On February 3, 2026, Vitalik Buterin made a statement on X.

This statement has caused a stir in the Ethereum community, comparable to the impact of his advocacy for a "rollup-centric" roadmap in 2020. In that post, Vitalik openly admitted, "The original vision of using Layer 2 as 'branded sharding' to solve Ethereum's scalability issues is no longer valid."

This single statement almost marked the end of Ethereum's mainstream narrative over the past five years. The once highly anticipated Layer 2 ecosystem, seen as a lifeline for Ethereum, is now facing its greatest legitimacy crisis since its inception. More direct criticism soon followed. In a post, Vitalik bluntly wrote: "If you create an EVM that can process 10,000 transactions per second, but its connection to L1 is achieved through a multisig bridge, then you are not scaling Ethereum."

Why did yesterday's lifeline become today's burden, ready to be discarded? This is not merely a shift in technological direction, but rather a ruthless struggle involving power, interests, and ideals. The story begins five years ago.

How Did Layer2 Become Ethereum's Lifeline?

The answer is simple: it's not a technical choice, but a survival strategy. Let's go back to 2021, when Ethereum was mired in the quagmire of becoming an "elitist chain."

The data doesn't lie: On May 10, 2021, the average Ethereum transaction fee reached a historical high of $53.16. During the peak of the NFT craze, gas prices even surged above 500 gwei. What does this mean? A regular ERC-20 token transfer could cost tens of dollars, and a single token swap on Uniswap could cost as much as $150 or more.

The DeFi Summer of 2020 brought unprecedented prosperity to Ethereum. The total value locked (TVL) surged from $700 million at the beginning of the year to $15 billion by the end, an increase of over 2100%. However, the cost of this prosperity was extreme network congestion. By 2021, when the NFT craze swept in, the minting and trading of blue-chip projects like Bored Ape Yacht Club further strained the network, with gas fees for a single NFT transaction often reaching hundreds of dollars. There were even cases where collectors were outbid on a Bored Ape for over 1,000 ETH in 2021 but ultimately gave up due to the high gas fees and complex transaction process.

At the same time, a challenger named Solana emerged unexpectedly. Its data was astonishing: tens of thousands of transactions per second, with transaction fees as low as $0.00025. The Solana community not only mocked Ethereum for its performance but even directly criticized Ethereum's bloated and inefficient architecture. The claim that "Ethereum is dead" became rampant, and anxiety filled the Ethereum community.

Against this backdrop, in October 2020, Vitalik formally proposed a vision in "An Rollup-Centric Ethereum Roadmap": positioning Layer2 as Ethereum's "branded shard." The core idea of this concept is that Layer2 processes a massive number of transactions off-chain, then packages and returns the compressed results to the mainnet. This theoretically enables infinite scalability while inheriting the security and censorship resistance of the Ethereum mainnet.

At that moment, the future of the entire Ethereum ecosystem was almost entirely hinged on the success of Layer2. From the Dencun upgrade in March 2024, which introduced EIP-4844 (Proto-Danksharding) to provide cheaper data availability specifically for Layer2, to various core development meetings, everything was paving the way for Layer2. After the Dencun upgrade, the cost of data publication for Layer2 dropped by at least 90%, and Arbitrum's transaction fees plummeted from about $0.37 to $0.012. Ethereum is striving to gradually push the L1 layer into the background, allowing it to quietly serve as a "settlement layer."

But why wasn't this bet settled?

Those "centralized databases" valued at $1.2 billion

If Layer2 solutions could truly achieve their original vision, they wouldn't be out of favor today. But the question is, what exactly did they do wrong?

Vitalik pointed out the critical issue in his article: the slow progress toward decentralization. Most Layer 2 solutions have not yet reached Stage 2—having a fully decentralized fraud or validity proof system that allows users to withdraw their assets permissionlessly in emergency situations. They are still controlled by centralized sequencers that manage transaction batching and ordering. Essentially, they are more like centralized databases disguised as blockchain.

The conflict between commercial reality and technological ideals is clearly exposed here. Take Arbitrum as an example: its development company, Offchain Labs, raised $120 million in a Series B funding round in 2021, achieving a valuation of $1.2 billion. The investment was led by top-tier institutions such as Lightspeed Venture Partners. However, to this day, this giant, which holds over $15 billion in total value locked (TVL) and accounts for about 41% of the Layer2 market, remains stuck in Stage 1.

The story of Optimism is equally intriguing. This project, led by Paradigm and Andreessen Horowitz (a16z), completed a $150 million Series B funding round in March 2022, with a total funding amount reaching $268.5 million. In April 2024, a16z even privately purchased $90 million worth of OP tokens. However, despite such strong financial backing, Optimism has also only reached Stage 1.

The rise of Base reveals another dimension of the issue. As a Layer 2 solution launched by Coinbase, Base quickly became a market favorite after its mainnet launch in August 2023. By the end of 2025, Base's TVL had reached $4.63 billion, accounting for 46% of the entire Layer 2 market and surpassing Arbitrum to become the Layer 2 with the highest DeFi TVL. However, Base is less decentralized, as it is entirely controlled by Coinbase, making its technical architecture more similar to a centralized sidechain.

The story of Starknet is even more ironic. This Layer 2 solution, built on ZK-Rollup technology and developed by Matter Labs, has raised a total of $458 million in funding, including a $200 million Series C round in November 2022 led by Blockchain Capital and Dragonfly. However, the price of its token, STRK, has dropped by 98% from its historical high, with a current market capitalization of about $283 million. According to on-chain data, the daily protocol revenue it generates is not even enough to cover the operating costs of a few servers. Moreover, its core nodes remain highly centralized, and it is not until mid-2025 that it is expected to reach Stage 1 of decentralization.

Some project teams have even privately admitted that they may never achieve full decentralization. Vitalik cited a case in a post: a certain project claimed that they would not further decentralize because "regulatory requirements from their clients necessitated that they retain ultimate control." This completely angered Vitalik, who responded bluntly and without hesitation:

"This might be the right thing to do for your customers. But it's obvious that if you do this, you're not 'scaling Ethereum'."

This comment effectively condemns almost all projects that claim to be Ethereum L2 solutions but refuse to embrace decentralization. Ethereum seeks a reincarnation that can extend decentralization and security into broader realms, not a group of projects that wear the Ethereum name while practicing centralization in reality.

A deeper issue lies in the irreconcilable tension between decentralization and commercial interests. A centralized sequencer means the project team can control MEV (Maximum Extractable Value) revenue, respond more flexibly to regulatory requirements, and iterate products more quickly. In contrast, full decentralization means giving up these controls and transferring power to the community and validator network. For projects funded by venture capital and under pressure to grow, this is a difficult choice.

If Layer 2 truly achieves full decentralization, will they still fall out of favor? The answer might still be yes. Because Ethereum itself is changing.

When the mainnet is faster and cheaper than the sidechain

Why is Ethereum less in need of Layer 2 for scaling now?

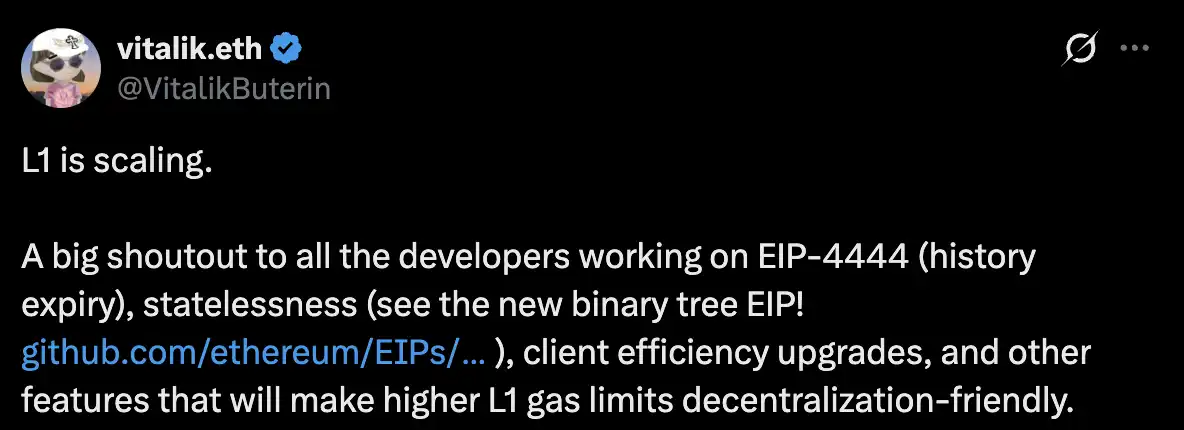

As early as February 14, 2025, Vitalik released a key signal. He published an article titled "Reasons for a Higher L1 Gas Limit Even in an L2-Dominant Ethereum," clearly stating, "L1 is scaling." At the time, this statement sounded more like a reassurance to Ethereum mainnet purists, but in retrospect, it was actually the rallying cry marking the Ethereum mainnet's renewed competition with Layer 2 solutions.

Over the past year, the expansion of Ethereum's L1 has far exceeded everyone's expectations. Technological breakthroughs have come from multiple dimensions: EIP-4444 has reduced the storage requirements for historical data, stateless client technology has made node operations more lightweight, and most importantly, the Gas Limit has continued to increase. At the beginning of 2025, Ethereum's Gas Limit was 30 million, but by mid-year, it had risen to 36 million, representing a 20% increase. This is the first significant increase in Ethereum's Gas Limit since 2021.

But this is just the beginning. According to the Ethereum core developers' roadmap, two major hard fork upgrades are planned for 2026. The "Glamsterdam" upgrade will introduce perfect parallel processing capabilities, and the gas limit will surge from 60 million to 200 million, an increase of over three times. The "Heze-Bogota" fork will add the FOCIL (Fork-Choice Enforced Inclusion Lists) mechanism, further improving block-building efficiency and censorship resistance.

The Fusaka upgrade, completed on December 3, 2025, has already demonstrated the power of L1 scaling to the market. Post-upgrade, Ethereum's daily transaction volume increased by approximately 50%, and the number of active addresses rose by about 60%. The 7-day moving average of daily transactions reached a historical high of 1.87 million, surpassing records from Ethereum's DeFi peak in 2021.

The results are astonishing: transaction fees on the Ethereum mainnet have dropped to extremely low levels. In January 2026, the average Ethereum transaction fee fell to $0.44, a decrease of over 99% compared to the peak of $53.16 in May 2021. During off-peak hours, the cost of a single transaction often drops below $0.10, sometimes as low as $0.01, with gas prices as low as 0.119 gwei. This level is already approaching that of Solana, and the cost advantage of Layer2 solutions is being rapidly eroded.

Vitalik did a detailed calculation in his February article. He assumed an ETH price of $2500, a gas price of 15 gwei (a long-term average), and a demand elasticity close to 1 (i.e., doubling the gas limit would halve the price). Under these assumptions:

Anti-censorship requirement: Currently, it costs about 120,000 gas (approximately $4.50) to force a censored L2 transaction through L1. To reduce this cost to less than $1, L1 needs to scale by 4.5 times.

Cross-L2 asset transfer: Currently, withdrawing from one L2 to L1 requires about 250,000 gas, and then depositing into another L2 requires 120,000 gas, for a total cost of $13.87. With ideal optimization, it would only require 7,500 gas, costing $0.28. To achieve the $0.05 target, a 5.5x improvement is needed.

Mass exit scenarios: Taking Sony's Soneium as an example, PlayStation has approximately 116 million monthly active users. If an efficient exit protocol (7,500 gas per user) is used, the current Ethereum network could just support emergency exits for 121 million users within one week. However, if multiple applications of this scale are to be supported, the Layer 1 (L1) would need to scale by about 9 times.

And these extended goals are gradually being realized by 2026. Technological advancements are fundamentally changing the game. If L1 itself can become fast and inexpensive, why would users still tolerate the cumbersome cross-chain bridges, complex interaction experiences, and potential security risks of Layer2?

Security issues with cross-chain bridges are not a cause for undue worry—they are a real and pressing concern. In 2022, cross-chain bridges became a major target for hackers. In February, the Wormhole bridge was hacked, resulting in a loss of $325 million. In March, the Ronin bridge suffered the largest DeFi attack in history, with $540 million stolen. Other bridge protocols, such as Meter and Qubit, were also successively compromised. According to Chainalysis, the total value of stolen cryptocurrency from cross-chain bridges in 2022 reached $2 billion, accounting for the majority of all DeFi-related losses that year.

Liquidity fragmentation is another pain point. As the number of Layer 2 solutions rapidly increases, DeFi protocols' liquidity is spread across dozens of different chains, leading to increased trade slippage, reduced capital efficiency, and a worsened user experience. A user who wants to move assets between different Layer 2 networks must go through a complex bridging process, wait for long confirmation times, and bear additional fees and risks.

This leads us to the next, and perhaps harshest, question: What should those Layer2 projects that raised massive funds and issued tokens do now?

Valuation Bubbles and Ghost Cities

Where did the money for Layer2 go?

In recent years, the Layer 2 space has felt more like a massive financial game than a technological revolution. Venture capital firms have been waving their checks, pushing the valuations of one L2 project after another to astonishing heights. zkSync has raised a total of $458 million, while Offchain Labs, the company behind Arbitrum, is valued at $1.2 billion. Optimism has raised $268.5 million, and Starknet has raised $458 million. Behind these figures are top-tier venture capital firms such as Paradigm, a16z, Lightspeed, and Blockchain Capital.

Developers are enthusiastic about "nesting" different L2s, building complex DeFi Legos to attract more liquidity and airdrop hunters. However, real users are gradually worn out by the cumbersome cross-chain operations and high hidden costs.

A harsh reality is that the market is becoming highly concentrated at the top. According to data from crypto research firm 21Shares, the top three Layer 2 (L2) platforms—Base, Arbitrum, and Optimism—have already captured nearly 90% of the trading volume. Base, leveraging the traffic advantages and user base of Coinbase, experienced explosive growth in 2025, with its Total Value Locked (TVL) surging from $10 billion at the beginning of the year to $46.3 billion by year-end. Its quarterly trading volume reached $590 billion, representing a 37% quarter-over-quarter increase. Arbitrum holds the second position with a TVL of approximately $190 billion, followed closely by Optimism.

However, beyond the top tier, most Layer 2 (L2) projects have seen their actual user numbers rapidly plummet to near-freezing levels after the initial hype and airdrop expectations faded, turning them into literal "ghost towns." Starknet is the most typical example. Although its token price has dropped by 98% from its peak, its price-to-earnings ratio remains in an extremely inflated range when compared to its very low daily active user count and transaction fee revenue. This indicates a massive gap between the market's expectations for its future and its current ability to generate real value.

Even more ironically, when Layer 2 fees dropped significantly due to EIP-4844, the data availability fees they paid to the L1 also plummeted, which in turn reduced Ethereum's L1 fee revenue. In January 2026, an analysis pointed out that the Dencun upgrade caused a large number of transactions to shift from L1 to cheaper L2, becoming one of the main reasons for Ethereum network fees dropping to their lowest level since 2017. While Layer 2 is reducing its own costs, it is also draining the economic value of L1.

In its 2026 Layer2 Outlook Report, 21Shares predicts that most Ethereum Layer2 solutions may not survive until 2026. The market will undergo a harsh consolidation, with only projects offering high performance, true decentralization, and unique value propositions ultimately succeeding.

This is exactly the true intention behind Vitalik's recent criticism. He aims to burst the bubble of self-congratulatory infrastructure development and pour a bucket of cold water on this unhealthy market. If a Layer 2 solution cannot offer more interesting and valuable features than a Layer 1, it will ultimately become nothing more than a costly transitional product in Ethereum's development history.

Ethereum is reclaiming its sovereignty.

Vitalik's latest proposal has outlined a new path for Layer 2: moving beyond scalability as the sole selling point and instead exploring functional value-adds that Layer 1 is either unable or unwilling to provide in the short term. He specifically highlighted several directions: privacy (enabling private on-chain transactions via zero-knowledge proofs), application-specific efficiency optimizations (such as for gaming, social networks, and AI computation), ultra-fast transaction finality (in milliseconds rather than seconds), and the exploration of non-financial use cases.

In other words, the role of Layer 2 will shift from being an extension of Ethereum to becoming diverse, specialized plugins. They will no longer be the sole savior for scaling, but rather a functional expansion layer within the Ethereum ecosystem. This represents a fundamental shift in positioning, and also a return of power—the core value and sovereignty of Ethereum will be re-anchored on the L1.

Vitalik also proposed a new framework: viewing Layer 2 as a spectrum, rather than a binary classification. Different Layer 2 solutions can have varying trade-offs in terms of decentralization, security guarantees, and functional features. The key is to clearly communicate to users what specific guarantees they provide, rather than all claiming to be "scaling Ethereum."

This reckoning has already begun. Layer2 projects that have been propped up by high valuations but lack real daily active users are now facing their final judgment. Projects that can identify their unique value propositions and genuinely achieve decentralization may survive in the new landscape. Base might continue to leverage Coinbase's traffic advantages and its ability to bring in Web2 users to maintain its lead, but it must address criticisms regarding its insufficient level of decentralization. Arbitrum and Optimism need to accelerate their Stage 2 development to prove they are more than just centralized databases. ZK-Rollup projects like zkSync and Starknet must not only demonstrate the unique value of their zero-knowledge proof technologies but also significantly improve user experience and foster ecosystem growth.

Layer2 has not disappeared, but the era in which it was seen as Ethereum's sole hope has come to an end. Five years ago, when competitors like Solana pushed Ethereum into a corner, Ethereum placed its scalability hopes on Layer2 and even restructured its entire technical roadmap around it. Five years later, it has realized that the best scalability solution is to make itself stronger.

This is not a betrayal, but growth. Those Layer2 projects that cannot adapt to this evolution will become the cost. When the Gas Limit surges to 200 million by the end of 2026, when Ethereum L1 transaction fees stabilize at just a few cents or even lower, and when users realize they no longer need to endure the complexity and risks of cross-chain bridges, the market will vote with its feet. Projects that once boasted sky-high valuations but failed to deliver real value to users will be forgotten by history in this process of natural selection.

Click to learn about BlockBeats' job openings.

Welcome to join the official Lulin BlockBeats community:

Telegram Subscription Group:https://t.me/theblockbeats

Telegram discussion group:https://t.me/BlockBeats_App

Official Twitter account:https://twitter.com/BlockBeatsAsia