Why does US debt matter to ordinary people who do not follow fiscal policy closely?

2026/04/24 07:15:02

Introduction

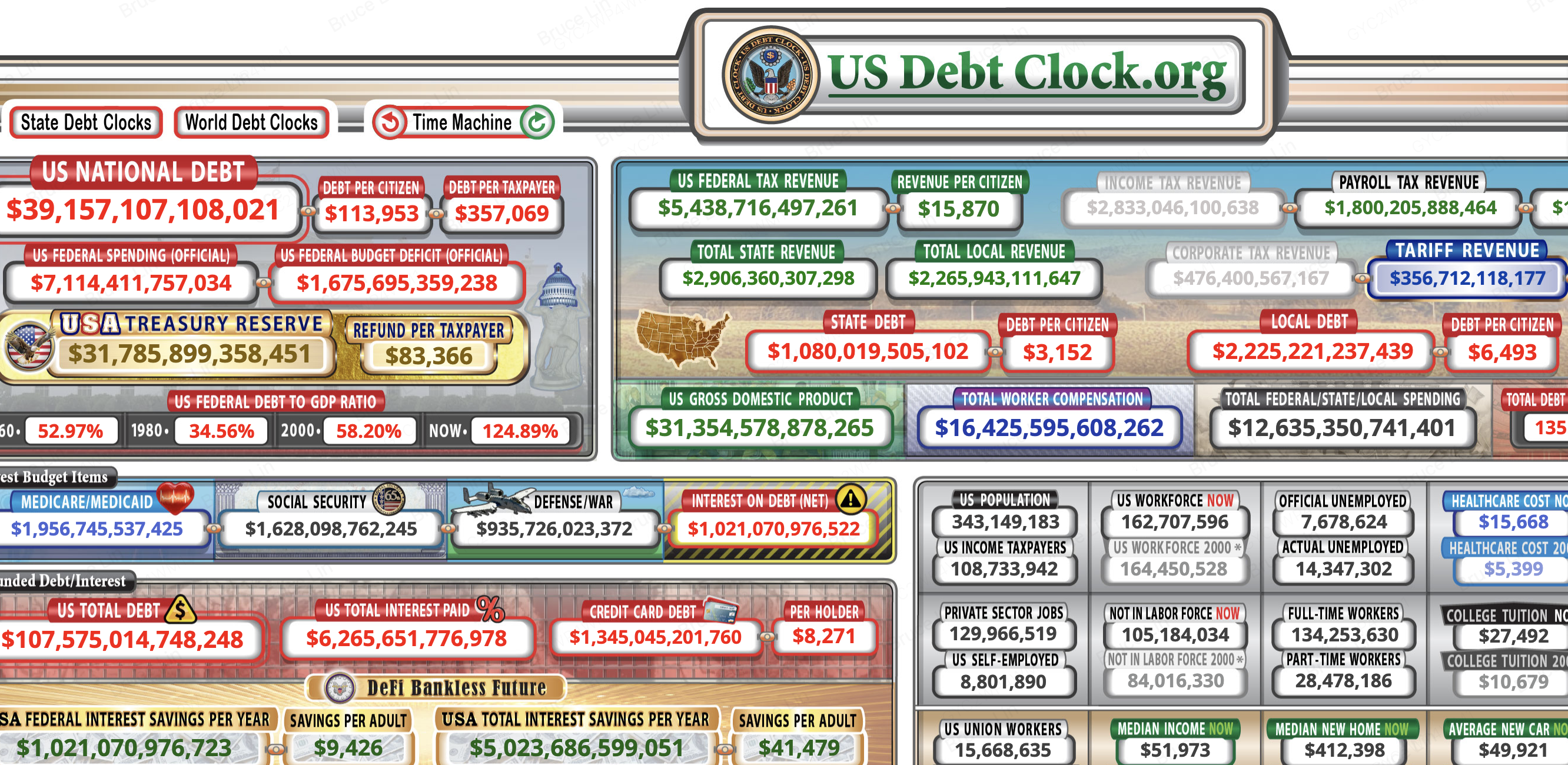

Did you know that every person living in the United States currently owes more than $113,000 in federal debt? Rising US debt directly erodes purchasing power, raises the cost of borrowing, and threatens the social services millions rely on — even if you have never watched a congressional budget hearing. The national debt has surpassed $39.14 trillion, based on USDebtClock.org data, with each taxpayer shouldering approximately $357,000. These figures are not abstract accounting entries. They translate into higher prices at the grocery store, steeper mortgage rates, and reduced Medicare and Social Security benefits in the years ahead.

Understanding this connection matters because it affects where you keep your savings, how you plan for retirement, and what assets can preserve value when fiscal pressure mounts.

For readers seeking deeper context:

-

Record $40 Trillion US Debt examines how sovereign borrowing expansion is altering cryptocurrency market dynamics in 2026,

-

while Tokenized Treasuries explains how to earn government bond yields through blockchain-based instruments on KuCoin.

The Debt Is Already in Your Wallet

Every dollar of the $39.14 trillion national debt weakens purchasing power and pushes consumer prices higher, meaning your salary buys less even when the number on your paycheck stays the same. When the federal government runs a deficit — currently $1.68 trillion per year based on USDebtClock figures — it funds the shortfall by issuing Treasury securities. Those securities are purchased by banks, institutional investors, and the Federal Reserve. When the Fed buys Treasuries, it effectively creates new money to do so. That monetary expansion dilutes the value of every dollar already in circulation.

The result is the inflation ordinary Americans experience at gas pumps, grocery stores, and rental offices. You do not need to follow bond auctions or budget projections to feel the impact. When the money supply expands faster than the production of goods and services, prices rise. That is precisely what has happened as the debt has climbed past $39 trillion. Your savings account loses real value even if the nominal balance never drops. A dollar held in a standard checking account five years ago purchases significantly less today, not because the account changed, but because the debt-fueled expansion of the monetary base changed the value of the dollar itself.

| Metric | Current Figure |

| US National Debt | $39.14 trillion |

| Debt per Citizen | $113,906 |

| Debt per Taxpayer | $357,069 |

| Federal Budget Deficit | $1.68 trillion |

| Interest on Debt (Net) | $1.63 trillion |

| Debt-to-GDP Ratio | 124.88% |

| Total Debt Including Unfunded Liabilities | $107.50 trillion |

| Total Debt per Citizen | $313,074 |

How $39 Trillion Translates to Everyday Prices

The federal government funds its deficit spending by issuing Treasury bonds, which expands the money supply and dilutes the value of existing dollars. According to USDebtClock, federal spending now exceeds $7.11 trillion annually while revenue falls short, forcing the Treasury to borrow the difference. That borrowing does not happen in a vacuum. It injects liquidity into financial markets that eventually flows into the broader economy.

When more dollars chase the same quantity of food, housing, and energy, prices adjust upward. This dynamic explains why periods of rapid debt accumulation often coincide with higher inflation rates. Ordinary workers feel the squeeze most acutely because wage growth typically lags behind price increases. The debt-financed spending that politicians promise as stimulus becomes a long-term drag on household budgets.

The Hidden Tax You Did Not Vote For

Inflation acts as a regressive tax that hits low and middle-income households hardest because they spend a larger share of income on non-discretionary goods. Wealthier households can shift assets into stocks, real estate, or alternative investments that historically outpace inflation. Working families, however, keep most of their wealth in cash or low-yield savings accounts.

Based on USDebtClock data, the debt per citizen now stands at $113,906. That obligation will never be collected as a lump sum. Instead, it is collected gradually through the steady erosion of purchasing power. Every time you notice that your grocery bill is higher than it was last year, you are paying a portion of that debt. The mechanism is invisible, but the cost is real.

If you are a US taxpayer, your personal share of the federal debt is approximately $357,000, based on current USDebtClock figures. That number represents the total outstanding debt divided by the roughly 163 million Americans who actually pay federal income taxes. It is a staggering sum that exceeds the median home price in most states. Yet most taxpayers remain unaware of the liability because it never appears on a bank statement or tax bill.

The debt is not evenly distributed across the population. It concentrates on the minority of citizens who generate taxable income. As the population ages and the workforce shrinks relative to retirees, the burden on each remaining taxpayer will grow heavier unless dramatic fiscal reforms occur. This is not a theoretical projection. The USDebtClock population tracker shows roughly 343 million Americans against 162 million income taxpayers, a gap that illustrates how narrowly the fiscal burden is concentrated.

Why Taxpayers Carry the Heaviest Load

Only about 162 million Americans pay federal income taxes, which means the debt burden concentrates on a shrinking pool of productive workers rather than spreading evenly across the entire population. USDebtClock shows the US population at roughly 343 million, meaning less than half the country shoulders the entire federal debt obligation through current and future taxation.

This concentration creates a fiscal tension that will intensify over the coming decade. As more Baby Boomers retire and draw Social Security and Medicare, the ratio of workers to beneficiaries declines. Each worker’s implicit debt burden rises automatically even if Congress freezes all new spending. The $357,000 figure is not static. It grows every second the clock ticks.

Unfunded Liabilities and Future Generations

When unfunded liabilities are included, total debt obligations exceed $107 trillion, pushing the per-citizen burden to over $313,000 and threatening the solvency of programs young workers are paying into today. USDebtClock tracks these broader obligations, which include promised Social Security and Medicare benefits that lack dedicated funding.

Younger generations face a double penalty. They will pay payroll taxes throughout their careers to fund current retirees, yet the trust funds are projected to face shortfalls that could reduce the benefits they themselves receive. The $107 trillion figure is not speculative accounting. It represents legally promised payments that the government has no current plan to fully fund. For a twenty-five-year-old entering the workforce today, this means paying into a system that may return far less than previous generations collected.

Interest Payments Are Crowding Out Public Services

The United States now spends over $1.6 trillion annually on net interest alone, a sum that rivals the entire federal discretionary budget and leaves less room for infrastructure, education, and healthcare. Based on USDebtClock, interest on the debt has become one of the largest budget items, competing directly with defense, Medicare, and Medicaid for limited revenue.

This crowding-out effect has real consequences for ordinary people. When interest costs consume a larger slice of the federal pie, Congress has less flexibility to respond to emergencies, invest in roads and bridges, or expand healthcare access. The money that could build schools or fund research instead flows to bondholders. In fiscal year terms, the $1.63 trillion interest bill means that the first several months of all tax revenue collected simply service old debt rather than funding current priorities.

What Gets Cut When Interest Costs Rise

As interest consumes a larger share of federal revenue, Congress faces pressure to reduce spending on Medicare, Social Security, and defense — programs that ordinary Americans rely on daily. Politicians rarely cut benefits explicitly. Instead, they allow inflation to erode the real value of payments, raise eligibility ages, or reduce provider reimbursements.

The result is longer wait times for medical care, smaller cost-of-living adjustments for retirees, and deteriorating public infrastructure. These are not abstract policy debates. They manifest as potholed roads, overcrowded emergency rooms, and seniors struggling to afford prescriptions. When the interest bill reaches $1.6 trillion, something has to be given. Ordinary citizens ultimately bear that sacrifice.

The Debt-to-GDP Ratio Signals Long-Term Instability

The federal debt-to-GDP ratio has climbed to 124.88%, a level that economists historically associate with slower growth, higher borrowing costs, and reduced fiscal flexibility during recessions. According to USDebtClock, US gross domestic product stands at approximately $31.34 trillion. When debt exceeds the total annual output of the economy, servicing that debt becomes progressively harder.

High debt-to-GDP ratios create a vicious cycle. Slow growth reduces tax revenue, which widens deficits, which requires more borrowing, which further slows growth. Countries that cross the 100% threshold often experience prolonged periods of stagnation. For ordinary workers, that means fewer job opportunities, smaller raises, and greater economic insecurity.

Why This Metric Predicts Your Economic Future

When debt grows faster than the economy, the government must borrow ever-larger amounts just to pay old interest, creating a feedback loop that raises mortgage rates, credit card APRs, and business lending costs. The 124.88% ratio recorded by USDebtClock indicates that debt accumulation has outpaced economic expansion.

Lenders notice. As sovereign risk rises, they demand higher yields on Treasury bonds. Those yields serve as the benchmark for virtually every other interest rate in the economy. When Treasury rates climb, mortgage rates follow. So do auto loans, student loans, and small business credit lines. The debt that Washington accumulates today becomes the higher monthly payment you face tomorrow. A family shopping for a home will qualify for less house at the same income level because the debt load has pushed benchmark rates upward.

How Fiscal Pressure Is Reshaping Personal Finance

As traditional savings lose value to inflation and government bonds offer yields that barely keep pace, ordinary investors are increasingly exploring alternative stores of value, including cryptocurrencies and tokenized real-world assets. The $39 trillion debt pile is not merely a political problem. It is a signal that conventional fiat-denominated savings strategies may be insufficient to preserve wealth over long time horizons.

When the purchasing power of the dollar declines steadily, holding cash becomes a losing proposition. This reality is pushing mainstream investors toward assets with fixed or algorithmically capped supplies, as well as toward yield-bearing instruments that can be accessed without traditional brokerage accounts.

Diversifying Beyond Traditional Savings Accounts

With the national debt expanding by roughly $1.68 trillion per year in deficit spending alone, keeping wealth exclusively in fiat currency exposes savers to steady erosion. USDebtClock illustrates the scale of this expansion in real time. Investors who recognize the pattern are reallocating a portion of their portfolios into assets that operate outside direct government monetary policy.

Cryptocurrencies like Bitcoin offer supply caps that cannot be altered by central banks. Tokenized Treasuries offer a different advantage: they allow investors to capture government bond yields while maintaining the liquidity and accessibility of digital assets. Both approaches represent pragmatic responses to a fiscal environment where debt monetization has become the default policy tool. Rather than accepting gradual impoverishment through inflation, investors can use these tools to build resilience.

Should You Explore Crypto and Tokenized Treasuries on KuCoin?

KuCoin offers tools that let ordinary investors respond to fiscal uncertainty by accessing both cryptocurrency markets and tokenized Treasury products that mirror traditional government bond yields. As US debt approaches $40 trillion, diversification is no longer a strategy reserved for institutional portfolio managers. It is a necessity for anyone seeking to protect purchasing power.

On KuCoin, users can trade major cryptocurrencies that historically have served as hedges against currency debasement. The platform also supports tokenized Treasury products that allow investors to earn yield from government bonds without navigating traditional brokerage infrastructure. These instruments combine the stability of US Treasury backing with the efficiency of blockchain settlement.

Opening an account takes minutes. New users can register at KuCoin and Get Up to 11,000 USDT in New User Rewards. Once registered, users can deposit funds, explore trading pairs, and allocate capital across digital assets and tokenized fixed-income products. The platform provides security features and user-friendly interfaces that make these instruments accessible even to those who are new to digital finance.

Conclusion

The US national debt is not a distant concern confined to Washington policy debates. It is a force that shapes the prices you pay, the interest rates you face, and the benefits you can expect in retirement. With the debt exceeding $39.14 trillion, each citizen effectively owes over $113,000, while each taxpayer faces a burden near $357,000. Interest costs have surpassed $1.6 trillion annually, crowding out spending on services that ordinary Americans depend upon. The debt-to-GDP ratio at 124.88% signals that borrowing has outrun economic growth, setting the stage for higher borrowing costs and slower wage growth. Meanwhile, total obligations including unfunded liabilities exceed $107 trillion, suggesting the official debt figure understates the true challenge.

These trends do not require you to become a fiscal policy expert. They require you to recognize that traditional savings and fixed-income strategies may be insufficient in a high-debt environment. By understanding the mechanisms through which debt infiltrates daily life, you can make informed decisions about where to hold your wealth. Platforms like KuCoin provide access to both cryptocurrency markets and tokenized Treasury yields, offering tools to navigate an era of unprecedented sovereign borrowing.

FAQs

How does the national debt affect my personal finances directly?

It erodes your purchasing power through inflation, raises the interest rates you pay on mortgages and loans, and threatens the future solvency of Social Security and Medicare. Based on USDebtClock, the $39.14 trillion debt translates to roughly $113,906 per citizen, which acts as a hidden tax on everything you buy.

Will the US debt cause my taxes to go up?

Yes, either through explicit tax increases or through the implicit tax of inflation. As the debt per taxpayer approaches $357,000, future Congresses will face intense pressure to raise revenue. If they avoid direct tax hikes, the Federal Reserve may monetize the debt, which produces the same result through higher prices.

What happens if the US debt keeps growing forever?

It cannot grow forever without severe consequences. Eventually, interest costs would consume the entire federal budget, forcing drastic cuts to entitlements and defense or triggering a currency crisis. The current trajectory, with interest exceeding $1.6 trillion annually, suggests that breaking point is closer than most politicians acknowledge.

How does US debt impact mortgage and loan rates?

Treasury yields serve as the benchmark for consumer lending rates. As debt rises and lenders demand higher yields to compensate for risk, mortgage rates, auto loans, and credit card APRs climb in tandem. The 124.88% debt-to-GDP ratio indicates that this pressure on rates is structural, not temporary.

Can I protect my savings from the effects of rising national debt?

You can mitigate the impact by diversifying into assets that are not tied directly to fiat currency depreciation. Cryptocurrencies with supply caps and tokenized Treasury products available on platforms like KuCoin offer alternative paths. These instruments allow you to move beyond cash savings and capture yields that may better withstand inflationary pressure.