Source: Culper Research

Translated by Azuma, Odaily Planet Daily

Editor’s Note: On March 6, Wall Street short-seller Culper Research suddenly published a report announcing its short position on ETH and related securities such as BMNR. Culper Research’s argument is that Vitalik and other developers miscalculated Ethereum’s demand elasticity prior to the Fusaka upgrade, thereby undermining ETH’s tokenomics. Culper Research also claims that Vitalik is fully aware of this issue and is acting to exit early, while Tom Lee, stubbornly clinging to his stance, is heading toward ruin.

In response to the institution's heavy short position, Vitalik himself and Tom Lee have not yet commented, but Vitalik’s father, Dmitry Buterin (dima.eth), responded: “Once you see the statement ‘Vitalik knows about this and is selling,’ you don’t need to read further. They are clowns seeking attention, not researchers.”

The following is the original content from Culper Research, translated by Odaily Planet Daily. Translating this article does not imply our endorsement of Culper Research’s views; it is intended solely to present certain Wall Street institutional perspectives on ETH and market sentiment.

We have recently disclosed that we are shorting ETH and ETH-related stocks, including Bitmine (BMNR).

We believe that after the Fusaka upgrade in December 2025, ETH’s tokenomics have been broken. Vitalik is well aware and is selling; while ETH’s most ardent bull, Tom Lee, continues to pour in ineffective investments. ETH will continue to decline.

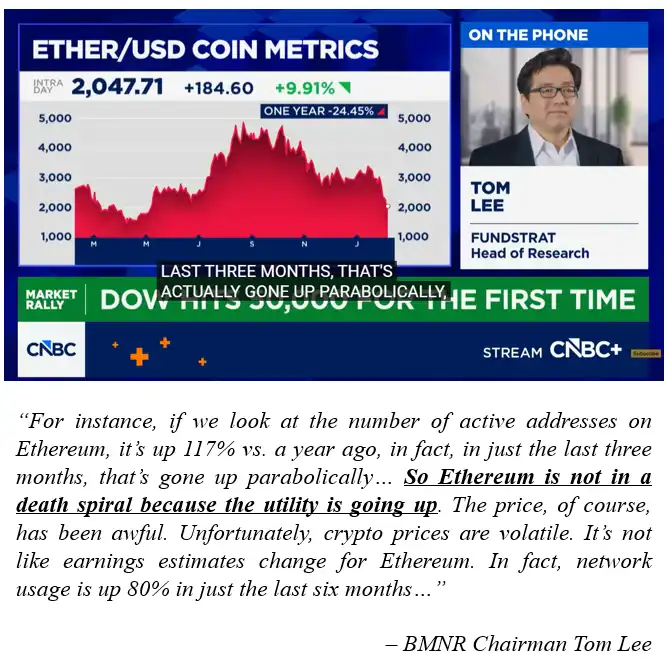

Tom Lee’s Bitmine has consistently defended ETH, claiming that “ETH is not in a death spiral as utility is increasing.” He cited the surge in active addresses and transaction volume on Ethereum following the Fusaka upgrade as evidence of所谓“fundamental improvements” and institutional adoption, but he is completely mistaken.

According to Tom Lee’s own logic, if Ethereum’s on-chain activity does not reflect genuine usage growth and fundamental improvements, then ETH is indeed in a death spiral.

And our research shows that this is exactly what is happening.

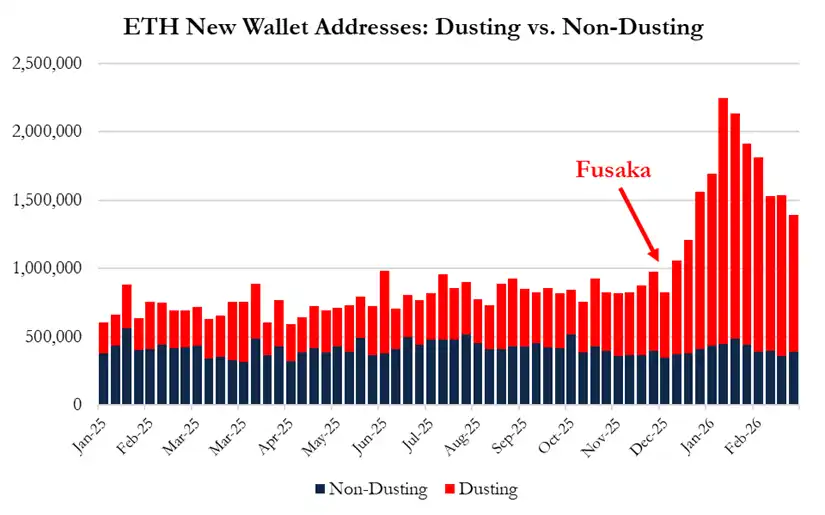

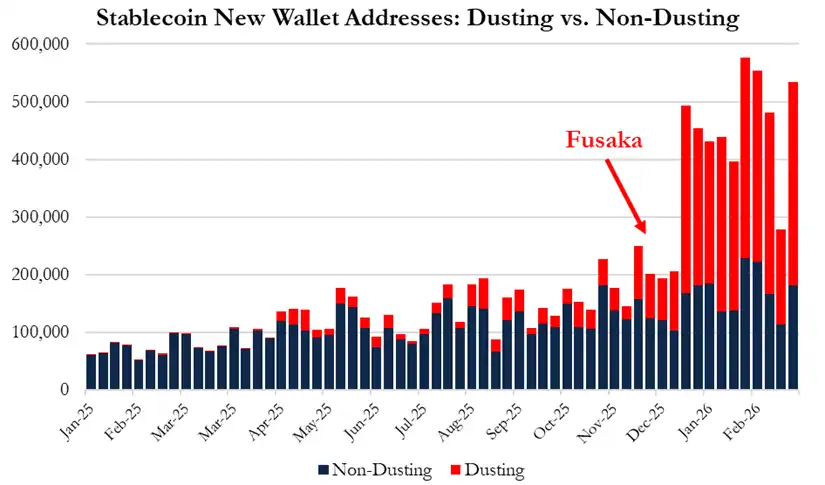

We conducted a comprehensive analysis of on-chain data from January 2025 to February 2026, revealing that Lee’s claim of “institutional adoption driving Ethereum activity growth” can actually be explained by widespread address poisoning and wallet dusting activities involving low-value addresses. These activities were triggered by excess block space following the Fusaka upgrade.

After the Fusaka upgrade:

· 95% of new wallet growth came from newly created dust addresses;

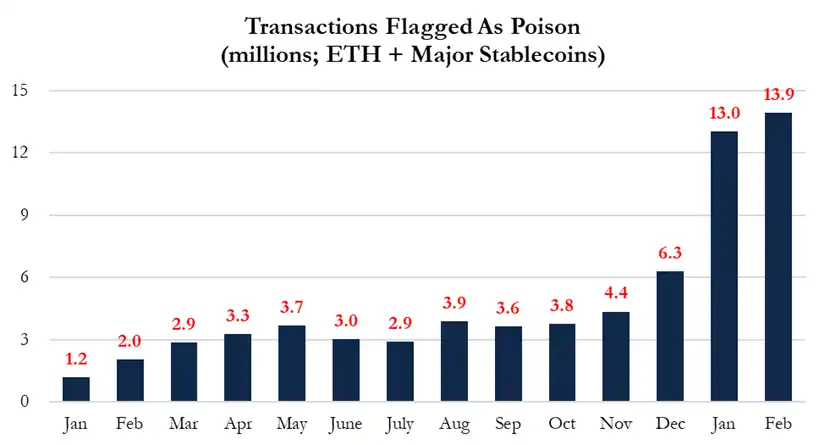

· The number of poisoning attacks has increased by more than threefold;

· Poisoning accounts for over 50% of Ethereum transaction growth;

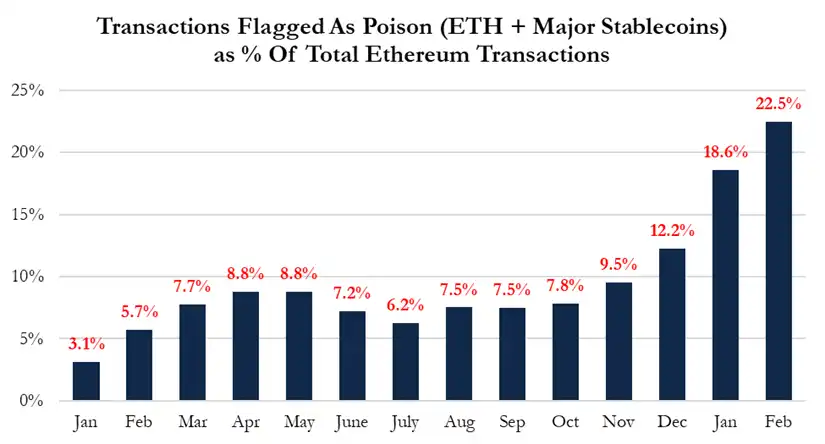

· Poison transactions currently account for 22.5% of all Ethereum transactions;

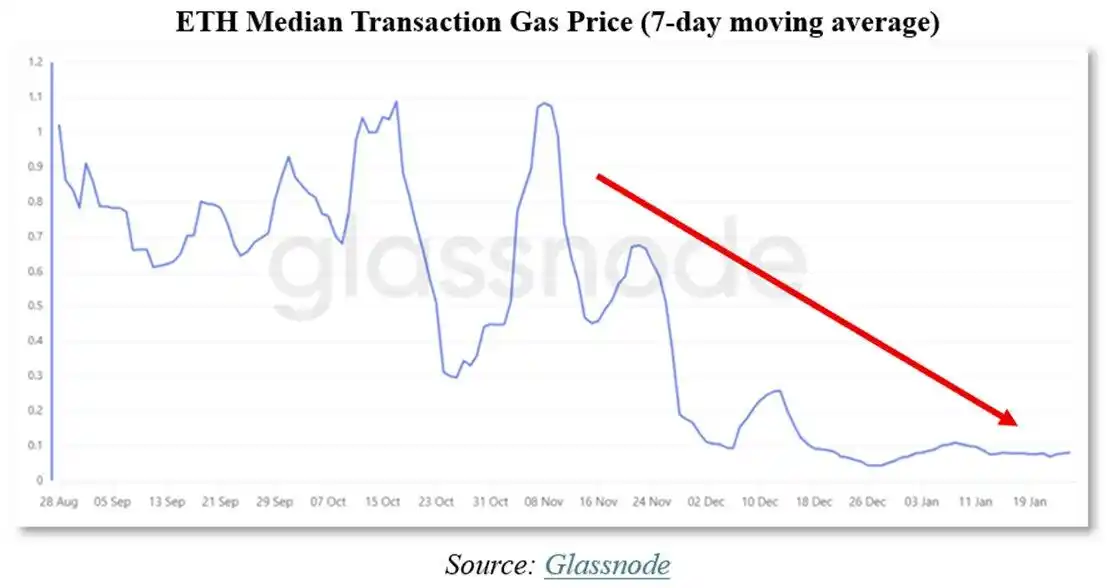

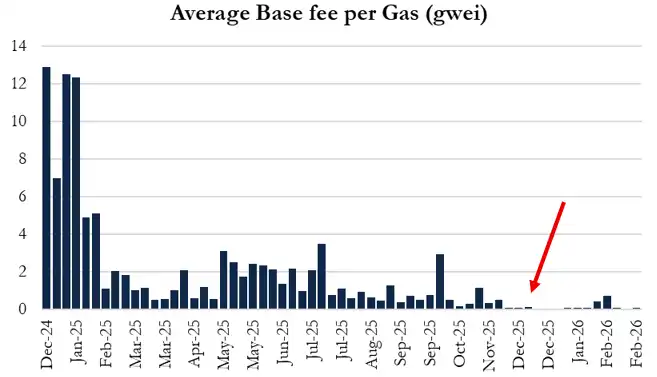

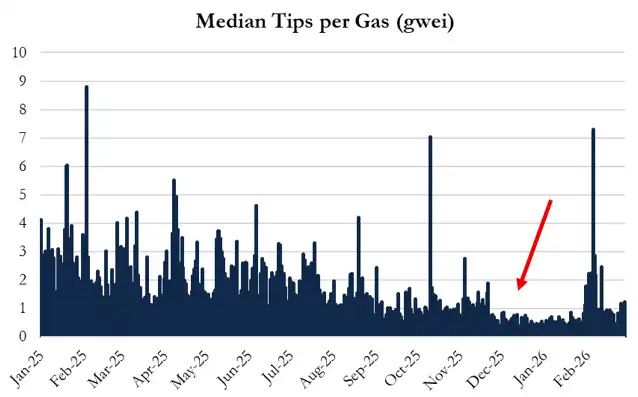

The Fusaka upgrade increased the gas limit from 45M to 60M to expand Ethereum Layer1 capacity. Vitalik and the protocol team previously anticipated a 10%–30% reduction in gas fees, but in reality, gas fees dropped by approximately 90%.

Vitalik and validators made a severe miscalculation in estimating the demand elasticity of Layer1. They used outdated mathematical models (based on assumptions from before EIP-1559 and the emergence of Layer2), overestimating Layer1 demand by 3 to 9 times. This is also why we believe Vitalik is selling large amounts of ETH. On January 30, Vitalik publicly announced he would sell 16,384 ETH to fund the Ethereum Foundation’s “austerity period,” but since then, he has sold over 19,300 ETH and continues to sell.

Vitalik understands what Tom Lee does not—that ETH's tokenomics have been broken.

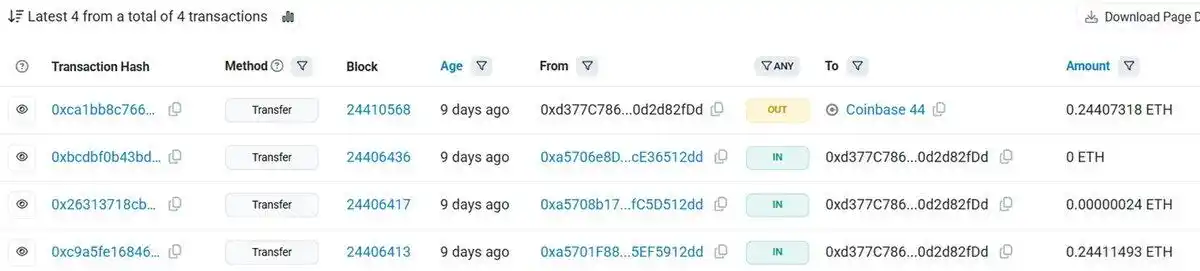

We personally documented Ethereum network address poisoning incidents. We created two new addresses and conducted transfers between them. Within five minutes, we were subjected to an address poisoning attack. We encourage readers to verify this phenomenon themselves. Currently, the rate of losses due to poisoning attacks has increased more than eightfold compared to before the Fusaka upgrade.

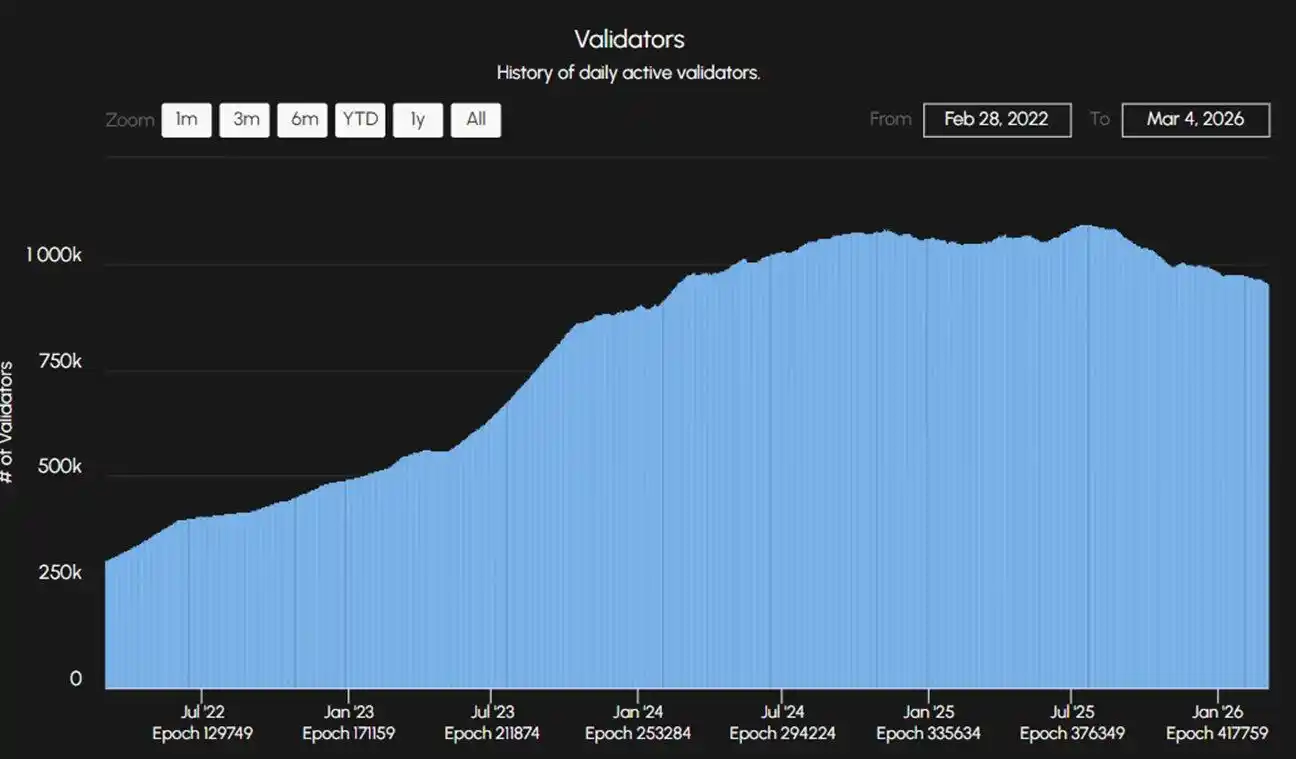

In addition, the increase in gas limit has negatively impacted Ethereum’s validator community, reducing tip income per unit of gas by 40%–50%. Lower yields will weaken staking demand and high-value transaction activity, further undermining institutional adoption. This flywheel has now begun to reverse.

Meanwhile, Ethereum continues to lose market share to Solana and its own Layer 2 networks.

· The number of Solana developers increased by 29% in 2025;

· Ethereum developer growth was only 6%;

· Talent is leaving the Ethereum ecosystem;

· Institutions such as Visa and Citigroup have chosen Solana for DeFi applications;

· The trading volume on Solana DEX has surpassed that of Ethereum by more than double.

During the dot-com bubble, Netscape and Nokia dominated the market for over a decade, but ultimately, Google and Apple reaped the greatest rewards. We believe Ethereum is in a similar position—we think Ethereum’s tokenomics have broken down, Tom Lee is trapped in his own stance, and the price of ETH will continue to fall.

Click to learn about the open positions at BlockBeats

Welcome to the official community of律动 BlockBeats:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia