KuCoin Ventures Weekly Report: Stablecoin Sector Faces Dual Shifts in Infrastructure and Yield Rules; Cooling Job Market Eases Rate Hike Concerns

2026/07/07 11:18:00

1. Weekly Market Highlights

Open Standard Launches OUSD; The Stablecoin Yield Distribution Landscape May Be Reconstructed

This week, the launch of the new USD-pegged stablecoin Open USD (OUSD), spearheaded by Open Standard, has become a core event in the stablecoin market. The focus of this project lies not only in its congregation of payment infrastructures such as Stripe and Bridge, alongside multiple traditional finance and tech companies, but also in its announcement to achieve day-one native issuance on Tempo, a payment-first Layer 1 blockchain co-incubated by Stripe and Paradigm.

Compared to traditional stablecoin issuers that emphasize issuance scale and reserve yield, OUSD attempts to reconstruct the profit distribution mechanism of stablecoins from the foundational level. By leveraging a dedicated on-chain infrastructure, it aims to address the long-standing implementation bottlenecks faced by stablecoins in real-world payment scenarios. Meanwhile, the controversy surrounding the partnership list involving South Korean enterprises during the project's early promotion also exposes the complexities of consortium-type stablecoins in commercial expansion and governance coordination.

Based on currently public information, Stripe has decomposed stablecoin-related capabilities into several key modules: Stripe itself is responsible for merchant payments and the global acquiring gateway; Bridge handles stablecoin issuance, exchange, orchestration, and cross-border flow; Privy manages wallets, accounts, key management, and the user-side asset experience; OUSD assumes the role of the currency layer; and Tempo further extends Stripe's layout to the on-chain settlement layer.

Based on market information, the core advantages of Open Standard / OUSD can be understood from the following aspects:

-

From Yield Monopoly to Reserve Yield Sharing: Traditionally, the core profit source for compliant stablecoin issuers is the interest generated by reserves (such as U.S. Treasuries, cash, etc.), with the vast majority of profits captured unilaterally by the issuer or shared among a select few channel partners (e.g., Circle and Coinbase). OUSD introduces a more broadly applicable profit distribution mechanism. After deducting necessary management fees, OUSD plans to return the yield generated by the reserves to ecosystem participants—namely, the enterprises that drive the adoption, distribution, and integration of OUSD into practical application scenarios (such as wallets, exchanges, payment gateways, and dApps).

-

Zero-Friction Large-Scale Circulation: OUSD promises zero fees during large-scale minting and redemption processes, with no transaction limits, thereby eliminating friction costs for institution-grade capital inflows and outflows.

-

Stablecoin-Native Gas: Users can directly utilize USD stablecoins such as USDC, USDT, or OUSD to pay for extremely low network fees (targeting under $0.001 per transaction). This eliminates the financial and accounting friction inherent in traditional public chains, which require holding volatile tokens for Gas.

-

Dedicated Payment Lanes: By isolating payment transactions from other on-chain activities at the protocol level, Tempo provides deterministic low latency (approximately 500ms for finality) and anti-congestion capabilities for payment flows. Combined with Tempo's proprietary Machine Payment Protocol (MPP), OUSD can offer a permissionless underlying payment rail for high-frequency AI Agent micro-transactions.

However, OUSD's consortium governance model has also encountered practical tests in its early stages. The official consortium list published by OUSD included many globally renowned enterprises, creating strong initial momentum. Subsequently, some well-known South Korean enterprises and financial institutions, including Samsung Electronics and Dunamu, successively clarified that the parties were only in the preliminary contact or evaluation stages, had not signed any binding cooperation agreements, and had not committed substantial resources. This controversy should not merely be interpreted as a promotional misstep; it more deeply reflects the inherent dilemma of consortium-type stablecoins: the more participants there are, the greater the market momentum, but the coordination costs for governance, execution, profit distribution, and commercial commitments will concurrently rise.

Therefore, when tracking and evaluating the subsequent development of OUSD, a more critical metric is the actual depth of integration by these renowned enterprises—whether they will practically incorporate OUSD into real payment workflows, wallet balances, merchant settlements, and cross-border capital flows.

Judging from the emergence of OUSD, the future competition in the stablecoin industry may be shifting. The mere issuance of stablecoins may increasingly resemble underlying licensing, balance sheet management, and compliant operations businesses in the future; the entities possessing stronger bargaining power may be payment networks, merchant gateways, wallet account systems, cross-border capital flows, and on-chain settlement infrastructures. The significance of Open Standard / OUSD lies precisely in bringing this shift to the forefront: the stablecoin profit pool will not necessarily remain concentrated primarily in the hands of issuers; distribution channels and real payment scenarios will demand more yield and governance influence.

Facing the challenge from OUSD, how leading stablecoin institutions represented by Circle will respond warrants continuous observation. Whether they will distribute a portion of the reserve yields, launch more targeted channel incentive programs, or build and deeply support specific payment chains may influence the future reallocation of stablecoin market shares. In other words, OUSD may not necessarily alter the dominant positions of USDC or USDT in the short term, but it has posed a longer-term question: should the core value of stablecoins be captured solely by the issuers, or shared collectively among payment networks, distribution gateways, and practical use cases?

2. Weekly Selected Market Signals

Weak NFP and Lower Oil Prices Ease Rate-Hike Pressure; U.S. Equities Stage a Partial Recovery, While Crypto Rebounds on a Still-Cautious Liquidity Base

Last week, the key variables for global markets were cooling U.S. labor data and a decline in energy risk premiums, which together eased concerns over a near-term Fed rate hike. U.S. nonfarm payrolls increased by only 57,000 in June, well below expectations. Although the unemployment rate fell to 4.2%, this was mainly driven by a decline in labor force participation, suggesting that the labor market was not reaccelerating but instead showing signs of marginal cooling. At the same time, the resumption of energy transportation through the Strait of Hormuz and OPEC+ signals of higher production led to a clear decline in the energy risk premium previously driven by Middle East tensions. The macro trading narrative therefore shifted from “inflation and rate-hike pressure” to “cooling employment, lower oil prices, and reduced near-term rate-hike probability,” creating a recovery window for equities, gold, and parts of the crypto market.

This shift was first reflected in energy, precious metals, and rates. Driven by expectations of OPEC+ production increases and the normalization of shipping through the Strait of Hormuz, oil prices continued to fall, with Brent crude dropping below USD 72 per barrel and WTI approaching USD 68 per barrel, largely giving back the risk premium built up during the previous Middle East conflict. Lower oil prices eased near-term energy inflation pressure and reduced the urgency for the Fed to hike rates immediately. Gold, supported by weaker employment data and cooling rate-hike expectations, rose more than 2% last week and approached a two-week high. Meanwhile, U.S. short-end Treasury yields declined and the U.S. dollar weakened. Market pricing shifted from the post-strong-NFP debate over “whether another rate hike is needed” to a stance closer to “near-term wait-and-see, with residual rate-hike tail risks later this year.” This is relatively supportive for risk assets, but since inflation has not yet returned to the Fed’s target range, markets have not re-entered a clear rate-cut trade.

In equities, U.S. stocks staged a partial recovery last week after weaker payroll data and lower oil prices, but this did not mark a broad-based expansion in risk appetite. Market leadership remained concentrated in large-cap technology, software, and communication services, while semiconductors, energy, and some previous momentum names pulled back. This suggests that capital was still rotating selectively between “easing rate-hike pressure” and “divergence within the AI trade,” rather than indiscriminately buying risk assets. In Japan and South Korea, South Korea remained one of the stronger markets, supported by AI memory, HBM, and the semiconductor cycle. Japan stayed in a high-level consolidation range amid the U.S. equity rebound and yen volatility, with semiconductor equipment, industrial automation, and AI-related supply chains still providing support. The most important development to watch is SK Hynix’s planned Nasdaq listing through an ADR. As a core player in Korea’s AI memory and HBM value chain, its U.S. listing would give global investors a more direct access point and could help Korean semiconductor assets move closer to the valuation framework of the U.S. AI hardware chain.

In crypto markets, BTC recovered after the weaker NFP print last week, but still underperformed U.S. technology stocks overall. BTC hovered around USD 60,000 at the beginning of last week, briefly fell toward USD 58,000 midweek, and then rebounded above USD 62,000 as rate-hike expectations cooled and both the U.S. dollar and Treasury yields declined. ETH performed relatively better, rebounding from around USD 1,600 to the USD 1,700–1,800 range. In the short term, weaker payroll data provided a macro-driven rebound window for crypto assets, but the recovery in BTC and ETH was driven more by easing rate pressure than by a clear improvement in crypto-native liquidity. ETF buying has not yet regained consistency, while total stablecoin supply continued to contract, indicating that on-chain liquidity remains cautious. Overall, the current crypto market is better characterized as a partial recovery driven by macro rate relief, rather than a broad recovery in risk appetite.

Data Source: SoSoValue

In ETF flows, based on SoSoValue data, U.S. spot BTC ETFs recorded around USD 527 million in net outflows last week, although the pace of outflows has started to ease. BTC ETFs continued to see net outflows from June 29 to July 1, before recording around USD 222 million in net inflows on July 2, ending 10 consecutive trading days of outflows. U.S. equities were closed on July 3 for the Independence Day holiday. Overall, BTC ETF selling pressure has moderated, but institutional capital has not yet returned to stable buying.

ETH ETF flows were closer to neutral, with only a small net outflow last week and materially less pressure than BTC ETFs. Current ETF flows appear to reflect a partial rebound after macro sentiment improved, rather than sustained one-way incremental inflows. Whether the crypto market can recover further in the near term will still depend on whether BTC ETF buying regains consistency and whether total stablecoin supply returns to expansion.

Data Source: DeFiLlama

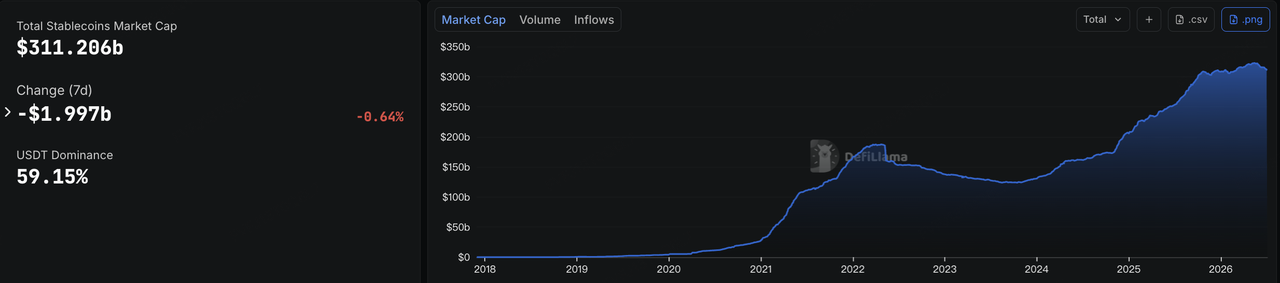

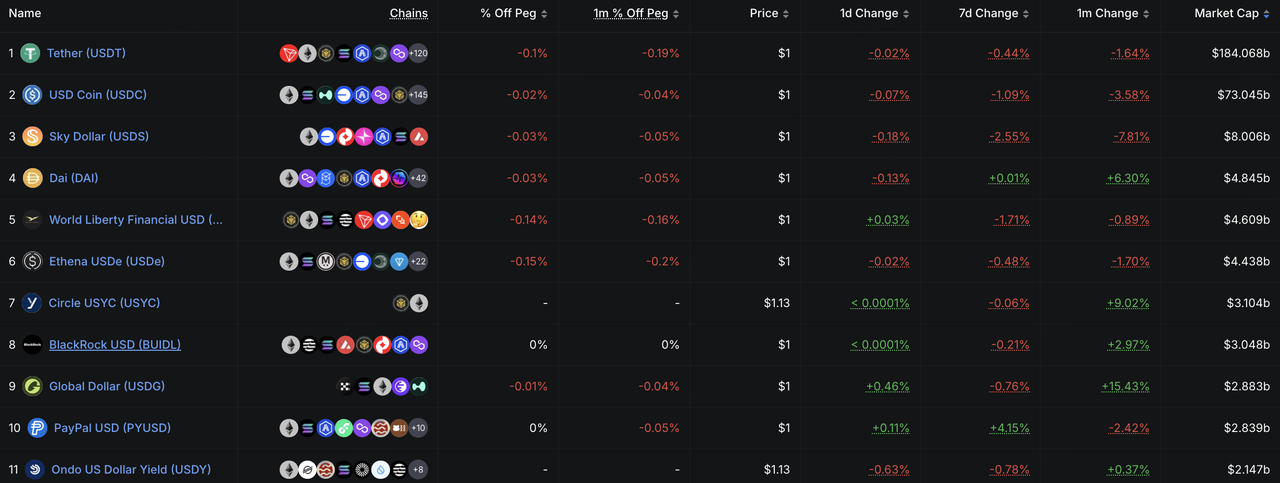

On stablecoins, DeFiLlama data shows that as of July 6, total stablecoin market capitalization stood at around USD 311.2 billion, down approximately USD 2 billion over seven days, a decline of around 0.64%. USDT’s market share was around 59.15%. This suggests that despite the rebound in crypto asset prices after the weaker payroll data, on-chain dollar liquidity did not expand in tandem, and market liquidity remains cautious.

Structurally, neither USDT nor USDC saw meaningful new liquidity inflows. Ecosystem-oriented and yield-bearing stablecoins such as USDS, USD1, and USDe also declined to varying degrees, indicating that the market rebound has not yet driven a renewed expansion in on-chain capital. By contrast, PYUSD and USYC still saw structural growth, suggesting that payment-focused stablecoins and institutional on-chain cash management tools remain resilient. Overall, the key signal from the stablecoin market is that price recovery has not yet brought back aggregate on-chain dollar liquidity. Capital is still being reallocated among mainstream settlement assets, payment stablecoins, and institutional cash management instruments.

Data Source: CME FedWatch Tool

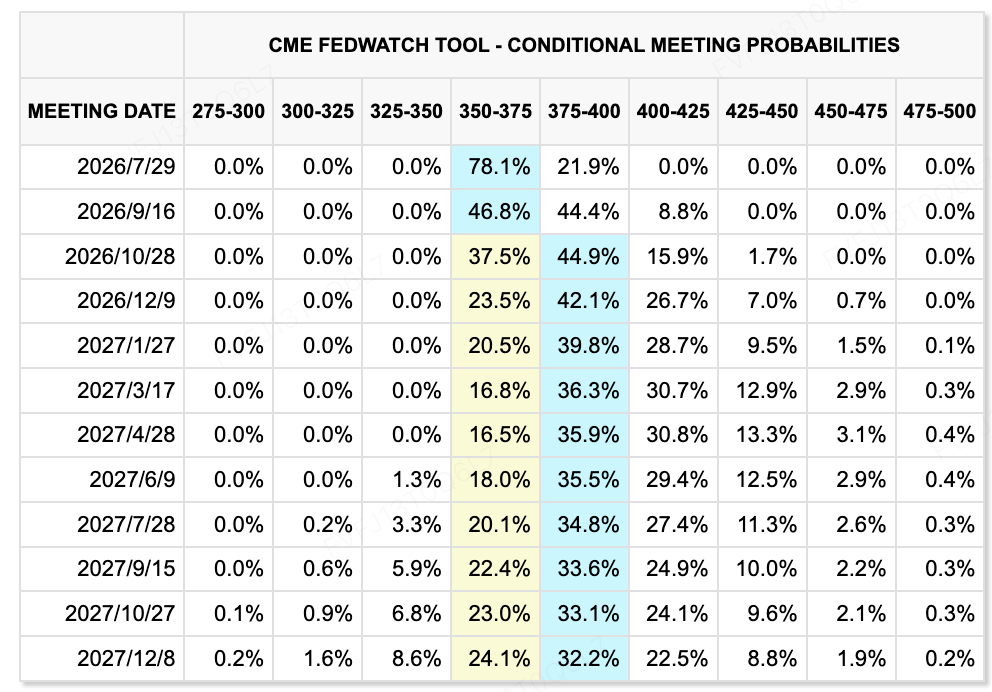

On rate expectations, the CME FedWatch Tool shows that markets still assign a relatively high probability to the Fed keeping the current 3.50%–3.75% target range unchanged at the July 29 meeting. After the weaker NFP data, the probability of a July rate hike fell significantly, and markets are more inclined to expect the Fed to remain on hold in the near term. However, some rate-hike pricing remains for September and later this year, suggesting that markets have not fully dismissed the scenario in which sticky inflation forces the Fed to tighten again.

The minutes of the Fed’s June meeting will be released at 2:00 p.m. ET on July 8. As this was the first FOMC meeting chaired by Kevin Warsh, markets will closely watch whether the minutes further confirm a hawkish tone and whether more officials view rate hikes as the baseline scenario. For risk assets, weaker payroll data has reduced near-term rate-hike pressure, but as long as the far-end rate path does not clearly move lower, valuation expansion in technology stocks and crypto assets will remain constrained.

Key Events to Watch This Week:

-

July 7: SpaceX enters the Nasdaq 100; USTR tariff hearings; Sun Valley Conference begins. SpaceX’s inclusion in the Nasdaq 100 could bring passive inflows and further test the market’s capacity to absorb large-cap technology growth valuations. USTR tariff hearings and the Sun Valley Conference correspond respectively to trade-friction risks and expectations for AI/technology industry cooperation.

-

July 9: China June CPI/PPI, financial data, foreign exchange reserves, and Fed June meeting minutes. China’s data will help markets assess price divergence, credit expansion, and domestic demand recovery. The Fed minutes will be the most important global macro event this week, with markets focused on internal disagreement over the rate path after Warsh’s first meeting as Chair.

-

July 9: Hong Kong lock-up expiries for Zhipu, MiniMax, Iluvatar CoreX and others; Hong Kong listings of Luxshare Precision and Chaozhou Three-Circle. AI unicorns and hardware supply-chain assets will face a liquidity test, with markets watching whether the scarcity premium for high-valuation AI assets can persist.

-

July 10: SK Hynix ADR tentatively set to list on Nasdaq. The listing would provide U.S. investors with direct access to a leading Korean AI memory-chip company. If trading is active, it could support a valuation re-rating of Korean semiconductor assets.

-

July 11: A new round of U.S.–Iran talks may take place in Pakistan. If negotiations continue to advance, the oil risk premium could fall further. If talks stall or disruptions around the Strait of Hormuz re-emerge, energy prices and inflation expectations could become volatile again.

-

U.S. Q2 earnings season begins this week, with PepsiCo and Delta Air Lines in focus. Earnings will help markets assess the impact of high rates, oil-price volatility, and consumer resilience on corporate profits, while also setting the stage for the upcoming technology and AI supply-chain earnings cycle.

Primary Market Funding Observations:

Data Source: CryptoRank

Based on CryptoRank’s broad statistical coverage, crypto primary-market financing continued to show three features last week: large deals remained concentrated, M&A activity was active, and AI plus institutional infrastructure continued to attract more attention. Compared with pure front-end applications or high-beta asset issuance, capital flowed more toward AI/HPC infrastructure, regulated trading platforms, privacy AI, institutional on-chain data, and decentralized compute markets. This indicates that primary-market investors still prefer projects with real demand, institutional customers, and monetizable use cases.

Among large deals, Ionic Digital completed a USD 400 million private equity placement and filed for a Nasdaq direct listing. The company is positioned across Bitcoin mining, AI, and high-performance computing infrastructure, with participation from Attestor, Oaktree Capital Management, and Sachem Head Capital. This case shows that miners are shifting from pure BTC production assets toward AI/HPC data-center infrastructure, while capital markets are more willing to re-rate companies with long-term compute contracts and AI revenue exposure.

On the M&A side, Japanese financial group SBI Holdings agreed to acquire crypto exchange Bitbank for approximately USD 289 million. This reflects the increasing concentration of Japan’s crypto market around regulated, bank-backed, and integrated financial platforms. It also suggests that traditional financial institutions are still using acquisitions to build out trading, custody, stablecoin, and on-chain finance capabilities.

AI and crypto remained another key theme. Venice AI completed a USD 65 million Series A round at a USD 1 billion post-money valuation, with investors including Dragonfly and Coinbase Ventures. The project is positioned as a privacy-first AI platform with strong ties to crypto-native users and token systems. Its financing suggests that capital is still looking for commercially viable AI x Web3 opportunities, but investors now prefer projects with existing users, revenue, and clear product forms over purely conceptual AI+Crypto narratives.

Institutional on-chain data and compute markets are also worth tracking. Allium completed a USD 40 million Series B round as an on-chain data platform for enterprises and financial institutions. Ornn raised USD 33 million to build a decentralized compute market and standardized compute-pricing infrastructure. Overall, last week’s primary-market keywords were not broad risk-appetite recovery, but “infrastructure, institutionalization, and AI.” With the secondary market still affected by ETF flows and macro rate volatility, primary-market capital continues to favor projects with explainable business models, institutional customers, and real-world demand.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.