On December 15th, Bitcoin fell from $90,000 to $85,616, a drop of over 5% in a single day.

There were no major scandals or negative events that day, and on-chain data showed no unusual selling pressure. Looking only at cryptocurrency news, it's hard to find a plausible reason.

However, on the same day, gold was priced at $4,323 per ounce, only $1 lower than the previous day.

One fell 5%, the other barely moved.

If Bitcoin truly were "digital gold," a tool to hedge against inflation and fiat currency devaluation, its performance in the face of risk events should resemble that of gold. But this time, its movement clearly resembled that of high-beta tech stocks on the Nasdaq.

What drove this decline? The answer may lie in Tokyo.

The Butterfly Effect in Tokyo

On December 19th, the Bank of Japan will hold its interest rate meeting. The market anticipates a 25 basis point rate hike, raising the policy rate from 0.5% to 0.75%.

0.75% may not sound high, but it represents Japan's highest interest rate in nearly 30 years. In prediction markets like Polymarket, traders are pricing in a 98% probability of this rate hike.

Why would a central bank decision from Tokyo cause Bitcoin to drop 5% within 48 hours?

This stems from something called "yen carry trades."

The logic is simple:

Japanese interest rates have long been near zero or even negative, making borrowing yen virtually free. Global hedge funds, asset management firms, and trading desks have borrowed massive amounts of yen, converted it into dollars, and then used it to buy higher-yielding assets—US Treasury bonds, US stocks, cryptocurrencies, etc.

As long as the returns on these assets exceed the cost of borrowing yen, the interest rate differential is the profit.

This strategy has existed for decades, its scale too large to be precisely measured. Conservative estimates put it at several hundred billion dollars, and if derivatives exposure is included, some analysts believe it could reach trillions.

Meanwhile, Japan has another unique status:

It is the largest foreign holder of US Treasury bonds, holding $1.18 trillion in US debt.

This means that changes in Japan's capital flows directly impact the world's most important bond market, subsequently affecting the pricing of all risky assets.

Now, with the Bank of Japan deciding to raise interest rates, the underlying logic of this game is shaken.

First, the cost of borrowing yen rises, narrowing arbitrage opportunities; more problematic is that the expectation of an interest rate hike will drive the yen's appreciation, and these institutions initially borrowed yen to exchange for dollars for investment;

Now, to repay the debt, they must sell their dollar assets and exchange them back for yen. The higher the yen appreciates, the more assets they need to sell.

This "forced selling" doesn't discriminate in terms of timing or asset type. Whatever has the best liquidity and is easiest to convert into cash will be sold first.

Therefore, it's easy to see why Bitcoin, with its 24-hour trading without price limits and a relatively shallower market depth compared to stocks, is often the first to be dumped.

Looking back at the timeline of the Bank of Japan's interest rate hikes over the past few years, this speculation is somewhat supported by data:

The most recent was on July 31, 2024. After the BOJ announced a rate hike to 0.25%, the yen appreciated against the dollar from 160 to below 140. BTC subsequently fell from $65,000 to $50,000 within a week, a drop of approximately 23%, wiping out $60 billion in market capitalization from the entire crypto market.

According to statistics from several on-chain analysts, after the past three BOJ rate hikes, BTC experienced a pullback of over 20%.

While the specific start and end points and time windows of these figures vary, the direction is highly consistent:

Every time Japan tightens monetary policy, BTC is hit hardest.

Therefore, the author believes that what happened on December 15th was essentially a market "preemptive strike." Funds had already begun to withdraw before the decision was announced on the 19th.

On that day, US BTC ETFs saw a net outflow of $357 million, the largest single-day outflow in nearly two weeks; over $600 million in leveraged long positions in the crypto market were liquidated within 24 hours.

This is likely not just retail investor panic, but a chain reaction of arbitrage trading liquidation.

Is Bitcoin still digital gold?

The mechanism of yen carry trades was explained above, but one question remains unanswered:

Why is BTC always the first to be sold off?

A common explanation is that BTC has "good liquidity and 24-hour trading," which is true, but not enough.

The real reason is that BTC has been repriced over the past two years: it is no longer an "alternative asset" independent of traditional finance, but has been welded into Wall Street's risk exposure.

Last January, the US SEC approved spot Bitcoin ETFs. This was a milestone the crypto industry had waited a decade for; trillion-dollar asset management giants like BlackRock and Fidelity could finally legally include BTC in their clients' portfolios.

The funds did indeed flow in. But this has brought about a shift in ownership: the holders of BTC have changed.

Previously, BTC was bought by crypto natives, retail investors, and some aggressive family offices.

Now, BTC is bought by pension funds, hedge funds, and asset allocation models. These institutions also hold US stocks, US bonds, and gold, managing their portfolios through "risk budgeting."

When the overall portfolio needs to reduce risk, they don't just sell BTC or just stocks; they reduce their holdings proportionally.

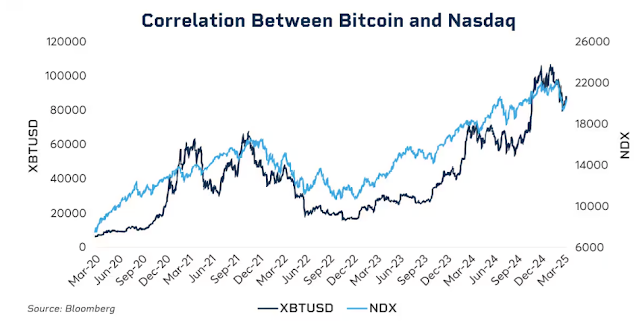

Data shows this correlation.

In early 2025, the 30-day rolling correlation between BTC and the Nasdaq 100 index reached 0.80, the highest level since 2022. In contrast, before 2020, this correlation hovered between -0.2 and 0.2, essentially negligible.

More importantly, this correlation increases significantly during periods of market stress.

The March 2020 stock market crash due to the pandemic, the Fed's aggressive interest rate hikes in 2022, and tariff concerns in early 2025... Every time risk aversion intensifies, the correlation between Bitcoin and US stocks becomes even stronger.

When institutions are in a panic, they don't distinguish between "crypto assets" and "tech stocks"; they only look at one label: risk exposure.

This raises an awkward question: does the narrative of digital gold still hold true?

Looking at a longer timeframe, gold has risen over 60% since 2025, its best year since 1979; Bitcoin, on the other hand, has retreated over 30% from its peak during the same period.

Both assets, touted as hedges against inflation and fiat currency devaluation, have followed completely opposite curves in the same macroeconomic environment.

This isn't to say that Bitcoin's long-term value is problematic; its five-year compound annual return still far exceeds that of the S&P 500 and Nasdaq.

But at this stage, its short-term pricing logic has changed: it's a highly volatile, high-beta risk asset, not a safe-haven tool.

Understanding this is crucial to understanding why a 25 basis point rate hike by the Bank of Japan could cause BTC to drop by thousands of dollars within 48 hours.

It's not because Japanese investors were selling BTC, but because when global liquidity tightens, institutions follow the same logic to reduce all risk exposures, and BTC happens to be the most volatile and easily liquidated link in this chain.

What will happen on December 19th?

As I write this, there are still two days until the Bank of Japan's interest rate meeting.

The market has already priced in the rate hike. The yield on Japanese 10-year government bonds has risen to 1.95%, the highest in 18 years. In other words, the bond market has already priced in the tightening expectations.

If the rate hike has been fully anticipated, will there still be an impact on the 19th?

Historical experience suggests: yes, but the intensity depends on the wording.

The impact of central bank decisions is never just the numbers themselves, but the signals they send. Both the Bank of Japan (BOJ) and Bank of Japan (BOJ) interest rate hikes have different implications. If BOJ Governor Kazuo Ueda states at the press conference that "future assessments will be cautious based on data," the market will breathe a sigh of relief.

However, if he says, "Inflationary pressures persist, and further tightening cannot be ruled out," it could be the start of another wave of selling.

Currently, Japan's inflation rate is around 3%, higher than the BOJ's 2% target. The market's concern isn't about this rate hike itself, but rather whether Japan is entering a sustained tightening cycle.

If the answer is yes, the collapse of yen carry trades won't be a one-off event, but a process lasting several months.

However, some analysts believe this time might be different.

First, speculative funds have shifted from net short to net long positions in the yen. The sharp drop in July 2024 was partly due to market surprise, as a large amount of capital was shorting the yen at that time. Now the position direction has reversed, limiting the potential for unexpected appreciation.

Second, Japanese government bond yields have risen for more than half a year, from 1.1% at the beginning of the year to nearly 2% now. In a sense, the market has already "raised interest rates itself," and the Bank of Japan is simply confirming a fait accompli.

Third, the Federal Reserve just cut interest rates by 25 basis points, and the overall direction of global liquidity is towards easing. Japan is tightening in the opposite direction, but if dollar liquidity is ample, it may partially offset the pressure on the yen.

These factors cannot guarantee that BTC will not fall, but they may mean that the drop this time will not be as extreme as previous ones.

Looking at the price action after previous BOJ rate hikes, BTC usually bottoms out within one to two weeks after the decision, and then enters a period of consolidation or rebound. If this pattern holds true, late December to early January may be the window of greatest volatility, but it could also be an opportunity to buy after being oversold.

Accepted and Influenced

Connecting the preceding text, the logical chain is actually quite clear:

Bank of Japan rate hike → Yen carry trade unwinding → Global liquidity tightening → Institutions reducing positions according to risk budgets → BTC, as a high-beta asset, is prioritized for selling.

In this chain, BTC did nothing wrong.

It was simply placed in a position beyond its control, at the end of the transmission chain of global macro liquidity.

You might find this hard to accept, but it's the new normal in the ETF era.

Before 2024, BTC's price fluctuations were primarily driven by crypto-native factors: halving cycles, on-chain data, exchange activity, and regulatory news. At that time, its correlation with US stocks and bonds was very low, making it, to some extent, a "separate asset class."

After 2024, Wall Street arrived.

BTC was placed within the same risk management framework as stocks and bonds. Its holder structure changed, and its pricing logic changed accordingly.

BTC's market capitalization surged from several hundred billion dollars to 1.7 trillion dollars. But this also brought a side effect: BTC's immunity to macro events disappeared.

A single statement from the Federal Reserve or a decision by the Bank of Japan can cause it to fluctuate by more than 5% within hours.

If you believed in the narrative of "digital gold," believing it could provide shelter in turbulent times, then the performance in 2025 was somewhat disappointing. At least for now, the market isn't pricing it as a safe-haven asset.

Perhaps this is just a temporary misalignment. Perhaps institutionalization is still in its early stages, and once allocation ratios stabilize, BTC will find its rhythm again. Perhaps the next halving cycle will once again prove the dominance of crypto-native factors...

But until then, if you hold BTC, you need to accept this reality:

You are also holding exposure to global liquidity. What happens in a Tokyo conference room may determine your account balance next week more than any on-chain metric.

This is the price of institutionalization. As for whether it's worth it, everyone has their own answer.