Article by Dong Jing

Source: Wall Street Journal

OpenAI may still be at least six months away from going public, but preparatory efforts on Wall Street have already begun quietly. Several investment banks are proactively reaching out to public market investors to gauge sentiment toward the listing prospects of ChatGPT’s parent company—but the responses have been far cooler than expected.

On March 9, according to the technology media The Information, informed sources revealed that several investment banks competing for OpenAI’s IPO underwriting business have begun polling public market investors. The Information interviewed 11 public market investors, most of whom do not currently hold OpenAI equity.

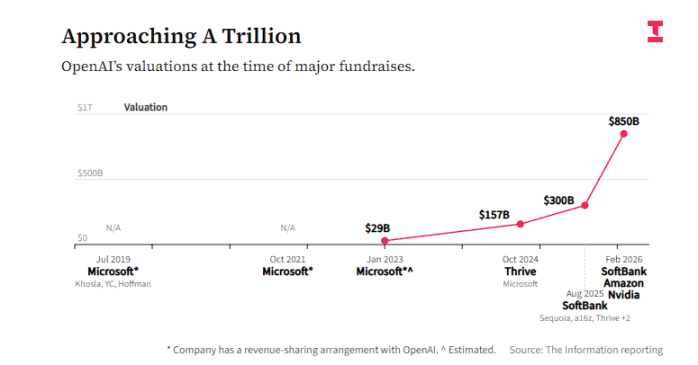

Respondents generally adopted a cautious stance toward this IPO, with primary concerns centered on two points: first, unclear profitability—OpenAI itself forecasts continued losses until at least 2030; second, an excessively high valuation—the company is currently raising funds at an $850 billion valuation, equivalent to 28 times its projected 2026 revenue, far exceeding NVIDIA’s price-to-sales ratio of approximately 12.

Reports indicate that the market's "cool" sentiment reflects the underlying tensions surrounding what could be the largest IPO in history: while investors widely acknowledge OpenAI's leading position in the AI competitive landscape, they remain cautious about whether it can achieve a fair valuation in the public markets. Meanwhile, the strong rise of competitor Anthropic is further diverting investor attention and enthusiasm.

Valuation Dispute: Why Is a 28x Price-to-Sales Ratio Expensive?

OpenAI is currently raising funds at an $85 billion valuation, with participants including NVIDIA, Amazon, and SoftBank. This figure has already deterred many public market investors, and its IPO pricing may be even higher.

Based on projected 2026 revenue, $850 billion corresponds to a price-to-sales ratio of approximately 28x. In comparison, NVIDIA, considered a benchmark for AI investments, currently has a price-to-sales ratio of about 12x.

According to reports, Bob Lang, founder of the trading firm Explosive Options, said directly:

I do believe OpenAI is an excellent company with a strong moat, but I don’t think any valuation on its first day of trading is fair to investors.

He stated that he is unlikely to participate in OpenAI’s public market offering, especially if its valuation multiple exceeds that of NVIDIA.

Lang also pointed out that the true beneficiaries of this IPO will be early investors who already hold shares and hyperscale cloud computing companies—they will gain an opportunity to cash out.

Prominent short-seller Jim Chanos questioned OpenAI’s valuation logic by using NVIDIA as a benchmark:

NVIDIA essentially dominates the market, with rapid growth, extremely high profit margins, and abundant cash flow. So why are you giving OpenAI a higher valuation?

Revenue Path: Burning Cash Until 2030—Will the Public Market Buy In?

According to reports, OpenAI itself predicts the company will continue to incur losses at least until 2030. This timeline has unsettled public market investors accustomed to evaluating profitability.

Some investors are concerned that the funds raised from OpenAI’s IPO may not be sufficient to carry it to profitability, potentially requiring additional financing that would dilute existing shareholders’ equity.

Mark Malek, Chief Investment Officer at Siebert Financial, said that even if OpenAI struggles to achieve significant profitability in the short term, he would still consider building a position after its IPO, but would strictly limit the position size—mirroring his strategy when he invested in Palantir.

Palantir currently has a price-to-sales ratio as high as 49x and is growing much faster than its peers, but Malek believes Palantir’s risks remain lower than OpenAI’s due to its more flexible cost structure.

If Palantir loses a government contract, that’s bad—but they can lay off employees. If you’ve spent five years building a data center, you can’t just say, “Never mind, forget it.” Palantir is driving a Formula 1 car, while OpenAI is operating a cargo ship.

In a report from January, JPMorgan analysts noted that OpenAI’s introduction of advertising in ChatGPT helps retain users, but also observed that customer sentiment toward OpenAI has been mixed following the company’s announcement of significant spending on chips and data centers.

Not everyone is standing by—some investors have explicitly stated they will consider shorting OpenAI’s stock once it goes public, betting that public markets have limited tolerance for its lengthy path to profitability.

Chanos holds a similar position. His core message to clients is: “You should go long on chip production and short on the locations where chips are stored.” The implication is that operating data centers itself is not a high-return business, and OpenAI’s business model heavily relies on massive investments in computing infrastructure.

Chanos also noted that there is currently insufficient financial information available about OpenAI to conduct a thorough analysis. However, he expects that once OpenAI formally files its IPO application, the public markets will engage in intense debate over its competitive landscape:

Is this a winner-takes-all scenario, or will the market remain fragmented like cloud computing, or will one company become the standard and maintain dominance long-term? So far, each model continues to outpace the others.

Anthropic's disruption: Competitors divert funding and attention

OpenAI’s path to an IPO also faces potential pressure from competitor Anthropic.

At this week’s Morgan Stanley Annual Technology Conference, Anthropic CEO Dario Amodei revealed that the company’s annualized revenue run rate has doubled to $20 billion. Anthropic recently completed a new funding round with a $380 billion valuation, and enterprise products such as its AI coding tool Claude Code are showing strong sales momentum.

Previously reported by The Information, Anthropic expects its costs for AI model training and operations over the coming years to be significantly lower than OpenAI's. Some investors now believe that, given its success in the enterprise customer market—where clients are willing to pay a premium for AI services—Anthropic may achieve better long-term profitability than OpenAI.

As Anthropic also prepares for its IPO, the two companies’ offerings may compete, further diluting investor capital and enthusiasm. Investors like Chanos have explicitly expressed a preference for Anthropic’s more restrained approach to compute investment, viewing it as a more prudent and sustainable business strategy.