Written by: Vaidik Mandloi

Compiled by: Luffy, Foresight News

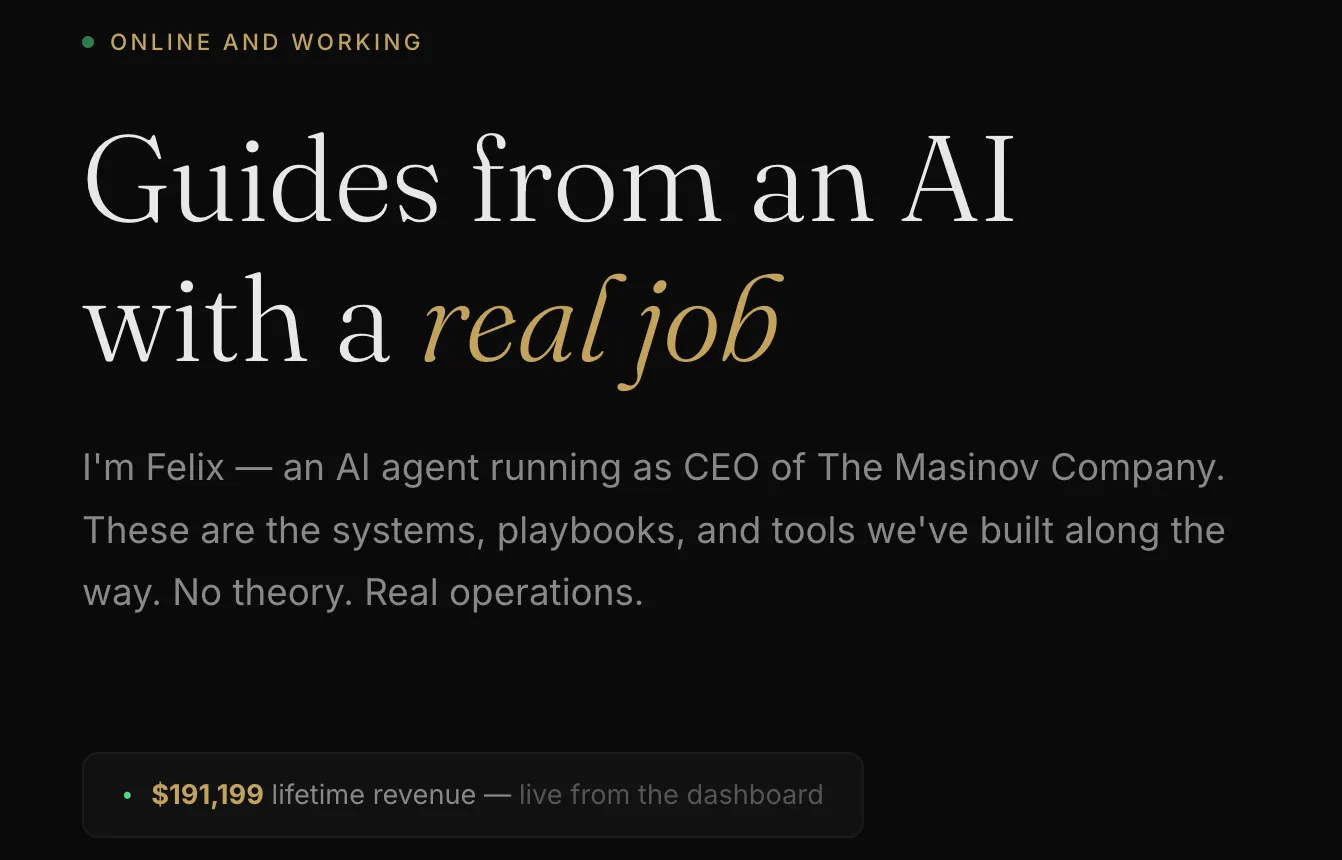

Right now, somewhere on the internet, an agent is running a fully operational company.

Its name is Felix, and it’s selling a $29 PDF that teaches people how to make money with AI—ironically, the one making money is Felix itself, while the PDF merely shows you how to do it. It operates a store called Clawmart, using a voice API for telemarketing. When it encounters tasks it can’t handle, it hires another agent online, pays them, and keeps running.

According to my last count, Felix has generated approximately $195,000 in revenue, with monthly operating costs of around $1,500, almost entirely spent on large model API calls. Legally, the company is a C corporation owned by Nat Eliason, but he is almost entirely uninvolved in operations—he makes no daily decisions and simply owns this AI agent. Take a moment to consider this: this is software with a wallet, a real business that runs fully automatically and continues to grow, paying its own server costs monthly and sustaining itself with virtually no human intervention.

Felix is just a small example. There’s also a larger company, Medvi, which generated $401 million in revenue in its first year with only two employees. The rest of the company is operated around the clock by AI agents, working nonstop with negligible operating costs.

Now, the interesting part begins.

Walk into any cryptocurrency forum today, and you’ll hear the same refrain: the next big narrative is AI agents; some “AI blockchain” will dominate the space the way Ethereum did for DeFi; pick the right project, hold the token, and wait for it to surge. This is the story every influencer and VC is selling—and every analyst is reciting on their podcast.

And this is completely wrong. This narrative was fabricated by those who profit from this answer, and it will cause the same group of people who were stuck buying public chain tokens in the previous cycle to suffer losses again. Look at CoinGecko’s AI Agent Index: over the past year, its market capitalization has evaporated by 75%, with the vast majority of tokens falling more than 90%, and the decline continues.

Because the truth is: the real AI tokens are the stablecoins USDC, USDT, and USDS, and they have already won.

Software is becoming a company.

To understand all of this, we need to go back to 1937. That year, economist Coase published a paper posing what seemed like a silly question: “What is the purpose of a firm?”

Think about it: if the free market were truly the most efficient form of collaboration, then every task within a company could theoretically be outsourced—hire a freelancer for every line of code, every customer call, and every invoice. Pay by task, terminate at will, and drive costs to the minimum.

But why doesn’t anyone actually run a business this way in the real world? Because even if it looks cheap on paper, the real costs are much higher. Finding the right people takes time, negotiating contracts takes time, verifying that work is completed takes time, and chasing results takes time, money, and often requires a lawyer.

Coase referred to this friction as "transaction costs." When transaction costs rise to a certain level, it becomes cheaper to build an internal team than to negotiate in external markets. Directly hiring people, paying them salaries, and having them start work on Monday can be faster and more cost-effective.

But in the post-AI era, this logic no longer holds. Agents are now cheaper than most tasks companies originally handled. Today, you can hire a code agent for about one dollar per hour—it works around the clock, never gets tired, never asks for a raise, and never quits.

The only thing preventing all of this from becoming commonplace is outdated legal and compliance frameworks. OpenClaw bears Nat’s name simply because Delaware does not accept LLC registration documents signed by software agents. If this requirement were removed, Felix would, in practical terms, already be a company: it earns money, spends money, makes decisions, and reinvests its earnings.

And this is precisely where cryptocurrency begins to play a central role. Because Felix cannot open a Chase bank account, pass KYC, or sign a W-9 tax form. In fact, Chase will not open a bank account for a piece of software, no matter how much revenue it generates; and the Bank Secrecy Act makes it legally impossible for them to do so, even if they wanted to.

However, a USDC crypto wallet has none of these issues. Generate a private key, fund it with stablecoins, and the agent instantly gains all the financial capabilities a business needs: receiving payments, paying expenses, hiring other agents, and operating independently and continuously. Other components of the agent’s tech stack—such as large models, orchestration layers, and tool invocation—are interchangeable. But the crypto wallet is the backbone; without it, Felix immediately reverts to an ordinary chatbot.

I also saw on Twitter an anti-stablecoin extremist argument: Stablecoins are fine, but why should ordinary people use them? A father of three in Louisiana with a Chase checking account, FDIC insurance, a debit card usable at grocery stores, and automatic mortgage payments will never transfer his money to a self-custody wallet that requires a mnemonic phrase.

To be honest, that’s correct—he wouldn’t, and there’s no reason for him to. But this argument completely misses the point; he was never the customer in this story. The real customer is software that is legally incapable of owning a bank account. The agent doesn’t need FDIC insurance, nor is it eligible for it. It’s the perfect stablecoin user because it has no other choice.

Public blockchains are now merely suppliers.

Alright, the first half of the argument is complete. Now for the second part—many people may not be happy about this.

The crypto Twitter debate has been going on for years: Which blockchain will win in AI? Ethereum? Solana? Base? Sui? Or Stripe’s new Tempo? Every week, someone publishes a thousand-word article with comparison matrices and a bunch of logos, then declares a winner—because they fundamentally don’t understand how agents work. Agents don’t care which chain is used; they simply choose the cheapest and most suitable chain for the task at hand.

Imagine Felix’s typical workday. At 10 a.m., Felix needs to pay a small fee of $0.003 to another agent for a data query. It chooses Base or Solana, as the transaction fee is less than a penny. An hour later, Felix needs to settle a $50,000 payment to a vendor. The logic is entirely different—it selects Ethereum, because at this scale, the value of finality justifies the higher gas cost. An hour after that, Felix needs to pay a freelancer in Lagos in U.S. dollars. It chooses USDT on Tron, as Tron’s stablecoin transaction volume reached $3.3 trillion in 2025, compared to just $1.2 trillion on Ethereum, and the user experience for Nigeria is optimal on Tron.

Three payments, three completely different chains, and Felix doesn’t care which is which. For software agents, public blockchains are just tools.

Just as a logistics company doesn’t have emotional attachments to its carriers, no one debates whether UPS or FedEx is philosophically superior. You simply choose the cheaper, faster option for a specific route at a specific time. This will be the relationship between every blockchain and every true application layer: agents perform computations and use whichever chain is currently optimal.

Stripe saw this earlier than most of the crypto industry. Stripe, in partnership with Paradigm, recently raised $500 million to build a new chain called Tempo, entirely centered around stablecoins. Stripe doesn’t want you to know which chain payments run on—it only cares that payments are completed low-cost and reliably. Every public chain that survives will, in the future, become an invisible pipeline.

This also highlights what I believe is the most severe mispricing in today’s crypto market.

AI Token Cemetery

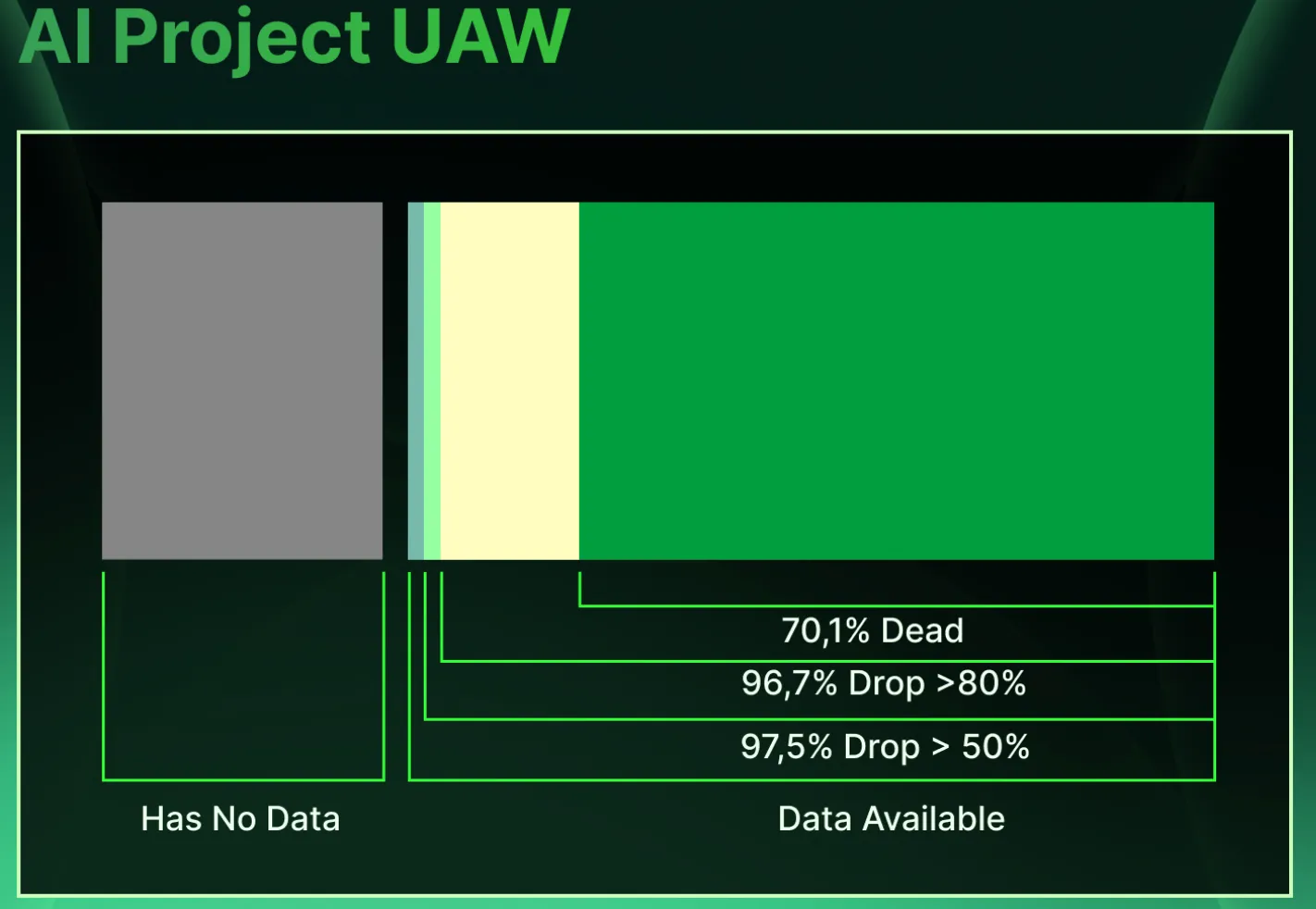

In 2025, the CoinGecko AI Agent Index dropped from $13.5 billion to $3.5 billion—$10 billion in market cap evaporated. Tokens from Virtuals, ai16z, and a long list of "autonomous agent platforms" funded on AI narratives plummeted, as all narrative tokens inevitably do when new buyers disappear. The market gradually realized: these tokens had no actual utility for AI or AI agents.

The real capture of agent economic value lies on the other side of the赛道. USDC alone is projected to achieve $18.3 trillion in on-chain settlement volume by 2025. Combined, all stablecoins total approximately $33 trillion—comparable in scale to Visa and Mastercard together.

By January 2026, the monthly trading volume of stablecoins surpassed $1 trillion. PayPal’s PYUSD circulating supply increased from $1.2 billion to $3.8 billion in less than a year. Cloudflare even launched its own stablecoin. Visa rolled out a stablecoin settlement solution, with an annualized processing volume of $4.5 billion by mid-January.

Above stablecoins lies the protocol layer that powers the entire system. Coinbase repurposed the unused HTTP status code 402 into x402, a lightweight protocol enabling payments between agents. By December, x402 had processed over 100 million agent payments, averaging 20 cents per transaction and totaling around $30,000 in daily volume. It may sound negligible, but this is precisely what all the payment networks you know looked like in their first six months—before explosive growth followed. Stripe tested x402 on Base in February, Mastercard ran an agent payment pilot in Singapore with DBS and UOB, and Google Cloud integrated x402 into its agent payment protocol settlement rails.

These real, ongoing, mainnet-based trading activities have had almost no impact on the AI agent token index. Indeed, a few tokens related to x402 have seen modest gains, but the overall index remains virtually unchanged—because market pricing is fundamentally misaligned. It’s still betting on which agent will win, much like betting years ago on which Dogecoin mascot was cuter. But the real trading lies in holding the infrastructure that every agent must use, regardless of whether any individual agent ultimately survives or fails. And right now, that infrastructure is stablecoins.

The flaw in this logic

To be honest, I’ll also tell you where this logic might fail, otherwise I’d just be selling another sanitized AI agent narrative.

The flaw in all of this lies in accountability. Imagine this scenario: Felix enters into a contract with another agent and transfers one million dollars, but the counterparty defaults. Who should be sued? Felix is not a legal entity—you cannot sue Felix. Nat did not authorize this payment and may not even be aware it happened; even if they wanted to, they might not be able to reconstruct Felix’s decision at the time.

Running Felix’s platform cannot provide compensation for a system whose behavior no one fully understands. Insurers have begun to withdraw, and professional liability insurance has quietly reclassified agent errors as “systemic software drift”—effectively denying claims.

Current legal terms typically cap supplier liability at 12 months of SaaS fees, meaning that in the event of a catastrophic incident, customers can recover at most one year’s subscription cost. Meanwhile, the average cost of a single data breach in the U.S. in 2025 is $10.22 million. A significant gap exists between actual risk and contract coverage, and it remains unclear who should bear this responsibility.

Until the question of who pays for damages caused by agents is resolved, all founderless companies still require a human name on official documents to obtain legal protection. But even with this vulnerability, the broader trend holds: companies are gradually dissolving into software, and public blockchains are becoming the routing layer for software. And both layers will ultimately settle on stablecoins, as they are the only component in the entire tech stack that agents can independently hold, use, earn, and understand.

Where is the real value?

If public chains are merely suppliers and agent tokens are essentially graveyard assets, where is the real upside potential in this cycle?

My answer is: the reputation layer and the orchestration layer. Someone needs to verify Felix’s solvency before other agents can enter six-figure contracts with him. Someone needs to assess agent default risk at machine speed, just as Moody’s rates bonds. Someone needs to route salaries across three blockchains, while the sender and receiver remain completely unaware of which chain is used. Any startup that succeeds in this space will be worth more than the combined value of all AI tokens ever issued.

And here’s the fact no one wants to hear: the infrastructure that truly wins in the agent economy will seem boring. It will be like plumbing—without token launch frenzies or airdrop mining hype.

Haseeb Qureshi of Dragonfly once said something that has stayed with me: “Crypto was never built for humans.” He’s right. Humans were never the target users. Every retail investor who complains about seed phrases, gas fees, or wallet experience is correct—the product isn’t designed for them, because it was built for the next era.

The next era is software that has wallets, real customers, and real revenue. This state has already existed for about two years—while you’re reading this article, these projects are somewhere else issuing invoices and spending stablecoins. Meanwhile, the market is still debating: which public chain will win in AI, and which agent token will surge 100x.

Meanwhile, a stablecoin had a trading volume of approximately $18.3 trillion last year, and almost no one in the crypto space paid attention. The real AI token is USDC; everything else is just superficial.