Author: David, Deep潮 TechFlow

Last Thursday, a new stock with the ticker VCX was listed on the NYSE.

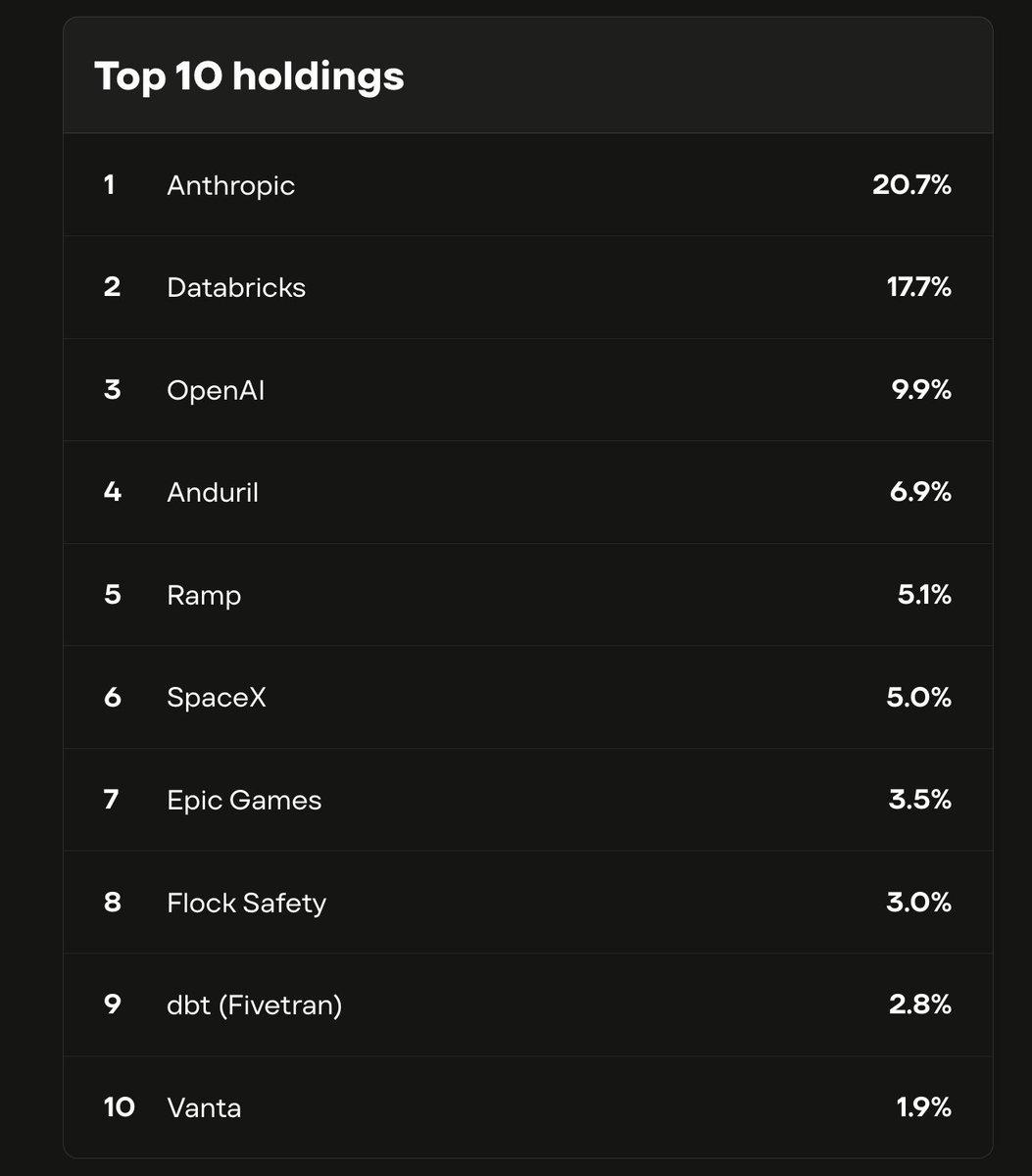

It is actually a fund that holds shares in companies such as Anthropic, OpenAI, and SpaceX. Anthropic accounts for 21% of the fund, and OpenAI accounts for 10%.

These companies have one thing in common: they are not publicly traded, so ordinary investors cannot buy their shares.

VCX is one of the very few products available today that allows retail investors to indirectly hold shares in Anthropic.

Its net asset value was $19 per share. On its first day of trading, it opened at $42, surged to $125 intraday, and closed at $76. On the fourth trading day, it reached an intraday high of $315 and triggered circuit breakers twice.

Four days, up from 19 to 315.

Investors are effectively buying this fund at a price 16 times its actual asset value—not because the fund manager is exceptionally skilled, but because it contains Anthropic.

A month ago, Anthropic raised $30 billion at a $380 billion valuation, making it the second-largest funding round globally this year. Its annualized revenue is $14 billion. However, it is not publicly traded and has no stock ticker—you won’t find it in any brokerage’s search bar.

If you can't buy the real thing, go for the shadow. VCX is currently the shadow of Anthropic—or the shadow of AI FOMO.

Why is it so expensive?

VCX is not a fund in the traditional sense.

With a traditional mutual fund, if you think it's expensive, you can wait for it to drop, because the fund manager can issue additional shares—supply is flexible. VCX is a closed-end fund; once listed, the number of shares is fixed and will not increase.

More importantly, the vast majority of shares cannot be sold. Investors who purchased before February 20 have their shares locked for six months and won’t be able to trade until September. With over 100,000 investors in VCX, only a very small portion of shares are currently available for trading.

This means there are many buyers but very few shares available. A small amount of buying pressure can drastically push the price up.

So that 16x premium is really pricing in "how many people want to access Anthropic and how narrow the door is." But this hunger isn't something VCX created on its own.

Chart: Top 10 Holdings of the Fundrise VCX Fund

Over the past decade, the tech industry has undergone a structural shift: the best companies are going public later—or not at all.

When Facebook went public in 2012, it was valued at $104 billion—a staggering figure at the time. Today, Anthropic’s private valuation is more than three times that amount, yet it hadn’t even announced a clear IPO plan before.

OpenAI is valued at $500 billion but has not gone public. Rumors about SpaceX preparing for an IPO have circulated for over a year, yet no official date has been confirmed.

Ten years ago, a company of this size would have already gone public on the NYSE. Now, it doesn’t need to. The private market can provide nearly unlimited capital without the pressure of quarterly earnings reports or the scrutiny of retail investors and short sellers.

For founders, this is a rational choice. For retail investors, it means the fastest-growing group of companies in history, visible only through glass.

VCX was originally scheduled to list on March 9, but was delayed by ten days due to the war in Iran. During those ten days, nothing changed—Anthropic’s price neither rose nor fell, and the fund’s holdings remained untouched. Yet the delay itself cultivated an additional ten days of anticipation.

On the day it finally listed, all the demand that had been suppressed for ten days squeezed through an extremely narrow channel.

Not all shadows are valuable.

There are other ways to gain exposure to private company stocks besides the VCX fund.

But before discussing these avenues, there's a more fundamental question: Anthropic is not publicly traded—how did a publicly traded fund acquire its shares?

The answer is backdoor.

Large private companies typically raise funding rounds every few months, progressing from Series A to Series G, with each round bringing in new investors. Last month, Anthropic closed a $30 billion Series G round, with a long list of institutional participants including GIC, Sequoia, and Goldman Sachs. These rounds are usually open only to institutional investors, with minimum investment thresholds often starting in the tens of millions of dollars.

But there is a second path.

Just because a company is not publicly listed doesn't mean its shares can't be traded privately. Early employees and angel investors hold shares, and some of them want to cash out early. This has given rise to a secondary market for private companies—private and opaque, but with real transactions taking place.

Fundrise began buying on both fronts in 2022, when valuations of private tech companies had just plunged, making them inexpensive. Over four years, they built a portfolio including Anthropic, OpenAI, and SpaceX, then packaged it into VCX and listed it on the NYSE, allowing ordinary investors to buy it like a stock.

In the same month, at least three other similar funds were trading on the NYSE, all selling the same concept:

We’re selling you what was bought through the back door, right through the front door.

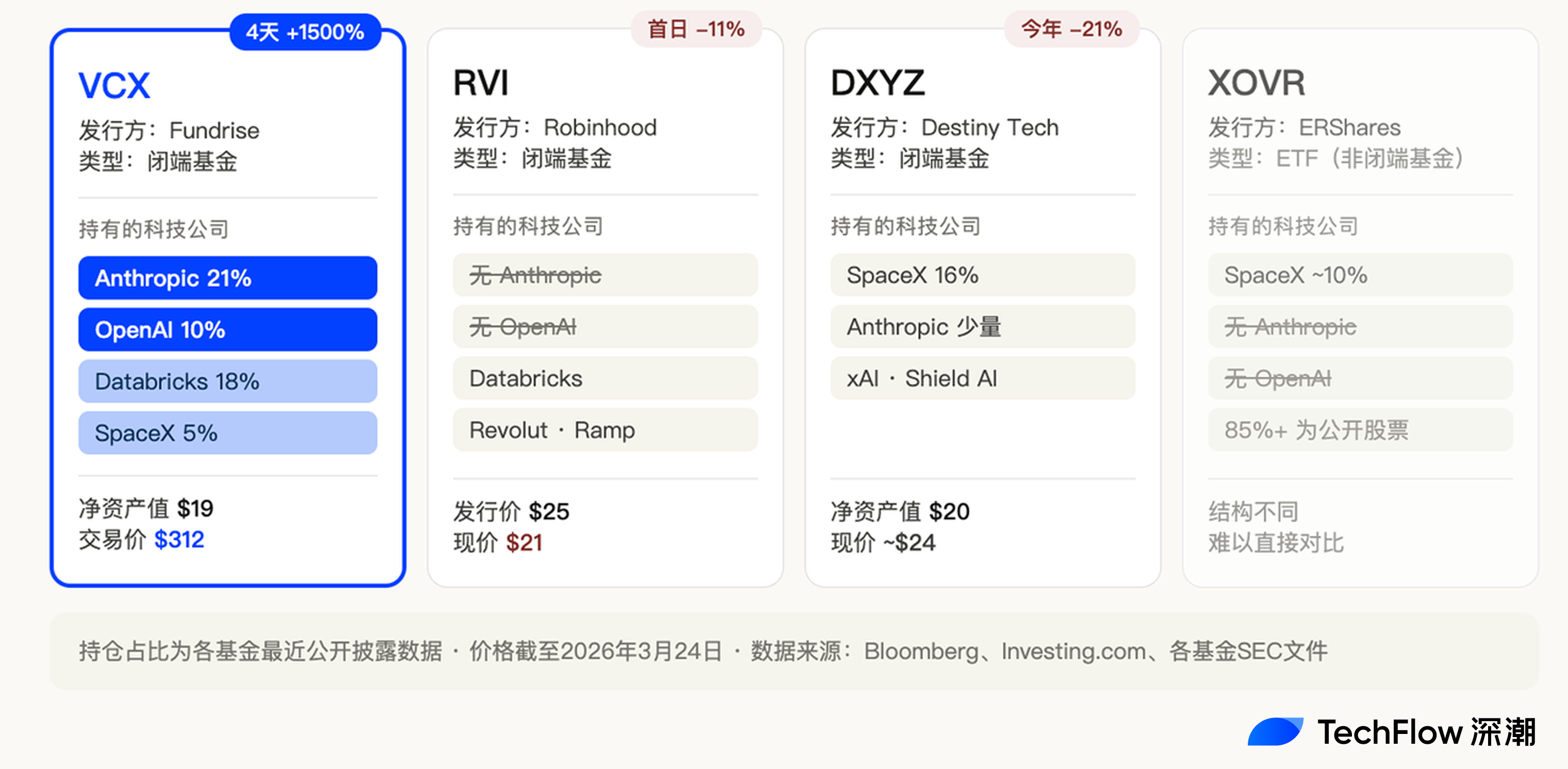

Robinhood launched a fund called RVI, which listed on March 6 at an offering price of $25. Its holdings include well-known private companies such as Databricks, Revolut, and Ramp. On its first day of trading, the fund fell 11%, closing at $21.

Destiny Tech100, ticker DXYZ, went public in 2024 and is among the pioneers in this sector. It holds a 16% weighting in SpaceX and only recently, in February this year, gained indirect exposure to Anthropic. The stock is currently trading around $24.

There is also XOVR, the first ETF approved to directly hold equity in private companies, with SpaceX accounting for approximately 21%.

Four funds, similar in structure and concept, trading on the same exchange—yet their fates are entirely different.

VCX rose 1,500% over four days. RVI broke below its offering price on its first day. DXYZ remained modest.

VCX holds 21% of Anthropic and 10% of OpenAI. RVI has no exposure to either Anthropic or OpenAI. DXYZ’s exposure to Anthropic was recently added and is minimal.

This indicates that, at least for now, the market is not competing for shares in private companies—it’s competing for Anthropic.

The closer you are to them, the more valuable you are.

That’s where Robinhood’s RVI falls short. Databricks and Revolut are certainly good companies, but clearly, right now, they’re not the names people are willing to pay a 16x premium for.

Shadows also have an expiration date.

What are people betting on when they buy VCX at $312?

They’re betting that someone will still be willing to pay a higher price for Anthropic before the door closes.

However, this door will not remain closed forever.

VCX has over 100,000 investors, the vast majority of whom have had their shares locked for six months. The lock-up period ends on September 19, at which point a large volume of shares will enter the market, causing supply to shift from extremely scarce to abundant overnight.

VCX trades at a 16x premium partly because it includes Anthropic, and partly because the available supply is so limited. Once the lock-up period ends, the second factor will disappear.

There is another larger variable.

Anthropic, OpenAI, and SpaceX are all rumored to be planning IPOs in the second half of 2026 through 2027. Anthropic recently raised $30 billion last month, valuing the company at $380 billion, and has already hired the Silicon Valley law firm Wilson Sonsini to prepare for its IPO. SpaceX’s CFO has been engaging with investors on IPO matters since late last year, with a target of mid-year this year.

Once the real thing is listed, the shadow becomes worthless.

If you can simply type Anthropic’s stock symbol directly into your brokerage’s search box, why pay a 16x premium to buy a fund that indirectly holds it?

For example, as mentioned earlier, when DXYZ first launched in 2024, its price surged dramatically; later, as SpaceX’s IPO was delayed and the hype faded, its stock price dropped by more than half from its peak.

Therefore, VCX investors are experiencing a classic countdown.

What they paid 16 times the price for isn't equity in Anthropic—it's a ticket with an expiration date. When the door opens depends on when Anthropic decides to go public.

Before that, the premium was sustained by scarcity; after that, the premium dropped to zero.

But the very existence of shadow stocks is not coincidental.

Each wave of technological innovation generates the same anxiety: you can’t buy the most important companies. In the 2000s, before Google’s IPO, Goldman Sachs employees fiercely competed for internal allocations. In the 2020s, it was SpaceX—Silicon Valley’s secondary market intermediaries suddenly became the most sought-after connections.

Now it's AI's turn.

And this time, the anxiety runs deeper: Anthropic and OpenAI may not yet be profitable, but they are rewriting the rules. Due to AI’s impact, SaaS stocks have crashed, cybersecurity stocks have crashed, and IBM lost $31 billion in a single day.

Investors don’t just see “this company is very profitable”—they see “if I’m not on its side, I might be on the side getting crushed by it.”

The 16x premium on VCX isn't pricing just a fund—it's pricing the anxiety itself.

Tickets expire, and premiums fade. But as long as AI continues to accelerate and the most valuable companies remain closed, someone will be willing to pay irrational prices for shadows.

It’s not about the shadow price—it’s the feeling of being locked out that’s too costly.