KuCoin Ventures Weekly Report: Super Apps and Stablecoins Reshape the Public Chain Settlement Narrative Amidst Dual Pressures from Macro Interest Rates and Geopolitical Risks

2026/05/18 09:36:02

1. Weekly Market Highlights

Infrastructure Power Shift: Super Apps Building Native Chains May Challenge Core Public Chain Narratives

Last week, the main theme of the crypto market focused on the evolution of underlying infrastructure and the establishment of dominance by compliant stablecoins in core liquidity pools. Stablecoin giants expanding to Layer 1 (L1),coupled with top-tier decentralized derivative protocols completing their asset system alignment, collectively reflect that the rules for on-chain liquidity distribution are undergoing profound changes.

Event Recap: Circle Arc's Massive Financing and Hyperliquid's Settlement Asset Transition

-

Circle Arc Completes Massive Financing, Moving Towards Underlying Infrastructure

Around May 11, USDC issuer Circle completed a $222 million pre-sale financing for its new L1 blockchain, Arc. The round was led by a16z, with participation from traditional Wall Street institutions including BlackRock, Apollo, and ICE. This move indicates that stablecoin issuers are shifting from cross-chain asset distribution to building fully autonomous settlement infrastructure.

Data Source: https://www.circle.com/blog/circle-expands-support-for-usdc-on-hyperliquid

-

Hyperliquid's Asset Landscape Restructuring: USDC Establishes a Core Position

The liquidity structure of the decentralized trading platform Hyperliquid has undergone a major adjustment. Coinbase and Circle announced the acquisition of the "USDH brand assets" deployed by Native Markets. The Hyperliquid platform is gradually pivoting away from its original native stablecoin (USDH) route, turning to establish the compliant stablecoin USDC as the sole underlying settlement asset for its native spot and derivatives markets.

The self-built L1s by stablecoin giants and the compliance of underlying assets in super apps are impacting the narratives of general-purpose public chains, such as ETH and SOL, as well as the capital structure of the DeFi sector.

For a long time, the core valuation of general-purpose public chains has relied on their economic security premium as the "settlement layer of the global on-chain financial system." However, when super apps with real, high-frequency users and massive accumulated funds—such as Circle (Arc) and Polymarket—choose to build their own native chains and establish dedicated L1s, the Gas consumption, MEV value, and clearing revenues that would have remained on general-purpose public chains will be captured by the application chains themselves. This could potentially dilute the value capture capabilities of traditional public chains to a certain extent.

The launch of Circle Arc also indicates that stablecoin issuers are beginning to seek deep vertical integration of "asset issuance," "on-chain clearing and settlement," and "application scenarios." By building their own underlying layers, Circle can achieve lower-cost compliance audits and programmable payments, while potentially bypassing the performance limitations of existing public chains to directly provide customized commercial settlement services to traditional financial institutions.

Furthermore, the deep participation of traditional institutions like BlackRock and Apollo in the Arc financing suggests that Wall Street's perspective may have shifted from simply "purchasing crypto assets" or "providing crypto asset management/OTC services" to "participating in the rule-making of on-chain financial infrastructure." The establishment of compliant stablecoin chains lowers the legal and technical barriers for traditional capital to enter the DeFi sector, and the RWA sector could potentially usher in a new round of compliant expansion.

From Polymarket to Circle, the trend of super apps building their own infrastructure indicates that in the current market cycle, real commercial use cases and traffic may carry more weight than pure technical superiority.

-

Scenarios Determine Liquidity Destination: Future stablecoin competition may no longer be limited solely to the scale of issuance, but could extend to the exclusive control over core high-frequency application scenarios (such as prediction markets, derivative DEXs, and cross-border settlements).

-

Complexity of the Multi-Chain Compliance Landscape: On the legal and regulatory policy front, the struggle for settlement rights between traditional financial capital and offshore native crypto forces may become more subtle. Objectively speaking, with the deployment of more compliant application chains, balancing compliance and regulatory requirements with the permissionless nature of decentralized protocols could become a systemic issue that the entire industry needs to collectively address in the next phase.

Under this paradigm shift, the valuation logic for next-generation L1s may need to pivot from "how many developers can be attracted" to "how many commercial scenarios it can inherently bring." The era of infrastructure serving applications is perhaps accelerating its arrival.

2. Weekly Selected Market Signals

Oil and Rate Shocks Weigh on Risk Appetite, AI Earnings Support Remains Intact, ETF Flows Weaken While the Stablecoin Base Continues to Expand

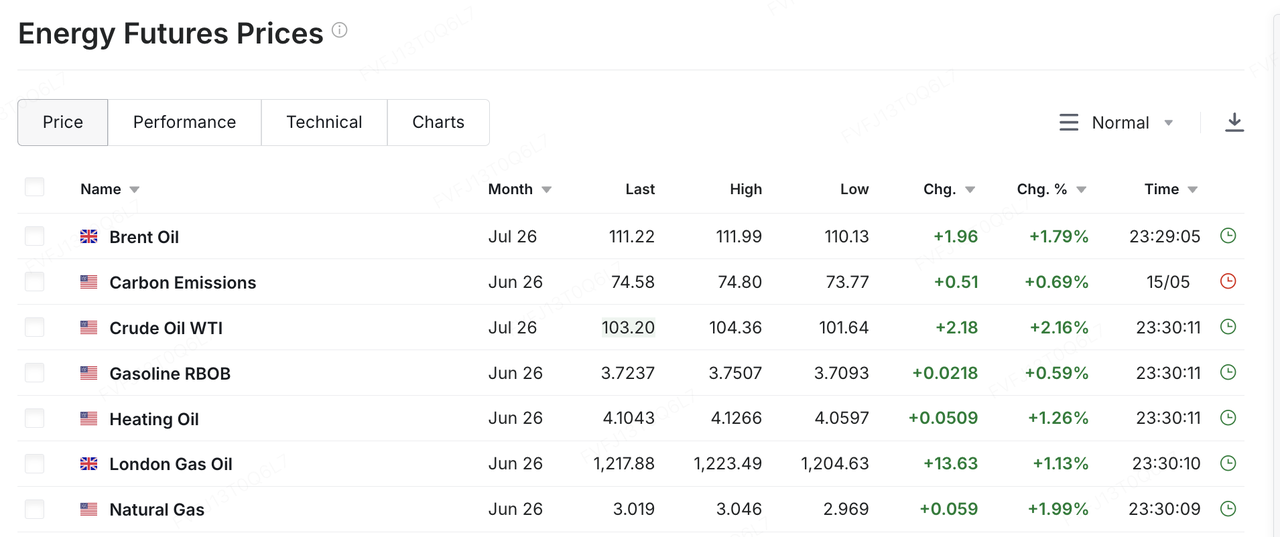

Last week, the key variable for global markets was the renewed escalation in U.S.–Iran tensions, which brought oil prices and inflation expectations back to the center of risk-asset pricing. Israeli Prime Minister Benjamin Netanyahu and President Trump reportedly discussed the possibility of restarting military action against Iran. Trump later warned that Iran was “running out of time” and should act quickly, or it would be left with “nothing.” Against the backdrop of limited negotiation progress and rising risk of potential military conflict, markets began to reprice the risk of disruptions to Middle East energy supply. WTI crude rose by more than 10% last week to around USD 105 per barrel, while Brent crude also moved above USD 110 per barrel. The rise in oil prices is not merely a commodity price move; it feeds into inflation expectations, long-term Treasury yields, and risk premiums, thereby compressing the valuation space for equities, cryptocurrencies, and other risk assets.

Data Source: https://www.investing.com/commodities/energy

U.S. macro data reinforced this pressure. April inflation data came in above market expectations, and higher energy prices made the path of disinflation more uncertain. At the same time, U.S. consumption and corporate earnings have not yet shown clear signs of losing momentum, meaning the Federal Reserve still lacks sufficient justification for a rapid rate-cut cycle. As a result, markets are facing an uncomfortable combination: the economy remains resilient, inflation pressure is rising again, and rate-cut expectations continue to be pushed back. Against this backdrop, long-term U.S. yields moved sharply higher, with the 30-year Treasury yield rising to around 5.1% and the 10-year yield moving above the 4.5% range. For high-valuation assets, this means the previous dual support of “earnings resilience + rate-cut expectations” is being replaced by a new environment of “earnings remain strong, but rates are higher.”

U.S. equities did not weaken across the board on a weekly basis, but structural cracks have become more visible. On a weekly basis, the S&P 500 still closed slightly higher and extended its winning streak to seven consecutive weeks, while the Nasdaq and Dow hovered near flat or edged slightly lower. Small caps, represented by the Russell 2000, came under more visible pressure. In terms of intra-week performance, major indices once reached fresh highs, but fell noticeably last Friday under the combined pressure of higher oil prices and rising Treasury yields. Technology stocks, especially AI-related names that had rallied strongly earlier, became the main focus of the pullback. In other words, U.S. equities have not entered a trend reversal, but the high-level rally is shifting from a broad risk-appetite recovery to a more selective phase based on earnings quality and valuation resilience. This week, NVIDIA’s earnings report, together with quarterly results from major U.S. retailers such as Walmart, Home Depot, and Target, will be closely watched. Markets will be testing both whether AI capex can continue to translate into revenue and profit, and whether high oil prices and sticky inflation are beginning to erode U.S. consumer spending.

Asia-Pacific markets were also affected by oil prices, the U.S. dollar, and foreign capital flows, but internal divergence became more pronounced. Most Asia-Pacific markets remained under pressure amid higher oil prices and weaker global risk appetite. South Korea, however, offered a more representative case of both “AI supply chain benefits” and “profit-taking at elevated levels.” The KOSPI briefly broke above 8,000 last week, supported mainly by semiconductor and AI supply chain stocks such as Samsung Electronics and SK Hynix. It later pulled back as foreign investors sold shares, technology heavyweights weakened, and Middle East risks intensified, falling 6.12% on Friday to 7,493.18. This suggests that global AI-related trades are already priced at elevated levels. Once macro rates or geopolitical risks deteriorate, previously strong sectors can also become targets for profit-taking.

In crypto markets, BTC returned last week to trading within the macro rates and ETF flow framework. At the beginning of last week, BTC was still holding above USD 80,000, but as oil prices, inflation, and long-term Treasury yields moved higher, it pulled back to around USD 77,000 by the weekend, down roughly 6% for the week. ETH was weaker, falling back to the USD 2,100–2,200 range. BTC remains the crypto asset with the strongest institutional allocation profile, but when ETF flows shift from consistent inflows to volatility, and rate-cut expectations are further compressed, BTC becomes more sensitive to macro data. ETH, meanwhile, has relatively less independent support amid weaker spot ETF flows and a lack of new ecosystem catalysts.

Data Source: TradingView

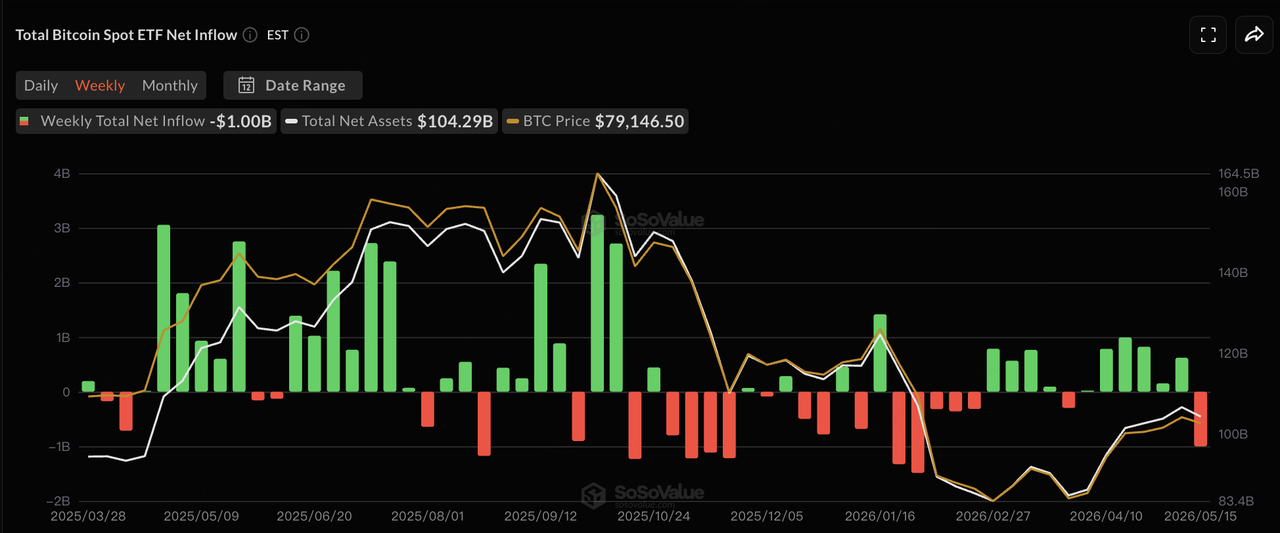

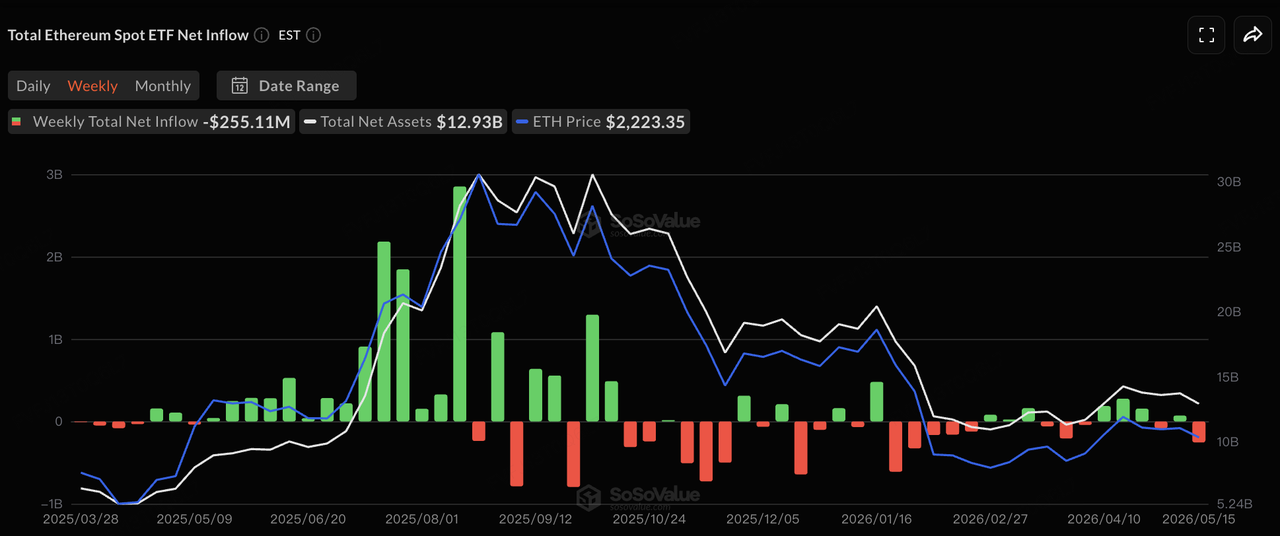

In terms of ETF flows, according to SoSoValue data, U.S. spot BTC ETF flows shifted from previous consecutive inflows to more visible volatility last week. On May 12, spot BTC ETFs recorded a single-day net outflow of around USD 233 million, while spot ETH ETFs saw net outflows of around USD 131 million. On May 14, BTC ETFs briefly returned to net inflows of around USD 131 million, while ETH ETFs still posted a small outflow. On May 15, spot BTC ETFs again recorded net outflows of around USD 290 million, with none of the 12 BTC ETFs posting net inflows that day. Spot ETH ETFs also recorded their fifth consecutive day of net outflows, at around USD 65.65 million. Overall, ETFs remain the core institutional gateway for BTC, but their marginal state has shifted from “continuously absorbing selling pressure” to being highly sensitive to macro shocks. In the short term, whether BTC can stabilize again will depend on whether ETF buying can regain consistency, and whether oil prices and long-term yields can retreat from elevated levels.

Data Source: SoSoValue

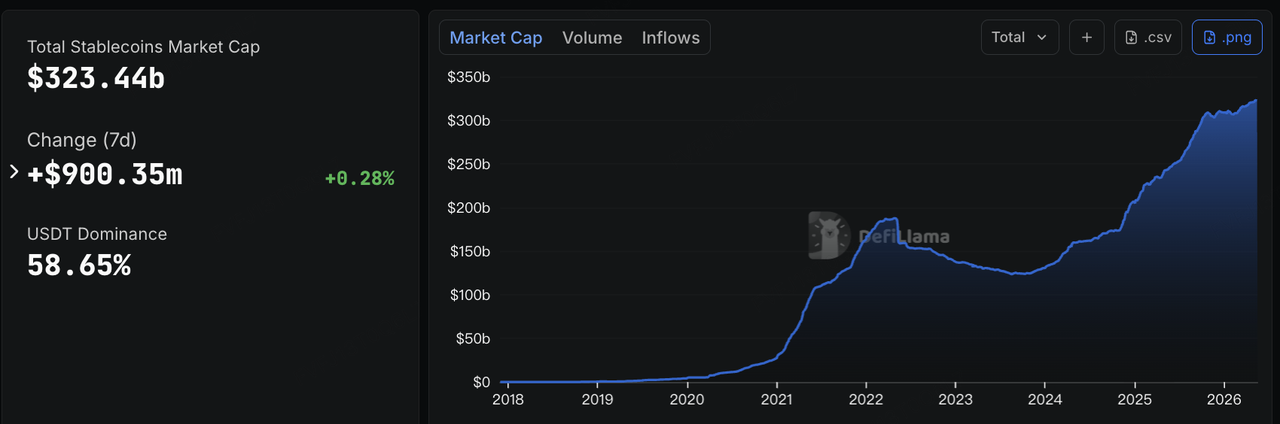

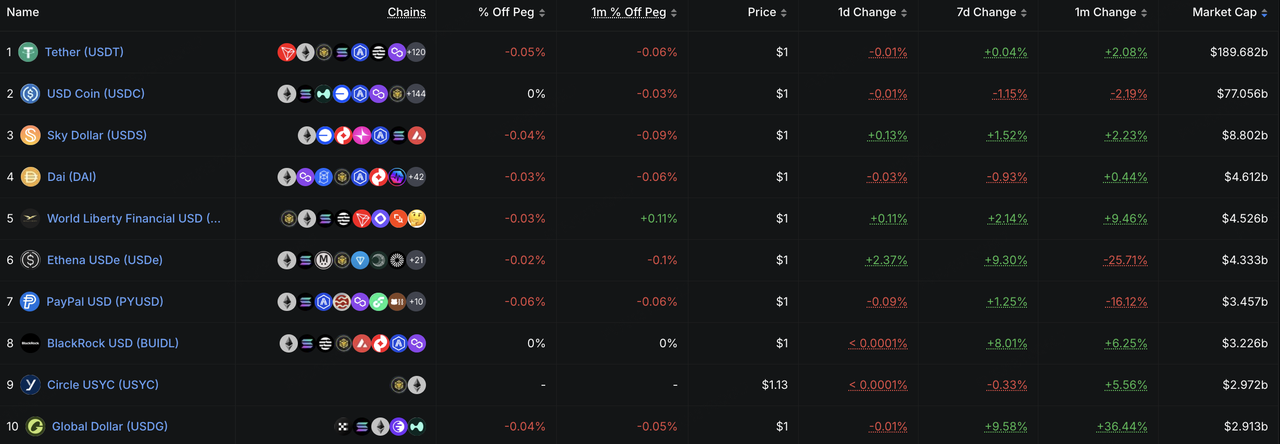

On stablecoins, DeFiLlama data shows that as of May 18, total stablecoin market capitalization stood at around USD 323.4 billion, up approximately USD 900 million over the past seven days, or about 0.28%. This suggests that the on-chain dollar liquidity base is still expanding modestly. Structurally, the growth of USDe, USDG, and BUIDL is particularly worth noting. USDe grew by around 9.3% over seven days, indicating that yield-bearing stablecoins can still attract capital seeking on-chain returns in a volatile environment. USDG grew by around 9.6%, reflecting the channel expansion of compliance-oriented stablecoins through exchanges, wallets, and payment partner networks, though its true usage stickiness still needs to be assessed through trading volume, transfer activity, and application retention. BUIDL grew by around 8.0%, reflecting continued institutional demand for on-chain cash management, tokenized money market funds, and yield-bearing dollar assets that can potentially be used as collateral. In other words, pressure on risk-asset prices does not necessarily mean on-chain dollar liquidity is leaving. Rather, capital is being reallocated from high-beta exposure toward yield management, cash management, and compliant on-chain dollar instruments.

Data Source: DeFiLlama

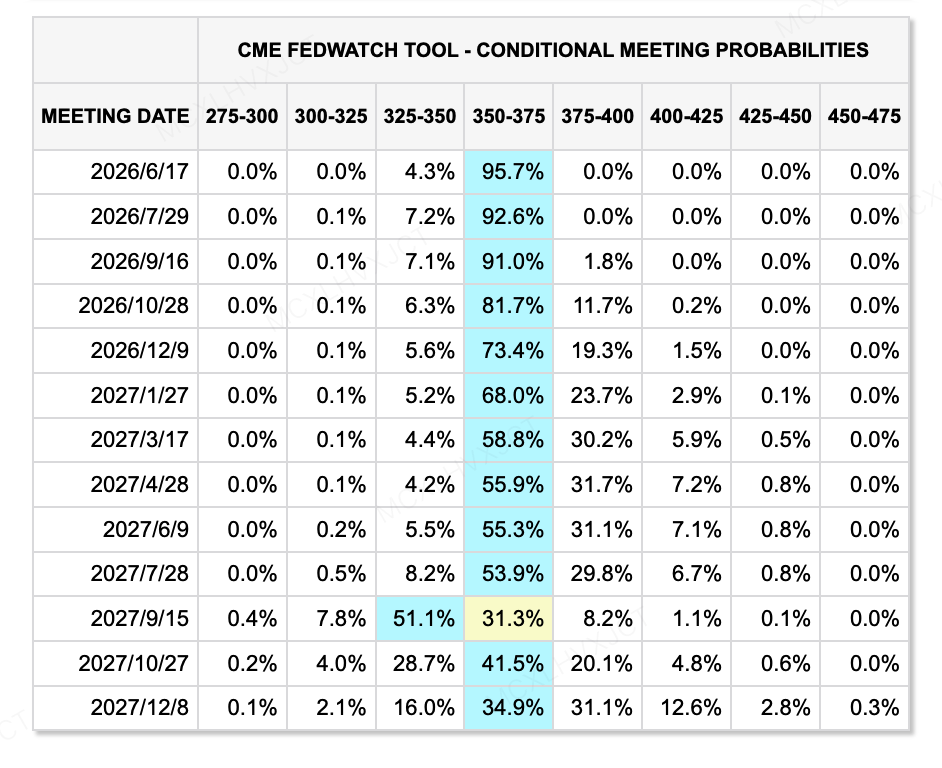

On rate expectations, as of May 18, the CME FedWatch Tool showed that the market has almost fully priced out the possibility of a June rate cut, while expectations for monetary easing this year have also cooled significantly. At the same time, Kevin Warsh was confirmed by the Senate as the new Fed Chair by a narrow 54:45 margin, marking one of the narrowest confirmation votes in Fed Chair history. Warsh is generally seen as more aligned with the Trump administration’s preference for rate cuts, but his past views also carry a more inflation-hawkish tone, and he has previously emphasized balance-sheet reduction and the importance of maintaining inflation credibility. Therefore, whether Warsh will truly follow Trump’s preference for rate cuts remains uncertain. For markets, the question is not simply whether rates will be cut. Even if short-term rates decline, if inflation, balance-sheet reduction, and long-term yield pressures remain in place, liquidity conditions may not quickly shift into broad easing.

Data Source: CME FedWatch Tool

Major Events to Watch This Week:

-

AI earnings validation: NVIDIA’s earnings, Google I/O, and related AI supply chain updates will determine whether technology stocks can continue to digest high valuations through revenue growth and profit delivery.

-

U.S. consumption and macro data: Earnings from major retailers, FOMC meeting minutes, PMI data, housing data, and consumer confidence readings will help markets assess whether high oil prices and high inflation are beginning to affect consumer spending and corporate profits.

-

Geopolitics and Asian macro events: Putin’s visit to China, China’s April industrial production, consumption and real estate data, and further developments in the Middle East may continue to affect oil prices, inflation expectations, and risk appetite. If geopolitical risks ease, risk assets may see a short-term recovery window. If oil prices remain elevated, concerns over inflation and rates are likely to persist.

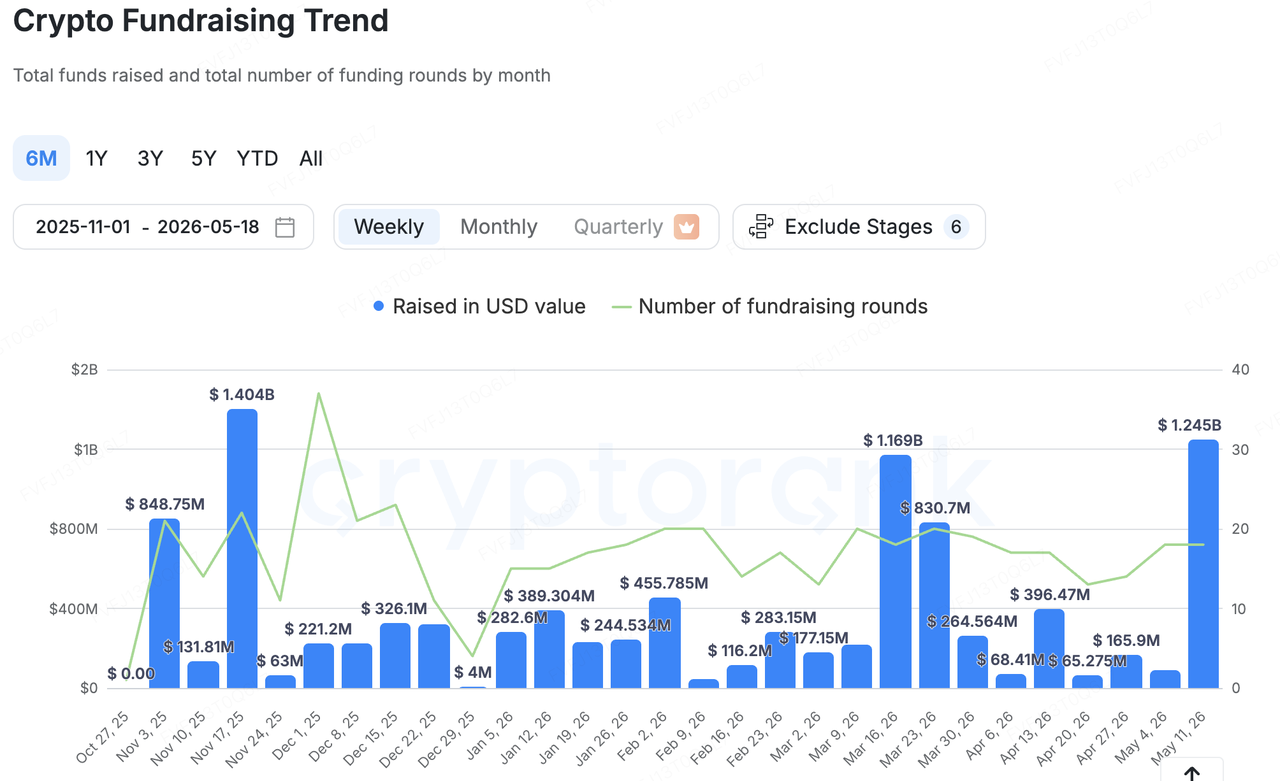

Primary Market Investment Observations:

Data Source: CryptoRank

Based on CryptoRank’s broad statistical coverage, total crypto primary-market fundraising increased significantly last week compared with the prior period, but capital distribution remained highly concentrated. The increase was mainly driven by a small number of large deals and institutional infrastructure financings. Therefore, the larger headline fundraising figure should not be interpreted simply as a broad recovery in primary-market risk appetite. A more accurate reading is that capital continues to concentrate in compliance, security, stablecoin financial infrastructure, wallet and key management, and institutional services.

Among representative deals, the most notable case last week was Elliptic, an on-chain compliance and risk analytics company, which completed a USD 120 million Series D round at a post-money valuation of around USD 670 million. Investors included One Peak, Nasdaq Ventures, Deutsche Bank, and the British Business Bank. This type of financing reflects continued demand from banks, payment companies, government agencies, and large crypto firms for on-chain risk control, transaction monitoring, sanctions compliance, and AI-native compliance tools. Unlike the previous cycle, when more capital flowed into applications and high-beta narratives, large financings today are increasingly directed toward the fundamental compliance capabilities required for institutions to enter the crypto market.

Stablecoin and payment infrastructure remained another key theme, indicating rising primary-market attention on how on-chain dollars can enter payment, savings, cash management, and trading collateral scenarios:

-

Digital asset platform Fasset completed a USD 51 million Series B round to expand its stablecoin-powered platform for payments, lending, and cross-border transfers.

-

Osero completed a USD 13.5 million financing round, positioning itself as an institutional-grade stablecoin savings platform based on the Sky Savings Rate.

-

Wallet and key management infrastructure provider Turnkey received USD 12.5 million in strategic financing, showing that capital continues to be allocated to account abstraction, custody, signing, security, and institutional-grade wallet infrastructure.

Overall, primary-market capital is not clearly chasing high-beta narratives. Instead, it continues to flow into underlying infrastructure that institutions can use, regulators can understand, and business models can more clearly monetize. Against a backdrop where secondary markets are pressured by macro factors and ETF flows have become more volatile, primary-market risk appetite has also become more defensive and practical.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.