On April 18, Kelp DAO’s cross-chain bridge was compromised, with the attacker minting 116,500 unbacked rsETH, which were then deposited into Aave and used to borrow WETH. The Aave Guardian initiated an emergency freeze within hours. According to on-chain estimates from Lookonchain, Aave V3 and V4 face potential bad debt of approximately $195 million.

In contrast, the lending protocol SparkLend within the MakerDAO (Sky) ecosystem suffered no losses.

This is not because Spark’s team is smarter than Aave’s, nor because they foresaw the vulnerability in this cross-chain bridge. Spark’s reason for exiting rsETH was stated in a governance forum post three months ago and has nothing to do with the security of the bridge contract.

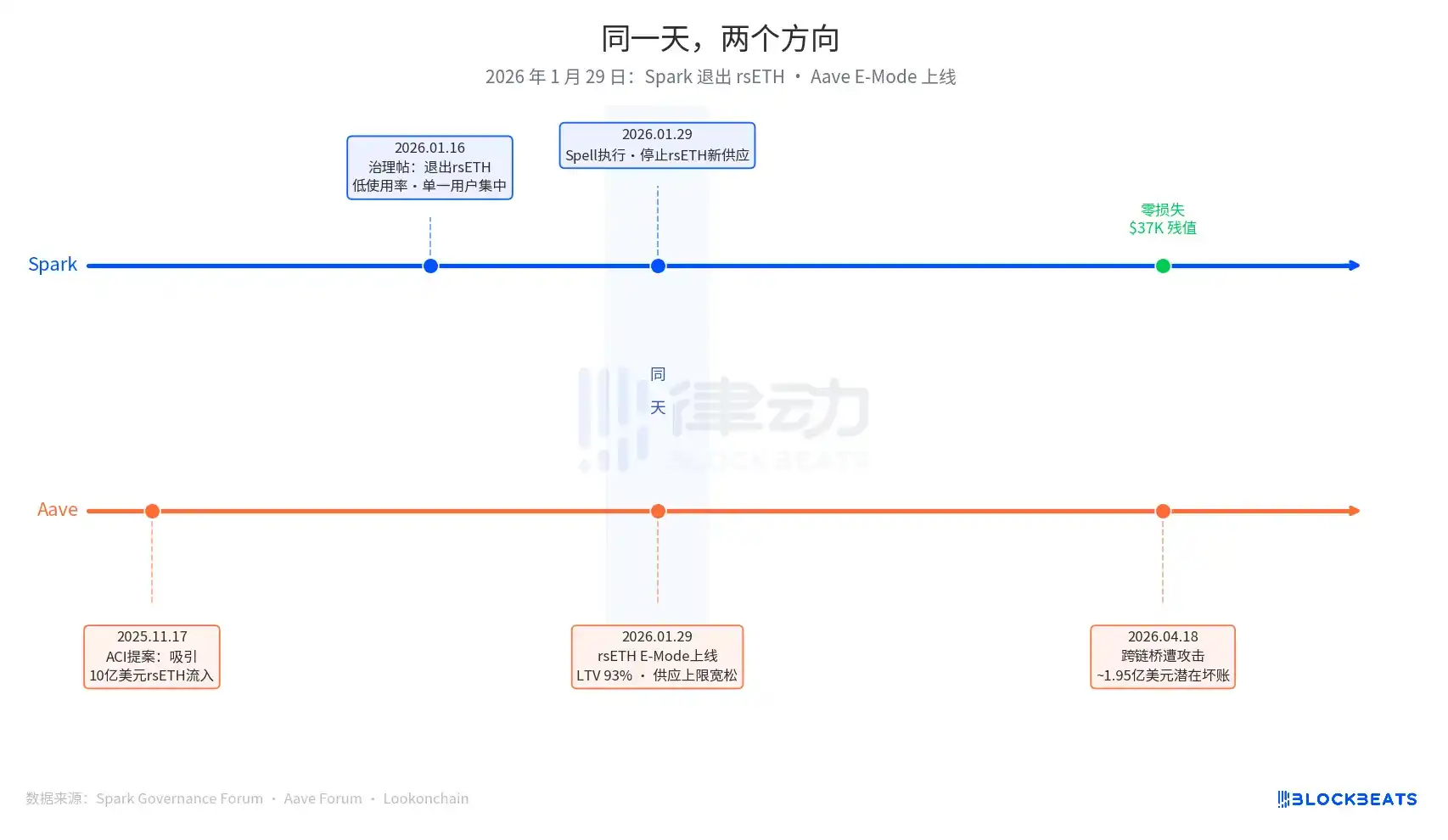

January 29, 2026, is the key date for this article. On this day, Spark executed a governance action called Spell, halting new supply of rsETH. On the same day, Aave launched rsETH E-Mode, allowing users to borrow WETH using rsETH as collateral with a maximum loan-to-value (LTV) ratio of 93%.

One exit, one expansion—both on the same day.

Spark’s decision to exit began with a governance proposal submitted on January 16, 2026, by PhoenixLabs (Spark’s ecosystem execution body). The rationale was straightforward: rsETH has low utilization, with nearly all usage originating from a single wallet (on-chain address 0xb99a), whose owner has indicated willingness to use alternative collateral such as wstETH or weETH. The original proposal stated, “Exiting rsETH can improve SparkLend’s safety margin and enhance risk-adjusted returns.” This was part of a periodic asset cleanup, alongside the simultaneous exits of tBTC, ezETH, and the entire Gnosis Chain market, all justified by the same reason: “low utilization.”

Aave's expansion decision originated earlier, stemming from a proposal initiated on November 17, 2025, by the ACI (Aave Chan Initiative, a governance proposal body led by Marc Zeller). The proposal's motivation was clear: “Restore WETH utilization, with the expectation of attracting $1 billion in rsETH inflows.” Chaos Labs completed its risk parameter validation in January, establishing an E-Mode LTV of 93% and a liquidation threshold of 95%. The decision-making process involved ACI, Chaos Labs, LlamaRisk, and Aave community voters. This was a collaborative expansion decision driven by multiple parties, not the result of a single institution’s error.

Three months later, the market provided the answer.

In Aave’s current Umbrella insurance mechanism, available funds amount to approximately $50 million, covering only 25% of the estimated $195 million in potential bad debt. The loss absorption order is as follows: aWETH stakers bear the first loss, followed by proportional sharing among WETH depositors, then stkAAVE holders, and finally the DAO treasury. Aave’s TVL dropped from $26.4 billion to $19.8 billion, including panic-driven withdrawals. The USDT market utilization rate reached 100% within hours, with new borrowings totaling approximately $300 million.

Spark has a current frozen residual value of $37,300, equivalent to 15.32 rsETH, in the SparkLend rsETH market. The wallet 0xb99a migrated nearly all its position to wstETH and weETH after new supplies were prohibited on January 29, fully aligning with the governance post’s prediction.

Spark co-founder Sam MacPherson (@hexonaut) reminded on April 19 that protocols claiming no exposure to rsETH do not necessarily have no exposure at all—if users have collateral deposited in affected lending markets, indirect exposure still exists. Spark has no direct losses, but indirect risks are still under evaluation.

The two protocols made opposing decisions on the same day—not to say that Spark or Aave made the correct choice, as the underlying issues for each system started from entirely different points.

Spark’s risk management logic is triggered by whether marginal cost exceeds marginal benefit. If any one of the following conditions is met—utilization falls below the threshold, single-user concentration exceeds limits, or risk-adjusted returns fail to meet targets—the asset is added to the exit candidate list. This is an active, efficiency-driven tightening mechanism, unrelated to the asset’s inherent security risks.

Aave's logic trigger is "market growth opportunity." With low utilization for WETH and a sufficiently large rsETH market, E-Mode can attract new capital. From this starting point, the parameter direction is expansion: LTV at 93%, relaxed supply caps, and multiple governance entities working together to drive progress.

These two protocols address entirely different questions: “Is this asset worth holding onto?” versus “How much incremental value can this asset generate?” Both lines of inquiry are valid business logic prior to a risk event; only after the event is triggered does the referee appear.

The security results of Spark are further supported by another layer.

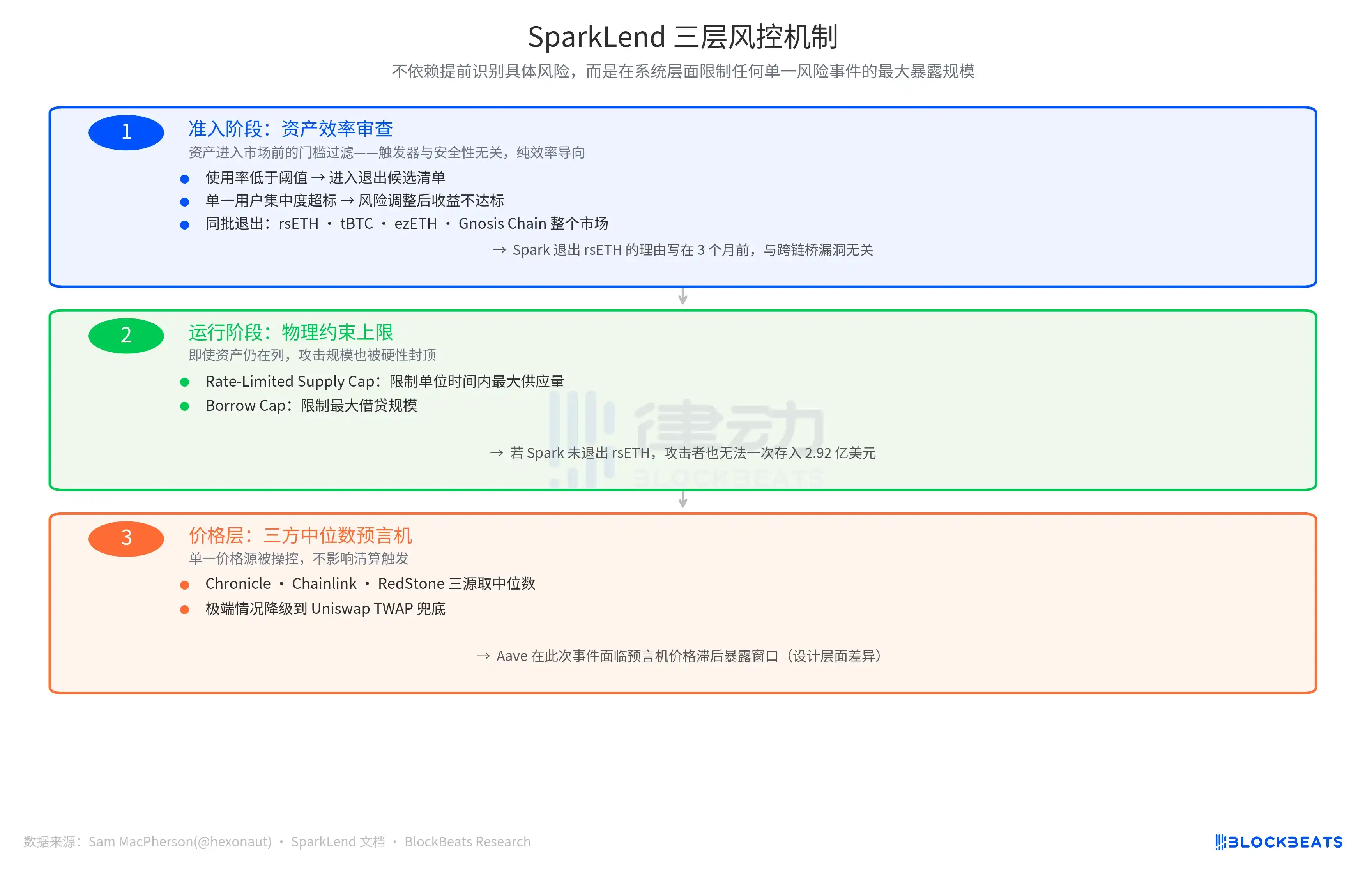

In his X post announcing "Exiting rsETH" on April 19, Sam MacPherson mentioned: "SparkLend has rate-limited deposit and borrowing caps, and its oracle mechanism uses a three-party median." This refers to two additional layers of Spark’s risk management system.

One is a physical constraint during operation. The Rate-Limited Supply Cap restricts the maximum supply per unit of time, and the Borrow Cap limits the maximum borrowing size. These design elements mean that even if Spark did not exit rsETH at the time, an attacker could not deposit $292 million worth of rsETH in a single transaction, as was possible on Aave—thereby hard-capping and containing the potential loss scale.

Another line of defense is at the price data layer: a three-party median oracle that takes the median of independent price feeds from Chronicle, Chainlink, and RedStone, with Uniswap TWAP as a fallback in extreme cases. Manipulation of a single price source will not trigger liquidations. In contrast, Aave experienced an exposure window during this event due to oracle price lag—a design difference, not an execution failure.

The design logic of the three lines of defense is consistent: rather than relying on prior identification of specific risks, it limits the maximum exposure to any single risk event at the system level.

The final loss figure depends on Kelp DAO’s loss allocation scheme. Three options are currently under consideration: socializing losses among all-chain rsETH holders (reducing the bad debt size), having only L2 rsETH holders bear the losses (keeping mainnet Aave bad debt unchanged), or rolling back the snapshot (extremely high operational complexity). This figure will be determined in the coming weeks.

The results of the two decision philosophies have already been quantified, with a difference of approximately $195 million, recorded in the governance action on the same trigger date.