A Historical Analysis of Berkshire Hathaway’s Strategic Cash Positions: Drivers and Objectives

2026/06/06 11:00:00

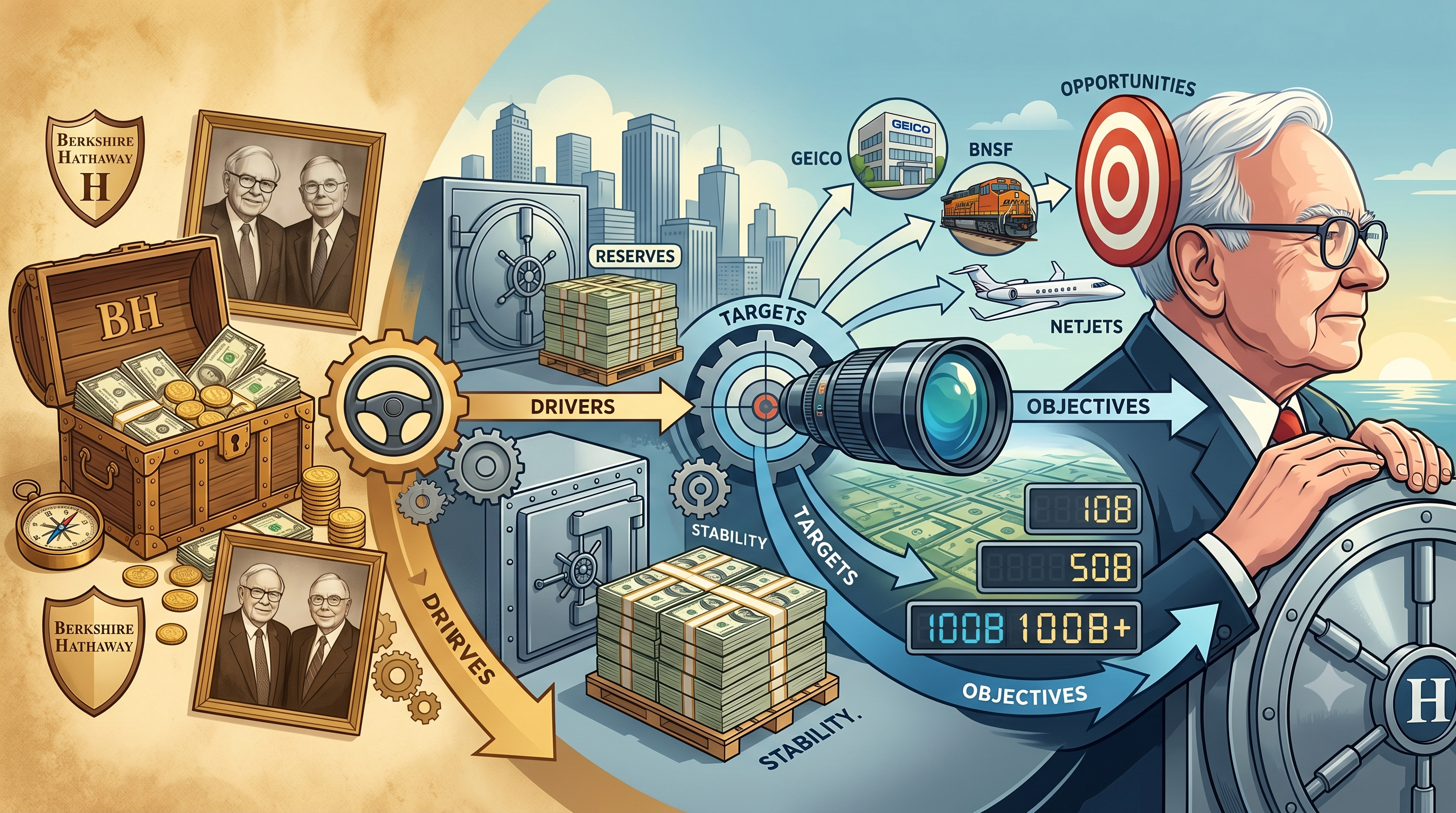

Berkshire Hathaway’s strategic cash accumulation stems from valuation caution, insurance float dynamics, and a commitment to preserving optionality for superior opportunities, a pattern evident across market cycles that prioritizes capital preservation and opportunistic deployment over constant investment. Berkshire Hathaway has built one of the largest corporate liquidity reserves in history, reaching approximately $397 billion in cash and short-term U.S.

Treasury bills by the end of Q1 2026. This position reflects decades of disciplined capital allocation under Warren Buffett and continues under new CEO Greg Abel. The company’s approach emphasizes patience over forced deployment, allowing it to generate steady operating earnings while maintaining flexibility. Recent quarterly results show continued net equity sales alongside strong performance from insurance and railroad operations, underscoring a philosophy rooted in long-term value rather than short-term market participation.

Evolution of Berkshire’s Cash Reserves Across Market Cycles

Berkshire Hathaway’s cash management has evolved significantly since Warren Buffett took control in the mid-1960s, transforming from a textile firm into a diversified conglomerate with substantial liquidity as a core feature. In the late 1990s, as technology valuations soared, Buffett built cash positions by avoiding the dot-com frenzy, a move that protected the firm during the subsequent bust. By the mid-2000s, reserves grew ahead of the 2008 financial crisis, enabling pivotal investments such as preferred stock in Goldman Sachs. Data from MacroTrends illustrates fluctuations, with cash on hand reaching notable levels in periods of perceived overvaluation, such as $44 billion around 2007 before crisis deployments.

Entering the 2010s and 2020s, Berkshire navigated low-interest environments where holding cash carried higher opportunity costs, yet it still accumulated reserves during stretched valuations. The COVID-19 period saw adjustments, with cash supporting stability amid volatility. By 2022-2025, the pile expanded dramatically as equity markets, propelled by technology and artificial intelligence enthusiasm, hit record highs. Q1 2026 figures show $58.122 billion in cash equivalents plus $339 billion in Treasury bills, totaling around $397 billion, a record that represents a substantial portion of investable assets.

This historical journey shows consistent drivers: avoidance of overpriced assets and preparation for dislocations. Operating businesses, particularly insurance, generate reliable cash flows that bolster reserves without reliance on external financing. Under Greg Abel’s early tenure, the strategy persists, with net stock sales of about $8 billion in Q1 2026 contributing to growth despite resumed modest buybacks. The approach has allowed Berkshire to weather downturns while positioning for outsized returns when opportunities emerge, distinguishing it from peers chasing immediate yields. Interest income from Treasuries now provides meaningful returns in the current rate environment, reducing the traditional drag of cash holdings.

Key Drivers Behind Decades of Cash Accumulation

Valuation discipline stands as a primary driver of Berkshire Hathaway’s cash strategy, with leadership historically stepping back when asset prices appear elevated relative to intrinsic value. Buffett’s letters and meetings frequently reference the difficulty of finding “elephant-sized” deals at reasonable prices, a theme amplified in recent years amid high S&P 500 CAPE ratios. This caution led to net equity sales across multiple quarters, including trims in major holdings like Apple, contributing to the cash build-up from around $128 billion in late 2022 to nearly $400 billion by early 2026.

Insurance operations provide another critical driver through float, the premiums collected before claims are paid, which creates low-cost capital available for investment or holding. Float reached approximately $177 billion by late 2025, offering a stable funding source that supports liquidity without debt pressure. Strong underwriting results in Q1 2026 further enhanced earnings, feeding reserves. Additionally, higher short-term Treasury yields since 2023 have made cash holdings more attractive, generating billions in annual interest income and lowering the opportunity cost compared to zero-rate periods.

Tax considerations and succession planning also influence decisions. Trimming appreciated positions like Apple triggered capital gains but locked in gains ahead of potential policy shifts. Handing a robust balance sheet to Greg Abel ensures flexibility in uncertain markets. Berkshire’s decentralized structure and conservative leverage, with a debt-to-equity ratio around 19%, reinforce this fortress approach. These drivers interact to prioritize long-term resilience, enabling the firm to avoid forced sales during stress while awaiting quality entry points. Historical parallels, such as pre-2008 buildup, validate the logic, as deployments then yielded significant returns. In 2026, with equities near highs, this measured stance continues to shape capital allocation.

Insurance Float as a Foundation for Liquidity Strategy

Berkshire Hathaway’s insurance subsidiaries, including GEICO and reinsurance operations led by Ajit Jain, generate substantial float that underpins its cash position. This float, premiums held before payout, functions as interest-free leverage, historically averaging strong returns when invested wisely. By the end of 2025, float stood near $177 billion, up from prior years, providing a reliable base that supports larger cash reserves without compromising solvency. Underwriting discipline has improved results, with Q1 2026 operating earnings benefiting from better performance in this segment. Float allows Berkshire to maintain elevated liquidity while still deploying capital into equities or businesses selectively. Unlike traditional insurers, Berkshire’s scale and culture emphasize profitability over volume, minimizing reserve shortfalls.

This foundation enabled major crisis responses, such as post-2008 investments, where available capital translated into advantageous terms. The interplay between float growth and overall cash strategy creates a self-reinforcing cycle. Operating cash flows from insurance, combined with contributions from BNSF railway and utilities, consistently add to reserves. In high-valuation periods, management directs excess toward Treasuries rather than marginal equity purchases. This has proven effective, as evidenced by the firm’s ability to sustain record liquidity in 2026 while reporting solid earnings growth of around 18% in operating profits for Q1. The model contrasts with more leveraged peers, offering stability that appeals to long-term shareholders. Practical examples include using float for bolt-on acquisitions in energy and other sectors during favorable windows.

Impact of Market Valuations on Cash Build-Up Patterns

Elevated market valuations have repeatedly prompted Berkshire Hathaway to favor cash accumulation over aggressive equity deployment. In periods like the late 1990s dot-com era and the pre-2008 housing boom, leadership reduced exposure, building reserves that later funded recoveries. Similar dynamics played out from 2023 onward, with the S&P 500 driven by technology gains leading to net selling and cash growth to $397 billion by Q1 2026. Buffett and now Abel assess opportunities based on long-term cash flow potential versus price. When a few businesses meet hurdles, capital shifts to short-term Treasuries. This pattern avoids overpayment, preserving capital for superior future entries. Q1 2026 13F filings showed exits from positions like Visa and Mastercard, further swelling liquidity.

Such restraint carries implications for performance. Berkshire often lags in bull markets but demonstrates resilience in corrections, as seen historically. The current environment, with high multiples, echoes past cautionary phases. Interest on Treasuries offsets some holding costs, making the strategy viable. For investors, this signals a focus on margin of safety rather than momentum. Analysis of past cycles shows cash peaks preceding better entry points, reinforcing the valuation driver. Berkshire’s approach integrates quantitative metrics with qualitative judgment on business quality and management. In 2026, this continues to guide decisions amid AI enthusiasm and economic uncertainties. The result is a portfolio positioned for both defense and offense, reflecting decades of observed market behavior. With equities near highs, this measured stance continues to shape capital allocation. Investors can track parallel Bitcoin price movements for volatility context on KuCoin’s BTC price page.”

Role of Succession in Shaping Current Liquidity Objectives

Greg Abel’s transition to CEO in January 2026 coincided with Berkshire Hathaway maintaining and growing its cash reserves, reflecting deliberate planning for leadership continuity. Buffett, as chairman emeritus, remains influential on investments, but Abel oversees operations with a strong balance sheet emphasizing optionality. The $397 billion position provides Abel with flexibility to pursue deals or weather volatility without immediate pressure. Succession considerations favor a fortress balance sheet, allowing the new leader to act decisively rather than inherit a fully invested portfolio at peak valuations. Abel’s background in energy underscores operational strength, complementing investment caution. Early actions, including modest buybacks resuming in 2026, signal continuity while preserving dry powder.

Historical transitions at Berkshire emphasized cultural preservation, with cash serving as a buffer for adaptation. This setup aligns objectives around long-term compounding. Strong Q1 earnings under Abel highlight business durability, with liquidity supporting strategic moves. Observers note the position exceeds many companies’ market caps, underscoring scale. For shareholders, it represents confidence in disciplined deployment ahead. Practical outcomes include the potential for large acquisitions or increased equity stakes when conditions improve. The strategy mitigates risks associated with leadership change by prioritizing resilience. In a complex 2026 ecosystem, this liquidity supports evaluation of opportunities across sectors without haste.

Treasury Bills and Yield Environment in Cash Management

Berkshire Hathaway allocates a large portion of its reserves to short-term U.S. Treasury bills, which offered attractive yields in the 2023-2026 period. By Q1 2026, roughly $339 billion sat in these instruments, generating meaningful income while maintaining liquidity and safety. This allocation reflects adaptation to higher rate environments, where cash no longer represents a pure drag. Yields around 4-5% enabled billions in annual returns, supporting the decision to hold rather than chase marginal opportunities. This contrasts with post-2008 low-rate challenges. Management views Treasuries as a bridge to better equity or business investments. The approach minimizes credit risk and ensures immediate availability for deployments. Integration with the overall strategy enhances resilience. Insurance float and operating cash flows feed into this pool, creating a virtuous cycle.

Historical data shows shifts toward cash equivalents during cautionary periods, amplified by current yields. For Berkshire, this means earning while waiting, a practical advantage in disciplined capital allocation. In 2026, it positions the firm to respond to potential market shifts without forced sales. The policy aligns with conservative principles, prioritizing preservation alongside returns. Comparisons to peers highlight Berkshire’s unique scale and patience in utilizing such holdings effectively. This allocation shows adaptation to higher rate environments, where cash no longer represents a pure drag. Traders seeking exposure in similar liquid instruments may explore stablecoin trading pairs like BTC-USDT on KuCoin.”

Historical Deployments Following Cash Build-Ups

Berkshire Hathaway has a track record of deploying accumulated cash during market stress for attractive terms. Pre-2008 reserves enabled Goldman Sachs preferred stock investment with warrants, delivering strong returns as markets recovered. Similar patterns emerged in 2011 with Bank of America and later energy positions like Occidental Petroleum. These examples illustrate objectives: capitalizing on dislocations where quality assets trade at discounts. Cash peaks often preceded such windows, validating the buildup phase. In 2020, liquidity supported stability amid pandemic volatility. The current $397 billion reserve follows analogous accumulation, positioning for potential opportunities in a post-peak environment.

Deployments focus on businesses with durable competitive advantages and capable management. Scale requires “needle-moving” targets, limiting options in normal times but amplifying impact during stress. This cycle, accumulation then action, drives long-term outperformance. Under Abel, continuity suggests similar future use. Shareholders benefit from this patience, as evidenced by historical compounding. The strategy avoids permanent capital loss by emphasizing the margin of safety. In practice, it has converted liquidity into ownership of high-quality enterprises at favorable prices. 2026’s environment may test this playbook again.

Comparison of Cash Positions in Different Economic Regimes

Berkshire Hathaway’s cash levels vary meaningfully across economic regimes, from expansionary periods with lower reserves to cautious phases with higher holdings. In the low-rate 2010s, positions were managed tightly due to minimal yields. Post-2022, with inflation and rate hikes, reserves expanded as valuations stretched and yields improved. The 2025-2026 record near $397 billion contrasts with earlier decades but follows the same logic of opportunity cost assessment. During recoveries, deployment accelerates; in frothy markets, accumulation prevails. Insurance and operating businesses provide steady cash regardless, buffering regime shifts.

Q1 2026 data shows resilience, with earnings growth despite net selling. This adaptability stems from decentralized operations and centralized capital decisions. Regime awareness guides objectives toward cycle survival. High cash in elevated markets acts as insurance, while lower levels in bargains facilitate growth. Historical comparisons, such as 2007 versus 2009 actions, demonstrate efficacy. In today’s context, with AI-driven concentrations, the position reflects a measured response. Investors gain insight into risk management across conditions. The approach prioritizes facts over forecasts, maintaining relevance through changing environments.

Operational Cash Flows Supporting Liquidity Build

Berkshire Hathaway’s diverse operating subsidiaries generate robust cash flows that sustain and grow reserves. BNSF railway, utilities, and manufacturing units contribute consistently, with 2025 operating cash flow around $46 billion. Q1 2026 operating earnings rose nearly 18% year-over-year to $11.35 billion, bolstering liquidity. These flows reduce dependence on equity markets for capital needs. Insurance underwriting profits add variability but trend positively under disciplined management. The result is self-funding capacity for reserves without dilutive financing.

This operational strength aligns with strategic objectives by creating reliable dry powder. Historical growth in earnings power supports larger absolute cash targets as the firm scales. In 2026, it enables patience amid external uncertainties. Practical benefits include funding bolt-on acquisitions and maintaining ratings. The model contrasts with acquisition-heavy peers reliant on markets. The operations form the backbone, allowing the investment arm flexibility. Strong free cash flow metrics underscore sustainability.

High cash reserves at Berkshire Hathaway influence shareholder returns through enhanced stability and potential for opportunistic value creation. The position supports conservative leverage and buybacks when shares trade below intrinsic value, as resumed modestly in 2026. It also signals caution, potentially tempering short-term stock enthusiasm but appealing to long-horizon investors. Implications include lower volatility compared to fully invested peers during downturns. However, in strong bull markets, it may contribute to relative underperformance.

Historical returns demonstrate the strategy’s effectiveness over full cycles. For BRK.B holders, liquidity represents embedded optionality. Practical analysis shows cash exceeding many firms’ market caps, highlighting unique scale. Shareholders benefit from alignment with value principles. In a succession context, it provides Abel maneuverability. The approach prioritizes per-share intrinsic value growth over time.

FAQs

How has Berkshire Hathaway’s cash position evolved historically in relation to market conditions?

Berkshire Hathaway has consistently increased cash reserves during periods of high market valuations, as seen in the lead-up to major corrections, allowing for strategic deployments afterward. This pattern continued into 2026 with the record hoard, driven by similar caution.

What role does insurance float play in supporting Berkshire’s liquidity objectives?

Insurance float provides low-cost capital that bolsters cash reserves, enabling the company to maintain high liquidity while generating underwriting profits, as demonstrated in recent quarterly results under new leadership.

Why does Berkshire prefer short-term Treasury bills for much of its cash holdings?

Short-term Treasury bills offer safety, liquidity, and attractive yields in the current environment, allowing Berkshire to earn returns on reserves while preserving flexibility for future investments without credit risk.

How might Greg Abel’s leadership influence future cash deployment decisions?

Greg Abel is expected to maintain Buffett’s disciplined approach, using the substantial reserves for high-quality opportunities when valuations align, supported by strong operational cash flows from core businesses.

What are the main challenges associated with managing such large cash positions?

Challenges include finding sufficiently large, attractive investments and managing opportunity costs, though higher yields and operational strength help mitigate these in Berkshire’s case.

Can individual investors learn from Berkshire’s cash management strategy?

Individual investors can adopt principles of patience and valuation focus, maintaining liquidity for opportunities while avoiding overcommitment in elevated markets, much like Berkshire’s historical practice.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. Cryptocurrency investments carry risk. Please do your own research (DYOR).