Article by Sleepy.txt

On February 25, Stripe released its annual public letter.

In 2025, the total transaction volume flowing through Stripe’s payment network reached $1.9 trillion, equivalent to 1.6% of global GDP and surpassing Australia’s annual GDP. Yet, instead of boasting about these achievements in their annual letter, Stripe’s founders, the Collison brothers, discussed the Industrial Revolution, the Nobel Prize in Economics, and black hole physics.

Why would a payment company discuss these topics? What is it really trying to say?

Stripe believes a quiet war has already begun over who will build the next-generation global commercial infrastructure—and it intends to be the one setting the rules. This letter is its call to arms, a manifesto addressed to CEOs and entrepreneurs around the world.

This machine is spinning faster and faster.

Stripe feels this is a pivotal moment, as the machine called "the market" is operating at an unprecedented pace.

The purpose of this machine is not to ensure shared prosperity for all, but to ruthlessly filter out profits, capital, and talent, reallocating them to the most productive enterprises. In the past, this machine turned slowly, and everyone had enough to eat. But now, AI has installed a new engine into this machine.

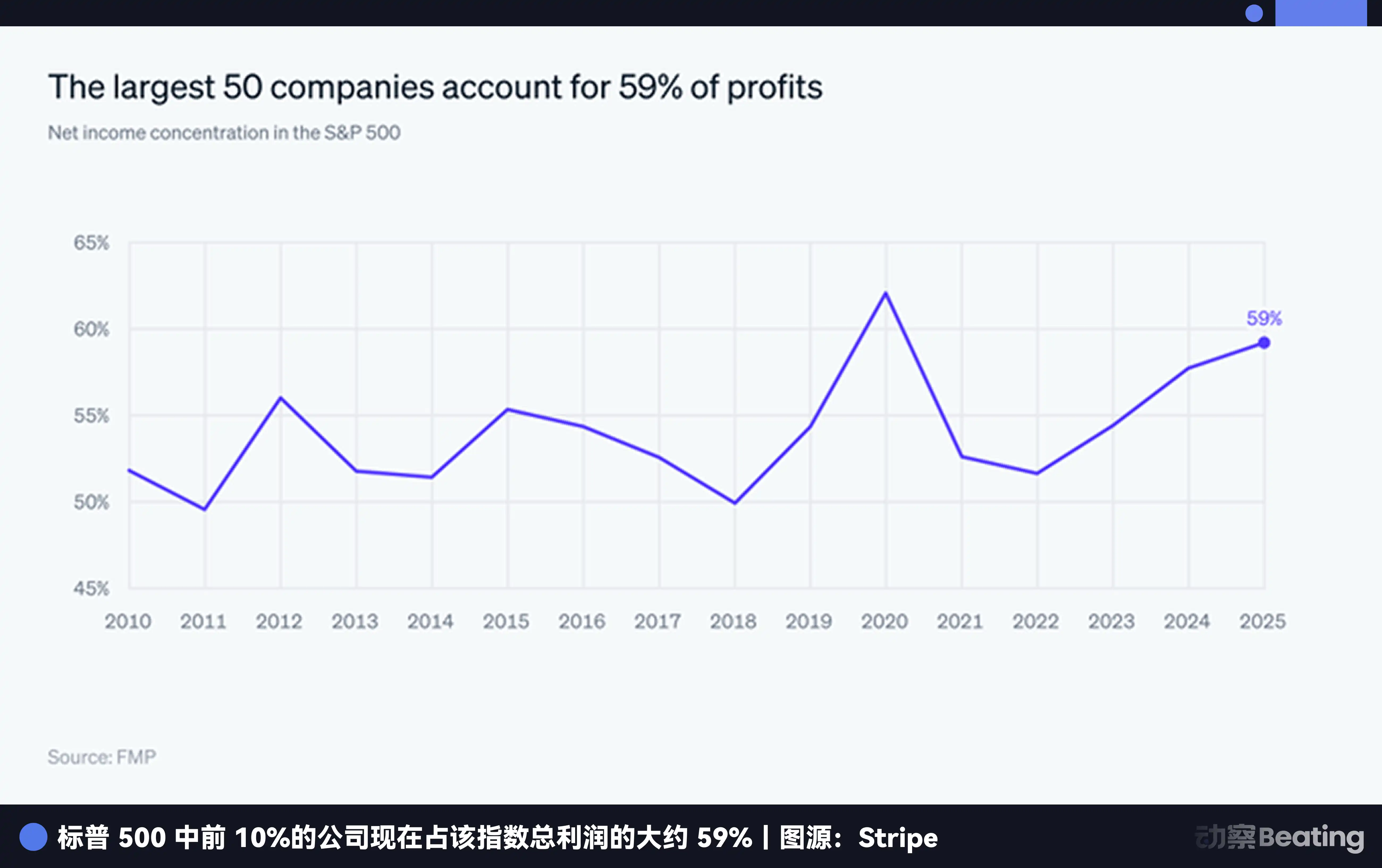

Stripe cited a set of data in its letter: the top one-third of profitable publicly traded companies in the U.S. account for two-thirds of the entire stock market’s valuation—the highest share on record since data collection began in 1963. JPMorgan’s early 2026 outlook also described the winner-takes-all dynamic, highlighting excessive market concentration. The top 10% of companies in the S&P 500 generated 59% of total profits.

This divergence is not only between large and small companies, but also a life-or-death struggle within the industry. The letter mentioned several industry examples; let’s add some context:

Retail: Over the past three years, offline physical sales, adjusted for inflation, have grown by only 5%, while e-commerce has grown by 30% during the same period. This means that if you're a purely offline retailer, you might feel your business is still barely manageable, but in reality, you've been left behind by the times.

Aviation industry: Delta Air Lines and United Airlines, the two giants, have captured nearly all of the U.S. aviation industry's profits for 2025. Other airlines are struggling to survive.

Healthcare: Traditional hospitals and insurance companies are seeing their profit shares shrink significantly, while the healthcare technology sector's EBITDA (earnings before interest, taxes, depreciation, and amortization) is projected to exceed $110 billion by 2029. Money is flowing from old models to new ones.

Broader data shows that demand for software, computers, and data centers drove nearly half of U.S. GDP growth in 2025. Where we once said software was eating the world, now it’s computing power driving growth. Industries that haven’t aligned with computing power and software are finding life harder by the day.

Let’s look at a few more data points about entrepreneurship. Code commits on GitHub surged by 41% in 2025 (up from an average annual growth of 10–12%), iOS app releases increased by 60% year-over-year in December, and the number of companies achieving $10 million in annualized revenue within three months has doubled.

AI is pushing the pace of entrepreneurship to the extreme.

Stripe's own company incorporation service, Stripe Atlas, also saw a 41% increase in registrations in 2025, and 20% of new Atlas companies received their first payment within 30 days—a figure that was only 8% in 2020.

They also launched Claimable Sandboxes, allowing developers to deploy Stripe accounts with a single click directly from AI programming tools like Vercel and Replit—over 100,000 sandboxes have been created this way. This means the entire process, from a developer having an idea to writing code and receiving their first payment, has been compressed to an unprecedentedly short timeframe.

The sorters are accelerating, and new species are emerging in large numbers, born global from day one. This raises the next question: these new species are inherently global—but can they truly accept payments worldwide?

Products have no borders, but money does.

The answer is definitely no.

The internet has made information and products borderless, but the flow of money is still blocked by invisible walls. This is the greatest structural contradiction in today’s global commerce—and Stripe’s most important battleground.

What did past globalization look like? Coca-Cola took 20 years to bottle its first soda in Cuba; McDonald’s and Starbucks took 27 and 16 years, respectively, to open their first stores in Canada. In the internet era, Facebook took 5 years to support international currencies, and Google took 4 years to receive its first pound sterling ad payment.

But now, this strategy of first building a strong home base and then expanding overseas is no longer popular.

Today’s AI products, from day one, have their “domestic market” as the entire internet, launching globally in sync and reaching all markets in a second. Yet, although their customers are spread worldwide, their ability to collect payments is strictly constrained by national borders.

Behind the movement of funds lies an old infrastructure built on the nation-state system—SWIFT, central bank clearing systems, local payment licenses, foreign exchange controls, and anti-money laundering compliance. This system was designed for money to move within nations, not for money to move across the internet.

A developer wanting to sell their software online must apply for a merchant account, a process that can take weeks; they must integrate a payment gateway, requiring extensive coding; they must handle currencies from different countries, involving complex foreign exchange calculations; and they must comply with regulations in each country, necessitating a legal team. For a small team of just two or three people, this is nearly impossible to accomplish.

The founders of Stripe, the Collison brothers, have experienced this firsthand.

In 2007, as two teenage Irish boys, they founded their first company, Auctomatic, a software tool for eBay sellers. They quickly realized that the hardest part wasn’t writing code or finding customers—it was collecting payments from clients around the world.

At the time, they had only two options: either use PayPal, which was extremely unfriendly to developers and would arbitrarily freeze accounts; or deal with banks, which was even more troublesome.

That’s exactly why Stripe was created. They wanted to turn online payments from a complex, licensed, friction-filled process into something as simple as calling an API.

Stripe's success stems precisely from addressing this pain point: it handles all the complex backend work—such as dealing with banks, credit card organizations, and regulators—then provides developers with an extremely simple interface. Developers no longer need to worry about those tedious, complicated details and can focus solely on their products.

But even Stripe cannot completely tear down this wall. The open letter notes that Stripe’s card issuance product, after seven years, only operates in 22 countries. Ironically, fintech companies themselves are among the slowest to globalize—Chime in the U.S. has remained confined to the U.S. for 12 years, and Brazil’s Nubank took six years to expand beyond Brazil.

But the demand was there—Gamma, an AI-powered PPT tool born in California, saw its monthly revenue from India surge by 22% immediately after integrating Stripe to enable UPI payments. This case illustrates that once infrastructure is in place, suppressed demand can explode instantaneously. Stripe’s data confirms this: for businesses whose primary revenue comes from overseas, 30% of their income comes not from their home markets or the top ten economies like the U.S., China, Japan, or Germany, but from obscure countries rarely mentioned in the news.

But if the old financial infrastructure was designed for the old world, how can we break down this wall?

Stablecoins, independent of cryptocurrency narratives

Stablecoins may no longer be considered cryptocurrencies. They represent a new global payment infrastructure that, for the first time, makes money flow on the internet as naturally as data does.

In 2025, during a crypto winter marked by a 50% drop in Bitcoin’s price, stablecoin payment volumes doubled to $400 billion, with 60% consisting of B2B payments. Stripe has dubbed this the “Stablecoin Summer,” as users are no longer relying on them solely for speculation, but increasingly for conducting business.

The stablecoin platform Bridge, acquired by Stripe, has seen its transaction volume more than quadruple. A Y Combinator founder can now receive funding in stablecoins, earn interest on them in Stripe’s financial account, and use them to pay engineers anywhere in the world—something that was unimaginable in the past.

More dramatically, the CEO of Swedish fintech giant Klarna was once a well-known cryptocurrency skeptic, yet Klarna has now become the first bank to issue a stablecoin on Stripe’s Tempo testnet, aiming to reduce settlement costs for cross-border payments.

Stripe predicts that future commerce will be conducted by AI agents, requiring a blockchain capable of supporting billions of transactions per second. However, existing blockchain infrastructure cannot yet support this future. So, Stripe has built its own chain—Tempo.

It specializes in payments, with sub-second confirmations, optional privacy, and seamless integration with compliance systems. Visa, Nubank, and Shopify are already using it to test various scenarios. Stripe has also launched Financial Accounts, covering over 100 countries on its first day—making it the first truly globally native financial product.

Stripe's ambition is to become the TCP/IP protocol of this new infrastructure. It aims to do more than patch up the old pipeline system—it wants to build an entirely new, internet-native global payment network.

Most businesses are burning money for nothing.

Stripe mentioned in the letter: Most businesses live in a "low-revenue mode," wasting significant amounts of money daily on payment processing.

What is a low-revenue model? It’s when payment infrastructure is not optimized, leading to wasted spending on conversion rates, authorization rates, and fraud prevention. What is a high-revenue model? Stripe provides several real-world examples:

Microsoft conducts monthly performance evaluations of payment service providers, continuously optimizing authorization rates, which has significantly increased revenue.

After Gatwick Airport switched its payment system to Stripe, its payment success rate increased by 2.5 percentage points—a seemingly small number, but when multiplied by tens of millions of transactions per year, it represents a significant cost saving.

The credit scoring company FICO fully switched to Stripe through A/B testing, increasing its authorization rate by 1 percentage point.

After integrating Stripe, telehealth company Ro saw a 2% increase in authorization rates and a 3% decrease in dispute rates, earning tens of millions of additional dollars annually.

These cases illustrate that optimizing payments is a necessary step.

Another challenge businesses face is difficulty in securing financing. Since the 2008 financial crisis, credit for small businesses globally has continued to tighten. Loans to small businesses in Ireland plummeted by 66%, small loans under $1 million in the U.S. declined by 5%, and GDP growth in OECD countries fell from an annual average of 2.8% to 1.0%. Traditional banks are reluctant to lend to small businesses because they lack sufficient data to assess risk, and the approval costs are high.

Stripe Capital’s logic is that it has access to all of your transaction data and understands your business better than any bank. It uses merchants’ real-time transaction data to provide loans, bypassing the cumbersome approval processes of traditional banks. Businesses that receive funding from Stripe Capital grow 27 percentage points faster over the following year compared to similar businesses that don’t, with the fastest-growing recipients seeing more than three times the growth rate.

Stripe is transforming from a payment tool into a business operating system. It doesn’t just help you collect payments—it also helps you raise capital, issue cards, manage finances, and prevent fraud. It aims to become the financial brain of a business, not just a payment terminal.

But these are all problems that arise in a world where humans make decisions and humans make purchases. What would this infrastructure need to evolve into if the decision-makers and purchasers became AI agents?

AI agents are here—who will manage their wallets?

When AI agents become new consumers, the entire payment infrastructure must be redesigned, and who controls this design will determine the rules of the next generation of commerce.

What is agentic commerce? Simply put, when AI becomes intelligent enough, it’s no longer just a search tool—it becomes an agent you can authorize to act on your behalf. You say, “Book me the most cost-effective window seat flight to Shanghai next Tuesday,” and it independently compares prices, places the order, and completes the payment—all without any further input from you.

We are on the brink of a breakthrough in this new world. Just as in the mid-1990s with the internet, foundational protocols like HTTP, HTML, and DNS are emerging from a chaotic battle, and no one knows which will prevail—just as AltaVista competed with Google. Today, it’s equally unclear who will become the “HTTP” of agency commerce.

Stripe divides the evolution of agency businesses into five levels:

L1 eliminates web forms—AI can automatically fill out those annoying registration, login, and payment forms for you;

L2 is descriptive search, where you can use natural language to tell the AI what you're looking for, and it will find and present the results for you;

L3 is persistent memory; the AI remembers all your preferences and history;

L4 is an authorized delegation, allowing you to grant AI the authority to make purchase decisions on your behalf within a specified limit;

L5 is proactive prediction—AI can arrange everything for you even before you realize what you need.

Stripe believes we are currently at the edge of L1 and L2. Once we cross into L3 and L4, the very nature of commerce will be completely transformed. When thousands of AI agents are conducting transactions on the internet on behalf of humans, they will need their own wallets and their own payment protocols.

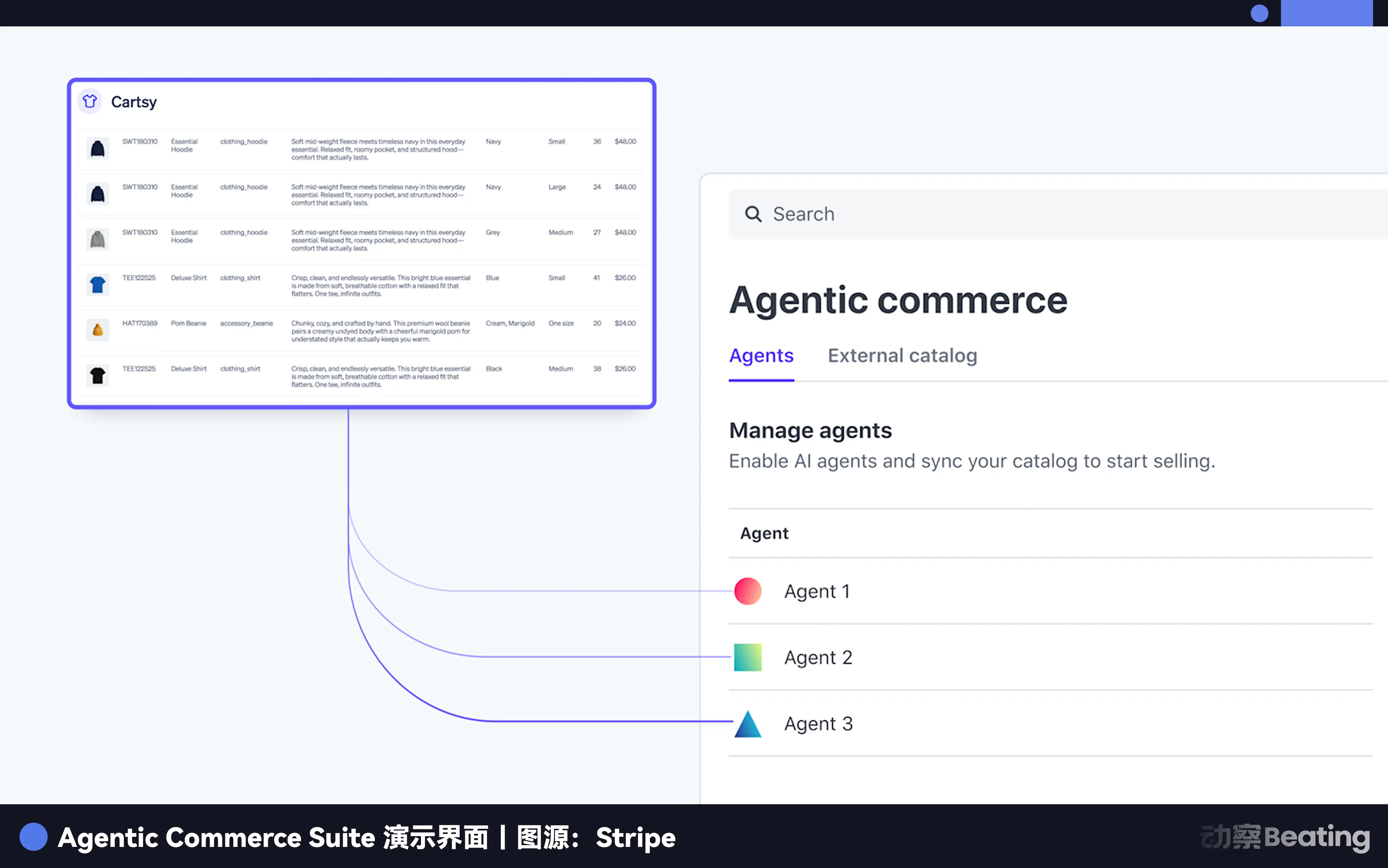

This is precisely the future Stripe is competing for. They’ve partnered with OpenAI to develop agent commerce protocols, collaborated with Microsoft to enable payments for Copilot, and launched the Agentic Commerce Suite, allowing brands like Etsy and Coach to integrate once and sell to AI agents across multiple AI platforms. They’ve even introduced a feature called Machine Payments, enabling AI agents themselves to become a new type of paying customer—meaning not only do humans buy from AI, but AI can also pay other AI.

When AI agents become new consumers, Stripe aims to be the one providing them with wallets and payment protocols—a battle much larger than payment processing itself.

Technical barriers, whether cross-border payments or AI agent wallets, Stripe is addressing one by one. But there remains an older, more stubborn wall standing in front of all these possibilities.

The final enemy

“A Republic of Permissions.” This is the judgment, quoted at the end of the letter by Stripe, drawing on the theory of Joel Mokyr, the 2025 Nobel laureate in Economics and economic historian—a judgment rarely voiced openly by any business: what is holding all of this back is not technology, but the system composed of regulators, committees, and courts, which, under the guise of “preventing bad things from happening,” systematically stifles “good things from happening.”

Mokyr's core argument is that the Industrial Revolution occurred in 18th-century Britain not merely because of coal and steam engines, but because the political environment and social culture of the time fostered an attitude of improvement that encouraged innovation and commercial risk-taking. Throughout history, countless new technologies have failed not because they were inherently flawed, but because they were suppressed by non-market aggregators—such as governments, guilds, and churches.

Stripe believes we currently live in a vast "republic of permits." It presents a list of criticisms:

In AI-driven drug development, although AI can now complete protein folding predictions that once took years in just weeks, the pace of new drug approvals is still held back by slow clinical trial processes, averaging over 10 years.

European entrepreneurs are being held back by the complex provisions of the EU AI Act, with small AI startups potentially spending vast amounts of time and money to meet compliance requirements rather than focusing on product development.

Newer, safer, and more efficient nuclear energy technologies are hindered from deployment by rigid, veto-based regulation, despite the growing urgency of climate change.

Waymo's autonomous vehicles have been hindered by local regulations in San Francisco, despite data showing they are safer than human-driven vehicles.

But Stripe is not entirely pessimistic. It also presents counterexamples of those thriving in the gaps:

Mistral AI from France and Bending Spoons from Italy have grown into world-class AI companies despite Europe’s stringent regulatory environment;

Zipline in Rwanda and Varda in the U.S. are gradually securing approvals and carving out new business models in highly regulated fields such as drone delivery and space manufacturing;

In the most conservative industry—healthcare—Spring Health and Maven Clinic in the United States have transformed mental health and women’s health services through software and data to improve efficiency.

This is Stripe’s deepest concern and the heaviest undercurrent of this letter. It compares the current AI transformation to falling into a black hole: at the very moment you cross the event horizon, you feel nothing, but your future has already been irrevocably altered. Stripe believes we stand on the eve of a different, hopefully better, singularity.

At the end of this letter, Stripe offers no optimistic assurances, no pessimistic predictions. It simply says that the market’s sorting machine will not stop—it will only spin faster. Whether you become the winner selected by the machine or the redundant data cast aside depends on how you respond right now.

Coming from Dromineer, a village of just 102 people in Ireland, Stripe turned seven lines of code into a commercial empire processing 1.6% of global GDP over fifteen years. Its next step is to define the next generation of global commerce rules.

Click to learn about the open positions at BlockBeats

Welcome to the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia