Written by:Oluwapelumi Adejumo

Compiled by: Saoirse, Foresight News

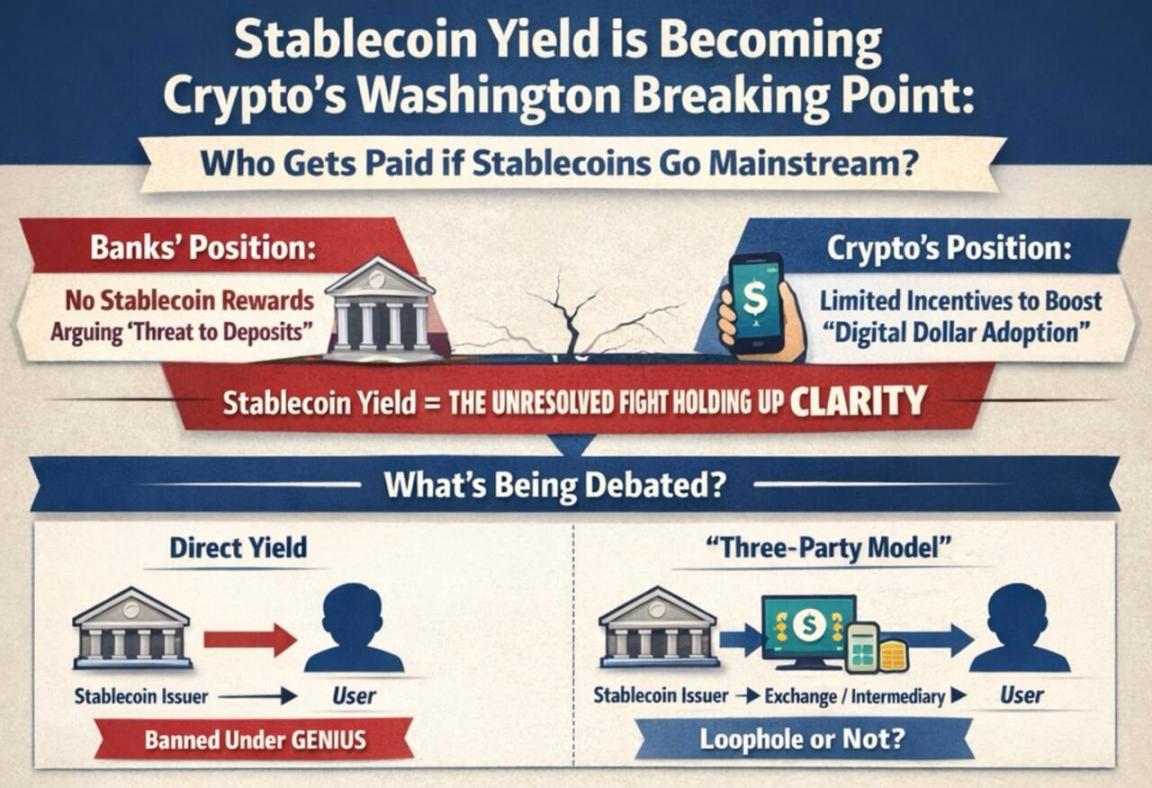

Legislative efforts, backed by the president, aimed at establishing more comprehensive regulatory rules for the U.S. cryptocurrency market are nearing political deadlines in Congress. Meanwhile, the banking industry is pressuring lawmakers and regulators to prohibit stablecoin providers from offering yields similar to bank deposit interest.

This博弈 has become one of the most central unresolved issues in Washington’s crypto agenda. The core debate centers on whether dollar-pegged stablecoins should focus solely on payment and settlement functions, or whether they can also incorporate investment features that compete with bank accounts and money market funds.

The Senate's market structure bill, titled the CLARITY Act, has stalled due to failed negotiations over so-called "stablecoin yields."

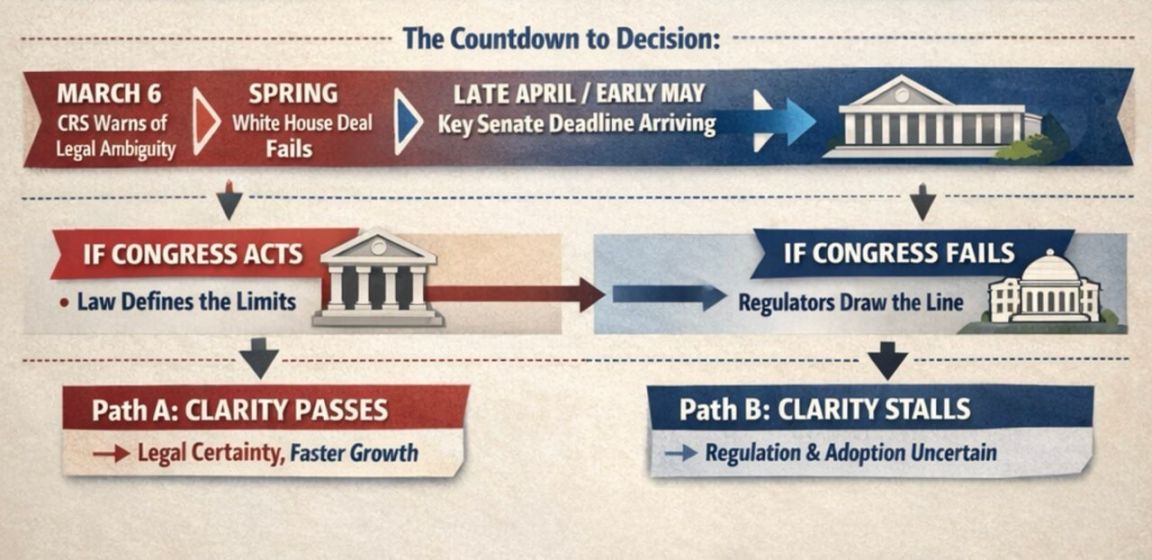

Industry insiders and lobbyists say that late April to early May will be the practical window to advance the bill if it is to have a realistic chance of passing before the election calendar tightens.

The Congressional Research Service has intensified the legal dispute.

The Congressional Research Service's definition of this issue is narrower than the scope of public debate.

In a report on March 6, the Congressional Research Service noted that the GENIUS Act prohibits stablecoin issuers from directly paying yields to users, but does not clearly determine the legality of what it calls the "third-party model," in which intermediaries such as exchanges operate between issuers and end users.

The Congressional Research Service stated that the bill does not clearly define "holder," leaving room for debate over whether intermediaries can still pass on economic benefits to their customers. This ambiguity is precisely why the banking industry hopes Congress will clarify it within a broader market structure bill.

Banks believe that even limited yield incentives could make stablecoins a strong competitor to bank deposits, particularly impacting regional and community banks.

However, crypto companies believe that incentives tied to payments, wallet usage, or network activity can help the digital dollar compete with traditional payment channels and potentially enhance its standing in mainstream finance.

This disagreement also reflects differing views on the future role of stablecoins.

The infographic shows that as the usage of the digital dollar expands, banks and crypto companies are sharply divided over who should receive the yields from stablecoins.

If lawmakers primarily view stablecoins as payment tools, the rationale for imposing stricter limits on associated incentives becomes stronger. Conversely, if lawmakers see them as part of a significant transformation in how value flows through digital platforms, the case for supporting limited incentives is more compelling.

The Banking Association has urged lawmakers to close what they call a "regulatory loophole" before these reward mechanisms become more widespread. Banks argue that allowing idle balances to earn rewards could prompt depositors to move their funds out of banks, thereby weakening the core source of funding banks rely on to lend to households and businesses.

Standard Chartered Bank estimated in January that stablecoins could withdraw approximately $500 billion in deposits from the U.S. banking system by the end of 2028, with smaller banks facing the greatest pressure.

The infographic compares why banks and cryptocurrencies are focused on the stablecoin bill, highlighting deposit outflows, impacts on lenders, cashback rewards, and bank protectionism.

Banks also attempted to demonstrate to lawmakers that their position is supported by the public. The American Bankers Association recently released the results of a poll:

- When the issue mentioned “allowing stablecoin yields could reduce bank lendable funds and impact community and economic growth,” respondents supported Congress banning stablecoin yields at a 3:1 ratio;

- At a 6:1 ratio, stablecoin-related legislation should be approached cautiously to avoid disrupting the existing financial system, particularly community banks.

But the crypto industry argues that banks are merely trying to protect their own funding models by limiting competition from digital dollars.

Industry figures, including Coinbase CEO Brian Armstrong, believe that under the GENIUS Act, stablecoin issuers would face stricter reserve requirements than banks—stablecoins issued must be fully backed by cash or cash equivalents.

Increased trading volume raises the stakes in Washington's博弈.

The market size has made this yield competition impossible to ignore as a niche issue.

Boston Consulting Group estimates that the total volume of stablecoin transactions last year was approximately $62 trillion, but after excluding bot trading, internal exchange transfers, and similar activities, genuine economic activity amounted to only about $4.2 trillion.

The vast gap between surface trading volume and actual economic utility explains why the debate over "yield" has become so critical.

If stablecoins remain primarily clearing tools for trading and market structure, lawmakers are more likely to classify them as payment instruments; however, if yield mechanisms turn stablecoins into widely used cash storage tools within user apps, pressure on banks will rise rapidly.

To this end, the White House earlier this year attempted to broker a compromise: allowing partial returns for a limited number of scenarios such as peer-to-peer payments, while prohibiting returns on idle funds. Crypto companies accepted this framework, but the banking sector rejected it, causing Senate negotiations to completely stall.

Even if Congress takes no action, regulatory agencies may step in to tighten yield models.

The U.S. Office of the Comptroller of the Currency, in a proposed rule implementing the GENIUS Act, states that if a stablecoin issuer provides funds to an affiliate or third party to pay returns to stablecoin holders, this will be deemed an indirect provision of prohibited returns.

This means that if Congress fails to establish clear legislation, the executive branch may define the boundaries through regulatory rules.

There is little time left in Congress

Currently, the博弈 is divided into two lines:

- Congress debates whether to address the issue through statutory law;

- Regulators define the boundaries of corporate behavior within the existing legal framework.

Time itself is the greatest pressure for the Senate bill.

Alex Thorn, Research Head at Galaxy Digital, wrote on social media:

If the CLARITY Act does not pass committee review by the end of April, the probability of it passing in 2026 will be extremely low. The bill must be sent to the full Senate for a vote by early May. Legislative time is running out, and each passing day reduces the likelihood of passage.

He also cautioned that even if the yield dispute is resolved, progress on the bill remains uncertain:

Currently, external observers believe that the controversy over stablecoin yields is stalling the CLARITY Act. However, even if a compromise is reached on the yield issue, the bill is still likely to face other obstacles.

These challenges may include decentralized finance regulation, regulatory authority, and even ethical issues.

Before the mid-term elections in November, cryptocurrency regulation is likely to become a larger political battleground. This makes the current stalemate more urgent—any delay in the legislation will face a more crowded political calendar and a more challenging legislative environment.

Prediction markets also reflect a shift in sentiment. In early January, Polymarket gave the bill a roughly 80% chance of passing; following recent setbacks—including Armstrong stating the current version is unworkable—the probability has dropped to near 50%.

Kalshi data shows a 7% probability of the bill passing before May and a 65% probability of passage by the end of the year.

The failure of the bill will shift more decision-making power to regulators and the market.

The implications of failure extend far beyond the battle over returns. The core purpose of the CLARITY Act is to define whether crypto tokens are securities, commodities, or another category, providing a clear legal framework for market regulation.

Once the bill stalls, the entire industry will rely even more on regulatory guidance, interim rules, and future political changes.

This is also one of the reasons the market is closely watching the fate of the bill. Earlier this year, Matt Hougan, Chief Investment Officer at Bitwise, said the CLARITY Act would codify the current favorable regulatory environment for crypto; otherwise, future governments could reverse existing policies.

He wrote that if the bill fails, the crypto industry will enter a period of "proving itself," requiring three years to demonstrate its indispensability to the general public and traditional finance.

Under this logic, future industry growth will rely less on expectations of legislative implementation and more on whether products such as stablecoins and asset tokenization can achieve true large-scale adoption.

This presents the market with two entirely different paths:

- Bill passes → Investors price in the growth of stablecoins and tokenization;

- The bill failed → Future growth will rely more on actual adoption, while facing uncertainty due to shifting policy trends in Washington.

The flowchart illustrates the countdown to the Senate’s stablecoin decision, with deadlines of March 6 and late April or early May leading to two paths: if Congress acts, it will bring regulatory clarity and faster growth; if Congress fails to act, uncertainty will ensue.

At this stage, the next decision rests in Washington. If senators can revive this market structure bill this spring, they still have the opportunity to define for themselves the extent to which stablecoins can deliver value to users and how much of a crypto regulatory framework can be codified into law. If not, regulators are clearly prepared to establish at least some of the rules themselves.

Regardless of the outcome, this debate has long moved beyond whether stablecoins belong in the financial system, and has instead delved into how stablecoins will operate within it, and who stands to benefit from their development.