Author: danny

When we talk about public blockchains during a bear market, what are we really discussing? Price? Community? Or governance? At a deeper level, operating a public blockchain is essentially governing a digital nation. Tokens are currency, developers are citizens, DApps are industries, and on-chain governance is the government. If we reexamine Solana’s history through the lens of statecraft, many seemingly random decisions reveal clear underlying logic.

Introduction: No one is born strong

On August 9, 1965, Lee Kuan Yew wept in front of television cameras. Singapore was expelled from the Malaysian federation, becoming a tiny island nation with no hinterland, no resources, and no army. Few believed it could survive.

On November 11, 2022, FTX filed for bankruptcy. Solana’s TVL dropped by more than 75% within a week, and the price of SOL plummeted from $32 to $8. The entire crypto community’s reaction: "Solana is done."

The beginnings of the two stories are strikingly similar: a discarded small entity struggling to survive in a hostile environment. And their subsequent paths—from dependence, to gray-area survival, to transformation and upgrading—are almost frame-for-frame comparable.

This article is not about price or community, but a more fundamental issue: operating a blockchain is essentially governing a digital nation. Tokens are currency, developers are citizens, DApps are industries, and on-chain governance is the government. If we reexamine Solana’s history through the lens of statecraft, many seemingly random decisions reveal clear underlying logic.

Chapter One: The British Military Era — SBF and the Umbrella of FTX

British military economy in Singapore

In its early independence, Singapore's economy relied heavily on the spending and employment generated by British military forces. The British military bases contributed approximately 20% of the GDP at the time. Singapore was well aware of the fragility of this dependence, but for a newborn nation, there was no luxury of choosing its customers. Survival was the top priority.

In 1968, the United Kingdom announced it would withdraw all its military forces east of the Suez Canal by 1971. This was a devastating blow to Singapore. But it was precisely this "abandonment" that forced Singapore to seriously ask: If the protective umbrella is gone, what will I rely on to survive?

Solana's SBF era (2020–2022)

The Solana mainnet launched in March 2020, but what truly set it apart from the many other "Ethereum killers" was Sam Bankman-Fried and his empire. FTX and Alameda Research were not only the largest capital providers to the Solana ecosystem, but also its key credibility endorsers. Nearly all of the early core ecosystem projects—such as Serum, Raydium, and Maps.me—had deep involvement from FTX-affiliated capital.

During this period, the Solana ecosystem resembled Singapore under British occupation: superficially prosperous, with impressive metrics (TVL once surpassed $12 billion), but built on fragile foundations. Much of the on-chain activity stemmed from Alameda’s market-making funds circulating within the ecosystem, while genuine organic demand was far less healthy than the data suggested.

Singapore relied on British military spending, and Solana relied on SBF’s funds. The common characteristic is that the prosperity was real, but its source was exogenous, concentrated, and could vanish at any moment.

The collapse of the umbrella

In November 2022, FTX collapsed from the world’s second-largest exchange into ruins within 72 hours. The impact on Solana was systemic: Serum’s governance keys were controlled by FTX, causing the project to grind to a halt; large amounts of treasury assets from ecosystem projects were frozen within FTX; the concentration of SOL staking was laid bare; market confidence vanished, and developers began to leave.

This is Solana's "1968 moment." The umbrella wasn't slowly removed—it was blown away overnight.

Chapter Two: How a Small Nation Without Resources Survives—Solana’s Foundational Endowments

Singapore's "unique resource": geographic location

Singapore has no oil, no mineral resources, and even relies on imports from Malaysia for freshwater. But it has one gift from nature: its strategic location at the chokepoint of the Strait of Malacca. About 25% of global maritime trade passes through here. Lee Kuan Yew understood early on: I don’t need to have resources—I just need to be the best node for their flow.

Solana's "Unique Resource": Performance and Cabal

In the world of public blockchains, Solana lacks Ethereum’s first-mover advantage, Bitcoin’s narrative mythos, and Cosmos’s modular flexibility. But it has one thing:极致 performance at the native layer. 400-millisecond block times, a theoretical peak of 65,000 TPS, and extremely low transaction fees (typically under $0.001).

This is not an optional technical parameter. Just as Singapore’s geographic location at the Strait of Malacca enabled it to become a trade hub, Solana’s performance characteristics make it naturally suited to support high-frequency, low-value, high-volume on-chain activity.

For Singapore, geography is like block speed and transaction cost are to Solana: it’s the ticket that convinces cabals to come here and compete.

Chapter Three: Survival Wisdom in the Gray Zone — From Money Laundering Haven to Meme Casino

Singapore's "less-than-glamorous" intermediate stage

This is a period of history often downplayed in Singapore's official narrative. During its rapid development from the 1970s to the 1990s, Singapore did not become a regional financial center solely due to its reputation for "clean and efficient" governance.

A harsh reality is that during that era in Southeast Asia, neighboring regimes—the Suharto regime in Indonesia, the Marcos family in the Philippines, and Myanmar’s military junta—generated vast amounts of money requiring "cleaning." These funds needed a secure, non-inquisitive, and legally predictable place to rest. Singapore恰好 provided such an environment: strict banking secrecy laws, efficient financial infrastructure, and an unspoken, pragmatic attitude of “as long as you follow my rules, I won’t ask where your money came from.”

Business makes no moral judgments—only survival strategies. A small country with limited resources must, in its early stages, accept some "imperfect money" to build up sufficient capital reserves and lay the foundation for future transformation.

The key is that Singapore has never been laissez-faire. While attracting capital, it has consistently maintained extremely high administrative efficiency and legal certainty (Temasek and GIC are among the top 10 sovereign wealth funds in the world). You can bring your gray money, but you won’t disrupt my territory. This “orderly gray” is an exceptionally delicate balancing act.

Solana's Meme Season and Pump.fun (2023–2024)

After the collapse of FTX, Solana faced survival pressures no less severe than those of Singapore in its early independent years: TVL drying up, developers leaving, and its narrative crumbling. At this point, what it needs is not "correct" growth, but any kind of growth—just to survive.

From late 2023 to 2024, the Meme wave swept across Solana. The emergence of Pump.fun lowered the barrier to launching Meme tokens to near zero: anyone could create a token in minutes without code or auditing. The wealth-creation myths surrounding BONK, WIF, BOME, and other Meme tokens attracted massive speculative capital.

From the perspective of traditional finance or technological fundamentalism, this would seem like a disaster. The Solana chain is flooded with rug pulls, sniper bots, and countless zero-value garbage tokens. But if viewed through the historical framework of Singapore, you’ll find striking similarities—and profound rationality:

Memes to Solana are like gray money to early Singapore—it didn’t make it onto the tech geek’s stage, but it brought three key things:

Funds inflow (foreign reserves): Meme trading has generated massive on-chain transaction volume and fee revenue, directly bolstering the validator economic model and stabilizing the network’s fundamental operations.

User base (population): Millions of new users were introduced to Solana wallets (Phantom’s downloads surged during this period), even if they initially came for gambling.

Infrastructure stress testing (urban development): The extreme trading load during the Meme peak exposed the true bottlenecks of the Solana network, accelerating the development of critical infrastructure such as the Firedancer client.

Singapore's wisdom lies not in "accepting gray funds," but in "never ceasing to build legitimate institutional infrastructure while accepting gray funds." Similarly, Solana's key lies not in the Meme itself, but in whether it has simultaneously advanced truly valuable foundational development under the cover of Meme mania.

Chapter 4: Money as Sovereignty — The Governance Logic of Tokenomics

Singapore's monetary policy philosophy

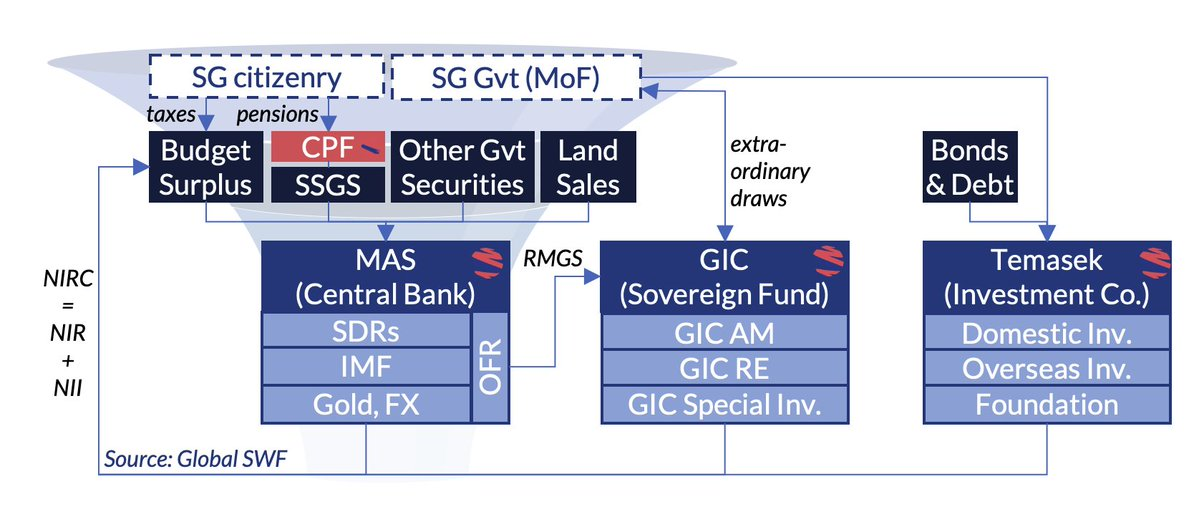

The Monetary Authority of Singapore (MAS) has a unique monetary policy among central banks: instead of using interest rates as its primary tool, it manages the exchange rate band of the Singapore dollar to regulate the economy. An appreciating channel is used to curb inflation and attract capital, while a depreciating channel stimulates exports and maintains competitiveness.

The core logic is: money is not static—it must be dynamic and responsive. How much money to print, whether to appreciate or depreciate the currency, depends on the needs of the current economic cycle. Excessive money printing dilutes national wealth and triggers inflation; excessive tightening stifles economic vitality. Sound monetary policy is a continuous balancing act.

SOL's tokenomics: The dynamic博弈 from inflation to deflation

The tokenomics of Solana have also undergone a similar evolution.

Initial inflation phase (quantitative easing): When the Solana mainnet launched, it set an annual inflation rate of approximately 8%, decreasing by 15% per year, with a long-term target converging to 1.5%. These newly minted SOL tokens are used to pay staking rewards, essentially functioning as a "fiscal expenditure" to subsidize validators—similar to how emerging nations heavily invest in infrastructure early on; you must first incur costs to attract and retain "citizens" (validators) who maintain network security.

Introduction of a burn mechanism (contractionary policy): In 2023, Solana introduced a partial burn mechanism for transaction fees—50% of the base fee from each transaction is permanently burned. When on-chain activity is sufficiently high, the amount of SOL burned may approach or even exceed the amount newly issued, putting SOL into a deflationary state in practice.

It’s like a country’s central bank finally gaining the ability to “raise interest rates”: when the economy (on-chain activity) is sufficiently prosperous, it recovers money supply to maintain the currency’s value.

But the issue is that Solana currently lacks a truly dynamic, responsive monetary policy framework. Its inflation rate decreases mechanically along a preset curve, while the burn rate depends entirely on market activity, with no intelligent adjustment mechanism like MAS connecting the two.

This is a deeper governance issue that Solana (and nearly all public blockchains) has yet to address: token issuance and burning should not follow a fixed curve, but should be dynamically adjusted like a sovereign nation’s monetary policy, based on the network’s “economic cycle.” During periods of network congestion (economic overheating), the fee burning ratio should be increased to curb speculation; during periods of low activity (economic recession), the staking threshold for validators might be lowered and incentives increased.

A truly mature public chain economy requires not a fixed inflation curve hardcoded into the code, but a on-chain "central bank" governance mechanism.

Only a few understand that tokens don't only appreciate when burned.

Chapter 5: HDB Politics — "Only those with assets will defend the nation"

The real crisis in Singapore's early years: not poverty, but the sense of division among ethnic groups

When most people talk about the Singapore miracle, they focus on economic growth. But Lee Kuan Yew himself repeatedly emphasized that the most dangerous enemy in the early days of nation-building was not poverty, but racial division.

In 1965 Singapore, Chinese made up about 75% of the population, Malays about 15%, and Indians about 7%. The three ethnic groups spoke different languages, held different beliefs, and distrusted one another. One of the key reasons Singapore was expelled from the Malaysian Federation was the irreconcilable racial tensions between the Chinese and Malays—during the 1964 racial riots, 23 people died and hundreds were injured.

After independence, Singapore faced a harsh reality: the people on the island did not see themselves as "Singaporeans." The Chinese identified with Chinese culture, the Malays with the Malay Federation, and the Indians with India. No one felt a sense of belonging to the concept of "Singapore," let alone was willing to sacrifice for it.

The fundamental problem Lee Kuan Yew needed to solve was: how to get a group of people who don’t trust each other to voluntarily stay under the same roof and be willing to contribute to maintaining it?

HDB: More than a home, it's a national bonding mechanism

The answer is HDB flats—perhaps one of the most sophisticated social engineering feats in human history.

On the surface, public housing addresses housing needs. In 1960s Singapore, a large portion of the population lived in slums and shantytowns. The government launched a large-scale public housing program, selling homes to citizens at prices far below market value and allowing the use of Central Provident Fund (CPF) savings to pay for mortgages. Today, over 80% of Singaporeans live in public housing.

But the real genius of public housing lies in the political logic behind it. Lee Kuan Yew once said something extremely candid (paraphrased): "When a person owns assets in a place, he is more willing to defend it."

The public housing system simultaneously achieves at least three strategic objectives:

First, create "stakeholders." When you're just a tenant, the rise and fall of the city matters little—you can always move away. But when you own a home, your wealth becomes tied to the nation’s fate. When property prices rise, your net worth increases; when the country struggles, your assets decline. Every public housing owner becomes a "shareholder" in Singapore’s destiny.

Second, mandatory racial integration. This is the most underappreciated design of the HDB system. HDB enforces strict ethnic quotas (Ethnic Integration Policy): each HDB estate has upper limits on the proportions of Chinese, Malay, and Indian residents, ensuring no single-race enclaves form. Your neighbors are guaranteed to be different from you. Children play together in the same building and attend the same schools. After one generation, racial divides are gradually dissolved through enforced physical integration.

Third, link personal wealth to the quality of national governance. The appreciation of HDB flats depends on Singapore’s continued prosperity and sound governance. When the government governs well, neighborhoods develop and amenities improve, increasing the value of your home. This creates a powerful positive feedback loop: citizens are motivated to support good governance because it directly enhances the value of their assets.

A public housing system that simultaneously achieves the three goals of aligning interests, removing barriers, and incentivizing governance. This is not merely a housing policy—it is the foundation of the nation. To secure the outside, one must first stabilize the inside; Lee Kuan Yew understood this well.

Solana's "racial issue": A divided community

Switch the perspective back to Solana. The Solana community after the FTX collapse faced fragmentation on par with Singapore in 1965.

There are at least three "groups" on-chain, each with vastly different interests:

Speculators and Meme traders. They are the largest contributors to activity on the Solana chain, driving trading volume, fees, and buzz. However, they have no loyalty to Solana and move to whichever chain is trending, essentially acting as a mobile population.

Native developers and builders. They have invested significant time and technical capital into Solana, building DeFi protocols, infrastructure tools, and DePIN projects. They have a nuanced and tense relationship with meme speculators—needing them for users and traffic, yet resenting them for diluting the ecosystem’s seriousness.

Validators and stakers. They are the foundation of network security, investing real hardware and staked capital. They care about network stability, staking yields, and the long-term value of SOL, and are neither involved in nor concerned by short-term hype.

The competitive tensions among these three groups are divisive. Meme traders complain that priority queues unfairly disadvantage retail users during network congestion; developers complain that Meme coins drain all attention and funding; and validators complain that the MEV distribution mechanism lacks transparency. Without a mechanism to align the interests of these three parties, the centrifugal forces within the Solana community will only grow stronger.

Where is Solana's "group house"?

Lee Kuan Yew’s wisdom—encouraging citizens to hold assets and aligning personal interests with collective destiny—offers what insight for Solana? Solana’s ecosystem already has some mechanisms similar to "public housing," but they are far from being systematically implemented:

Staking is the design closest to "public housing." When you stake SOL, you lock your assets into the network, and your rewards directly depend on the network’s healthy operation. Stakers naturally become "shareholders" in network security. However, currently, Solana staking is primarily concentrated among large holders and institutions, resulting in low participation rates and limited sense of involvement among ordinary users—this is like selling public housing only to the wealthy, leaving the poor as renters; in such a case, the effect of "aligned incentives" would be significantly diminished.

Governance tokens and airdrops are a form of "housing allocation." Ecosystem projects distribute governance tokens to early users and developers (such as the JTO and JUP airdrops), essentially "allocating assets"—turning participants from observers into stakeholders. Jupiter’s JUP token airdrop reached nearly a million active wallets, rapidly creating a large base of users with a strong sense of ownership toward the Jupiter protocol. When designed well, this mechanism can be as effective as public housing.

Superteam DAO's global community is an attempt at "ethnic integration." Superteam establishes localized communities across different countries and regions, enabling developers from India, content creators from Turkey, and DeFi users from Nigeria to collaborate within the same organizational framework. This is somewhat like HDB’s ethnic quota system—using structured mixing to reduce cliques and factionalism.

But Solana still lacks a truly systematic "asset binding—alignment of incentives" mechanism. Imagine a more refined version: if the Solana ecosystem could establish a system where developers receive ongoing protocol-level revenue shares for deploying successful applications on-chain; where active users accumulate non-transferable "on-chain credit" or "citizenship" through long-term usage; and where validator rewards are tied to the reliability of their services and their contributions to decentralization—then every participant’s personal wealth would be tightly aligned with Solana’s overall prosperity.

Only when speculators, developers, and validators become "owners," not just "tenants," will they truly fight for the long-term success of the chain. This is the most profound lesson Lee Kuan Yew taught us with public housing: people won’t fight for abstract ideals, but they will fight fiercely for their own assets.

Chapter Six: The Crossroads of Transformation — "What Then?"

Three leaps in Singapore

Singapore's economic transformation can be roughly divided into three phases:

Phase One (1960s–1970s): Labor-intensive manufacturing. Attracting multinational corporations to set up factories by leveraging low-cost labor, earning foreign exchange, and addressing employment needs. This was the phase of "survival."

Phase Two (1980s–1990s): Financial and Trade Hub. Leveraging geographic and institutional advantages, it became a regional center for capital aggregation and shipping logistics. Gray capital played an indispensable role during this phase. This was the stage of "establishing a foothold."

Phase Three (2000s–present): The knowledge economy and advanced manufacturing. Heavy investment in education, attraction of talent (Global Talent Program), and development of high-value-added industries such as biopharmaceuticals, semiconductor design, and financial technology. Simultaneously, anti-money laundering regulations have been tightened, gradually "cleaning up" the financial system. This is the phase of "defining ourselves."

Each transition does not occur naturally, but rather involves proactively shifting to a new model before the profits of the old model are fully exhausted. This requires immense strategic resolve and political will—because transition means deliberately giving up part of current gains.

Solana's current position: The end of Phase Two

If viewed through the lens of Singapore’s framework, Solana is currently in the late middle stage of phase two. The capital and user benefits brought by the meme wave are still present, but their marginal returns are beginning to diminish. Market fatigue with the search for the "next 100x meme" is growing, and if Solana fails to transform before this wave of hype fades, it risks becoming a "casino chain"—just as Singapore might today be just another Cayman Islands if it had remained stuck in the gray finance phase.

What could be the third phase of Solana?

I don't know either, but it's definitely not some AI agent.

Conclusion: The fate of public blockchains is ultimately the fate of their governance.

Looking back at Singapore’s story, its success was not due to luck, but because at every critical juncture, it made counterintuitive yet logically and commonsensical decisions: opening when it should open (even accepting gray capital), controlling when it should control (enforcing strict laws to maintain order), and transforming when it should transform (even at the cost of current interests).

Solana stands at a similar crossroads. The meme boom has provided it with renewed momentum and an active user base, but if it fails to accomplish three things before this红利 fades—establishing a dynamic token economic governance mechanism, achieving true decentralization to earn institutional trust, and cultivating a core industry ecosystem beyond memes—it risks becoming like countless other "almost-successful" nations that hesitated during their window of transformation and were ultimately left behind by history.

Competition among public blockchains is short-term driven by narratives, medium-term by technology, and long-term by governance.

Tokens are not just price symbols; they are the currency of digital nations. And monetary policy has never been a fixed curve—it is an art of balance, timing, and restraint.

Postscript:

This article uses Singapore’s development as an analogical framework to analyze the Solana blockchain ecosystem, aiming to provide a new perspective on blockchain governance. Singapore’s historical narrative has been simplified to serve the analogical logic and does not constitute a comprehensive evaluation of Singapore’s policies.

Also, you asked whether the same comparison framework can be used for other blockchains—sure, why not?