Original author: David, Shenchao TechFlow

On March 18, another blockchain mainnet went live.

It’s called Tempo, backed by Stripe and Paradigm. Stripe is one of the world’s largest online payment companies, processing $1.9 trillion in transactions last year; Paradigm is one of the largest venture capital firms in the crypto industry. Together, they invested $500 million in Tempo last year, giving the project a valuation of:

5 billion.

A $5 billion blockchain, not trading coins, not doing DeFi, not launching memes. On its mainnet launch day, Tempo's most prominently released product was:

Have machines pay other machines.

This might sound a bit abstract, but you can think of it this way: every step AI takes now costs money—calling an API costs money, purchasing computing power costs money, and retrieving a batch of data from a database also costs money...

But existing payment systems are all designed for people: bank accounts require ID verification, credit cards require facial recognition, and Alipay requires mobile phone verification codes.

AI can't pass even one.

It can handle the entire workflow, but when it comes to payment, it must pause and wait for a human to click “Confirm.”

Alongside the mainnet, an open protocol called MPP (Machine Payments Protocol), co-developed by Stripe, was launched.

In simple terms, it establishes a set of rules for machine-to-machine transactions, including how to request payments, authorize transactions, and settle them.

The envisioned scenario is that AI can autonomously spend within a preset budget without requiring human approval for each transaction. On the launch day, over 100 service providers had already integrated, including OpenAI, Anthropic, and Shopify.

But Tempo isn't the only one doing this this week.

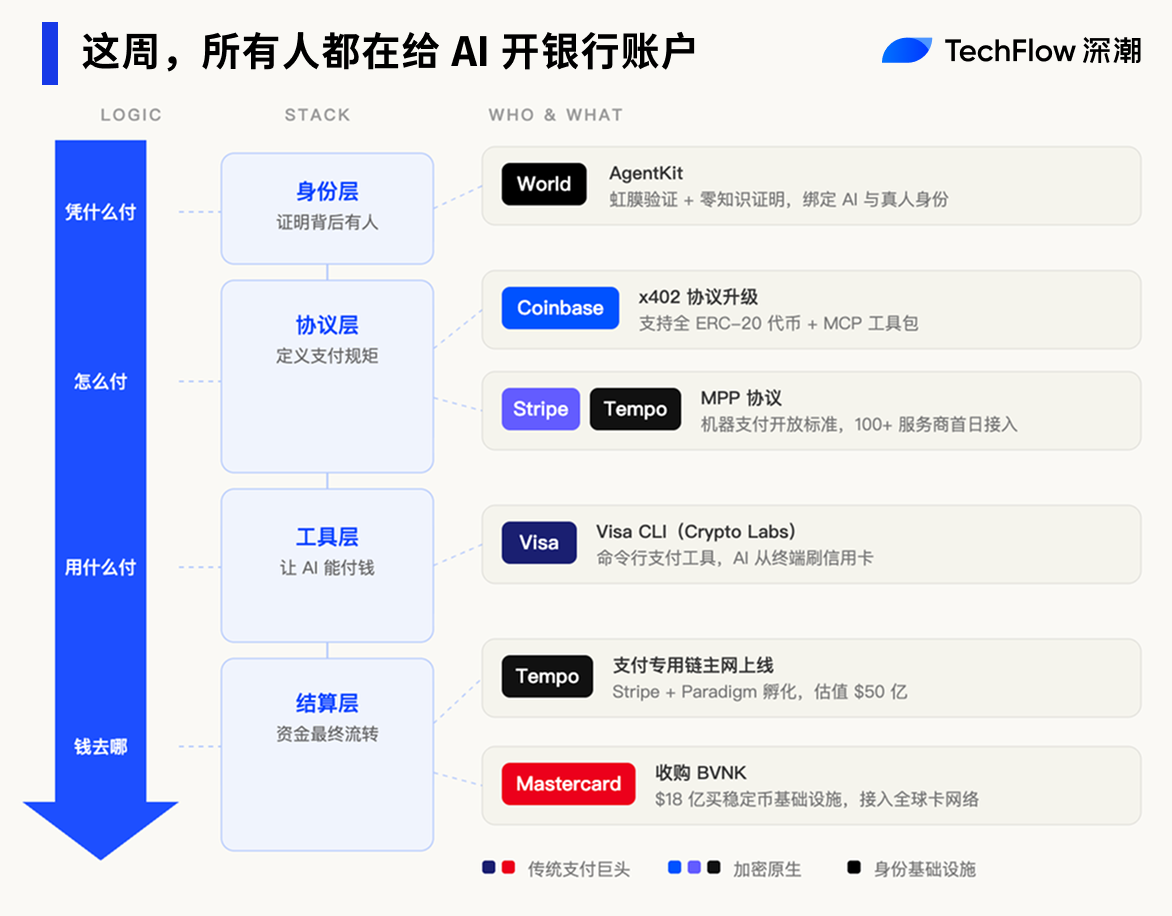

Within five days, Visa launched a new division and released an AI-powered payment tool; Coinbase upgraded its payment protocol significantly; Mastercard acquired a stablecoin company for $1.8 billion; and Sam Altman’s World released a specialized toolkit for AI identity verification.

Five giants rushed through the same door in a week, eager to open bank accounts for AI.

Two paths, one door

Tempo focuses on enabling AI settlements. However, settlement is only one component of a payment system. For an AI agent to truly spend autonomously, it also needs payment tools, funding channels, and identity verification.

Here, traditional payment companies and crypto companies are both vying for market share using their respective strengths.

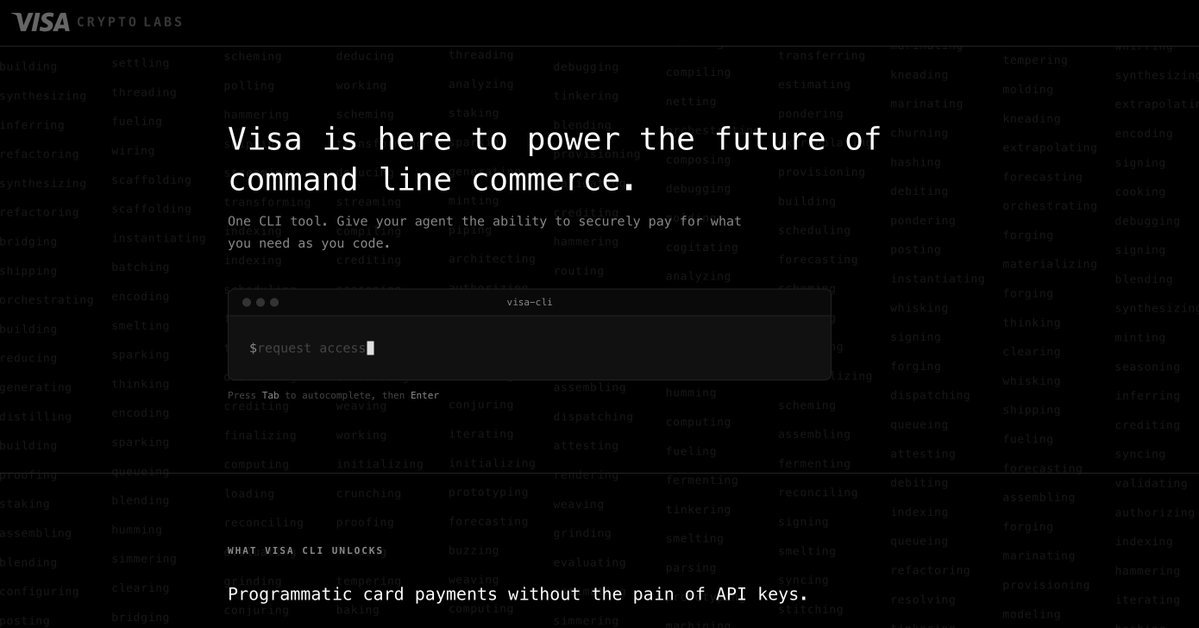

On March 18, the same day Tempo launched its mainnet, payment giant Visa also took action. Its newly established Crypto Labs department released its first product: Visa CLI, a tool that enables AI agents to initiate credit card payments directly from endpoints.

No API key required, no prior registration needed—when the AI needs to purchase a service during task execution, just type one command to pay. Visa calls this "command-line commerce."

Visa’s global card network connects billions of cards and millions of merchants; if AI-powered payments can operate on this existing network, they won’t need to wait for any new infrastructure to mature.

Visa is following the old path. Its competitor, Mastercard, chose a different approach: buying the route directly.

On March 17, Mastercard announced the acquisition of London-based stablecoin infrastructure company BVNK for $1.8 billion, marking the largest stablecoin acquisition in crypto history.

The purpose of this acquisition is also straightforward: if AI payments are made in stablecoins, those stablecoins will flow through my pipeline.

On the crypto-native side, activity is equally intense.

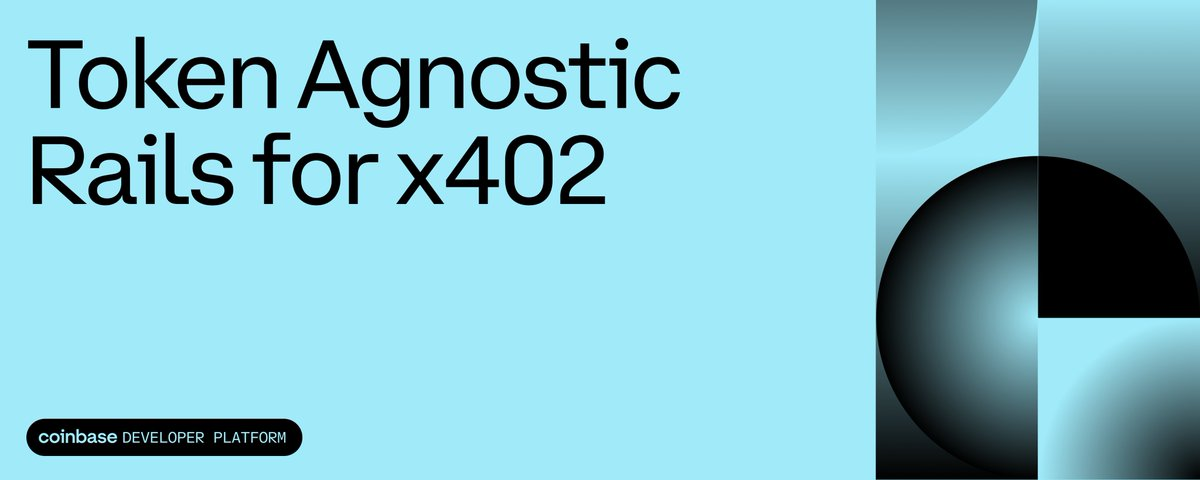

Coinbase's x402 protocol has undergone a major upgrade, expanding payment support from several stablecoins to all ERC-20 tokens, and has launched the MCP toolkit, enabling developers to connect AI tools to the payment network with a single click.

Although the starting points seem different, both sides are moving in the same direction: traditional payment companies are embracing cryptocurrency, while crypto companies are adopting AI. Ultimately, crypto infrastructure is becoming the underlying pipeline for AI-powered payments.

There’s one final step left. AI can spend money, but how do merchants know if there’s a person responsible behind the AI making the purchase?

On March 17, World, co-founded by Sam Altman, launched AgentKit, integrated with Coinbase’s x402. Its sole purpose is to enable AI to pay while proving that a verified human is behind the transaction. Merchants can confirm that someone is accountable for the payment, but cannot see who that person is.

Five days, five companies—each step—settlement, channels, tools, protocols, and identity—has been blocked.

The AI cake has been divided; only the cash register remains.

Over the past three years, the key positions in the AI industry chain have largely been taken.

The model layer is a battleground dominated by OpenAI, Anthropic, Google, and numerous Chinese companies, with computing power tightly controlled by NVIDIA, while the application layer—from coding assistants to search engines—has become a fiercely competitive red ocean.

Each floor is packed with people, and the barriers to competition grow higher with each level.

However, the payment layer is still relatively underdeveloped.

It’s not that no one thought of it—it’s just that the timing isn’t right. For AI Agent payments to be viable, AI must first be capable of independently completing an entire task chain. If it can only chat, without needing to call APIs, purchase computing power, or hire other Agents to do work, then payment isn’t a necessity.

Over the past year, this premise has gradually begun to hold true.

OpenClaw enables AI to directly control computers, while the MCP protocol allows AI to connect to external services. In the second half of 2025, the agent capabilities of major large models will see concentrated breakthroughs. AI is transitioning from a “conversational tool” to a “task-executing tool”—and doing work means spending money...

The demand to spend is here, but the infrastructure to spend is not yet in place.

That’s why Stripe, Visa, Mastercard, and Coinbase are all moving at once. For traditional payment companies, this is the first time in the AI wave that they’ve gained a home-field advantage. They can’t build the models or manufacture the chips, but payments are what they’ve been doing for decades.

Visa’s global card network connects billions of cards and millions of merchants, Mastercard operates in over 200 countries, and Stripe processed $1.9 trillion in transactions last year. If every AI expenditure flowed through these channels, the more AI accomplishes, the more they earn.

For crypto companies, the logic is different.

Coinbase CEO Brian Armstrong once said quite directly: "AI can have a crypto wallet, but it can't open a bank account."

Every step in the traditional financial system verifies "who you are"—opening a bank account requires an ID, applying for a credit card needs facial recognition, and every transaction requires an SMS verification code. AI is software, not a person, and it cannot pass any of these checkpoints.

But crypto wallets don’t need these. A private key is an account, and for an AI agent, on-chain payments are the path of least resistance.

Whether encrypted or not, AI payments will be a new infrastructure-level market. The only difference lies in which pipeline is better suited for machines.

The road is built, but the vehicle hasn't arrived.

At this point, it seems everything is in place, with the five giants each taking their positions.

But there is one number worth taking a look at.

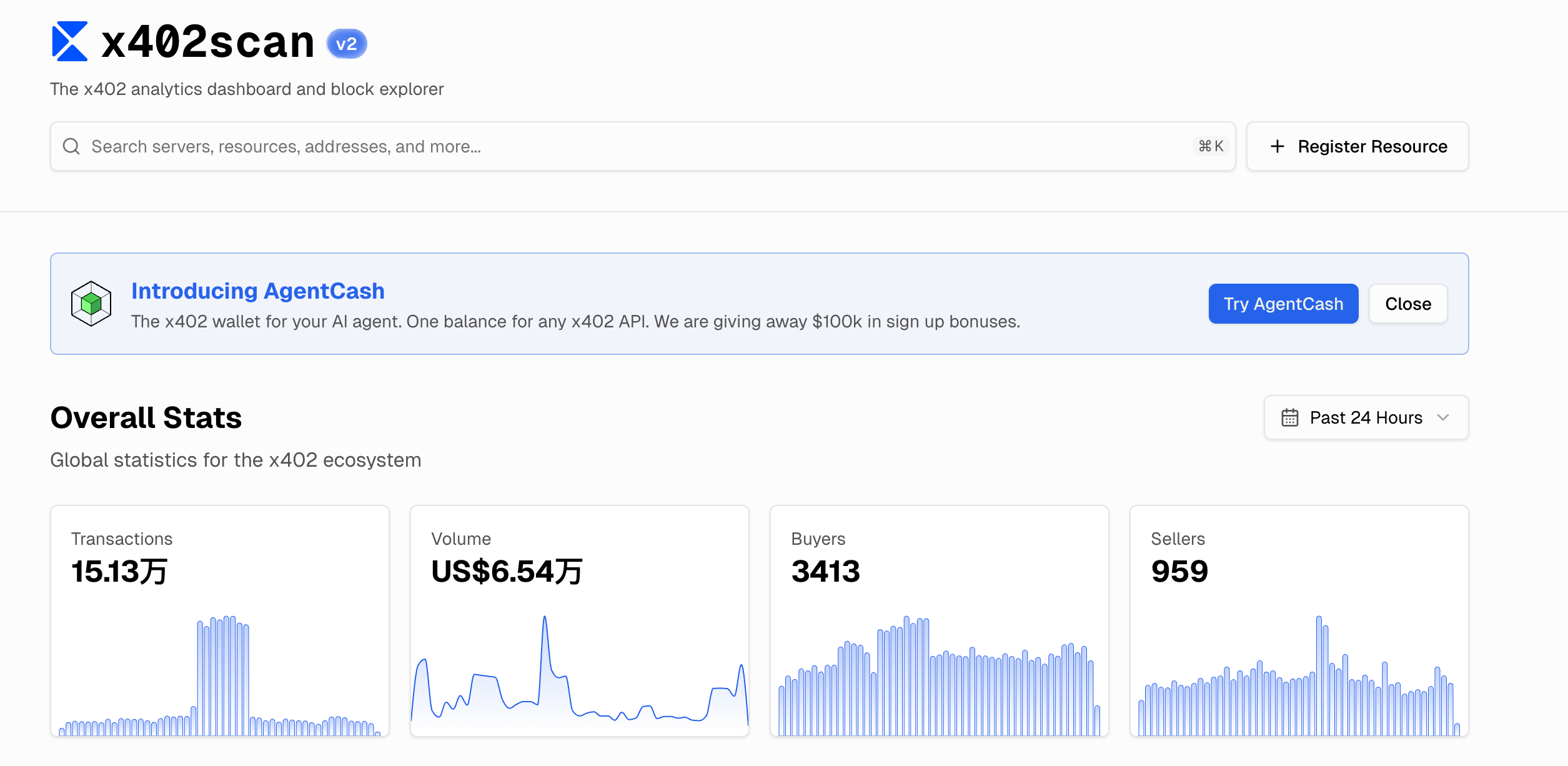

Coinbase's x402 protocol is currently the earliest deployed and most widely adopted AI payment protocol. According to data from x402scan, the total transaction volume across the ecosystem in the past 24 hours was $65,400, with 150,000 transactions averaging less than $0.50 per transaction.

What infrastructure is being built behind this number? Tempo is valued at $5 billion, Mastercard spent $1.8 billion to acquire BVNK, Visa created a dedicated new division, and Stripe is directly building the protocol themselves.

An infrastructure valued in the billions serving a market with daily trading volumes comparable to a street-side bubble tea shop.

All infrastructure businesses seem to follow this norm.

On the eve of the dot-com bubble in 2000, telecommunications companies laid millions of kilometers of fiber optic cable underwater. After completion, they discovered that global internet traffic required only 5% of it. Most of those companies went bankrupt, but the fiber remained.

Ten years later, video streaming and mobile internet filled those pipelines. The ones who paved the way didn’t make money, but the roads were real.

AI payments are at this stage now. The logic behind the demand is sound: AI agents are indeed becoming more capable, they do need to spend autonomously, and they truly require a new financial infrastructure.

Everyone is on the starting line, but after the starting gun fires, you realize you’re the only one on the track.

As for whose path will ultimately succeed, and when the first truly autonomous AI agent transaction will occur in your life, it may happen faster than anyone expects—or slower.

The only certainty is that the battle has already begun, and your wallet and mine may be the last to know.