Author:Cosmo Jiang, Pantera Capital General Partner

Translated by: Hu Tao, ChainCatcher

2025 will not be a year in which the returns of the cryptocurrency market are primarily driven by fundamentals. Instead, factors such as macroeconomic conditions, positions, capital flows, and market structure will be the main drivers—especially for assets other than Bitcoin.

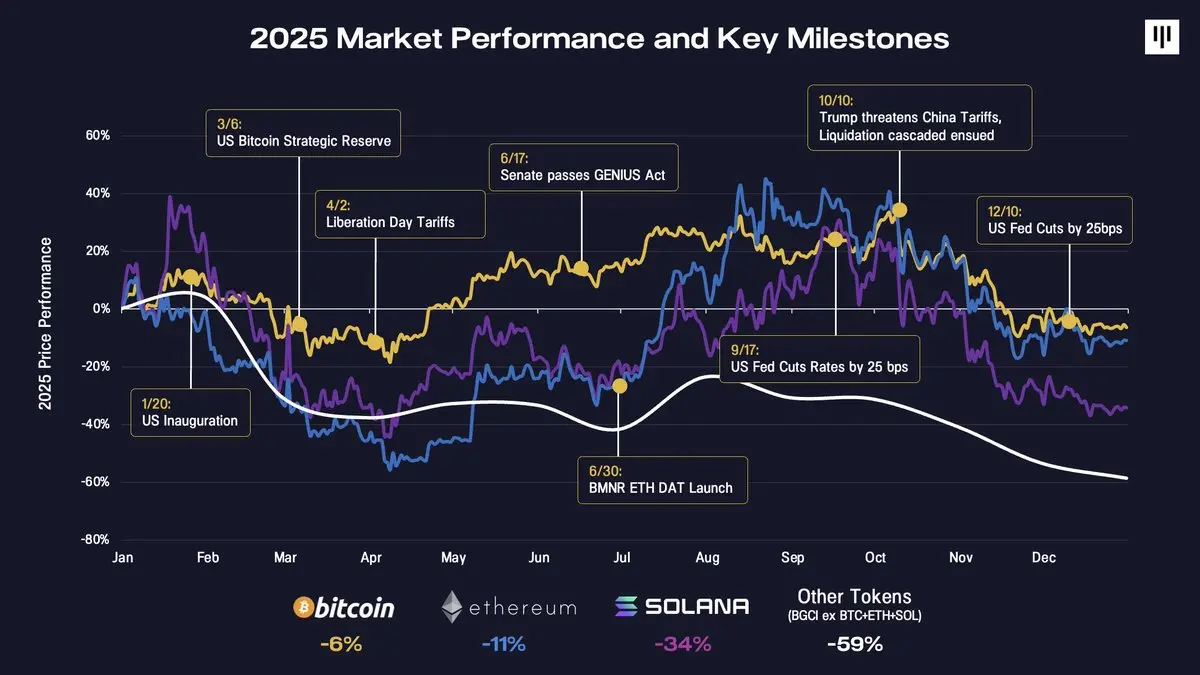

Looking back at the major macroeconomic and policy turning points this year can help explain why market movements feel so disjointed.

The U.S. presidential inauguration at the beginning of the year ultimately proved to be a classic "sell-the-news" event and an early warning signal of market volatility. In the following months, market risk appetite fluctuated repeatedly—from optimism over the announcement of a strategic U.S. Bitcoin reserve, to renewed pressures from the "Liberation Day" tariffs. Some constructive developments emerged in the middle of the year, including the...GENIUS ActThe passage of [unspecified event or regulation], the rise of digital asset treasuries (DAT) such as Bitmine Immersion, and the Federal Reserve's initiation of interest rate cuts have stabilized market sentiment within a few months.

The fourth quarter marked a decisive turning point, as multiple challenges emerged in quick succession. A sell-off on October 10 triggered the largest liquidation cascade in cryptocurrency history—surpassing even the Terra/Luna collapse and FTX liquidations—erasing over $200 billion in notional positions. The market needed time to digest this shock. Meanwhile, the marginal buyers critical to the year (DAT) began exhausting their incremental purchasing power. Seasonal pressures further intensified this downward momentum, including tax-loss selling (especially in the ETF and DAT sectors), portfolio rebalancing, and systematic CTA inflows toward year-end.

Bitcoin fell slightly by about 6% by the end of 2025, while Ethereum dropped approximately 11%. After that, the performance of other tokens deteriorated sharply. Solana fell by 34%, and the broader token market (BGCI, excluding BTC, ETH, and SOL) declined nearly 60%.

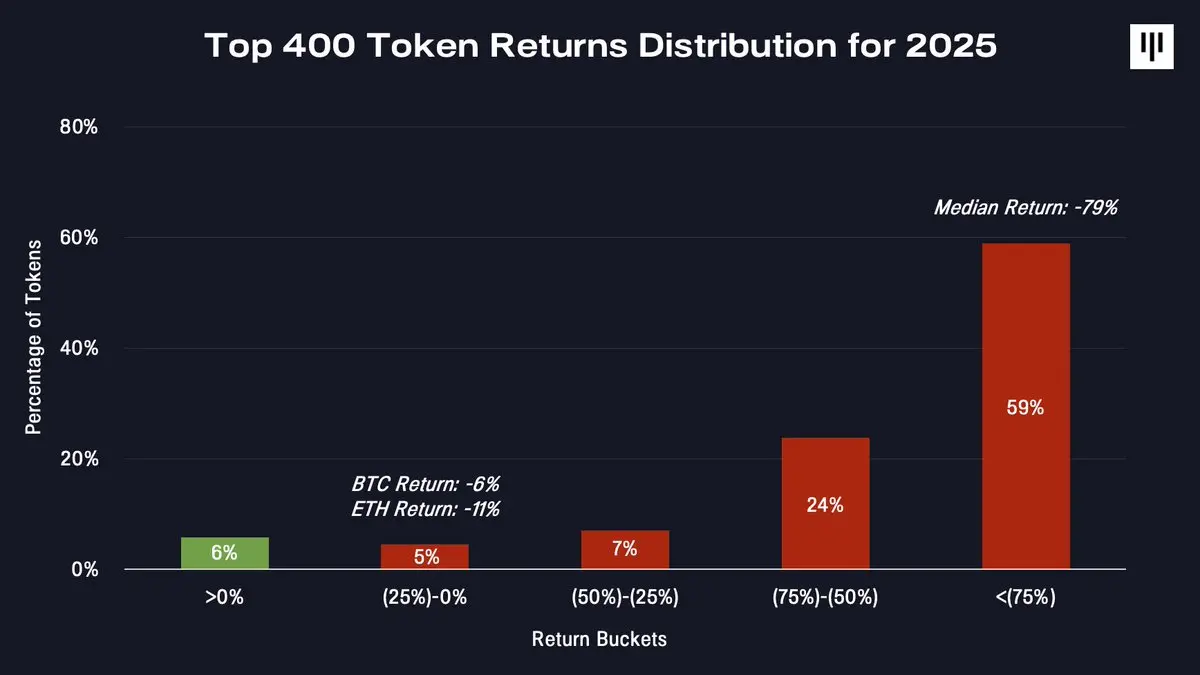

This is an exceptionally narrow market. When examining the return distribution across the entire token market, this dispersion becomes even more apparent.

Only a small number of tokens generated positive returns. The vast majority of tokens experienced significant declines—the median token fell by 79%.

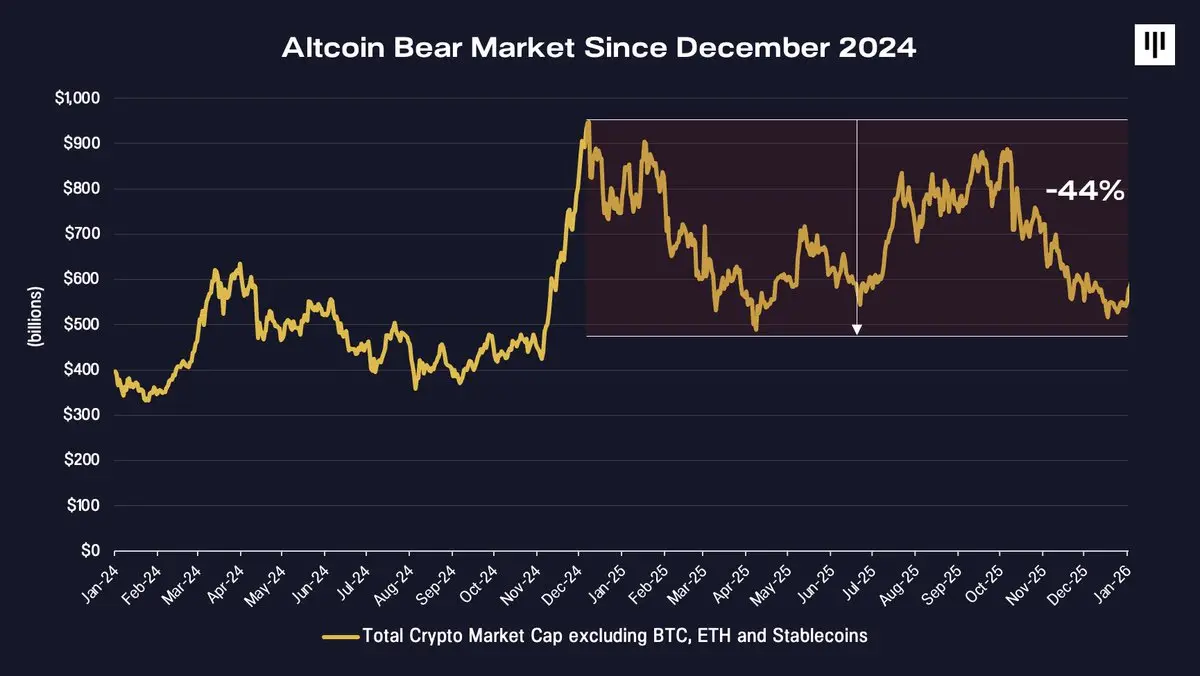

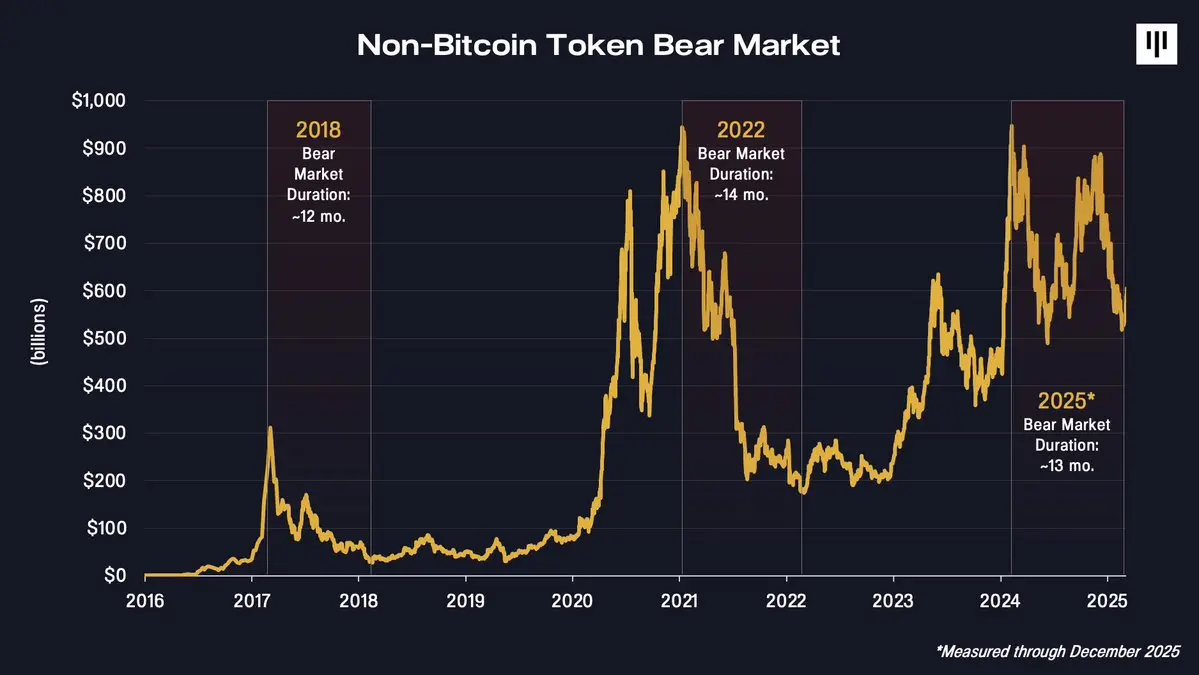

A山寨币 bear market lasting over a year

Perhaps the most underestimated reality of 2025 is that the non-Bitcoin token market has actually been in a bear market since December 2024.

The total market capitalization of cryptocurrencies excluding Bitcoin, Ethereum, and stablecoins peaked by the end of 2024, after which it continued to decline—falling by about 44% by the end of 2025. From this perspective, while Bitcoin appeared to have a year with at least some positive performance, it marked a continuation of a bear market for other cryptocurrencies.

Portfolios with a large holding of small- and medium-sized tokens tend to perform poorly in structure.

The difference between Bitcoin and the broader token market reflects their fundamental distinctions. Bitcoin benefits from a single, widely recognized concept — digital gold — and is increasingly gaining from mechanical demand from institutional actors such as sovereign states, governments, ETFs, and corporate treasuries. In contrast, other tokens represent a heterogeneous array of disruptive technologies, with lower entry barriers and less institutional support.The value capture mechanism is also more complex..

This discrepancy is evident in the prices.

Structural headwinds facing token issuance

In 2025, multiple factors intensified the overall pressure on the token system.

1. Value Accumulation and Investor Rights

One of the most challenging issues is the unresolved question of value accrual. In traditional stock markets, shareholders have clear legal rights to claim cash flows, company governance, and residual value. In contrast, tokens typically rely on protocol-level mechanisms, where value is enforced by code rather than legal frameworks enforced by governmental institutions.

This year, several high-profile cases have highlighted this tension, particularly when token ecosystems were acquired or restructured without providing direct compensation to token holders, as seen in the cases of Aave, Tensor, and Axelar. These incidents have triggered strong market reactions and even shaken confidence in projects previously considered to have relatively stable token economies.

In this context, digital asset stocks outperformed tokens, benefiting from clearer value capture pathways, as investors are now seeking defensive investments.

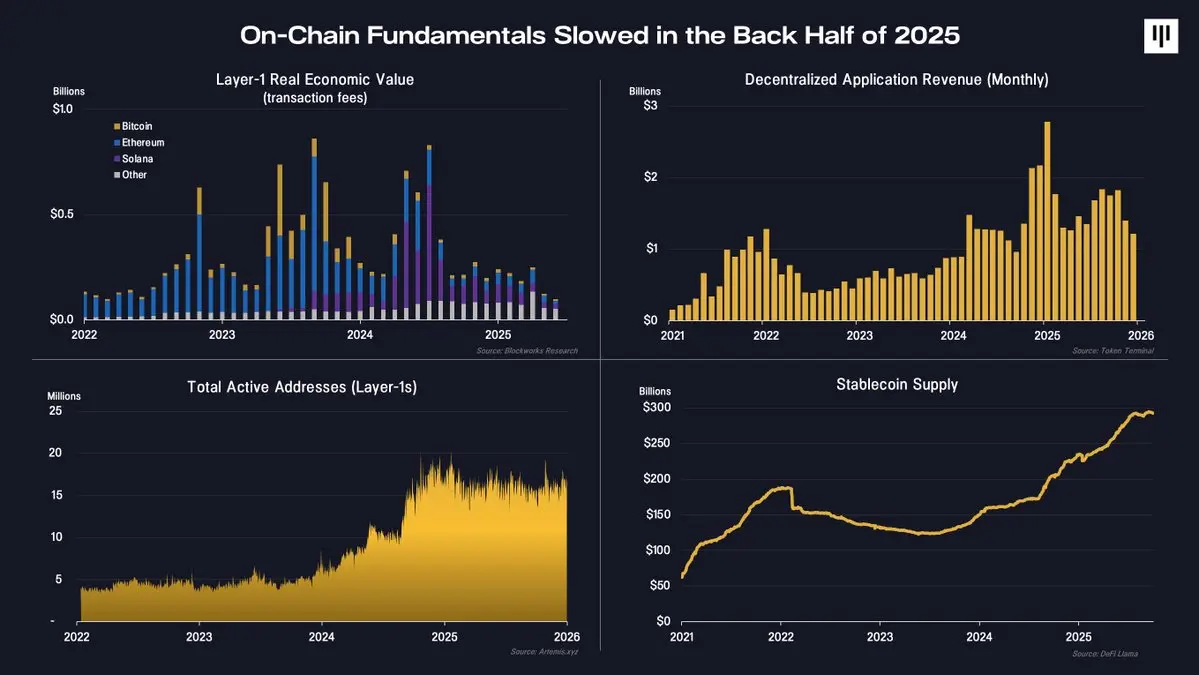

2.Decrease in on-chain activity

The on-chain fundamentals also showed some weakness in the second half of the year.

Key metrics, including Layer 1 blockchain revenue, decentralized application (dApp) fees, and active addresses, indicate a slowdown in the pace of blockchain activity. Notably, the continued growth in stablecoin supply suggests that blockchain applications in the areas of payments and settlements are still increasing. However, most of the economic value associated with stablecoins is flowing into off-chain equity-based companies rather than token-based protocols.

In fact, the use of the base layer continues to exist, but marginal procyclical activities have decreased. This shift has directly affected the token's price trends.

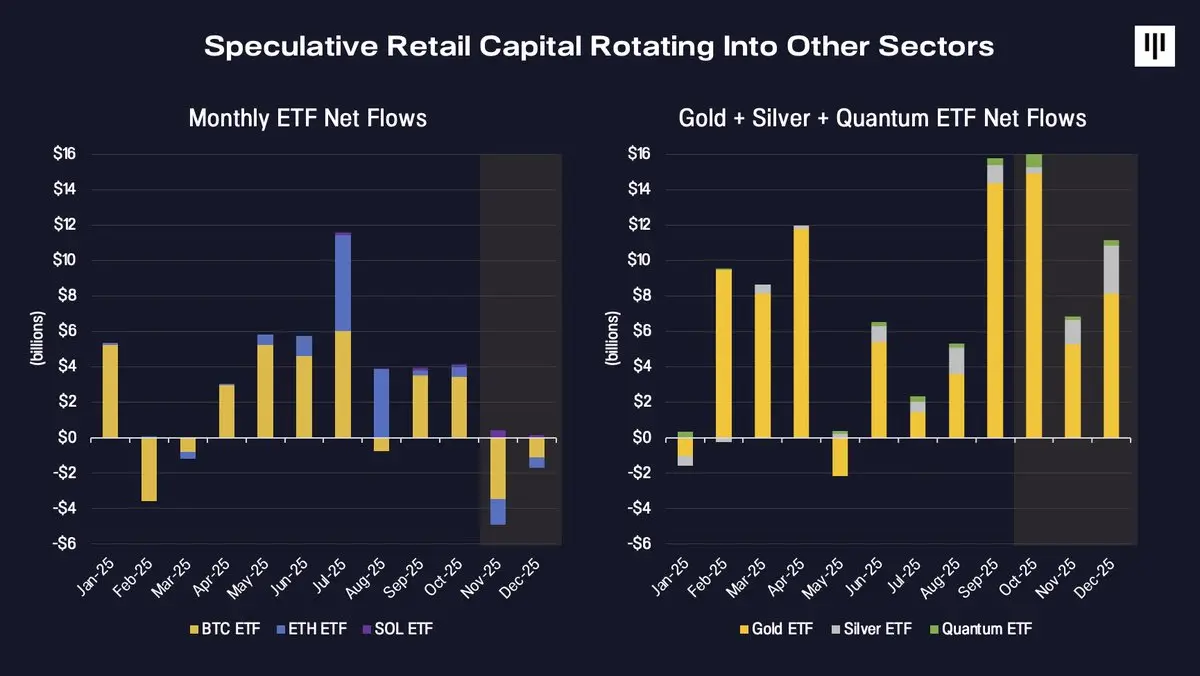

3.Churning of speculative capital

Ultimately, the flow of capital has reversed. Marginal capital supporting broader token ecosystems has historically been dominated by speculative retail investors. Although institutional adoption continues to grow, their capital remains primarily concentrated in assets offered in the form of ETFs, including Bitcoin, Ethereum, and Solana, which is expected to launch by year-end.

In 2025, speculators shifted their attention to other areas.

ETF inflows have significantly increased in emerging thematic trades such as gold, silver, and quantum computing, while inflows into digital asset ETFs have slowed and turned negative in the latter part of the year. This shift in capital coincided with a deterioration in the breadth of the token market, further intensifying the downward momentum.

Emotion, Positioning, and Historical Context

By the end of the year, market sentiment had been compressed to historically levels associated with surrender.

The Fear & Greed Index has reached its highest level since the FTX collapse, during a period of intense market tension. At the same time, the financing rates for perpetual futures have declined, indicating reduced leverage and less speculative excess.

Seasonal factors also play a certain role. Historically, December has often been a weak month for Bitcoin and the broader cryptocurrency market, as tax-loss selling, portfolio rebalancing, and liquidity constraints create mechanical pressures unrelated to fundamentals.

Importantly, from a longer-term perspective, the duration of the current non-Bitcoin decline aligns closely with previous cycles.

The bear markets of 2018 and 2022 lasted approximately 12 to 14 months. The current decline, measured from the peak at the end of 2024, also falls within the same range. This does not guarantee that the market has hit bottom, but it does indicate that the market has already experienced a considerable amount of time and price compression.

Why would the overall situation start to improve from here?

Although 2025 will be full of challenges, there are still several reasons to remain positive and optimistic about the future.

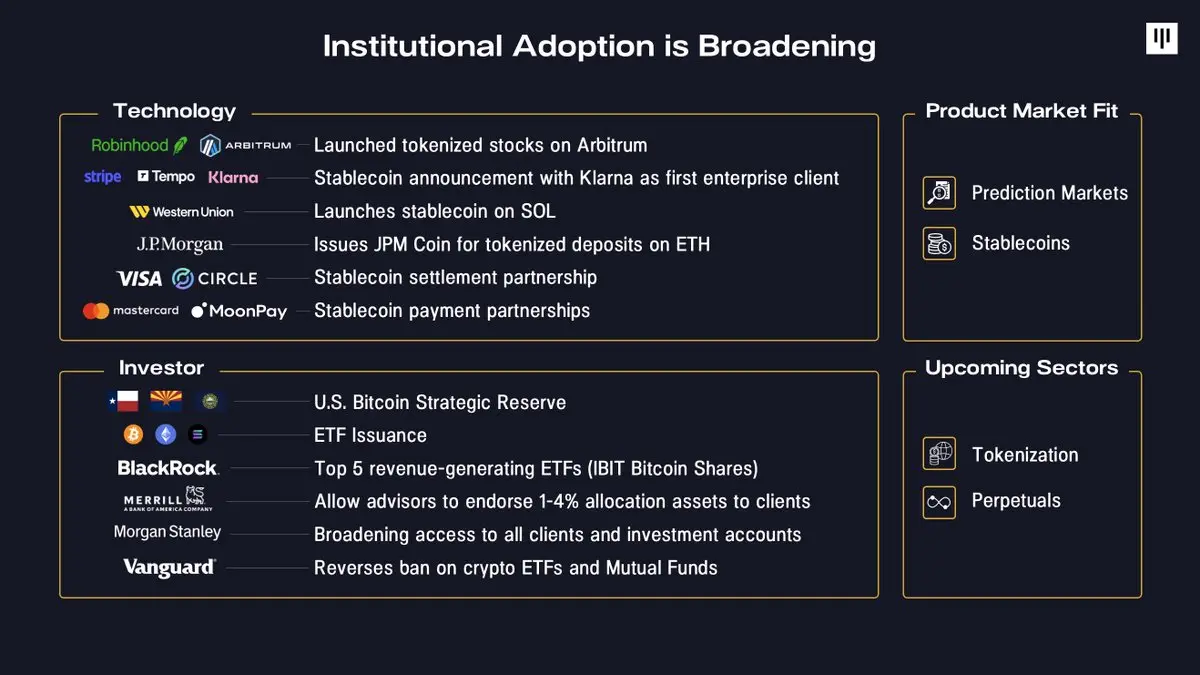

First, the scope of blockchain technology adoption by institutions continues to expand. Enterprises are increasingly integrating blockchain into their core products—from Robinhood's tokenized stocks, to Stripe's development of stablecoin infrastructure, to JPMorgan's tokenization of deposits. In terms of capital, sovereign wealth funds have already been established, and large brokerage firms, retirement platforms, and major asset management companies have significantly lowered the barriers to entry for participation.

Second, product-market fit is becoming increasingly clear. Stablecoins and prediction markets, as prominent application examples in 2025, have gained widespread attention and adoption. Additionally, broader tokenization and perpetual futures are also showing early signs of achieving product-market fit.

Third, the macroeconomic environment is favorable. The U.S. economy remains strong, with wage growth outpacing inflation and corporate profits expanding. As the Federal Reserve halts quantitative tightening, liquidity conditions are improving. Historically, falling long-term yields combined with accommodative monetary policy have been favorable for risk assets, including digital assets.

Finally, the penetration rate of digital assets remains very low. As Tom Lee from Bitmine noted: currently, only 4.4 million Bitcoin addresses hold Bitcoin worth more than $10,000, while the number of traditional investment accounts globally reaches 900 million. According to a survey of institutional investors by Bank of America, 67% of professional investment managers still do not invest in any digital assets. Even small shifts in asset allocation over time would represent a significant source of potential demand.

Conclusion

2025 will be a tough year for most participants in the token market, marked by extreme market fragmentation, strong performance from major tokens, and continued weakness in tokens outside of Bitcoin. However, this year also promoted adoption by institutional investors, clarified product-market fit, and compressed valuations for the majority of tokens within the ecosystem.

After a year-long bear market, a strong fundamental recovery in the overall token market may present investment opportunities. With market sentiment cooling, leverage ratios decreasing, and the period of significant price repricing behind us, forward-looking investment positioning appears increasingly asymmetric—provided fundamentals stabilize and market breadth recovers. Historically, market turbulence has often laid the foundation for the next phase of growth.