly $5 in payment processing fees alone. Adyen’s Interchange++ model offers greater transparency for large clients, but when combined with card network fees on cross-border transactions, the total cost still easily exceeds 4%. High-risk industries also face higher surcharges and rolling reserves—Stripe outright refuses to serve most digital entertainment and high-risk categories.

A merchant processing $500,000 in online transactions annually pays $15,000 to $20,000 in processing fees alone, not including chargeback losses, currency conversion fees, or monthly platform charges.

The cost structure for stablecoin merchant acquiring is entirely different. Platforms like Triple-A typically charge an all-in fee of 0.5%–1.5%, with no cross-border surcharges or currency conversion intermediaries—on-chain transfers inherently make no distinction between "domestic" and "cross-border." More importantly, settlement speed has changed dramatically: traditional merchant acquiring has a fund settlement cycle of T+2 to T+3, while stablecoin settlements can achieve T+0 or even real-time processing.

According to Eric Barbier, founder of Triple-A, stablecoins can reduce the working capital required for cross-border payment operations to one-tenth of traditional models. For startups, this isn’t just an efficiency gain—it’s a matter of survival.

Requirement three: Reach coin holders and global internet consumers

This is the fastest-growing and most underestimated of the three requirements.

BVNK partnered with YouGov to survey over 4,600 stablecoin holders across 15 countries (respondents were active users who held or planned to purchase cryptocurrency within the past 12 months and do not represent the general consumer population). Three findings stand out: 52% of holders deliberately chose to spend at merchants that accept stablecoins—payment methods are not just tools, but channels for customer acquisition; stablecoin holders’ willingness to spend exceeds actual spending across all tested categories, indicating the bottleneck lies not in demand but in merchant adoption; stablecoin users exhibit stronger international payment needs, with naturally higher average order values and conversion rates compared to local credit card users.

On-chain data from Visa and Allium shows that in August 2025, the total volume of stablecoin transfers under $250 reached $5.84 billion, a record high. This signals everyday spending, not speculation.

However, stablecoin payment processing reaches more than just “coin holders.” For consumers in emerging markets with weak banking infrastructure, stablecoins provide a pathway to bypass traditional banking systems and directly participate in global e-commerce. Transaction data from NOWPayments between 2023 and 2025 reveals entirely different driving factors across markets: convenience in the U.S., circumventing banking restrictions in India and Nigeria, and serving as an alternative after traditional payment channels fail in Russia and other emerging markets. A one-size-fits-all global payment strategy would lose 15%-20% of potential conversions in these markets.

Here's how Razer Gold integrates with Triple-A: a single payment interface that reaches over 130 countries' internet consumers, eliminating the need to separately integrate local payment methods for each market.

The common thread among these three needs: Stablecoins are addressing real business problems here, not minor improvements to payment experiences. Stablecoin payments have already occurred at scale before regulatory frameworks were fully established. The real challenge for regulators is not whether to allow it, but how to bring order to something that is already happening.

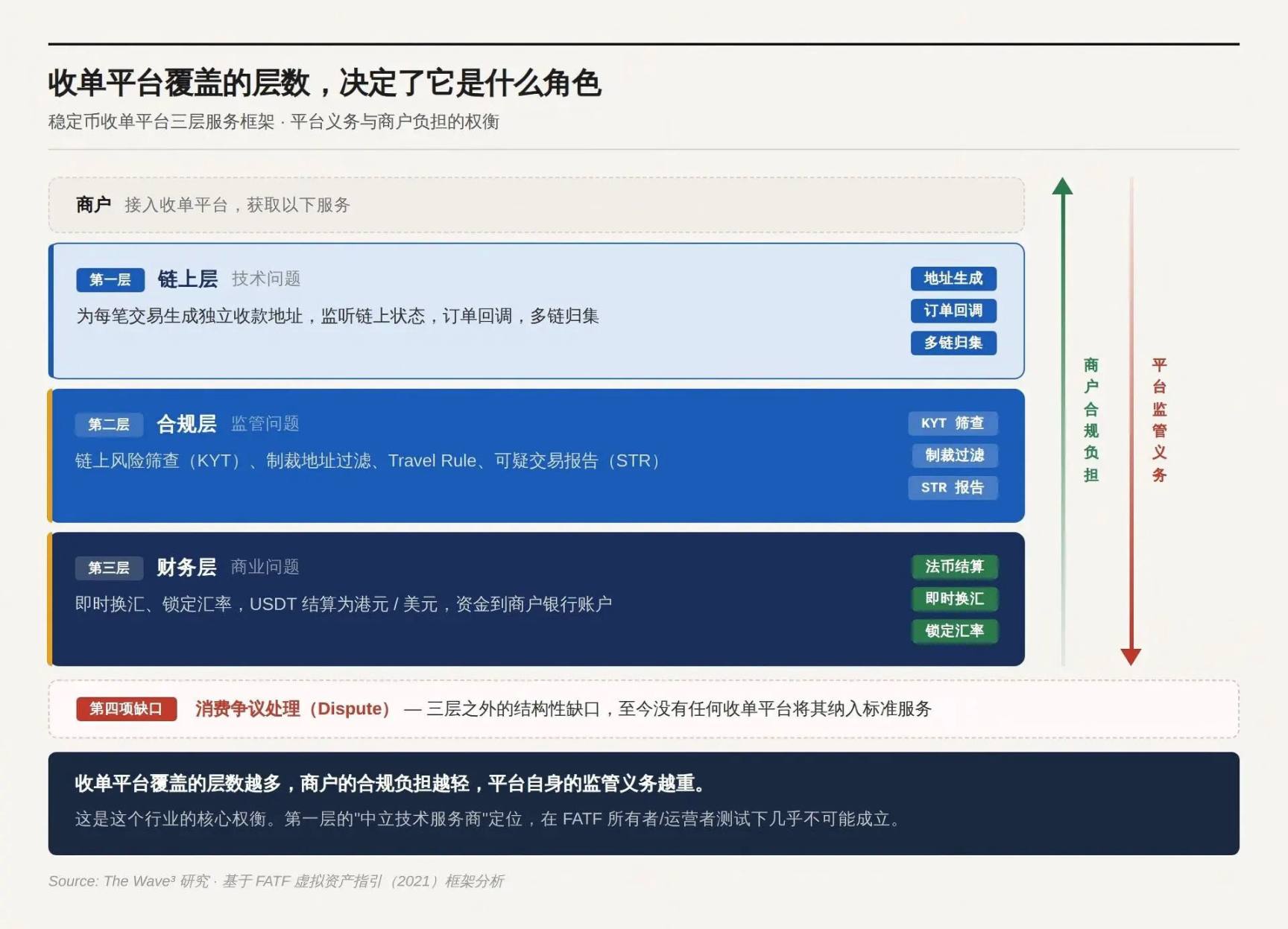

Three Layers of Logic for the Payment Processing Platform

On-chain confirmation is complete, and the funds have arrived at the address—what’s next?

The on-chain transfer does not solve any of these issues: the order system doesn't recognize on-chain addresses, the accounting system doesn't record USDT, the balance sheet cannot hold cryptocurrencies, regulators require reporting of suspicious transactions, and customers who pay the wrong amount need someone to handle it.

The product logic of a stablecoin payment platform is to progressively take on these issues. The more issues it assumes, the higher its service value—and the greater its regulatory obligations.

Layer 1: On-chain layer

Generate a unique receiving address for each transaction, monitor on-chain status, confirm receipt, and translate on-chain events into order callback signals recognizable by the merchant system. Mature platforms also offer multi-chain aggregation, smart contract-based profit distribution, and order status management (e.g., automatic closure upon timeout, partial payment top-ups).

Without this layer, merchants would have no way of knowing which on-chain transfer corresponds to which order. It is precisely at this layer that many platforms claim to be “neutral technology service providers”—offering only technical tools without intervening in fund flows, and therefore arguing they should not be considered regulated entities.

Whether this statement holds true depends on the determination of the next layer.

Layer 2: Compliance Layer

Every incoming fund requires on-chain risk screening (KYT): Is this wallet address on any sanctions list, and has it interacted with mixers, darknet markets, or known fraudulent addresses? Transactions exceeding a threshold amount must trigger sender identity verification. The Travel Rule requires the exchange of sender and recipient information between VASPs. Suspicious transactions must be reported to regulators (STR).

This layer is the primary source of compliance obligations and the key test used by regulators to determine the nature of the platform.

The FATF’s October 2021 update to its guidance on virtual assets established two principles: First, function over form—regulation focuses on the business function, not the technical form; non-custodial, decentralized, and smart contract-based arrangements do not constitute exemptions. Second, the owner/operator test—even if an arrangement appears decentralized, “creators, owners, operators, or others maintaining control or sufficient influence” may still fall under the VASP definition; factors include whether they profit from the service, whether they have the ability to set or modify parameters, and whether they maintain an ongoing commercial relationship with users.

The entity that exercises substantive control over fund flows—regardless of whether it handles the funds directly—is the regulated party. If a platform has a front-end interface, collects fees, and has a recognizable operating entity, its self-proclaimed status as a “neutral technology service provider” no longer holds. The scope of this test is much broader than most platforms realize.

Layer Three: Financial Layer

The user pays in USDT, but the merchant needs HKD or USD. Someone needs to provide instant foreign exchange, lock in the exchange rate, and settle fiat currency directly into the merchant’s bank account. Merchants do not want to hold cryptocurrency on their balance sheets—this is not merely a preference, but a strict compliance requirement for most corporate accounting policies.

Without fiat settlement, receiving stablecoins is a financial burden, not a payment tool, for most businesses.

Beyond the three layers: Structural gaps in dispute resolution

The first three items (KYC, KYT, STR) correspond to the three layers above and are already systematically covered by existing platforms. However, the fourth item—dispute resolution—is not included as a standard service by any acquiring platform, leaving this gap unaddressed to date.

In the credit card system, consumers' right to chargeback for disputed transactions is not a customer service feature—it is a legal obligation (under U.S. Regulation E / Regulation Z and EU PSD2). The on-chain immutability of stablecoins eliminates chargebacks and, with them, consumers' avenues for recourse. What merchants perceive as an "advantage" is, from a regulatory perspective, a "gap."

Three types of remediation solutions are emerging in the market: off-chain manual refunds at the platform level (Triple-A model), smart contract escrow with conditional release, and on-chain arbitration protocols like Kleros—but none of these have been widely adopted in merchant payment scenarios. Consumer protection is not waived simply because the underlying technology has changed. This issue remains unresolved.

The more layers a payment processing platform covers, the lighter the compliance burden on merchants, but the greater the regulatory obligations on the platform itself. This is the core trade-off in this industry.

Four: Choosing which layer to cover means choosing which role to take on.

The three-layer framework is a multiple-choice question. Choosing which layer to cover determines your role and the regulatory environment you face. The three mainstream market architectures correspond to three different choices and outcomes.

Light Intervention: The Window of Regulatory Arbitrage

The platform operates only at the first layer: generating addresses, monitoring receipts, and directing funds directly to the merchant’s wallet. NOWPayments is a typical example of this model—the operating entity is registered in Saint Vincent and the Grenadines, where there are virtually no substantive regulatory requirements for virtual asset businesses. The handling of compliance obligations is explicitly stated in the service agreement: FD Transfers LLC clearly declares that the platform “assumes no responsibility for KYC, KYB, or AML compliance for merchants or end users,” and that “merchants and end users bear full responsibility for transactions they execute.”

CoinPayments (a non-custodial payment gateway supporting over 100 crypto assets) and PayRam (focused on self-hosted node deployment) follow the same path: the platform provides only technical tools, with full compliance responsibility delegated to merchants and users.

This model operated efficiently during the regulatory gray area, serving markets traditionally rejected by conventional payment processors. However, on-chain records are permanent, and all historical transactions conducted during the unlicensed period can be traced at any time. This means that today’s compliance decisions determine not only tomorrow’s risk exposure, but also the legal liability incurred over the past two years.

The issue with the NOWPayments model isn't "whether something will happen now," but "that the window will already be closed when something does happen."

Intermediation: Not handling money does not mean you don't need a license

The platform does Layer 1 plus Layer 2: conducting KYT screening and sanctions filtering before releasing funds, but not performing currency exchange or fiat settlement. Coinbase Commerce (now renamed Coinbase Payments) is the most commonly misunderstood example of this model.

The logic of a on-chain direct architecture is compelling: funds go directly from the user’s wallet to the merchant’s wallet, with the platform never touching the funds—so how can I be called a financial service provider? Coinbase’s approach directly contradicts this logic. Coinbase Payments’ terms of service explicitly state that it does not custody merchant assets—yet it retains the right to modify, suspend, or terminate the service. It offers a frontend interface, charges fees, has a recognizable operating entity, and has the ability to shut down the service—all conditions for being identified as an owner/operator are simultaneously met.

Coinbase holds a FinCEN MSB registration, multi-state money transmitter licenses, and a New York BitLicense in the United States, and in Europe, it holds a CASP license through its Luxembourg entity, covering the EU. This is the correct industry approach to structuring intermediary involvement: by operating at the second layer, you acknowledge yourself as a regulated entity—not attempting to evade classification by claiming you are “only doing risk management.”

Re-engagement: Turning Compliance into a Product

The platform covers all three layers—receiving funds, screening, and foreign exchange settlement—so merchants see only normal fiat currency deposits, with no exposure to cryptocurrency throughout the process. Triple-A is the mature form of this model.

Triple-A’s terms of service directly reflect this role: not a technology tool provider, but a comprehensive payment processing and settlement service provider—the platform executes currency exchange and settles merchants in fiat net of fees, and the merchant’s KYB review and ongoing compliance obligations are also included in the agreement. Licensed map: Singapore MAS Major Payment Institution (MPI) license, France ACPR Payment Institution license (covering 27 EU member states via the EU passporting mechanism), FinCEN MSB registration, money transmitter licenses in 17 U.S. states, Canada FMSB, and South Africa FSCA registration.

Grab, Razer, and Farfetch chose Triple-A not because it offers the lowest fees—but because Triple-A absorbs all three layers of complexity, enabling businesses to access an otherwise unreachable market through a single API, without ever touching any crypto assets. In the same space, Stripe supports USDC settlements via its acquisition of Bridge (1.5% fee, no additional fixed costs), and traditional payment giant Shift4 is launching a stablecoin settlement option by the end of 2025. The entry of traditional payment companies is itself a signal of market maturity.

Compliance itself has become a product. The value of this product increases as regulations tighten.

The window for light intervention is closing, the regulatory boundary for moderate intervention is tightening, and the threshold for heavy intervention is rising. NOWPayments’ growth红利 comes from regulatory vacuum, while Triple-A’s growth红利 comes from regulatory tightening. In the same industry, two completely opposite driving forces.

Five: Online Merchant Selection Options

The most common question merchants ask is: “Is it compliant for our platform to integrate stable coin payment processing?”

There is no answer to this question because it is based on a faulty premise. Compliance is not a binary judgment—it is the result of two variables intersecting:

Where are your consumers located? How much compliance responsibility does your integrated platform assume?

Two variables must intersect to determine the merchant's remaining obligations.

Variable one: Where are consumers?

Regulatory obligations follow the location where the business occurs, not the jurisdiction of incorporation. A Cayman Islands-registered payment processing platform serving transactions where Hong Kong users pay Hong Kong merchants is fully subject to Hong Kong regulatory authority, regardless of where the platform is registered. Offshore registration can help avoid taxes, but it cannot evade regulation.

Major markets still differ in their regulatory classification of stablecoins (as virtual assets vs. payment instruments), leading to different licensing requirements; however, regardless of the classification, the obligation to obtain a license is equally strict.

Tether has not yet received MiCA authorization, creating clear uncertainty regarding the regulatory status of USDT in the EU, leading some EU-based platforms to delist USDT. Payment processors serving EU consumers should prepare contingency plans in advance when selecting stablecoins.

Variable 2: How much compliance responsibility is assumed by the integrated platform?

The more compliance responsibilities the platform assumes, the fewer obligations remain for the merchant, but the higher the premium on payment service fees.

On-chain consumer KYC deviation

Stablecoin payments have a structural issue that traditional payment processing does not: on-chain payments inherently carry no identity information. When a user scans a code, USDT is transferred from one wallet address—this transaction reveals only a string of on-chain addresses, with no name, ID number, or bank account. In traditional payment processing, the cardholder’s KYC is completed by the issuing bank, and the acquiring bank trusts this result. Stablecoins have no issuing bank, so this KYC chain never existed from the start.

This does not mean that anonymous wallets are exempt from compliance requirements. Regulatory mandates require “measures commensurate with the risk”: KYT is the baseline, sanctions address filtering is the red line, transactions exceeding a threshold amount trigger identity verification, and unusual behavior triggers in-depth investigations. The Travel Rule requires VASPs to transmit payer and payee information, but when consumers use self-custody wallets for payments, this information simply does not exist.

These issues do not yet have uniform answers in regulatory texts—but regulatory authorities will not wait for answers to be standardized before sending their letters.

Obtaining a license only proves that regulators permit you to operate. True compliance means conducting KYT screenings on every transaction, completing KYB reviews for every merchant onboarding, and being able to produce complete transaction records when regulators request them. Missing either the license or the execution creates a vulnerability—it’s only a matter of which one gets discovered first.

Six, what happens next

Rules are taking shape, but the answer differs as to whether this is good or bad news for which type of participant.

Clear regulation is the ticket in.

2024–2025 marks a watershed moment for stablecoin regulation. The three most important global financial regulatory jurisdictions have each completed foundational legislation within this two-year period—but completion of legislation does not equate to clear rules. The GENIUS Act regulates issuance, but the传导路径 for merchant acquisition remains under negotiation among state regulators; the CASP license under MiCA faces substantial differences in approval standards across member states; Hong Kong’s Stablecoin Ordinance regulates issuers, yet the scope of coverage for merchant platforms has yet to be clarified by any enforcement case. A February 2025 survey by Fireblocks of 295 financial institutions and payment providers showed the proportion viewing regulation as a barrier dropped from around 80% to under 20%—but a reduced barrier does not mean the path has been fully paved.

Compliance endorsement is replacing product strength as the primary driver of customer acquisition.

Over the past two years, Triple-A has significantly expanded its enterprise customer base—not because its product is superior, but because its compliance backing enables companies like Grab, Razer, and Farfetch to integrate with confidence. Stripe has launched stablecoin settlement, and Shift4 now offers stablecoin settlement options to its hundreds of thousands of merchants—the entry of traditional payment giants signals to the market that stablecoin merchant acquiring has evolved from a "gray-area alternative" into a "mainstream payment infrastructure."

Extended implication: The market value of compliance advisors, on-chain analysis tools (Chainalysis, TRM Labs), and cross-jurisdictional legal services serving stablecoin acquiring platforms will rise in tandem with regulatory intensity. Compliance is not a cost center—it is the business itself.

The answer to cost issues is not technology, but the competitive landscape.

Who ultimately bears the compliance costs? If the platform passes them on to merchants, those who can’t afford it will leave. If the platform absorbs the costs itself, it must recoup them through higher pricing, bringing merchants back to the comparison logic of: “Why not use a cheaper, unlicensed platform?”

Experience from the traditional payments industry shows that after regulation becomes standardized, competition does not disappear—it simply shifts from “compliant vs. non-compliant” to “who can achieve lower costs within the regulatory framework.”

Stablecoin payment processing will undergo the same process—when unlicensed platforms systematically exit, compliance costs become the common baseline for all players, and the next competition becomes who can achieve maximum efficiency within that baseline. Triple-A and BVNK’s current scale advantages are essentially positioning themselves for that future competition.

Which one can complete the entire journey without guessing?