Author:Beyond Research, Wall Street Insights

In the past, silver was called the "poor man's gold" not because it was actually cheap, but because the market never took its scarcity seriously.

Ample supply, adjustable inventory, and diversified uses— for a long time, the market has firmly believed that no matter how demand fluctuates, silver can always be quickly replenished. As a result, it has been repeatedly traded as "shadow gold," but has rarely been taken seriously for allocation.

But this premise has already been shattered by reality.

Since 2021, the global silver market has experienced a physical supply-demand deficit for consecutive years. Unlike previous short-term shortages amplified by financial cycles, this time the gap directly stems from the industrial sector: key areas such as photovoltaics, electrification, and high-end electronics have simultaneously driven rapid growth in demand for silver, while supply has been nearly unable to accelerate.

More fatally, the supply system of silver is highly insensitive to price signals.

More than 70% of the world's silver production comes as a by-product of other metals, with its production pace determined by the investment cycles of copper, lead, and zinc, rather than silver prices themselves. This means that even if prices rise, supply cannot quickly increase. When inventory buffers are continuously depleted, what the market faces is no longer a temporary fluctuation, but a sustained constraint.

It is precisely at this moment that silver is beginning to truly break free from the narrative of being the "poor man's gold." It is no longer merely a cheap alternative when gold rises in price, but is instead becoming a material that is continuously consumed by key industries and difficult to replace.

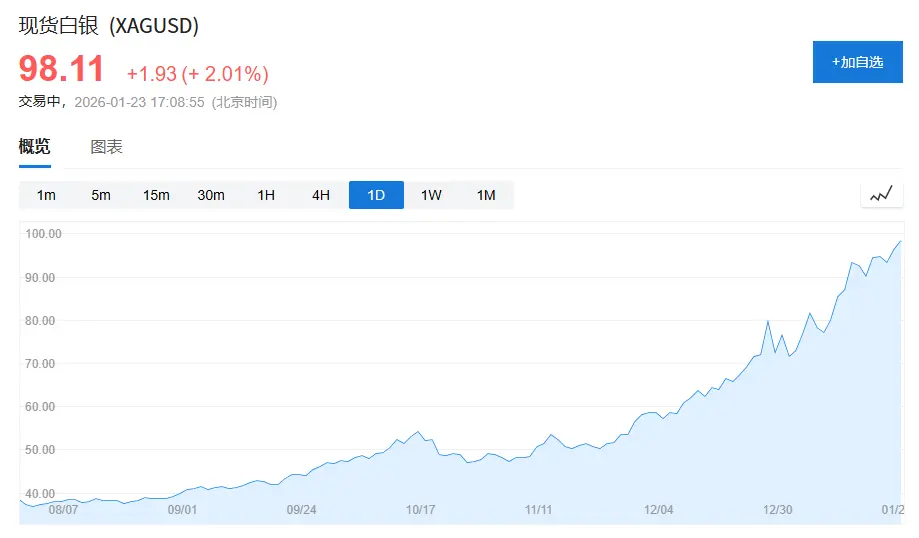

(Silver prices are approaching $100 per ounce. Silver prices were only $50 per ounce in mid-October last year, nearly doubling in three months.)

1. Silver's "Identity Crisis": Caught Between Gold and Industrial Metals

To understand why silver has been undervalued for a long time, we first need to understand its "identity dilemma."

In the modern commodity system, assets can generally be divided into two categories:

One category is credit-based assets, with gold being a typical example. The value of gold is not derived from its industrial uses, but rather from the credit system and demand for reserves. Even in years of the weakest overall demand, the net gold purchases by central banks can still account for 15% to 25% of annual total demand, providing a stable foundation for its price.

Another category consists of growth-oriented assets, such as copper, crude oil, and iron ore. These commodities have almost no financial attributes, and their prices are primarily driven by the economic cycle, infrastructure investment, and manufacturing investment.

Meanwhile, silver is precisely caught between the two.

According to the *World Silver Survey 2025*, total global silver demand in 2024 was 1.164 billion ounces (approximately 362,000 metric tons), including:

Industrial demand of 68.1 million ounces, accounting for approximately 58%;

Demand from jewelry and silverware amounts to 263 million ounces, accounting for approximately 23%.

Investment demand (silver bars, silver coins, ETFs) amounted to approximately 19.1 million ounces, accounting for about 16%.

The issue is that the behavioral patterns of these three types of needs are completely different:

Industrial demand depends on the business cycle, jewelry demand is highly price-sensitive, and investment demand is easily influenced by macroeconomic sentiment, leading to frequent entries and exits.

This structural division has long prevented silver from having a stable, unified, and dominant pricing anchor.

The result, in terms of price, is that silver has been compelled to trade at a long-term discount to gold.

An intuitive indicator is the gold-to-silver ratio. Over the past half-century, its historical average has been roughly between 55 and 60; however, between 2018 and 2020, this ratio once exceeded 90, and even approached 120 during the most severe phase of the pandemic.

Even against the backdrop of record-high industrial demand for silver in 2024, the gold-to-silver ratio has remained consistently within the 80–90 range in the long term, significantly higher than its long-term average.

This is not about silver being "useless," but rather the market is still using the financial logic of gold to price silver.

2. The Re-positioning of Silver: From "Diverse Applications" to "Locked into Industries"

Real change does not begin with financial markets, but quietly occurs at the industrial level.

Summarize the current changes in one sentence: Silver is transitioning from a dispersed industrial metal with various applications to a functional material that is critical and essential to key industries.

1. Photovoltaics: Silver Makes Its First Appearance as "Indispensable"

Photovoltaics is the most critical component in the structural changes of silver demand.

In 2015, the global newly installed photovoltaic capacity was approximately 50 GW; by 2024, this figure had exceeded 400 GW, increasing more than 8 times in less than a decade.

The industry is indeed continuously "de-silvering." The silver consumption per watt has decreased from about 0.3 grams in the early days to approximately 0.1 grams under current mainstream technologies.

However, the expansion speed of installed capacity is much faster than the decline in unit consumption.

According to the "World Silver Survey 2025," the actual demand for silver in the photovoltaic industry in 2024 reached 198 million ounces, an increase of more than 1.6 times compared to 2019, accounting for approximately 17% of the total global demand for silver.

More importantly, silver's role in photovoltaics is not "easily replaceable." In terms of core indicators such as conductivity, long-term stability, and reliability, silver remains the choice with the best overall performance. Technological advancements change the methods of usage, not the position of silver.

This gave silver its first large-scale, rapidly growing, and price-insensitive source of demand.

2. Electric Vehicles and AI Infrastructure: The usage is not exaggerated, but the difficulty of substitution is extremely high.

If photovoltaics brings certainty in terms of demand scale, then electric vehicles and digital infrastructure bring changes in the nature of demand.

A traditional fuel-powered vehicle uses an average of about 15–20 grams of silver, while an electric vehicle typically uses 30–40 grams of silver.

Against the backdrop of limited overall growth in global car sales, the penetration rate of new energy vehicles has increased from less than 3% in 2019 to nearly 20% in 2024, structurally boosting the demand for silver.

At the same time, the demand for silver in data centers, AI servers, and high-end electronic devices is more reflected in its irreplaceability rather than the absolute amount used.

In 2024, the demand for silver in the fields of electricity and electronics reached 461 million ounces, setting a new historical high for consecutive years.

These application scenarios are relatively insensitive to price but highly sensitive to supply stability.

3. The reality on the supply side: Silver is not a metal that can be increased in production simply by raising prices.

In sharp contrast to the certainty on the demand side is the rigidity on the supply side.

In 2024, global silver mine production was approximately 820 million ounces, with a year-over-year growth rate of less than 1%.

More importantly,More than 70% of the world's silver production comes from by-products, primarily associated with lead, zinc, copper, and gold mining.This structure has undergone little substantial change over the past two decades.

The production of native silver amounts to only about 228 million ounces, accounting for less than 30%, and it is still on a long-term downward trend.

This means that silver production is not determined by the price of silver, but is instead driven by the investment cycle of base metals.

4. Moving from cyclical shortages to structural tightness

Looking back in history, silver has indeed experienced bull markets before, but past trends were mostly derivatives of financial cycles.

The difference is that since 2021, the physical silver market has experienced a supply-demand deficit for consecutive years.

According to the "World Silver Survey 2025," the global annual silver supply and demand deficit averaged between 150 to 200 million ounces from 2021 to 2024, with the cumulative deficit approaching 800 million ounces.

Moreover, the visible silver inventory itself is not abundant. The current globally available inventory can only cover approximately 1–1.5 months of consumption, which is significantly below the 3-month safety line typically considered for commodities.

Once a large amount of silver enters photovoltaic modules, electrical equipment, and infrastructure, it becomes very difficult to return to the circulation market.

5. Silver is no longer just the shadow of gold.

Silver has not suddenly become scarce; it's just that for the first time, three conditions have been met simultaneously:

The demand scale is real and sustainable.Key uses are hard to replace.

Supply growth is highly constrained.

In the past, these three factors have never appeared simultaneously.

When the market still understands silver as "poor man's gold," the industry chain has already started to shut down.Key Functional MaterialsRe-examine it based on the standard.

Silver may still fluctuate, but it is certain that it no longer follows merely in the shadow of gold.

And this is the most important yet often underestimated fundamental change in this round of market movement.