Written by: Thejaswini M A

Compiled by Saoirse, Foresight News

I never fully believed in all of this—not because I’m smarter than anyone else, but because the people who shout the loudest about decentralization are often the same ones most eager to pull your money into their ecosystem. Throughout history, this combination has never been a good sign.

But I still keep watching. You can’t help but watch, because this is truly the most captivating drama right now. The entire industry is built on the radical idea of “trustless money,” yet almost everyone in it is utterly untrustworthy. Irony is everywhere.

Today, as all obvious truths eventually become widely known, people have gradually reached a conclusion—something some of us already knew deep down: decentralization has always been more of a performance than a genuine belief. The goal has always been to harvest "dumb money." Those who constantly proclaimed "banks are the enemy" are now shaking hands with the most centralized political powers on the planet, simply because it benefits their portfolios.

I’m not even angry. I’m just watching because this drama is too good to miss.

On October 31, 2008, amid the lingering effects of the financial crisis, Satoshi Nakamoto published a nine-page whitepaper proposing an electronic currency that requires no banks, no government, and no permission from anyone. Two parties could transact directly, without intermediaries taking a cut or a central authority determining whether you were eligible to transact.

To be fair, the original idea was compelling. It emerged directly from a world where hedge funds and central banks excessively leveraged the economy, profited at the expense of ordinary people, and relied on government bailouts when things went wrong. The anger behind it is entirely justified. If such a system—where elites grow rich while the public bears the cost—doesn’t provoke outrage, then what does?

The brilliance of Satoshi Nakamoto's design lies in its elimination of human factors. With no single point of control, there is no single point of failure. Instead, there are thousands of nodes, all equal and mutually verifying each other. You cannot bribe the entire network, nor can you threaten it with a single phone call. Nor can someone's wallet be frozen because a regulator is having a bad day.

The design's ownerless model is a wonderful concept.

People often blame industry decline on the influx of venture capital, NFT chaos, or the FTX collapse. But these are merely symptoms. The real problem emerged much earlier—if you paid close enough attention, it was evident from the very beginning.

The problem with decentralization is that it’s expensive, slow, and requires thousands of participants with no incentive to reach consensus to coordinate. Centralization, by contrast, is efficient, fast, and profitable. So when real money enters the picture, economic laws begin to operate as they always have. The industry begins to diverge, yet few are willing to openly acknowledge it.

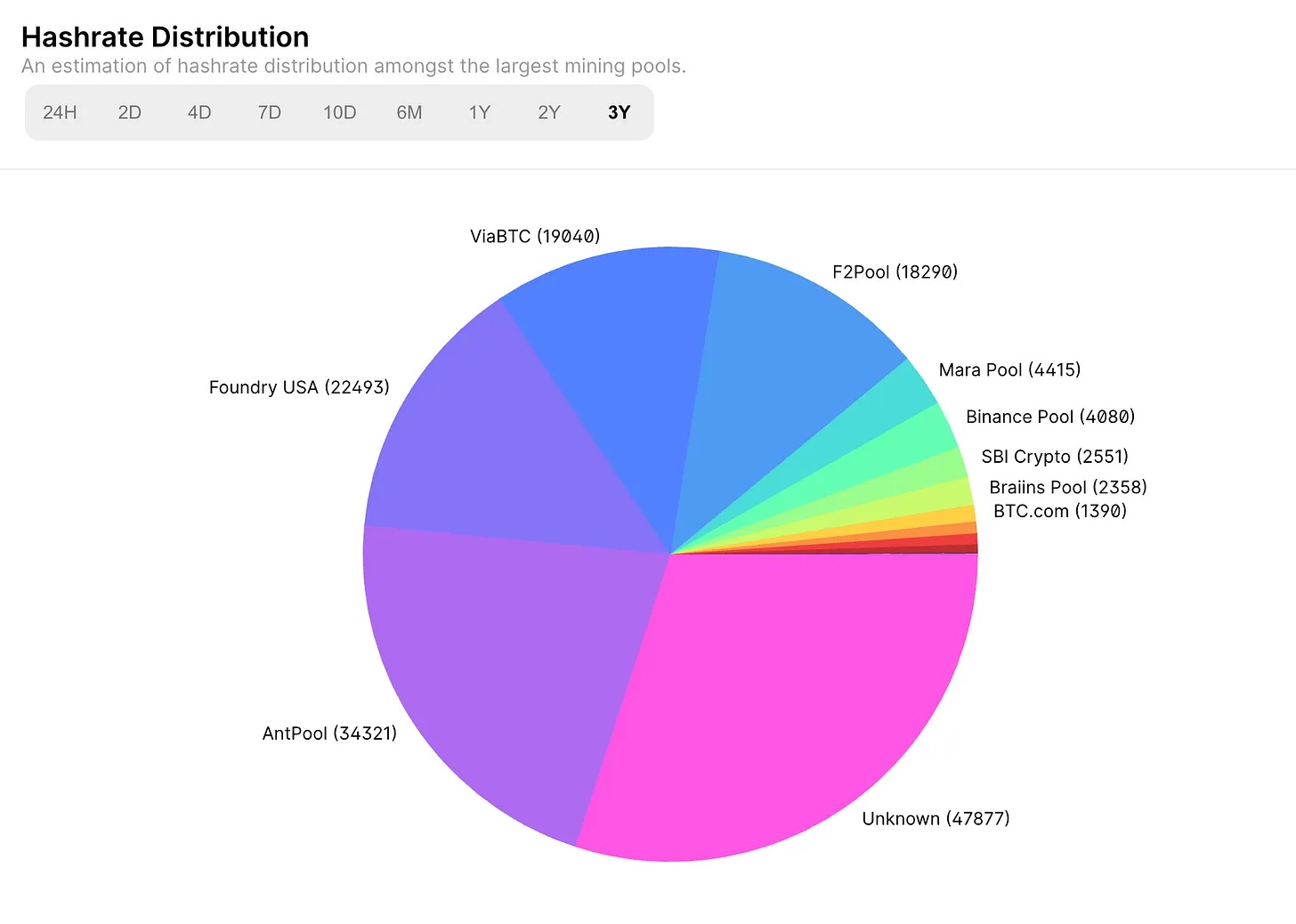

In May 2017, the combined hash rate of the top two Bitcoin mining pools accounted for less than 30%, and the top six pools together held less than 65%. This was the most decentralized moment in Bitcoin mining history. Nine years later, that peak is long gone. By December 2023, the top two mining pools controlled over 55% of the hash rate, while the top six accounted for a staggering 90%.

Today, Foundry USA controls approximately 30% of the total network hash rate, while AntPool holds about 18%, bringing their combined share close to 50%. By March 2026, the abstract risk finally became reality: Foundry mined six consecutive blocks, triggering a rare double blockchain reorganization that overwritten legitimate blocks from AntPool and ViaBTC. Small miners watched helplessly as their valid work was erased from the ledger. Although Bitcoin has never experienced a 51% attack and network integrity remains intact, the centralization risk the whitepaper was designed to prevent is no longer theoretical—it has become a numerical trend on a chart heading steadily toward danger.

The whitepaper describes a system that no single entity could achieve. This year, it turns eighteen. You can judge for yourself.

I want to be more precise in what I say, because lazy criticism easily goes off track. Believe me, I’ve tried it too.

When you look at all cryptocurrency products today that have real users, real trading volume, and real revenue, you’ll find that the vast majority are not decentralized.

But did they really claim to be decentralized? Confusing this point makes your criticism seem sharp—but misses the mark.

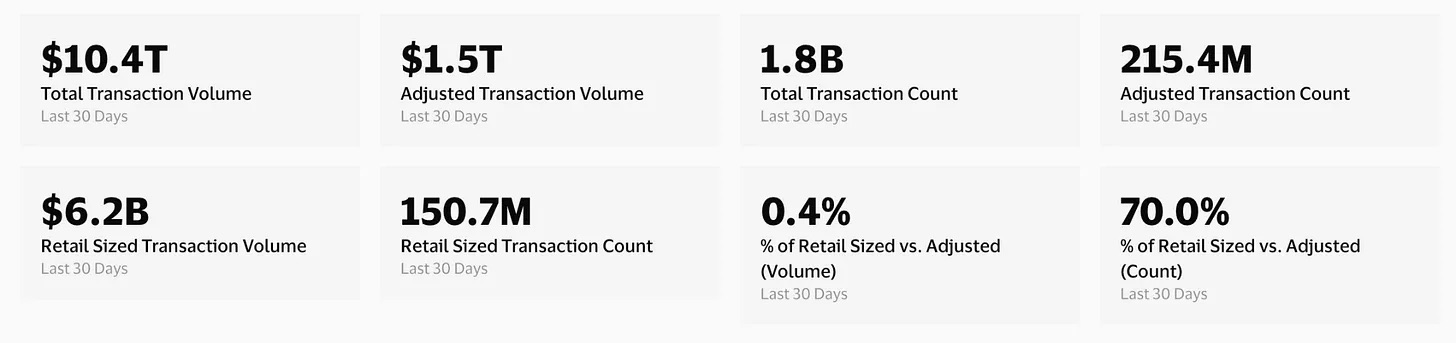

Stablecoins are the only category in the crypto industry with unanimous success. They are used for trading, cross-border remittances, and as a payment instrument in countries where local currencies continuously depreciate. As of 2025, USDT and USDC together account for 93% of the total stablecoin market capitalization and process transaction volumes in the unprecedented trillions of dollars.

@visaonchainanalytics

USDC and USDT are both issued by companies and can freeze wallets. Moreover, their reserves are held in banks—the very institutions the industry was meant to replace. DAI, often cited as proof that decentralization still exists, holds only a 3%–4% market share. No one has ever sold USDT to you as a decentralized product; its selling point has always been efficiency.

Transfer dollars across borders in minutes, settle in seconds—no correspondent banks, no SWIFT codes, no three-day clearing period. They kept the issuer but eliminated all inefficient and costly intermediaries between the issuer and users. The true revolution that traditional finance lost was a centralized dollar reissued on a blockchain. And this is exactly what it promised—and delivered.

Hyperliquid has billions in trading volume, is extremely fast, and its product is impressive. But in any practical sense, it is controlled by just 16 validators. During the JELLY event in March 2025, these 16 validators reached consensus and delisted a token within two minutes, turning a projected $12 million loss for the protocol into a profit. Two minutes. Getting Ethereum governance to reach any decision in two minutes would likely require a natural disaster—and even then, someone might still publish a dissenting blog post from some forgotten timezone.

Some call it FTX 2.0, but that characterization is inaccurate. Hyperliquid made corporate-style decisions. What truly earned its recognition was solving problems, compensating users, implementing an on-chain validator voting mechanism for future delistings, and continuing operations. The issue is that, for a period, Hyperliquid’s marketing heavily emphasized that it was not a company—while operating in every way like one.

Prediction markets. Polymarket experienced the crypto industry’s first true mainstream breakout during the 2024 U.S. election. Journalists cited its prices, and people who had never held ETH were using it. No one asked whether it was decentralized enough—people only cared whether it was accurate. And it was. Occasional articles surfaced discussing insider trading and its positioning as a “truth machine,” some of which I authored. But it was simply a well-made product that used crypto technology as underlying infrastructure, not as a ideological badge.

I could write a whole paragraph about DAOs, but the three words “decentralized autonomous organization” are probably the most absurd combination in the language. I’ll stop here.

These are the things that are actually working, and most of them are much more practical than the solutions described in the whitepaper.

The cryptocurrency world today is divided into two categories.

One category is infrastructure-level: built for efficiency, scale, and real-world usage, trading decentralization for performance, and most are upfront about this.

Another category is the protocol layer: Bitcoin, Ethereum, Solana—these remain fundamentally different from all prior systems; decentralization is not merely marketing rhetoric, but a design attribute that persists under immense adversarial pressure. Products compromise to meet user demands, and users simply want something easy to use. Under the pressure of real-world competition, the industry inevitably moves toward centralization. This is simply a natural law, not a moral failure. Revolutionary rhetoric from the protocol layer is continually borrowed by the product layer, even though the two are no longer the same thing.

In 2019, the founder of the Cypherpunk Manifesto was still being cited in keynote speeches; by 2023, he was sitting before a Senate hearing, claiming he had always sought constructive cooperation with regulators. For much of the industry, decentralization is merely a regulatory strategy dressed in ideological clothing: if no one is accountable, then no one needs to take responsibility. This ideology has been sufficiently persuasive to confuse lawyers and regulators, buying time to raise funds and launch products—and in many high-profile cases, make a clean exit. When regulation becomes unavoidable, this ideology is quietly set aside to avoid trouble.

There are still true believers in the industry. They entered the crypto world after witnessing governments destroy currencies, freeze accounts for political reasons, and exclude entire groups from basic financial services. They have become the moral cover for an industry fundamentally driven by profit. Profit-seeking itself is not wrong, but it shouldn’t be disguised.

In my view, this transaction may well be worth it, and those making the choice know it deep down—even if they won’t openly admit it. The pure ideal of decentralization has always struggled against reality. No one sat together to conspire against decentralization. The truth is simply that whenever people choose between a “usable product” and an “unworkable principle,” they always pick the former. Quietly, without announcement, and without a funeral.

And I find the truly darkly humorous aspect to be how this story has played out on a political level.

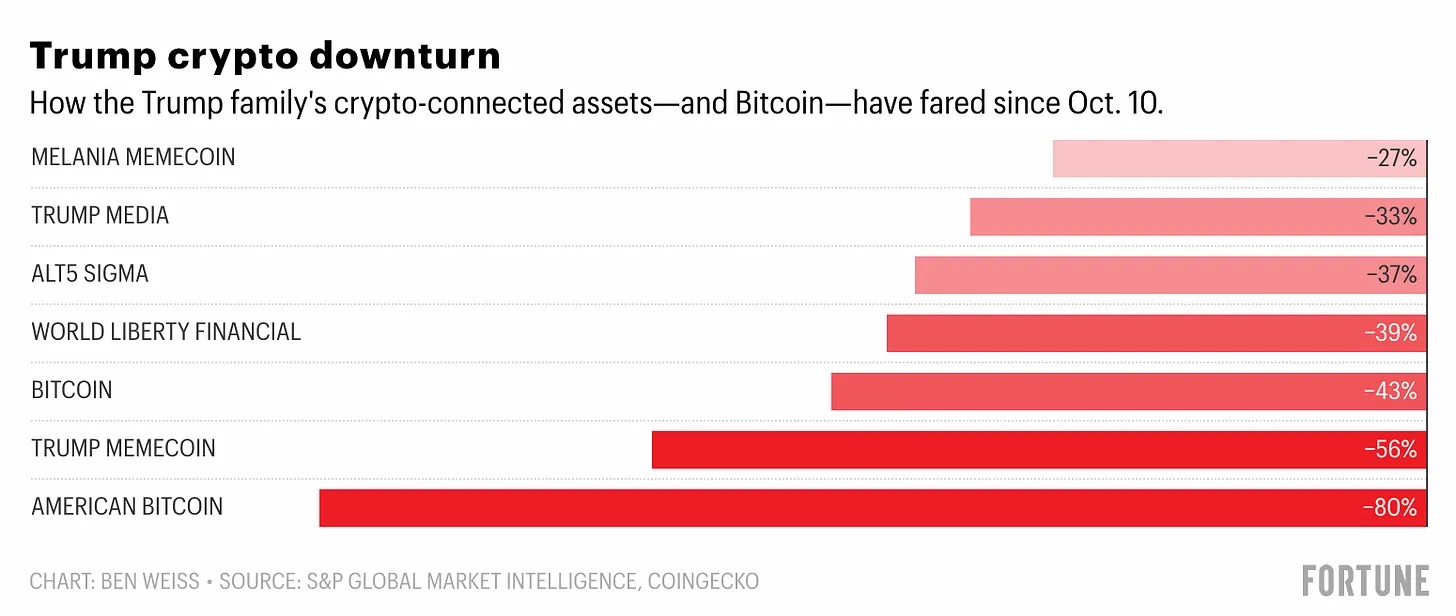

Before any crypto-related legislation was signed or any pro-crypto regulator was appointed, the Trump Organization's revenue in the first half of 2025 surged 17-fold to $864 million, with over 90% coming from crypto-related projects. According to an analysis by The Wall Street Journal, by early 2026, the Trump family had cashed out at least $1.2 billion from World Liberty Financial alone. His 19-year-old son Barron is listed on the project’s website as a “DeFi visionary.” To be honest, it’s hard not to feel sorry for the person who wrote this copy.

@fortune.com

This person called Bitcoin a scam in 2021, but by 2024 was standing on the stage at a Bitcoin conference. Meanwhile, those who had long advocated that "the government has no right to control your money" watched as a sitting president directly profited from the very industry he regulated—and the mainstream response was predicting coin prices and shouting, "The bull market is here!"

In economics, there is a concept called revealed preference: what you actually do matters more than what you claim to believe. The preference demonstrated by the decentralized movement under real-world political pressures is this: we care about decentralization—until it costs us something; after that, we only care about price.

I don’t intend to pass too much judgment. I’m simply documenting the facts, because someone needs to.

The狂热劲头 of “we’re going to change the world” seen in 2017 and 2021 has largely faded. The NFT crowd has dispersed, and in the metaverse, people have found new topics on which to confidently voice their misconceptions. Those who remain are quieter, less messianic, and far more honest about what they’re actually doing. The protocol layer is functioning as designed, while the application layer has produced remarkable products. This revolution has still delivered practical financial infrastructure, transformed the way value moves globally, and made a vast number of people extremely wealthy.

I have only one thing to say: Be honest about what you're doing.

If you’re building a centralized exchange with a better experience and encrypted channels, say so. If your stablecoin is issued by a company, allows wallet freezes, and holds reserves in a bank, say so. If your DAO is effectively controlled by three wallets, and everyone in the room knows it, then say that too. Users can handle honesty. What they cannot endure long-term is the gap between narrative and reality. In the end, they will express their dissatisfaction by leaving.

Satoshi Nakamoto has been silent for fifteen years. Perhaps he foresaw all of this and chose to watch the grand spectacle from behind the scenes. Or perhaps he simply knew when to walk away.