Leopold Aschenbrenner Full Q1 2026 13F Breakdown

2026/05/20 08:00:00

The global financial landscape witnessed a seismic shift following the release of the regulatory disclosures for the first quarter of 2026. Institutional investors, macro hedge funds, and cryptocurrency market participants are deeply dissecting the latest moves of elite asset managers to position themselves for the next phase of the artificial intelligence and digital asset supercycle.

This comprehensive guide delivers a detailed Leopold Aschenbrenner Full Q1 2026 13F Breakdown, analyzing how his fund, Situational Awareness LP, balances a massive $8.5 billion semiconductor short position with strategic long bets in AI energy infrastructure and public bitcoin mining operations.

Key Takeaways:

The Explosive Growth of Situational Awareness LP

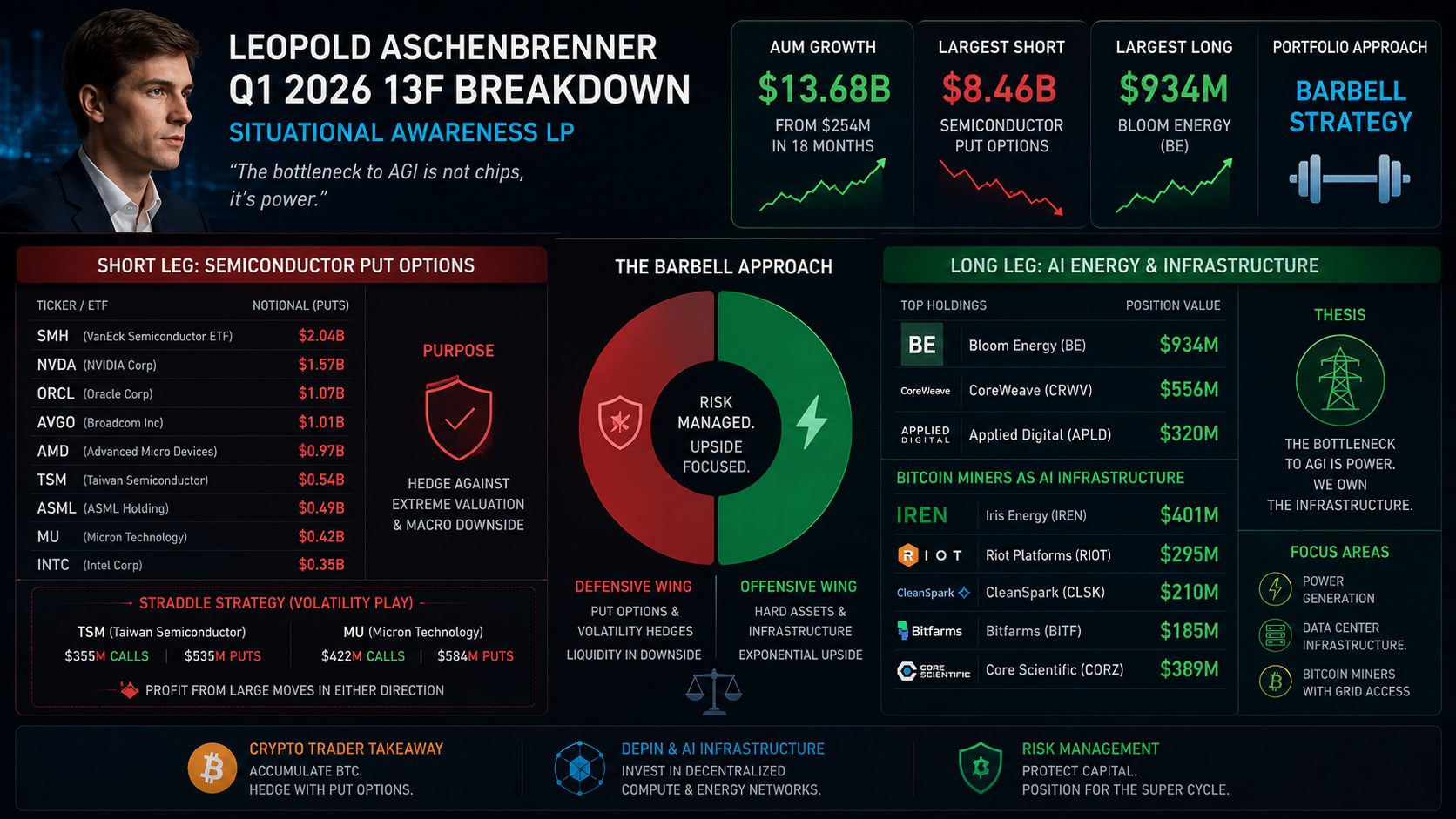

Leopold Aschenbrenner, the 24-year-old former OpenAI Superalignment researcher, has rapidly transitioned from a prominent Silicon Valley technologist to one of the most formidable macro forces on Wall Street. Founded on the core conviction that the path to Artificial General Intelligence (AGI) by 2027 is an inevitability, his investment vehicle, Situational Awareness LP, has seen its Assets Under Management (AUM) balloon from a modest initial capital base of $254 million to an astonishing $13.68 billion in institutional assets within roughly 18 months.

This meteoric rise represents one of the fastest expansions of a thematic macro hedge fund in corporate history. The fund's rapid capital accumulation reflects intense institutional appetite for a vehicle that unifies frontier AI intelligence, macroeconomic derivative structuring, and hard-asset infrastructure investing under a single strategic mandate.

Why the $8.5B Chip Short Caught Markets Off Guard

When the Q1 2026 13F regulatory filing officially went public, the headline figures sent a massive shockwave across global trading desks. The fund disclosed a staggering $8.46 billion notional short position concentrated heavily across the premium semiconductor supply chain. For a fund manager whose entire public persona and professional ethos are built on being an uncompromising, ultimate bull on the exponential acceleration of artificial intelligence, an aggressive multibillion-dollar bet against the very hardware enabling that revolution appeared fundamentally contradictory.

Retail trading communities and financial commentators immediately began pushing a narrative that the AI prophet had dramatically reversed his core thesis and was now anticipating a structural collapse of the global compute economy. However, as experienced derivative traders and institutional allocators know, looking at raw 13F data without context often results in highly flawed conclusions.

The 13F Filing Illusion: What You Aren't Seeing

To truly comprehend the portfolio architecture of Situational Awareness LP, one must understand the structural limitations inherent in institutional reporting frameworks. A standard Form 13F filing is a mandatory, backward-looking quarterly disclosure required by the U.S. Securities and Exchange Commission (SEC). Crucially, it only captures a highly restricted slice of an institutional manager's total book: long positions in U.S.-listed equities, shares of exchange-traded funds (ETFs), and long equity options (both calls and puts).

The 13F filing completely blinds the public to several critical components of a sophisticated hedge fund's total exposure, including:

-

Outright short equity positions (short selling actual stock shares)

-

Non-U.S. equity holdings (assets listed in London, Tokyo, or European exchanges)

-

Over-the-counter (OTC) equity swaps and customized exotic derivatives

-

Commodities, fixed-income products, credit structures, and cash equivalents

-

Direct holdings in physical spot crypto assets, futures, or private venture capital allocations

Consequently, when the public reviews Aschenbrenner's filing and observes massive put option exposure contrasted against near-zero long equity positions in companies like NVIDIA, they are viewing an illusion of transparency. The multi-billion-dollar put options do not imply a blind, directional bet on a tech sector collapse. Instead, they represent a highly calculated, structured leg of a much broader, multi-asset macro relative value trade that utilizes alternative instruments completely hidden from public SEC view.

The Short Leg: Analyzing the $8.5B Semiconductor Puts

Big Bets Against Tech: Dissecting SMH and NVDA Puts

The core of the fund’s disclosed defensive perimeter lies in massive put option positions targeting the primary locomotives of the multi-year technology rally. Rather than stock picking small-cap downside, Situational Awareness LP went straight for the systemic core of the market's liquidity and valuation expansion.

The breakdown reveals that the disclosed Q1 2026 put option positions are heavily concentrated by notional value. The VanEck Semiconductor ETF (SMH) takes up approximately $2.04 billion of the book. NVIDIA Corp (NVDA) follows closely with a massive $1.57 billion allocation. Oracle Corp (ORCL) commands $1.07 billion, while Broadcom Inc (AVGO) sits right behind with a $1.01 billion position.

The massive position in SMH puts provides broad, highly liquid beta protection against a sector-wide contraction. Meanwhile, the $1.57 billion put position on NVIDIA targets a firm trading at peak multi-year valuation multiples. By purchasing these deep out-of-the-money or at-the-money put options, the fund isolates the extreme premium embedded in these names. If a broader macroeconomic slowdown, liquidity contraction, or systemic re-pricing occurs, these puts convert instantly into multi-billion-dollar cash engines. This strategy provides the fund with immense liquidity precisely when asset valuations elsewhere are depressed.

Hedging Global Risk: Broadcom, AMD, and ASML Positions

Beyond the immediate hyper-scalers, the short leg of the portfolio branches deeply into the foundational international monopolies and duopolies that underpin the hardware landscape. The breakdown reveals heavy put positions across crucial cross-sections of the silicon ecosystem:

-

Advanced Micro Devices (AMD): $969 million in notional put options, capturing downside risk in secondary GPU and x86 compute markets.

-

Taiwan Semiconductor Manufacturing Co. (TSM): $535 million in put exposure, hedging against geopolitical tail risks, supply chain friction, and fabrication concentration in the Taiwan Strait.

-

ASML Holding (ASML): $494 million in put positions, establishing a downside hedge against capital expenditure pullbacks by major foundries and slowing lithography machine demand.

-

Micron Technology (MU) & Intel Corp. (INTC): Combined hundreds of millions in additional put options, covering memory cycles and legacy foundry turnaround execution risks.

By executing this comprehensive sweep, Aschenbrenner has effectively shorted the valuation layer of the chip sector. The thesis here is not that these businesses will fail operationally, but rather that their current equity valuations assume flawless execution, infinite capital expenditure expansion, and frictionless global supply chains—assumptions that rarely survive a full market cycle.

The 45-Day 13F Lag: Did the Chip Rally Crush the Trade?

A critical factor that retail observers overlooked following the Q1 2026 data release is the temporal disconnect of the reporting mechanism. Form 13F filings reflect a historical snapshot of positions held precisely on March 31, 2026, and managers are granted a 45-day grace period to submit the documentation. In the intervening seven weeks between the end of the quarter and the mid-May public disclosure, global semiconductor equities experienced a powerful, liquidity-driven counter-trend rally.

On paper, financial commentators claimed that anyone holding outright puts on chipmakers through April and early May would have faced immense drawdowns or total premium wipeouts. However, this simplistic view assumes that the puts were static, unhedged, long-gamma directional gambles.

In institutional volatility trading, these options are dynamically managed. Long put options are routinely gamma-scalped, balanced against long futures contracts, or integrated into complex OTC total return swap architectures. The subsequent market rally does not mean the trade was "crushed"; instead, it likely indicates that the fund's hidden long exposures or dynamic delta-hedging mechanisms captured the upside, while the puts remained intact as essential structural insurance against a sudden macro breakdown.

The Hard Asset Long Leg: Betting on AI Energy Infrastructure

The AGI Bottleneck: Why the Next Constraint is Power

To reconcile Aschenbrenner’s absolute conviction in AGI with his massive semiconductor short, one must analyze the physical reality of scaling advanced neural networks. In his foundational research, Aschenbrenner continuously highlights that the ultimate bottleneck for training and operating next-generation frontier models is no longer the raw design or availability of processing chips. The true limiting factor of the late 2020s is the availability of consistent, base-load electric power and grid interconnection capacity.

A cluster of 100,000 modern GPUs requires hundreds of megawatts of continuous power. Scaling these clusters by another order of magnitude demands gigawatt-scale infrastructure. The AI scaling bottleneck evolution has moved rapidly. While 2022 to 2024 was focused on algorithmic efficiencies, and 2024 to 2025 centered on GPU fabrication and interconnects, 2026 and the future will be entirely dominated by megawatts and grid access.

The traditional civilian electrical grid is structurally unequipped to handle this unprecedented load growth, with interconnection queues stretching anywhere from five to seven years in major data center hubs. Consequently, the true value accrual in the AI ecosystem is shifting down the stack from the digital layer (chips and software) to the physical layer (electrons, land, and energy generation).

Bloom Energy (BE): Unpacking the Largest Long Position

The ultimate confirmation of this infrastructure-centric thesis is found in the fund's single largest disclosed long equity holding: Bloom Energy Corp. (BE). Situational Awareness LP revealed an absolute powerhouse position consisting of $879 million in direct common equity, supplemented by an additional $55 million in long call options, bringing the total disclosed exposure to $934 million. Bloom Energy specializes in manufacturing proprietary, utility-scale solid-oxide fuel cells that generate highly reliable, on-site baseload power using natural gas, biogas, or hydrogen.

This massive bet illustrates a clear operational strategy. Because hyperscalers cannot afford to wait over half a decade for local utility monopolies to approve grid hookups, they are increasingly entering into agreements for "behind-the-meter" power generation. Bloom Energy’s fuel cell technology allows massive data centers to be built completely independent of the traditional electrical grid. By holding the dominant long position in BE, Aschenbrenner is positioned directly at the literal source of the electrons required to keep the lights on in the world's most advanced compute clusters.

CoreWeave and Applied Digital: Controlling the Compute Layer

Directly adjacent to raw energy generation, the long leg of the 13F filing features massive, concentrated allocations into specialized, institutional-grade data center infrastructure operators:

-

CoreWeave: Disclosed at $556 million in equity and call options. CoreWeave is a pioneer in the specialized cloud provider space, securing tens of thousands of top-tier GPUs through elite partner allocations and housing them in highly optimized, ultra-low-latency data center environments.

-

Applied Digital Corp. (APLD): Held at $320 million within the portfolio. Applied Digital designs, builds, and operates massive, next-generation high-performance computing (HPC) data center facilities specifically engineered to handle the extreme power densities and liquid-cooling demands of modern AI clusters.

These positions demonstrate that Situational Awareness LP is avoiding the hyper-competitive commodity chip market. Instead, the fund is locking up the specialized physical real estate and infrastructure required to house and cool those chips. It is a classic "landlord" model applied to the cutting edge of technological advancement.

The Crypto Pivot: Bitcoin Miners as AI Land Grab

Selling Hut 8 and Cipher: Portfolio Rebalancing in 2026

One of the most compelling strategic developments revealed in the Leopold Aschenbrenner Full Q1 2026 13F Breakdown is the aggressive rotation occurring within the digital asset and crypto mining sleeve of the portfolio. The fund executed a decisive rebalancing maneuver, completely exiting or dramatically reducing its historical holdings in legacy operations such as Hut 8 Mining and Cipher Mining.

This liquidation was not an indictment of the broader digital asset ecosystem, but rather a calculated rotation away from companies with sub-optimal capital expenditure structures or lagging timelines in infrastructure conversion. Aschenbrenner redirected this newly unlocked liquidity into a highly concentrated group of institutional public bitcoin mining firms that possess a distinct structural advantage: immediate, massive power capacity and high-voltage grid interconnection permits that can be rapidly repurposed for high-performance computing and AI hosting.

Loading Up: Big Stakes in Riot, CleanSpark, and Bitfarms

The capital redeemed from legacy positions was immediately deployed into the undisputed titans of industrial-scale digital asset infrastructure. The Q1 2026 filing highlights major equity accumulation across a select basket of elite public miners. The public bitcoin mining infrastructure long positions show clear concentration: Iris Energy (IREN) commands $401 million; Riot Platforms (RIOT) sits at $295 million; CleanSpark (CLSK) holds $210 million; and Bitfarms (BITF) secures $185 million.

Additionally, the fund established a substantial $389 million position in Core Scientific (CORZ), which has set the gold standard for the industry by securing historic, multi-billion-dollar, multi-hundred-megawatt hosting contracts with hyperscalers like CoreWeave. These operators are no longer evaluated by institutional macro funds solely on their daily bitcoin production metrics. Instead, they are being valued as high-density energy infrastructure plays. Their massive, operational power footprints across North America and Europe make them the fastest vehicles through which hyperscalers can scale their hardware deployments.

Grid Permits: The True Real Estate Value of Crypto Mining

For a cryptocurrency exchange platform and its global trading user base, this specific section of the 13F breakdown offers profound long-term insights. The traditional investment community historically viewed bitcoin miners as highly cyclical, speculative proxies for the spot price of BTC. Aschenbrenner’s strategy completely reframes this narrative by treating public miners as premium, specialized real estate investment trusts (REITs).

The true underlying asset of an industrial bitcoin mining facility is not the fleet of ASICs currently hashing on the network. The true value lies in the physical land, the heavy-duty electrical substations, the proprietary cooling systems, and, most importantly, the approved high-voltage grid interconnection permits. The asset valuation framing has completely shifted from the legacy retail view of ASIC fleets and daily rewards to an institutional macro view focused on gigawatt power permits and high-voltage substations.

In 2026, obtaining a new 500-megawatt grid connection permit in a stable jurisdictional territory is an incredibly complex, politically fraught regulatory process that can take a long time to complete. Public bitcoin miners already possess these gigawatt-scale power allocations. If bitcoin mining profitability drops due to network difficulty or halving events, these firms can simply pivot their physical infrastructure to host AI GPUs for hyperscalers at incredibly high margins. This optionality creates a powerful, structural valuation floor that the market is only beginning to understand.

Options Strategy: Volatility vs. Directional Bets

TSMC and Micron Straddles: Trading the Volatility

A deep-dive technical options analysis of Situational Awareness LP’s portfolio completely dismantles the simplistic narrative that the fund is making a directional, apocalyptic bet against technology hardware. The definitive proof lies in the massive, simultaneous long call options and long put options held on core semiconductor supply chain names—specifically Taiwan Semiconductor Manufacturing Co. (TSM) and Micron Technology (MU).

The semiconductor straddle structures are massive in scale. For Micron (MU), the fund holds $422 million in long calls alongside $584 million in long puts. For TSMC (TSM), the layout consists of $355 million in long calls paired with $535 million in long puts. Both setups represent massive net volatility positions.

In professional derivative trading, holding large call and put positions with identical or similar expiration dates and strike prices forms a long straddle or long strangle options strategy. This structure is completely agnostic to directional market moves. The trade does not require the underlying stock price to rise or fall specifically; rather, it requires that the market experience a massive move in either direction that exceeds the combined premium paid for the options.

By structuring the portfolio this way, Aschenbrenner is monetizing extreme macro and industry volatility. This volatility can be driven by a variety of high-impact catalysts, including:

-

Major geopolitical escalations or supply chain blockades in East Asia

-

Extreme cyclical inflections in global high-bandwidth memory (HBM) supply-demand balances

-

Dramatic earnings surprises or sudden capital expenditure revisions from hyperscalers

The straddles ensure that the fund generates significant returns from structural market instability, completely independent of whether the broader tech market goes up or down.

Storage Boom: Why Calls on SanDisk Fuel the Portfolio

Simultaneously, the fund has isolated specific hardware sub-sectors where demand is highly asymmetric and inelastic. This is evidenced by a major long position in SanDisk (via equity and a dedicated $380 million long call option sleeve), alongside a broader $724 million combined exposure in parent or related storage architectures.

The algorithmic reality of training advanced reasoning models in 2026 demands not just processing speed, but massive, ultra-fast data ingestion capabilities. High-density enterprise solid-state drives (SSDs) and NAND flash memory layers are experiencing unprecedented demand backlogs as data centers race to store petabytes of training data directly adjacent to compute clusters.

By purchasing leveraged call options on premium storage providers, Aschenbrenner injects pure, long-gamma upside into the portfolio. This exposure is designed to experience exponential value growth if a massive supply squeeze occurs in the enterprise flash memory market.

The Barbell Approach: Concentrated Longs vs. Tail Hedges

When we step back and synthesize the entire portfolio architecture revealed in this breakdown, we see a textbook implementation of Nassim Nicholas Taleb’s famous Barbell Investment Strategy. The fund actively rejects the traditional wealth management approach of holding a diversified, mediocre basket of highly correlated stocks. Instead, the portfolio is split into two extreme, hyper-focused domains.

The Situational Awareness LP portfolio barbell relies on an extreme defensive wing containing $8.5 billion in long put options and market straddles on one side, balanced against an extreme offensive wing composed of concentrated longs in energy, power, and public bitcoin miners on the other.

The defensive wing is built to generate immense liquidity and cash returns if a major market crash occurs. The offensive wing is highly concentrated in physical assets that possess structural pricing power and immense long-term upside. By structuring the portfolio this way, the fund is insulated from middle-tier market volatility. It is fully protected against black swan macro drawdowns while maintaining maximum upside exposure to the physical deployment of next-generation artificial intelligence infrastructure.

Exchange Insights: How Crypto Traders Can Play This

Crypto Barbell: Spot Bitcoin vs. Volatility Derivatives

For retail and institutional traders operating on cryptocurrency exchange platforms, the strategic insights gleaned from Aschenbrenner’s Q1 2026 13F filing provide an actionable blueprint for modern digital asset portfolio construction. The primary lesson is the immediate rejection of unhedged, directional exposure. Traders can mirror this professional asset management approach by constructing a digital asset barbell portfolio.

On our exchange platform, this looks like maintaining a core, highly secure allocation of Spot Bitcoin (BTC) or Ethereum (ETH) as your foundational long-term investment. Simultaneously, instead of chasing speculative, unhedged altcoins, a portion of capital is allocated to volatility derivatives.

By utilizing crypto options contracts—such as purchasing out-of-the-money put options on BTC during periods of historically low implied volatility—traders can effectively insulate their portfolios from systemic downside events. This approach ensures that if a sudden regulatory shock, liquidity squeeze, or macroeconomic drawdown occurs, the exponential gains generated by the long puts provide instant cash to accumulate deeply discounted spot digital assets at the absolute cycle bottom.

AI Coins and DePIN: Finding the Crypto Power Equivalents

As the traditional venture capital and macro hedge fund landscape rotates capital aggressively out of overvalued semiconductor equities and into physical power layers, crypto asset markets offer highly parallel, high-yield opportunities. Smart market participants should look beyond standard layer-1 protocols and identify digital assets operating directly at the intersection of AI compute coordination and decentralized physical infrastructure networks (DePIN).

The structural shift aligns perfectly when comparing traditional 13F institutional assets to on-chain crypto exchange analogs. While the fund targets Bloom Energy and public power grids, crypto traders can look toward decentralized energy networks via DePIN. Where the fund scales into CoreWeave for data center infrastructure, the crypto ecosystem offers decentralized GPU compute marketplaces. Finally, institutional plays in high-density enterprise storage map naturally onto decentralized storage protocols on the blockchain.

These decentralized cryptographic networks create dynamic, borderless marketplaces that optimize the utilization of global hardware resources. Rather than waiting years for centralized data centers to build physical facilities, on-chain compute protocols allow global enterprises to instantly aggregate idle computing power from distributed independent data centers worldwide. Investing in the native utility tokens of verified DePIN projects provides crypto traders with direct exposure to the exact same macroeconomic tailwinds that Aschenbrenner is targeting with his multi-hundred-million-dollar bets on CoreWeave and Applied Digital.

Risk Management: Using Put Options in Crypto Trading

The most critical takeaway for the global trading community from this portfolio breakdown is the elevated role of advanced derivative instruments as structural risk management tools, rather than instruments of blind gambling. In the digital asset markets, retail traders frequently abuse leverage through high-risk perpetual futures contracts, often resulting in sudden liquidations during normal market corrections.

Aschenbrenner’s widespread use of option structures demonstrates the immense value of defined-risk trading. When you purchase a put option on a cryptocurrency exchange, your maximum financial downside is strictly limited to the upfront premium paid for the contract, regardless of how high the market asset price rallies.

Conversely, the upside potential of that option contract if the asset price experiences a severe drop is multi-exponential. By integrating systematic options trading into your daily regime—such as buying protective puts prior to major macroeconomic events like Federal Reserve interest rate announcements, consumer price index (CPI) data drops, or major network upgrades—you ensure that your trading capital is fully protected against liquidation. This disciplined framework allows you to survive major market corrections and maintain the long-term positioning required to achieve generational wealth across the digital asset cycle.

Conclusion

In summary, the Leopold Aschenbrenner Full Q1 2026 13F Breakdown reveals a brilliant, multi-layered macro strategy that moves far beyond basic market narratives. By combining an $8.5 billion semiconductor short position with massive long bets on energy infrastructure and public bitcoin miners, Situational Awareness LP has built a highly resilient, convex barbell portfolio. For crypto traders and global digital asset investors, this filing provides a clear roadmap: reduce exposure to over-hyped valuation layers, accumulate the physical energy and decentralized compute protocols that form the infrastructure layer of the future economy, and systematically protect capital using advanced derivative options.

FAQ:

What is Leopold Aschenbrenner’s main investment thesis for 2026?

Leopold Aschenbrenner’s investment strategy focuses on the physical constraints of scaling artificial intelligence. His fund bets that the ultimate bottleneck for achieving AGI is the availability of electric power, land, and data center infrastructure, rather than chip designs which currently trade at peak valuation multiples.

Why did Situational Awareness LP buy $8.5 billion in semiconductor puts?

The $8.5 billion put option portfolio serves as a highly leveraged macro hedge against extreme valuations in the semiconductor sector. It is designed to protect the fund's concentrated long infrastructure positions and generate massive cash liquidity during a broader technology market correction.

What are the largest long positions in the Q1 2026 13F filing?

The single largest disclosed long equity holding is Bloom Energy Corp (BE), with over $930 million in combined stock and call options. Other major long allocations include specialized AI cloud data center provider CoreWeave, alongside several industrial public bitcoin mining firms.

Why does the fund hold massive positions in public bitcoin miners?

The fund treats public bitcoin mining companies as high-density energy infrastructure plays. These firms already possess valuable, gigawatt-scale grid interconnection permits and electrical substations, which can be rapidly pivoted to host high-performance AI GPU clusters for major hyperscalers.

What is a straddle option strategy, and how is it used in this portfolio?

A straddle involves simultaneously buying call and put options on the same stock. Aschenbrenner uses this strategy on highly volatile names like TSMC and Micron to profit from massive price swings caused by supply chain disruptions or earnings surprises, without needing to predict the market's direction.

How can crypto traders apply these insights on an exchange platform?

Crypto traders can mirror this strategy by maintaining a core spot Bitcoin holding while using protective put options to hedge against downside risk. Additionally, traders can rotate capital into decentralized physical infrastructure networks (DePIN) and decentralized compute tokens that mirror physical energy assets.