On April 28, the UAE announced its withdrawal from OPEC and OPEC+, effective May 1, ending nearly 60 years of membership. On the same day, the Brent June futures contract surged $1.11 to $109.34 per barrel. This is the story currently being reported in financial media. However, the Brent July futures contract rose only $1.08 to $102.77, trading $6.57 lower than June. When these two figures are placed side by side, they tell a different story.

The UAE is OPEC's third-largest oil producer, after Saudi Arabia and Iraq. Its position within OPEC has long been awkward, as its production capacity has expanded faster than its quota updates. In 2023, dissatisfied with its low quota, it delayed the entire OPEC+ output increase agreement for several months. This time, its direct departure has been interpreted by media outlets worldwide as the greatest challenge yet to Saudi Arabia's leadership.

Following the UAE's announcement, market sentiment on oil prices split into two camps: spot prices surged, while forward months remained unchanged. The gap between these two pricing regimes reflects the market's true response to the "UAE exit."

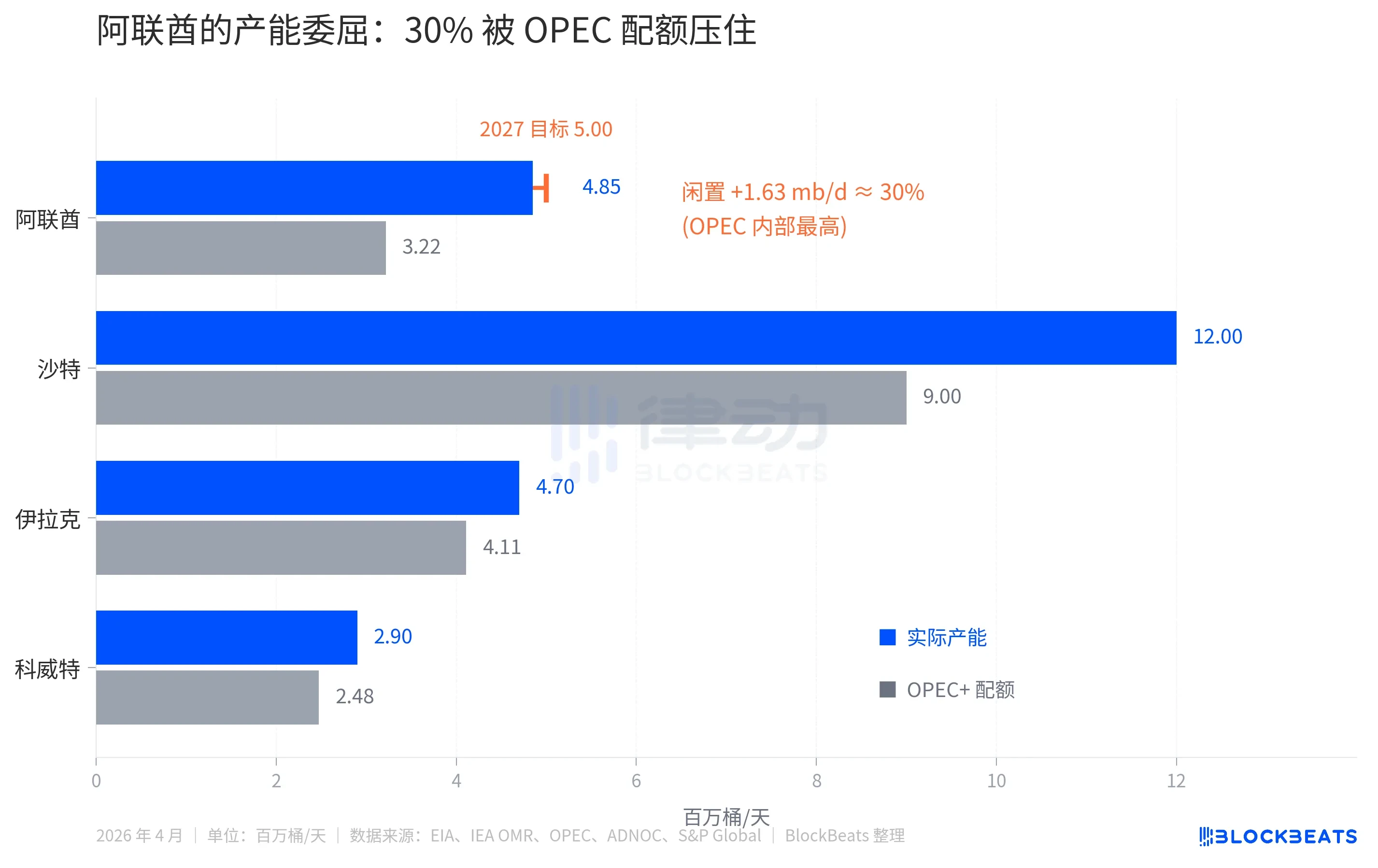

Actual production capacity is 1.5 times the OPEC quota.

According to EIA data, the UAE’s current actual production capacity is 4.85 mb/d (million barrels per day), but its OPEC+ quota has recently been capped at around 3.22 mb/d for 2025. The difference of 1.63 mb/d represents approximately 30% of its capacity being artificially idled.

A similar gap exists in Saudi Arabia at around 25% (actual production of 12 mb/d versus quota of 9 mb/d), while in Iraq and Kuwait it is only 10–15%. Among OPEC’s 13 members, the UAE is the most constrained.

There is another layer of dissatisfaction. The UAE’s national oil company, ADNOC, is accelerating its investments. According to ADNOC’s announcement, its capital expenditure budget for 2023–2027 is $150 billion, and its production target of 5.0 million barrels per day has been moved forward from 2030 to 2027. While investing heavily to expand capacity, it is constrained by OPEC quotas that prevent it from selling more, resulting in daily revenue losses measured in millions of barrels.

This is the financial rationale the UAE must follow. However, viewed in isolation, economic common sense suggests that a member country with 30% idle capacity shedding its quota would increase oil production. Increased production equals additional supply, which is bearish for oil prices.

Crude oil futures contango

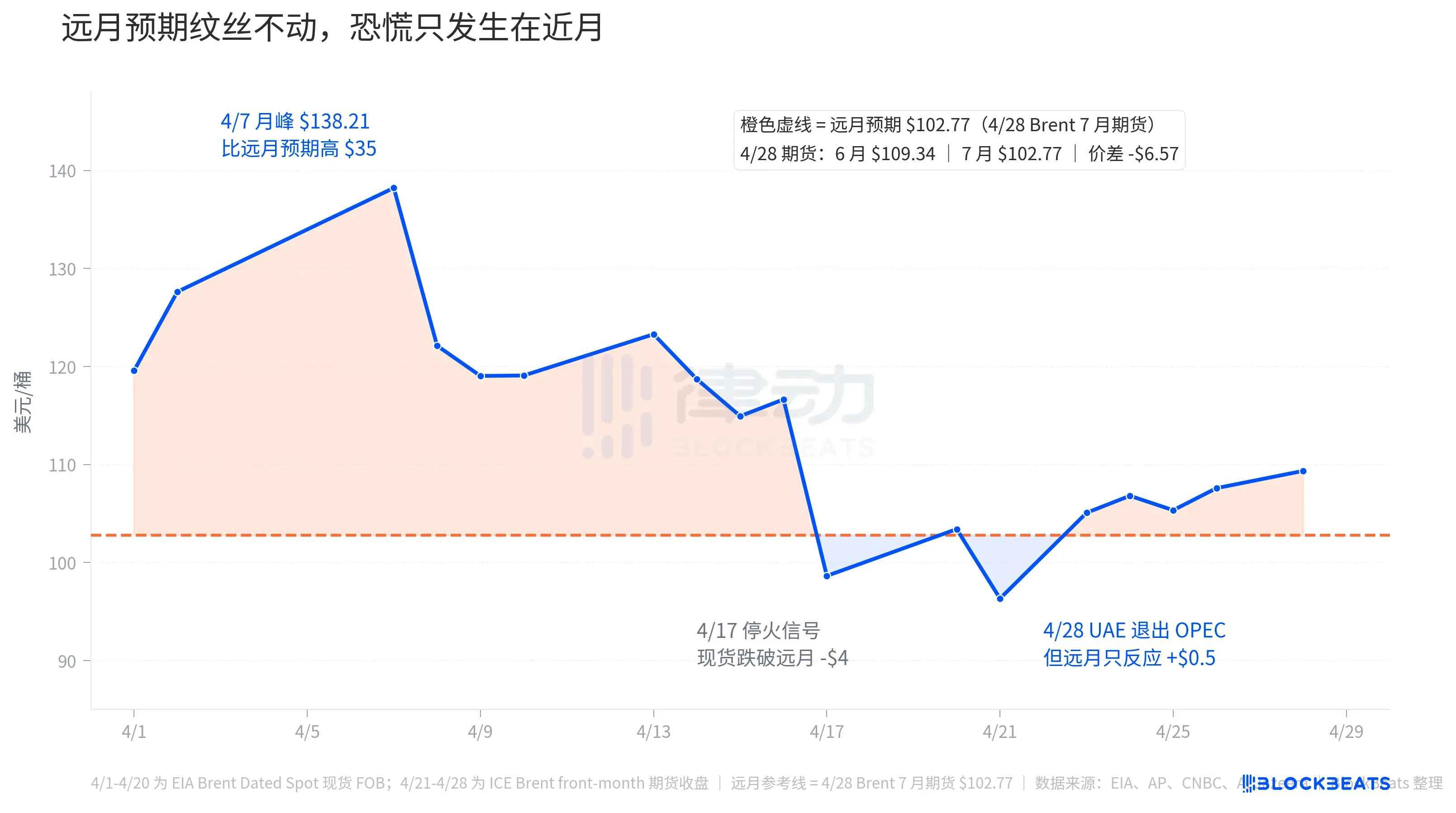

On April 28, mainstream media headlines read "Brent surges." But only the front-month contract surged; the orange dashed line representing long-term expectations remained virtually unchanged throughout April.

On April 28, the Brent futures close price for the June contract (front-month, equivalent to the price of receiving oil immediately) was $109.34, while the July contract was priced at $102.77, creating a spread of $6.57. This futures curve is in deep backwardation, with nearby months elevated and longer-dated months relatively cheaper.

The futures curve is not speculation—it reflects actual contract prices. It tells you that the market is currently willing to pay more for oil, but less for oil months from now. The underlying logic is simple: the market expects the Hormuz crisis to be resolved, OPEC’s supply coordination to loosen, and the UAE’s 30% spare capacity to enter the market.

When viewed in the context of the entire month of April, the situation becomes clearer. According to EIA Brent Dated spot data, the spot price surged to $138.21 per barrel on April 7—the monthly peak—$35 higher than the forward-month expectation of $102.77 on April 28. This $35 premium represented the market’s panic valuation for immediate access to oil. At the time, the U.S.-Iran conflict had entered its ninth week, with transit through the Strait of Hormuz nearly completely halted, reducing Middle Eastern crude oil shipments—approximately 20 million barrels per day—to near zero.

On April 17, a ceasefire signal emerged, causing Brent spot prices to drop to $98.63 that day, nearly $4 below forward-month expectations. The market briefly believed the conflict was ending, resulting in the unusual situation where "future oil prices" became higher than "current oil prices." This anomaly lasted only a few days; on April 21, Brent fell to its monthly low of $96.32, then rebounded again on April 23.

On April 28, the UAE announced its withdrawal, causing Brent June to rise $1.11 to $109.34, reasserting a $6.57 premium over the far-month expectation. However, this is only a fraction of the panic premium seen in early April. In other words, the market’s panic response to the “UAE withdrawal” was far smaller than its reaction to the Hormuz crisis.

The far-month curve puts it more directly. On the day the UAE announced its exit, the July futures contract rose only $1.08 to $102.77, nearly matching the June contract’s gain. This suggests the market views the UAE’s exit as having near-zero impact on medium-term oil prices—neither bullish nor bearish. The short-term spike was driven by headline noise combined with Hormuz-related sentiment.

The largest exit in the OPEC exodus

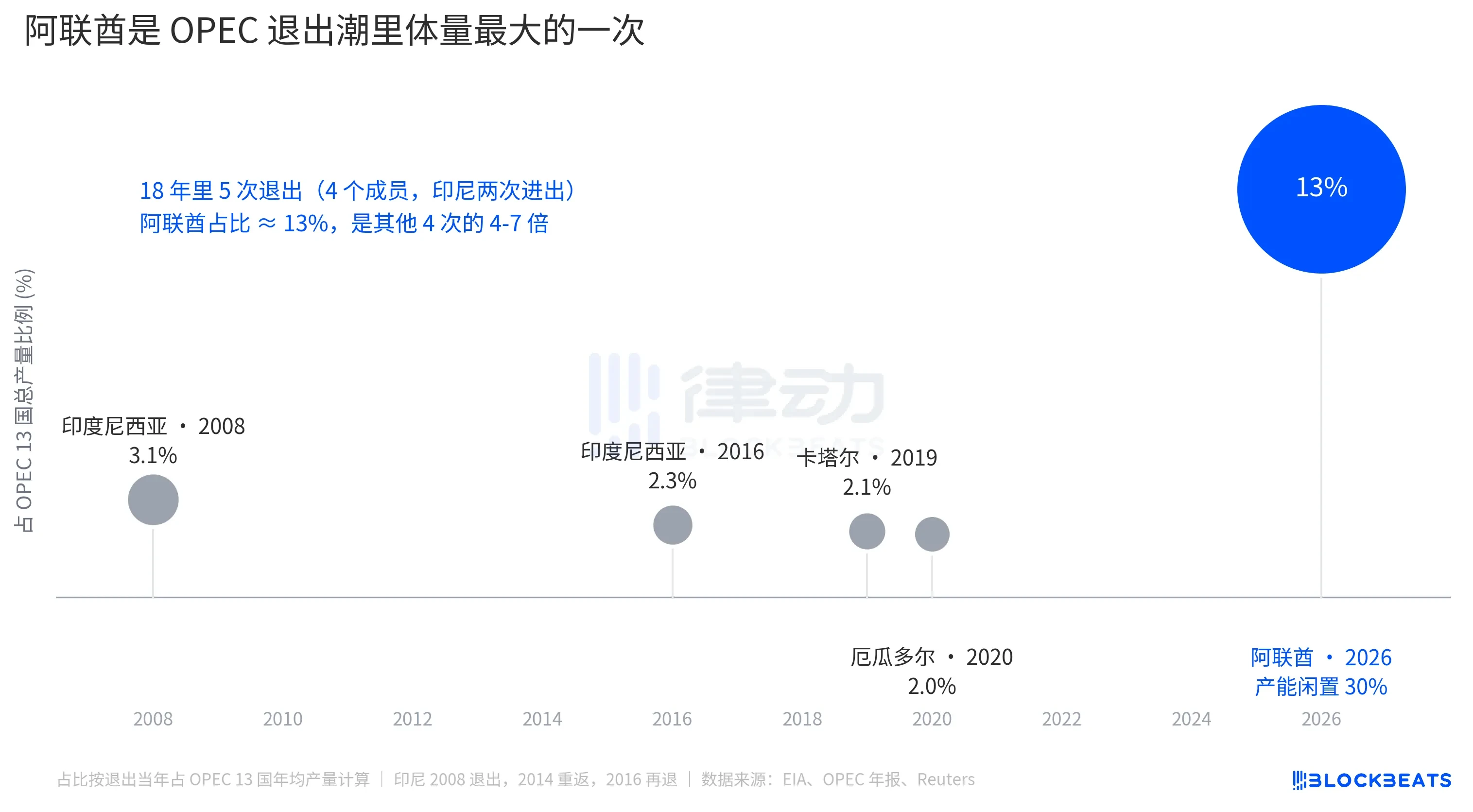

Indonesia left for the first time in 2008 (returned in 2014, left again in 2016), Qatar exited in 2019 to focus on LNG, and Ecuador withdrew in 2020 due to fiscal pressures. At the time of each of these four exits, the departing members accounted for 2–3.1% of OPEC’s total production. Each departure was interpreted as an isolated incident, and OPEC’s market share showed no significant decline following any of them.

The UAE accounts for 13%. A single exit exceeds 1.5 times the total of all exits over the past 18 years.

But when it comes to oil pricing, scale does not equate to influence. The 13% figure must be absorbed within Saudi Arabia’s leadership framework of OPEC discipline; Saudi Arabia still has approximately 25% of spare capacity available to offset the loss, and production quotas of other OPEC+ members can also be adjusted. The market has not interpreted “OPEC losing 13% of its volume” as “a future surge in oil prices.”

The real structural impact occurs at another level: OPEC’s role as a “price regulator” is further weakened. According to IEA estimates, OPEC+’s total spare capacity in early 2026 will be around 4–5 million barrels per day (mb/d), with the UAE contributing approximately 0.85 mb/d. After the UAE’s departure, the spare capacity of the remaining 13 OPEC countries will shrink to roughly 1 mb/d. This represents the “ammunition” available to the market in the event of future supply shocks—1 mb/d is only enough to cover about 1% of global demand.

So the far-month futures rose by $1—not because the UAE producing a few more barrels of oil would lower oil prices, but because OPEC’s ability to act as a price stability anchor has been further weakened.

Mainstream reports have conflated the UAE’s exit with the Hormuz price surge, making it appear as if OPEC’s dissolution is driving oil prices higher. The futures curve, however, separates the two events. In early April, Brent spot prices briefly exceeded those of distant months by $35—a Hormuz risk premium. By April 28, the near-far spread had narrowed to just $6.57, reflecting the combined impact of the UAE’s exit and media noise. The market’s true pricing of the UAE event is hidden in the nearly unchanged distant-month curve.