Author: Chen Mingkun's Macroeconomic Observations

This article primarily answers five questions:

First, when war breaks out, what does the market reassess first;

Second, why do different wars correspond to different asset languages;

Third, the four war dynamics each rewrite which layer of variables;

Fourth, which asset samples from modern warfare are most worth revisiting repeatedly;

Fifth, how to translate the judgment of war into methodology and position sizing.

If you're more concerned about your investment position, go directly to Section 5.

Many people see war first through the news.

Macro investors often aren’t looking at the news itself, but rather at the shift in asset rankings.

Over the past month, war has reignited in the Middle East, and from my desk at Tsinghua’s Zijing Garden, I repeatedly reviewed past conflicts and asset evolution in modern warfare, becoming increasingly certain of one thing:

What war changes first is often not the global order, but the asset hierarchy.

In my view, when studying war and assets, what matters most is not立场, not emotion, nor seizing the right to interpret. What truly matters is:

Break down the war into variables, map those variables to prices, and then align prices with positions.

So, a more important question than “What to buy when war comes” is:

When war breaks out, what does the market reassess first?

This article is written for serious traders. Not for spectators, and not for those looking for a simple “what to buy in a war” answer.

If, when the next big volatility hits, you can follow the herd a little less and judge a little more; let emotion guide you a little less and strategy a little more—then this article will have been worth it.

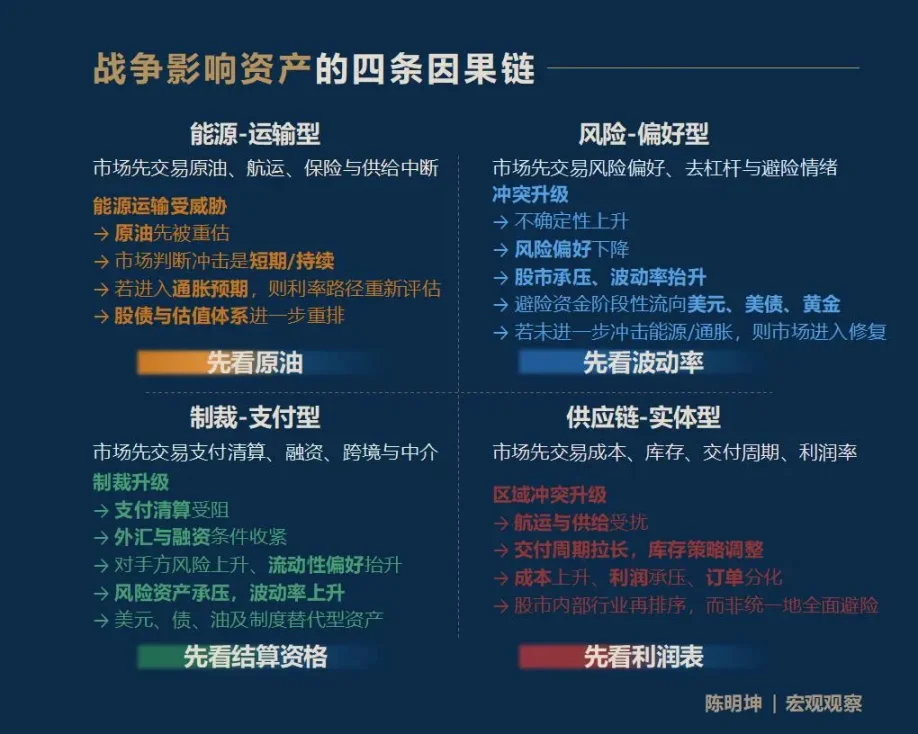

I. War affects assets—not through one answer, but through four pathways.

First, the conclusion: War affects assets, and the most common outcome is not a single unified answer, but four entirely different transmission pathways:

The first type is energy-transport warfare.

The market first trades oil, shipping, insurance, and supply disruption risks.

Second, risk-preference conflict.

The market first trades volatility, risk appetite, deleveraging, and risk-off sentiment.

The third is sanction-based payment warfare.

Markets first traded payment, clearing, financing, cross-border settlement, and financial intermediary functions.

The fourth type: supply chain—physical asset conflict.

Market first considers transaction costs, inventory, delivery cycles, profit margins, and industry reordering.

For investors, what matters most is not knowing all the answers, but quickly identifying the first variable to be reevaluated amid market noise.

I call it: the first-order variable.

Whoever captures the first-order variable will more easily understand the subsequent price path.

Jumping to conclusions about assets during volatile market conditions often leads to being corrected by the market.

If you were to compress this framework into one memorable phrase, it would be:

Energy—Transportation, start with crude oil;

Risk-seeking—check volatility first;

Sanctions—payment-related, first check settlement eligibility;

Supply chain—physical type, start with the income statement.

It should be noted that these four causal chains are not exhaustive, but rather entry points.

The impact of war on assets often continues to spread along longer, more intricate, and more complex chains. For example, how does the current U.S.-Israel-Iran conflict affect grain prices six months from now? The pathway—natural gas influencing fertilizer, fertilizer influencing grain, and grain influencing inflation and assets in vulnerable nations—is equally valid.

What I aim to provide is not a fixed answer, but a macro-level observational approach: enabling every market participant to build their own causal chain based on it.

When war comes, which variable will become the market’s first language?

Two: Four Most Commonly Misjudged Views During Times of War

Before diving into the specific analysis, I’d like to outline the foundational thinking behind this section:

Falsifiability.

I don’t believe in vague, correct-sounding macro calls that never translate into price or position.

The real value of war studies lies in putting judgments into the market to be tested.

Meaningful research claims must be falsifiable.

Past events are used to verify or falsify judgments about the past; future profits or losses are used to verify or falsify judgments about the present (a harsh statement, but that is the reality).

As the conflict escalates, the most common phrases on the market appear almost instantly:

Gold will definitely rise.

Bitcoin is digital gold and serves as a safe haven.

When oil prices rise, the stock market must fall all the way down.

Benefiting from defense, just buy defense stocks.

The issue with these statements is not that they are necessarily wrong,

But because they are too fast, too neat, and too much like common sense.

The underlying mindset here is "marking the boat to find the sword." War does not bring a single-directional outcome, but rather a series of pricing processes with different rhythms, levels, and causal logic.

Therefore, before entering the dynamic analysis of war assets, these most easily misjudged intuitions must be cleared away.

01 | Buy gold during wartime, right?

Gold is certainly one of the most important assets to monitor during times of war.

If "war = gold rises" were a reliable formula, gold prices across different war events should at least generally move in similar directions.

But historical prices were not like this.

What sounds smooth often most easily hinders thinking.

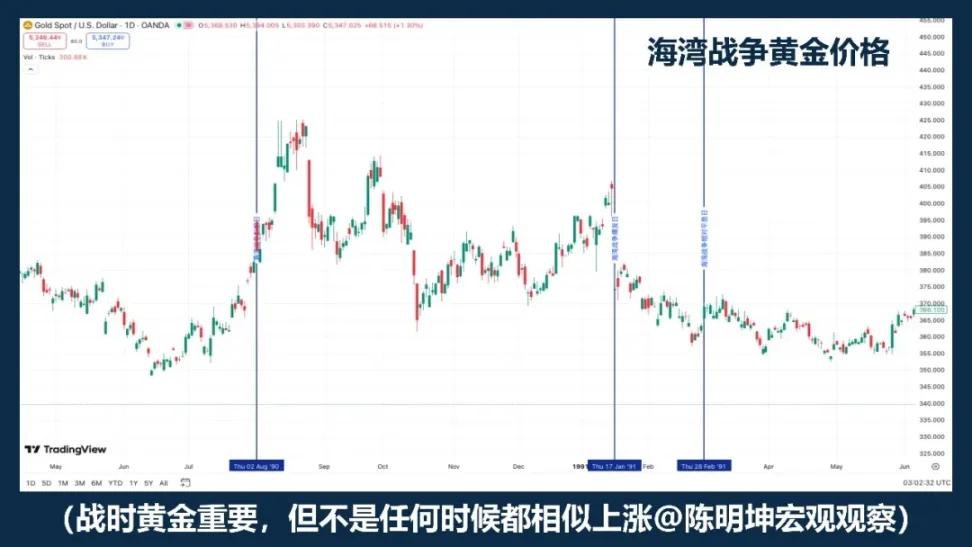

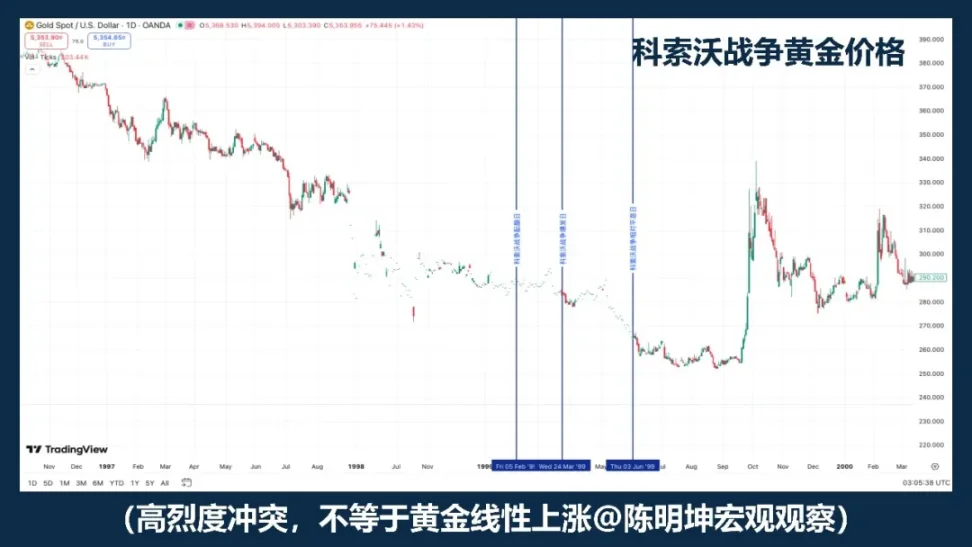

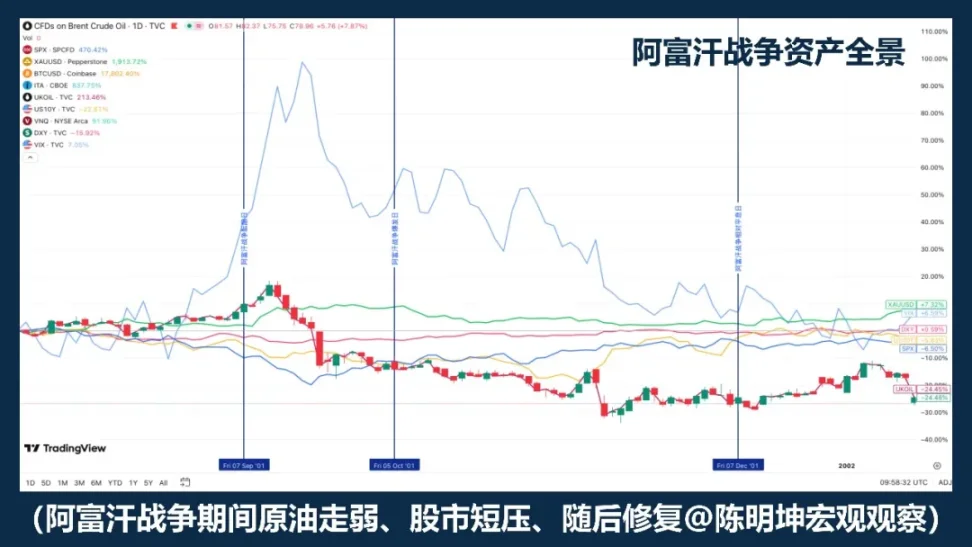

The 1999 Kosovo War is a good counterexample. High-intensity conflict alone is not sufficient to automatically imply a one-sided rally in gold.

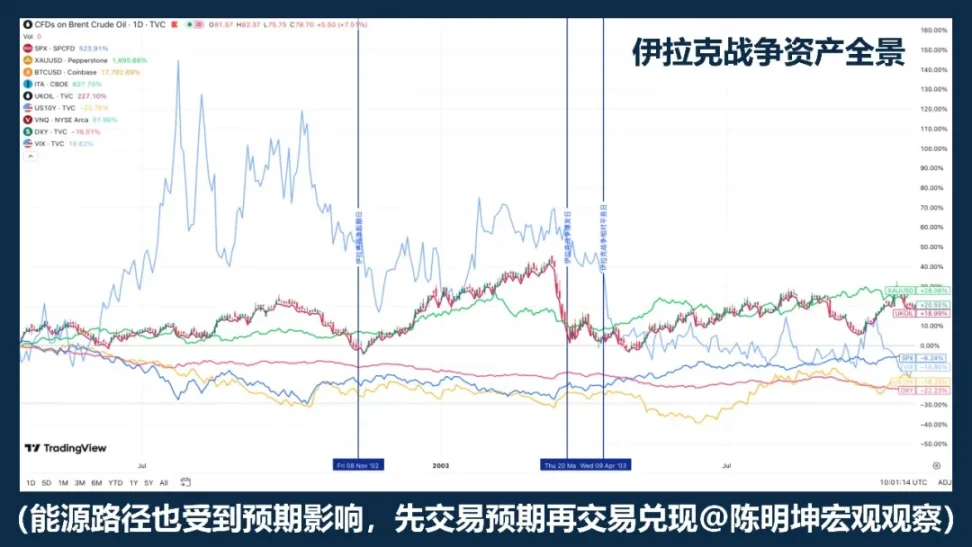

The 2003 Iraq War revealed another pattern: gold tends to be bought ahead of escalating war expectations, then enters a period of decline and consolidation after the official start of hostilities.

The study by Rigobon and Sack on the risks of the Iraq War also supports this: when war risks increase, oil prices, stock prices, U.S. Treasury yields, credit spreads, and the dollar all show significant responses, but gold does not exhibit a similarly robust statistical response.

What truly matters to remember is not a specific year, but a more important fact:

Gold is often traded not on the war itself, but on the expectation of war.

A more accurate statement is not "buy gold during wartime," but:

Gold is typically a priority asset to watch during times of war, but it is not a mechanical long button for war.

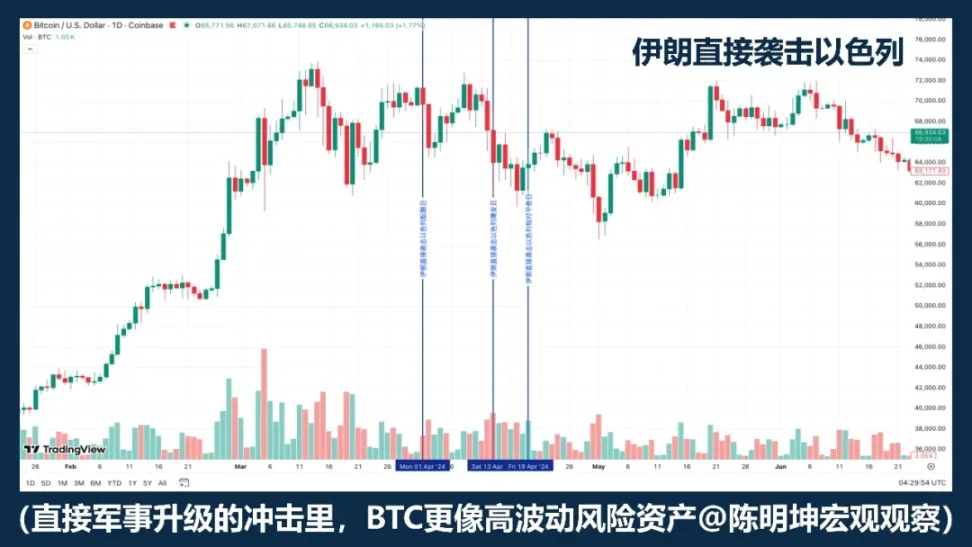

02 | Is Bitcoin a Safe-Haven Asset?

Classifying BTC simply as a "safe-haven asset" is itself not rigorous.

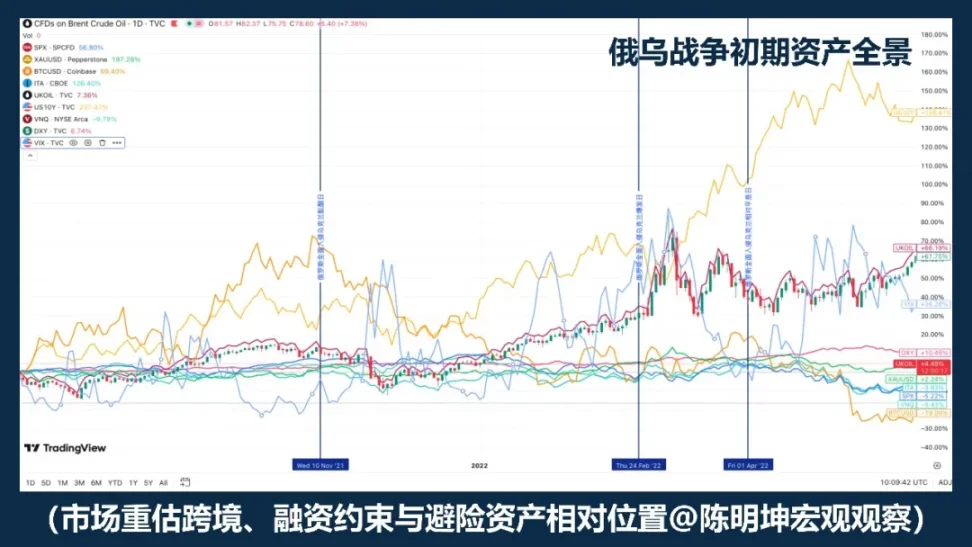

If Bitcoin always rose when war broke out, its performance across different conflict scenarios should be relatively consistent. But from the Russia-Ukraine conflict, the Israel-Hamas conflict, to recent escalations in the Middle East, the reality has been different: sometimes it fell, sometimes it strengthened, and sometimes it dropped first before stabilizing.

This is sufficient to show:

War is not a direct variable affecting BTC's price movements.

When the market first reacts with liquidity contraction, risk aversion, and deleveraging, BTC often behaves more like a high-volatility risk asset than a safe-haven asset, as these scenarios typically prompt investors to sell high-volatility, high-beta, and easily liquidatable assets first.

In other words, often, war doesn't prompt the market to "buy it as a hedge," but rather causes the market to first reduce positions in all high-volatility assets.

In this scenario, it behaves more like a risk-oriented tech asset than a safe-haven asset.

But that doesn't mean it lacks uniqueness.

Its biggest difference from gold is that it is not only a tradable asset, but also a digital asset that can be transferred across borders, operates 24/7, and does not rely on a single banking system.

So, a more accurate question is not "Will BTC act as a safe haven," but:

BTC is not a mechanical safe-haven asset in times of war.

It is traded by the market alternately as a risk asset, a liquidity asset, or an alternative settlement instrument across different phases of conflict.

War will not directly determine its price movements.

What war truly determines is which attribute of the market investors are more willing to trade right now.

03 | When oil prices rise, do stocks always fall?

This is the easiest phrase to say casually in war studies.

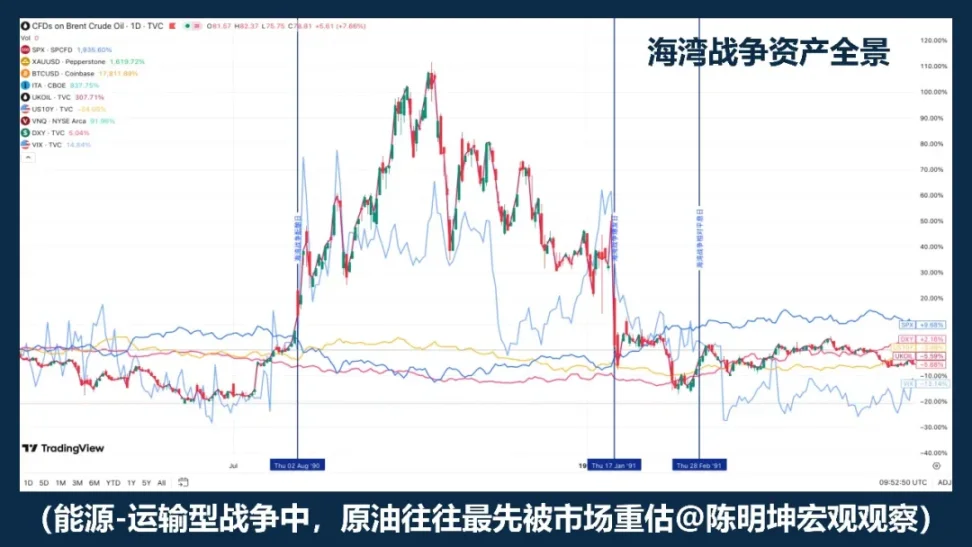

When conflict erupts in the Middle East, oil prices often react first—and that’s correct. This isn’t about ordinary risk; it’s about the energy transportation route itself. EIA data is clear: in 2024, approximately 20 million barrels per day of oil passed through the Strait of Hormuz, accounting for roughly 20% of global liquid petroleum consumption; about 20% of global LNG trade also transits through this corridor. As soon as markets begin to worry about this passage, crude oil prices naturally rise in response.

But the issue is that rising oil prices do not necessarily lead to falling stock prices.

The history of the Gulf War teaches us that "oil rises, stocks fall" can be the initial reaction; however, as the situation becomes clearer and the worst-case scenario does not continue to spread, the market later prices in risk recovery, leading to a stock market rebound.

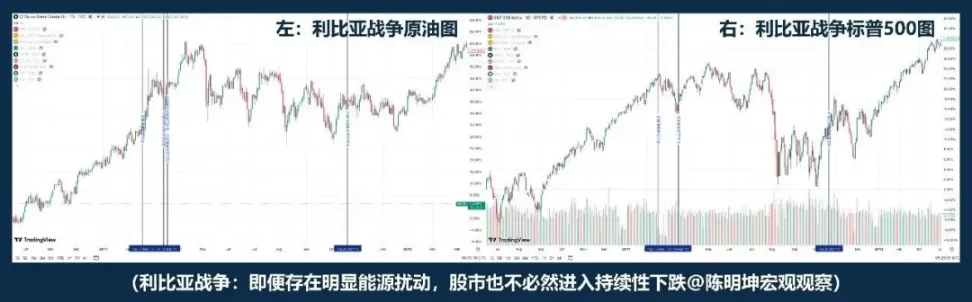

The conflict in Libya provides another example: closer to "oil up, stocks down." The logic of "oil rises, stocks fall" is not the true logic of war.

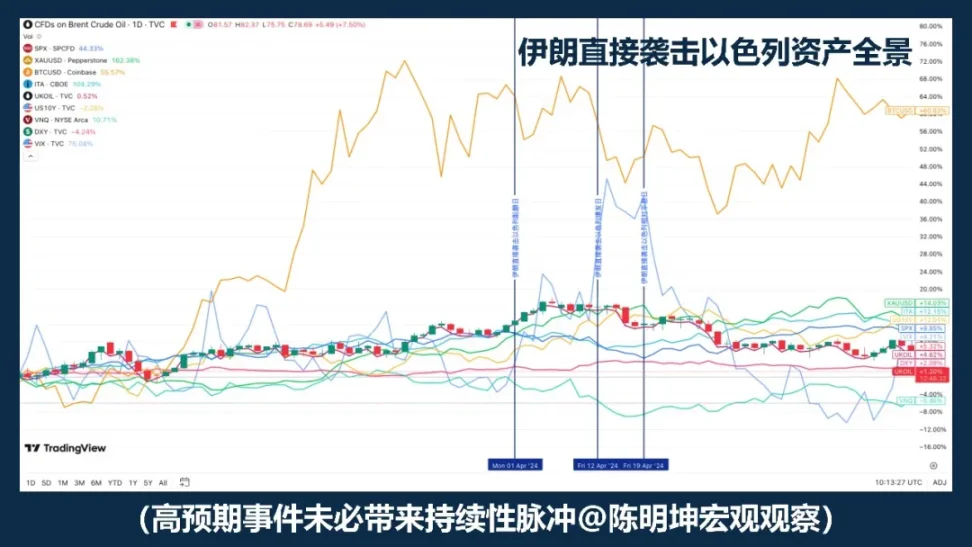

If the Gulf War and the Libyan War seem distant, the 2024 Iranian attack on Israel provides a more immediate example. Crude oil initially surged; during the outbreak period to the calming day, "oil falls, stocks fall"; however, the S&P 500 did not subsequently enter a systemic decline.

Rigobon and Sack also found when studying the Iraq War that when war risk rises, it’s not just oil that moves—but oil prices, stock prices, U.S. Treasury yields, credit spreads, and the dollar all move together. In other words, the market is not just trading oil; it’s simultaneously trading growth, inflation, risk aversion, and funding conditions.

So, what really matters isn't whether oil prices have risen, but the following three things:

First, is this energy shock short-term or long-term?

Second, will it lead to medium-term inflation expectations;

Third, will the central bank alter the interest rate path?

Therefore, a more accurate statement is not "oil rises, stocks fall," but rather:

Rising oil prices often mark the beginning of a war premium; how the stock market moves next depends on whether this shock further reshapes growth, inflation, and interest rates.

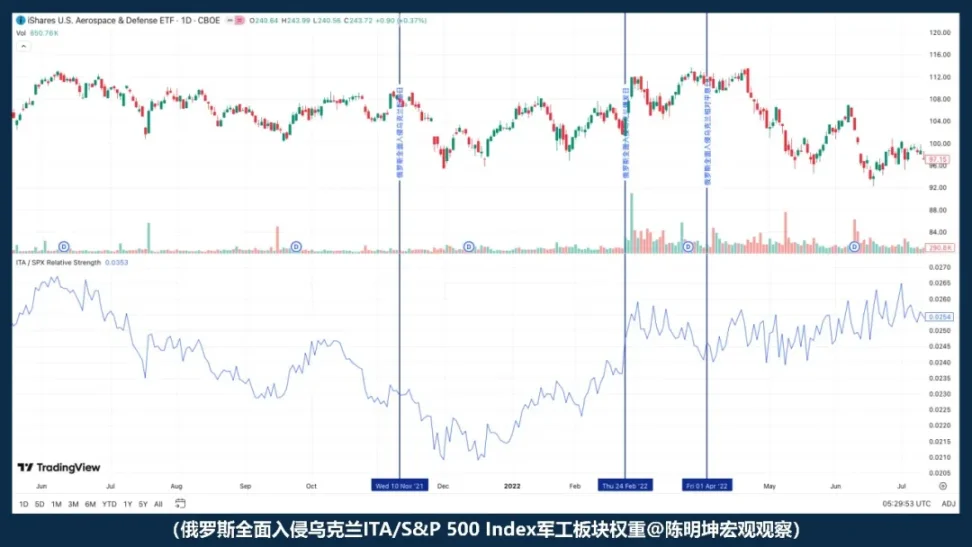

04 | If there's a war, will defense stocks definitely profit?

The biggest problem with the phrase "War benefits defense industries" is not that it's wrong, but that it's too easy to make people think they've already figured it out.

Logically, it makes sense:

As tensions rise, security concerns intensify, defense spending forecasts are revised upward, and the potential for orders expands—defense appears to be a naturally beneficial sector.

But the market isn't that simple.

Industry benefits do not necessarily mean immediate stock price increases;

A stock rising in price does not mean it outperforms the market.

After the full-scale invasion of the Russia-Ukraine war erupted, ITA did not strengthen relative to the S&P 500; instead, it weakened. In other words, at the moment the war began, the market did not immediately trade on the narrative of "defense sector benefits." Instead, it first priced in broader forces: risk appetite, liquidity, and macroeconomic uncertainty.

So, a more accurate statement is not "War benefits defense stocks—just buy defense stocks," but rather:

War elevates defense-related narratives, but at the moment of outbreak, what is typically priced in by the market first is not orders, but risk appetite.

Whether defense stocks can outperform has never depended solely on whether the logic holds up,

It also depends on valuation, expectations gap, and which layer of variables the market trades first.

The most dangerous thing in war is often not having an opinion,

But having opinions too quickly.

Three: The real question: When war arrives, what does the market reassess first?

After resolving these false positives, the real issue becomes clear:

War is not a single variable that directly determines asset price movements; it acts more like a trigger.

What truly determines how the market reacts is not just the conflict itself,

Rather, it is the type of conflict, macroeconomic cycles, event expectations, and the most critical first-order variable.

So, the question is no longer "What benefits from war and what suffers from it," but:

Which language will the market first use to price it?

Next, we will move beyond emotional judgment to discuss the four real war dynamics that influence asset pricing.

Four Types of War Dynamics: Understand War by First Identifying Its Type

To understand a war, you cannot look only at the battlefield itself.

More importantly, determine which layer of variables it rewrites first.

01 | Energy - Transportation Warfare

Why is crude oil always the first to be caught by the market?

The type of conflict that most quickly pushes the market into a "pricing state" is typically an energy-transportation war.

The common feature of such conflicts is not the severity of the conflict itself, but that it often immediately hits the upstream lifeline of the global economy:

Oil-producing regions, straits, tankers, ports, marine insurance, energy transportation routes.

Once these positions are threatened, what the market often reevaluates first is not the stock market, not gold, and not even macroeconomic growth itself, but rather positions closer to the upstream physical supply side:

Crude oil and transportation risks.

Crude oil always moves first not because it is "naturally sensitive," but because of its uniquely pivotal position in the modern economic system—it serves as both a fundamental input for industry and an upstream variable in the inflation chain.

When markets begin to suspect that transportation will be disrupted, insurance costs will rise, shipping routes will be rerouted, or supply will contract, crude oil will be the first to be priced in.

In energy-transportation warfare, crude oil is not a side effect, but the most direct vehicle of risk.

But there is a particularly important detail:

Crude oil often moves first, but moving first doesn't mean it will continue to rise.

The Gulf War is one of the most typical examples. During the buildup to the war, crude oil prices rose significantly; after the official outbreak, prices continued to surge; however, as the situation became clearer, prices quickly declined.

The Iraq War further revealed another layer of structure. In this case, during the phase when war expectations were escalating, crude oil and gold had already priced in the anticipation; by the time the war officially began, the market instead aligned more closely with the “buy the rumor, sell the fact” dynamic. This means that, while crude oil is typically the primary variable in energy-transportation wars, its price trajectory still depends heavily on two factors: first, whether the market had already fully priced in the expectation; and second, whether the worst-case scenario actually materialized after the event occurred.

Therefore, understanding this type of conflict cannot rely solely on whether "oil prices have risen," but must consider the two underlying contexts in which it occurs.

The first layer is the expectation gap. If the event itself is beyond expectations, the oil price pulse is typically stronger; if the event has already been widely discussed and priced in by the market, then even if the conflict officially erupts, oil prices may quickly shift into a range-bound pattern or even experience a "sell the fact" reaction.

Iran’s direct strike on Israel is a classic example: the risk did not enter the market unannounced, so while assets experienced a pulse, they did not unconditionally extend into a sustained revaluation.

The second layer is the macroeconomic cycle. If it occurs in an environment of low inflation and ample policy space, the market is more likely to view it as a temporary disruption;

If this occurs in an environment characterized by high inflation and already tight monetary policy, the market will immediately ask: Will this round of oil price increases enter medium-term inflation expectations? Will it delay policy pivots?

This is also the most important distinction between energy-transportation wars and other types of warfare: its impact originates in the physical world and propagates inward through the financial markets along this chain:

Energy transportation is at risk

Crude oil is first revalued

→ Determine whether the market sentiment shock is short-term or sustained

→ If inflation expectations rise, reassess the interest rate path

→ Reallocation of equities, bonds, and valuation frameworks

So, the most important takeaway from energy-transportation wars isn't that "oil will definitely rise,"

Instead: Crude oil is often the earliest upstream variable traded in the market.

But crude oil moving first doesn't mean the impact will automatically evolve into a long-term main theme.

What truly determines the subsequent path is never the oil price itself,

But whether oil prices can continue to influence inflation expectations, discount rates, and valuation frameworks.

In this type of war logic, crude oil moving first is not the conclusion, but the starting point of financial transmission.

02 | Risk - Preference War

What is often reassessed first by the market is not oil, but risk appetite.

The first thing altered by this kind of war is not the physical constraints of the macro world,

But rather the market's risk tolerance.

If the conflict does not directly threaten oil-producing regions, strait shipping lanes, oil tankers, or critical energy infrastructure, the market often first reassesses risk appetite rather than supply constraints.

The primary driver of this kind of conflict is not whether energy supplies will be cut off, but whether uncertainty will suddenly rise and whether risk assets can still be held confidently.

Therefore, the first transmission of this type of war is typically not "crude oil moving first," but:

Conflict escalates

→ Uncertainty increases

→ Decreased risk appetite

Stock market under pressure, volatility rising

→ Risk-off capital flows toward the U.S. dollar and gold, among others

→ If there is no further impact on energy and inflation, the market then enters a recovery phase.

This chain of causality explains an important phenomenon:

Why, after some wars break out, do stock markets fall and gold react, yet prices don’t automatically evolve into a longer-term one-sided trend? Because such wars first impact holding willingness, not deeper factors like supply, inflation, or discount rates.

The IMF's research on geopolitical risks also highlights that major military conflicts significantly impact stock and options market pricing through increased risk aversion, tighter financial conditions, and the spread of uncertainty. In other words, during this phase, markets first reprice not a shortage of any physical commodity, but rather the renewed valuation of future volatility and tail risks. The initial decline reflects more of a risk discount than a permanent downward shift in long-term valuation fundamentals. Only when the shock to risk appetite continues to propagate downward and affects deeper macroeconomic variables does this war-induced sentiment pulse escalate into a more persistent asset reallocation.

Therefore, a more accurate conclusion is not "War comes, gold must rise," nor "War comes, the stock market must fall," but rather:

In this type of war logic, the market typically re-evaluates volatility and risk assets first; the initial decline primarily reflects a risk discount and does not automatically establish a long-term trend.

03 | Sanctions - The War of Payments

The war of payments is not first rewritten by price, but by eligibility.

Sanctions—the core of payment warfare—are not about the price of a single commodity, but about accessibility to the cross-border financial system.

When conflicts escalate to the level of sanctions, what markets first reassess is often not just supply, but: payments, clearing, reserves, financing, and counterparty credit.

The Russia-Ukraine war is the most typical example of this type. After 2022, the European Union imposed a series of financial sanctions on Russia, including restrictions on Russia’s access to EU capital and financial markets, a ban on transactions with the Russian Central Bank, the removal of several Russian banks from SWIFT, and the freezing or "unavailable" status of certain Russian assets. The U.S. Treasury’s OFAC also implemented Directive 4, prohibiting Americans from engaging in related transactions with the Russian Central Bank, the National Wealth Fund, and the Ministry of Finance. At this point, the market is no longer just facing the question of “whether oil will be cut off,” but a deeper one: Can the existing cross-border financial infrastructure continue to function as before?

The typical transmission of this kind of war is not directly from price to price,

Instead, start with eligibility leading to price:

Sanctions escalate

→ Payment and settlement are blocked

→ Foreign exchange and financing conditions tighten

→ Counterparty risk and increased liquidity preference

Risk assets under pressure, volatility rises

Dollars, U.S. Treasuries, oil, and certain institutional substitute assets are being repriced.

Therefore, this type of shock differs fundamentally from energy-transportation wars:

Energy shocks first rewrite the supply price,

Payment shock first rewrites the settlement eligibility.

Once settlement eligibility begins to fluctuate, asset rankings rapidly diverge. Assets heavily reliant on the global banking system, cross-border financing, and mainstream clearing networks are more likely to face discounts; whereas new digital settlement tools that retain the ability to transfer, hold, or settle even under restricted payment conditions are more likely to attract additional attention.

The IMF's 2025 Global Financial Stability Report concludes that major geopolitical risk events, particularly military conflicts, transmit shocks to equity markets, sovereign risk premia, exchange rates, and commodity markets through heightened risk aversion, tighter financial conditions, and disruptions to trade and financial linkages; such events may also significantly depress stock prices and elevate sovereign risk premia. For markets, this means the focus of sanction-payment wars is not on whether any particular asset will rise, but on whether financial intermediation can continue to function smoothly.

The IMF’s research on geopolitical risks also illustrates this point. Major military conflicts not only depress equities and raise sovereign risk premiums through increased risk aversion and tighter financial conditions, but also spill over to third countries via trade and financial linkages.

This is why sanctions-related shocks often spread farther than the battlefield itself.

A more accurate description of the new on-chain settlement tools is not that they are “naturally hedging,” but rather: when traditional payment frictions, capital flow constraints, and cross-border settlement barriers increase, the market re-evaluates their attributes as non-bank, cross-border, 24/7 settlement channels. What is truly being re-evaluated by the market is not the alternative store-of-value narrative itself, but the institutional value of alternative settlement channels.

If an energy-transport war asks, "Will the goods still get through?"

So sanctions—the payment warfare—ask:

Can the money still be transferred?

04 | Supply Chain - Entity Type Conflict

The market trades the profit and loss statement first, not the risk-off narrative.

Another type of conflict neither directly strangles global energy supplies nor immediately rewires the international payment system, yet still significantly alters asset pricing.

This is: Supply Chain - Entity Conflict.

The core of this conflict is not whether the world will immediately enter a full risk-off mode, but whether the systems for production, transportation, inventory, and delivery will continue to be distorted.

What is often revised first are not crude oil, gold, or global risk appetite themselves, but variables closer to corporate operations:

Shipping costs, insurance, delivery cycle, inventory safety margin, profit margin, and capital expenditure expectations.

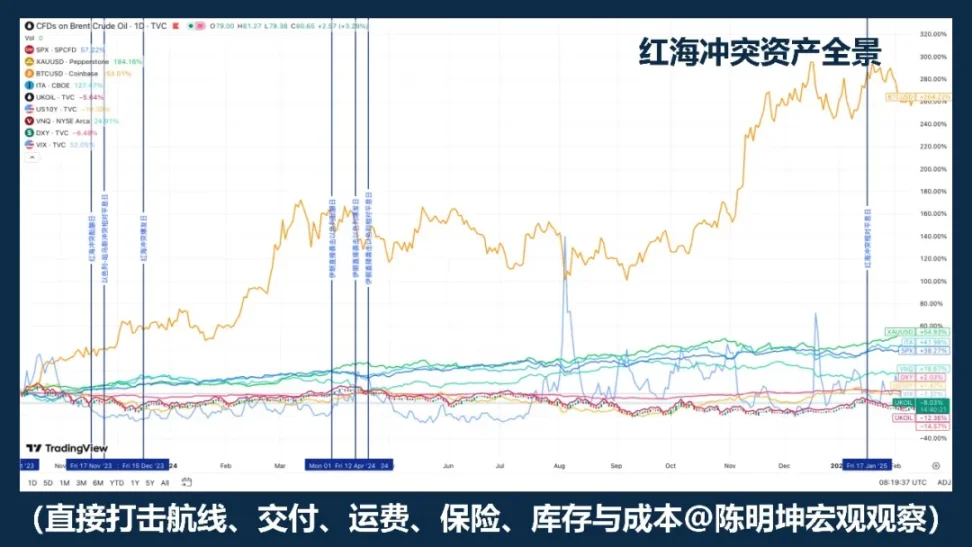

The most prominent example is the Red Sea conflict. The IMF noted that in the first two months of 2024, trade volume through the Suez Canal declined by approximately 50% year-over-year, as attacks forced numerous vessels to detour around the Cape of Good Hope, disrupting supply chains; UNCTAD also reported that by the first half of February 2024, container tonnage passing through the Suez Canal had dropped by 82%, with significant capacity rerouted to the southern tip of Africa.

In this type of market shock, the first trades are often not about "buying safe havens," but rather: who will face higher costs; who will experience slower deliveries; who will see their profit margins hurt first; who will lose orders; and who will have their alternative supply capacity reassessed.

Its transmission chain is typically not a safe-haven line, but rather one more closely tied to the real economy:

Regional conflict escalates

→ Shipping and supply disrupted

→ Extended delivery cycles and adjusted inventory strategies

→ Rising costs, pressure on profit margins, and order diversification

→ Reallocation within stock market sectors, rather than a uniform flight to safety

The most common misjudgment in this type of conflict is that many people automatically equate "conflict" with "risk-off."

But supply chain—physical-type conflicts often do not first create risk trades with a unified market direction.

Its more common outcome is:

Sector differentiation, profit differentiation, and regional differentiation.

This is also why the impact of this type of conflict on assets is often slower, but not necessarily smaller. What it truly rewrites usually falls into three levels:

First, there is the cost layer: shipping, insurance, warehousing, parts procurement, and alternative transportation routes have increased costs.

Second, it is the inventory layer. Companies often shift from prioritizing efficiency to prioritizing resilience.

Third is the profitability layer: Can the company still deliver profits at its original pace? At this stage, the conflict moves into profit forecasts and valuation models.

Therefore, under such conflicts, asset performance typically does not involve broad-based risk-off behavior across asset classes, but rather a structural repricing within the stock market. Companies more heavily impacted are often those reliant on single-region production, single-route transportation, single-component sourcing, or high-turnover, low-inventory models; relatively benefited entities may include those with alternative production capacity, geographically diversified operations, stronger pricing power, or the ability to absorb order shifts.

So, a more accurate conclusion for this type of war is not:

When conflict arises, buy safe havens.

Instead:

When war first impacts production, transportation, inventory, and delivery systems, market reassessment often focuses not on broad risk aversion, but on costs, profit margins, and industry rankings.

If an energy shock first alters prices,

The payment-type shock first rewrites the eligibility,

Then, the supply chain-type shock is rewritten as:

Income Statement.

Five: From Judgment to Position — Investment Methodology in War

The previous discussion was about how war enters asset pricing.

But for investors, the real question is not whether understanding ends here,

but take one step further:

How to convert a judgment into a position.

The most common illusion war creates is that it resembles a massive directional opportunity.

But if you carefully examine history, you'll find that wars do not consistently produce replicable outcomes.

What it more stably produces is: volatility, mismatches, and the breakdown of correlations.

So, in investing during times of war, what truly matters is not betting on the direction, but first identifying which variables the market is actually trading:

This variable is creating short-term pulses,

It will continue to propagate along the asset chain;

Which prices are merely emotional reactions?

What shocks will solidify into medium-term main themes?

If I were to make this more specific and actionable, I would break it down into four steps.

The first step is always to identify the primary variable.

After a war breaks out, the market does not price all information simultaneously. It always first latches onto one variable and pushes it to the center of pricing: sometimes oil, sometimes risk appetite, sometimes payment systems, sometimes inventory and profit and loss statements. Many people immediately try to form an overall judgment about the entire war, but this is usually too early and too crude. The truly effective approach is to first assess:

What is the market trading right now—supply, risk appetite, payment friction, or earnings statements?

Getting the primary variable right gives your position direction; if you get it wrong, even a fully coherent narrative will likely lead to incorrect trades.

The second step is to prepare in advance, rather than rushing to build positions during the conflict.

The best war trades often don't begin at the moment full-scale conflict erupts. Many high-odds opportunities arise before the event enters public consciousness. By the time the market starts discussing it, the cheapest price window has usually already passed.

Therefore, before the battle, it’s more important to: study the boundaries, prepare your tools, identify vulnerabilities, and set up hedges. Don’t wait until the gunfire starts to decide what weapons to use.

Step three: During wartime, switch your trading approach and focus on pricing discrepancies.

After the outbreak of war, what is least in short supply is explanation; what is truly scarce is judgment of price. War does not come with a mechanical asset template; on the contrary, the one thing more certain than anything else is that it will create upheaval.

Initially, it is common in markets for some assets to overreact, others to underreact, and still others to simply move in tandem due to sentiment. In other words, war does not necessarily bring clarity; more often, it amplifies mispricings over short periods.

This is also why war is not necessarily suitable for reliably betting on direction,

but are often better suited for arbitrage and structured trading.

When markets experience drastic changes, what is often disrupted first is not opinions,

but the previously stable order between prices:

Spot and derivatives may become misaligned

Assets under the same logic will be misaligned.

Risk-off narratives and actual pricing can become misaligned

Short-term sentiment and medium-term transmission can also become misaligned.

The most important thing at this stage is not to take a stance,

Instead, identify: which prices are merely emotional impulses, which misalignments will quickly revert, which shocks will settle into medium-term trends, and which spreads, basis differentials, and correlation gaps are worth trading.

This part especially relies on arbitrage intuition and accumulated experience.

Those who have carefully studied historical war scenarios often respond more quickly to asset movements triggered by conflict, deploying and executing strategies accordingly. For example, during the 2025 silver squeeze, sharp traders swiftly entered silver arbitrage opportunities; similarly, in the recent gold volatility stemming from the U.S.-Israel-Iran conflict, astute traders more easily identified pricing mismatches across different gold derivatives.

These opportunities often arise quickly and disappear just as fast.

For strong traders, it’s a window;

For weak traders, it’s often just a fleeting fluctuation passing before their eyes.

Step four: After the crisis escalates, shift your trading focus from the event to its transmission.

In the early stages of the war, the market trades the event itself; as the war continues to unfold, the market trades its downstream consequences. What truly determines whether a war evolves from a short-term pulse into a mid-term narrative is not the volume of news, but whether the shock continues to penetrate deeper variables: whether it enters inflation expectations, whether it affects discount rates, whether it impacts corporate profit statements, and whether it alters settlement and financing conditions.

If none of these variables have been genuinely rewritten, the first wave of volatility often resembles a risk discount rather than a long-term repricing; but if these variables truly begin to change, the conflict is no longer just news—it starts becoming part of a broader trend. At this stage, the trading logic must also shift:

Shift from event impulses to trend analysis,

Shift from news-driven to macro-driven themes.

Macro hedging means employing flexible strategies. Facing different macroeconomic phenomena, various types of wars, and distinct transmission pathways, one must adaptively switch between different tools and enter different capital markets.

Ultimately, a position is not an emotional byproduct, but a financial expression of thought.

War amplifies volatility and magnifies misjudgments.

The purpose of a position is to let logic be tested by the market.

Opinions must correspond to variables;

The judgment must correspond to the tool;

Logic must ultimately enter fund allocation.

This is also my understanding of the war investment methodology:

Analyze logic before the battle, identify mismatches during the battle, and examine transmission after the battle.

Look at the variables first, then the price, and finally the position.

Because positions make thoughts falsifiable.

Investing is the shortest straight line from thought to wealth.