Original Title: Silver Moon

Original Author: @abcampbell, Former Bridgewater Employee

Translated by SpecialistXBT, BlockBeats

Editor's Note: This article analyzes how irreversible industrial demand, rigid supply constraints, and strategic capital flows have become the driving forces behind the surge in silver prices. It also calmly highlights potential risks such as a rebound in the U.S. dollar and technological substitution, providing investors with a "barometer" to assess the true strength and weakness of the market.

The following is the original content:

It has been a month since we last discussed silver.

One month ago, the price of silver had risen by 45% for the year.

Do you remember me saying the situation was about to become "terrifying"?

Over the past year, silver trading has experienced a transformation from obscurity to a notable bull market, and finally to a historic shift of monumental proportions. The factors we identified years ago—robust demand from solar energy, rigid supply constrained by mining dynamics, Veblen-style speculative capital flows, strategic purchases by investors seeking to diversify away from the U.S. dollar, emerging market capital flight due to concerns about banking systems, and strategic stockpiling—have all now materialized and are fully driving the momentum.

Yet, this surge does not resemble a celebration; rather, it sounds more like a doomsday clock ticking away. It is not a threat to silver itself, but to the dollar and the global order it underpins. It is a signal indicating that the world in which our children will live will be vastly different from the one our parents knew.

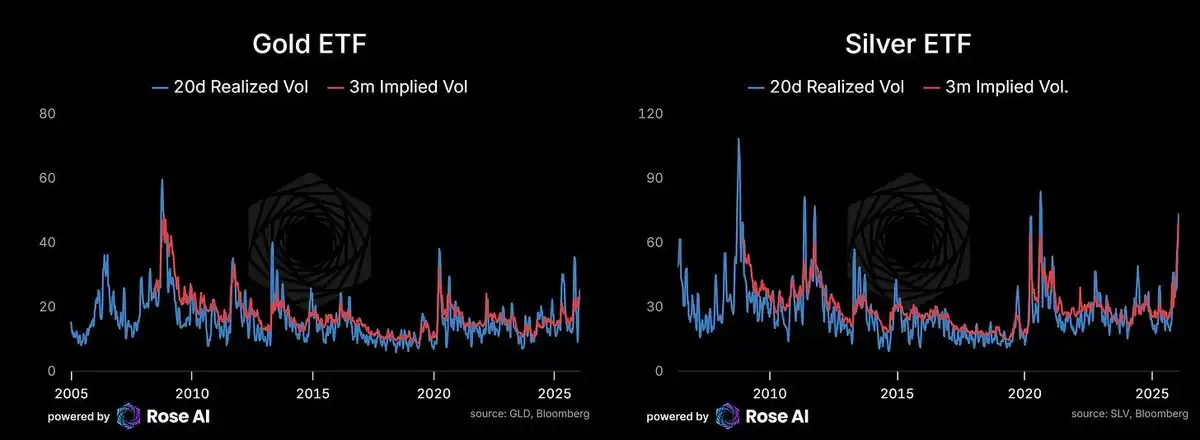

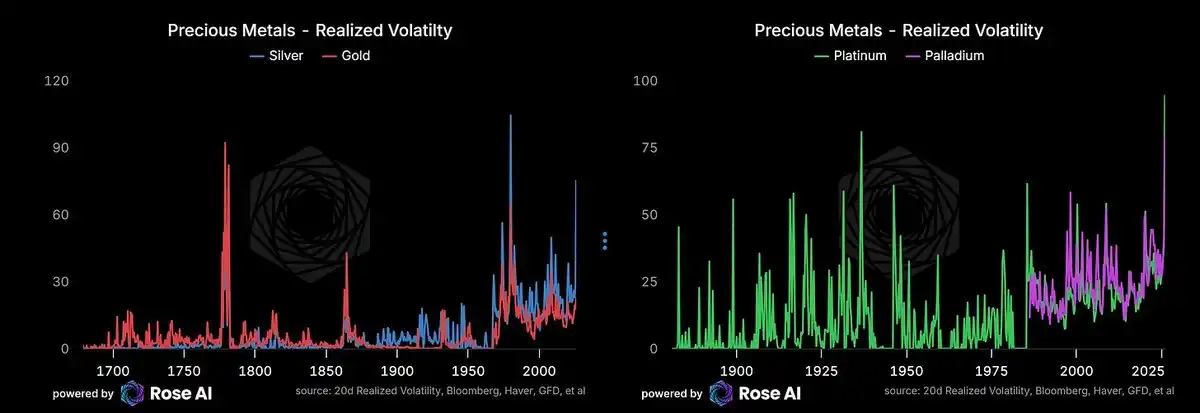

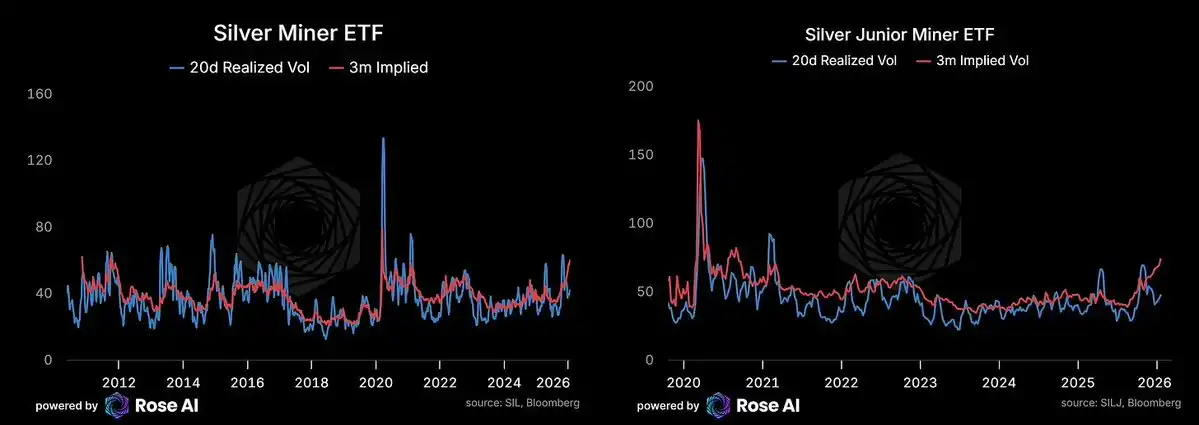

The options market is currently pricing in more than 4% daily volatility over the coming months, with volatility remaining above 3% in the foreseeable future. This has already been validated by realized volatility. In recorded history, there have only been two periods with higher silver volatility: the Hunt brothers' manipulation and squeeze in 1981, and during the American Revolutionary War (when the volatility stemmed from the collapse of local currencies against the British pound, rather than changes in the metal's price itself).

Gold volatility has also risen—consistent with broader currency depreciation trades, diversification flows out of emerging market currencies, and a trend among countries seeking substitutes for government bonds in their reserve portfolios.

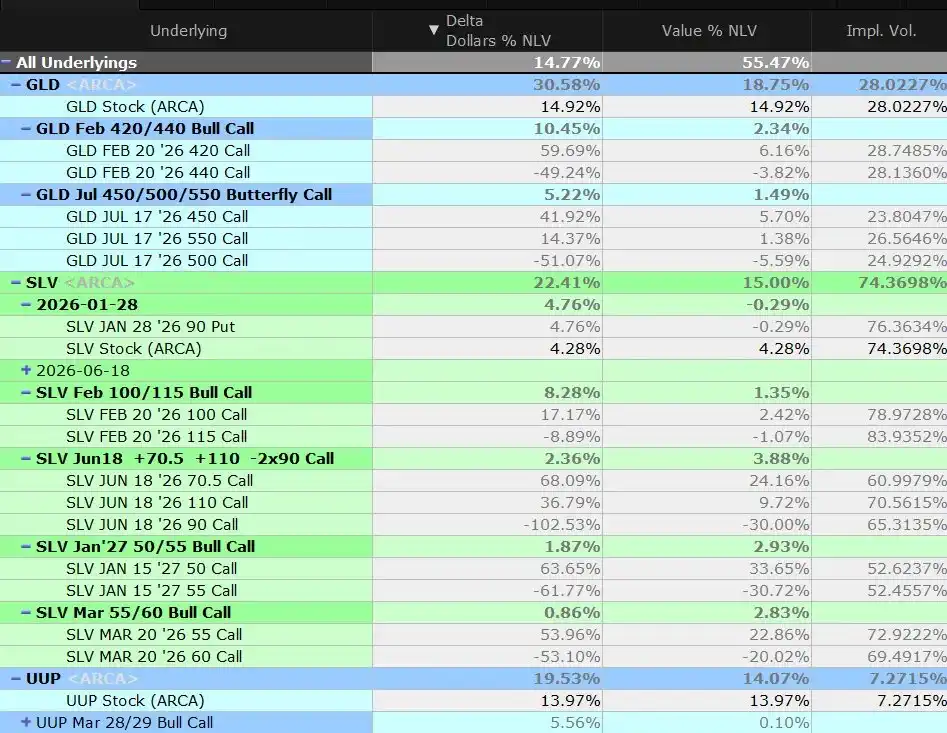

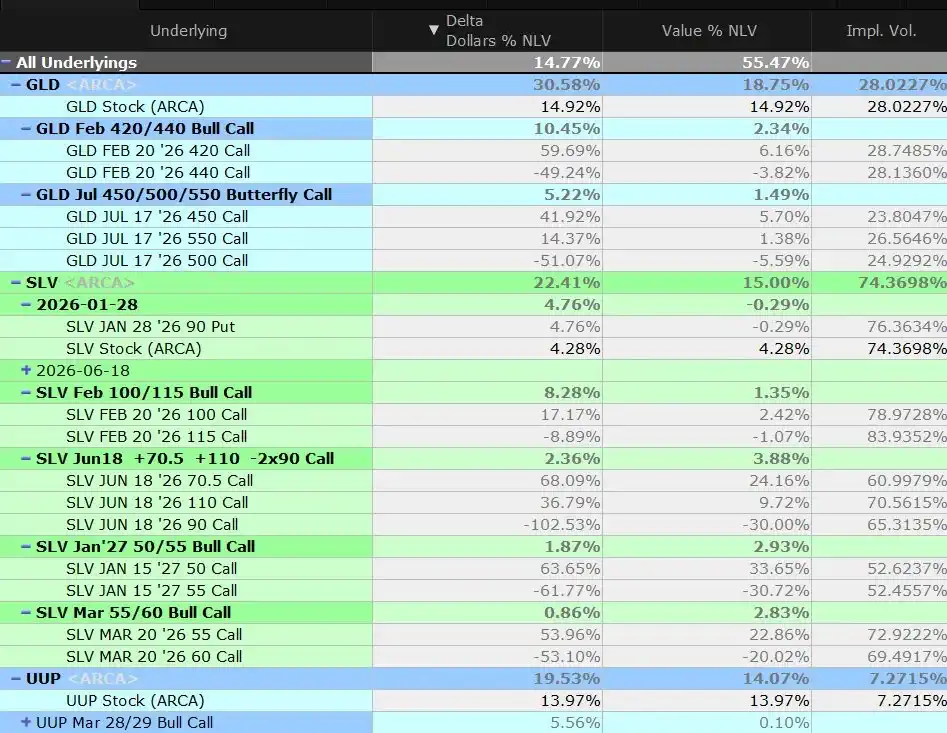

In short: We have reconfigured our gold position and closed slightly more than half of the butterfly spread positions last week when the spot price broke through the middle strike price. We currently still maintain a long position.

At the same time, we maintain short positions in U.S. equities, U.S. bonds/credit, and a small long U.S. dollar position to hedge against the implicit short U.S. dollar risk embedded in our metal holdings.

What is the driving force?

In markets where solar/AI demand has led to structural supply shortages, Chinese capital outflows remain a key short-term driver.

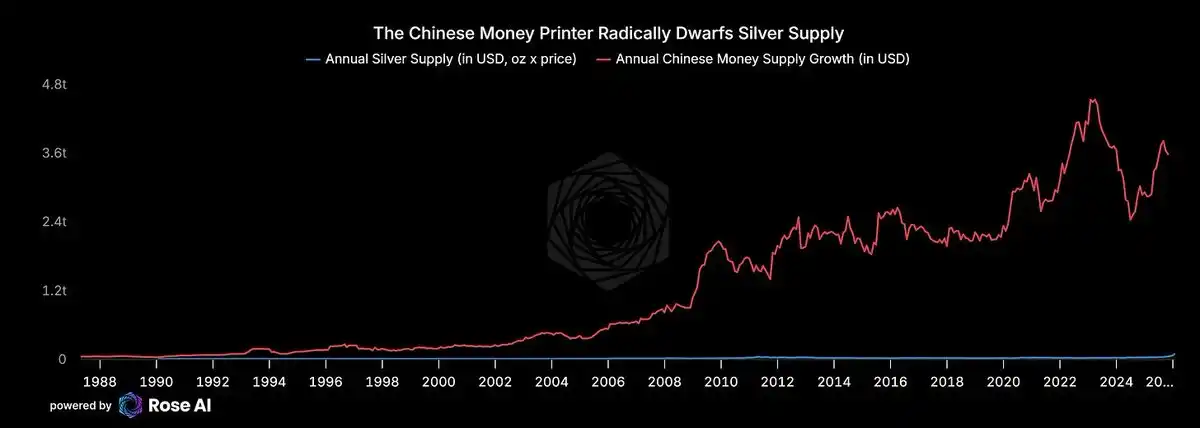

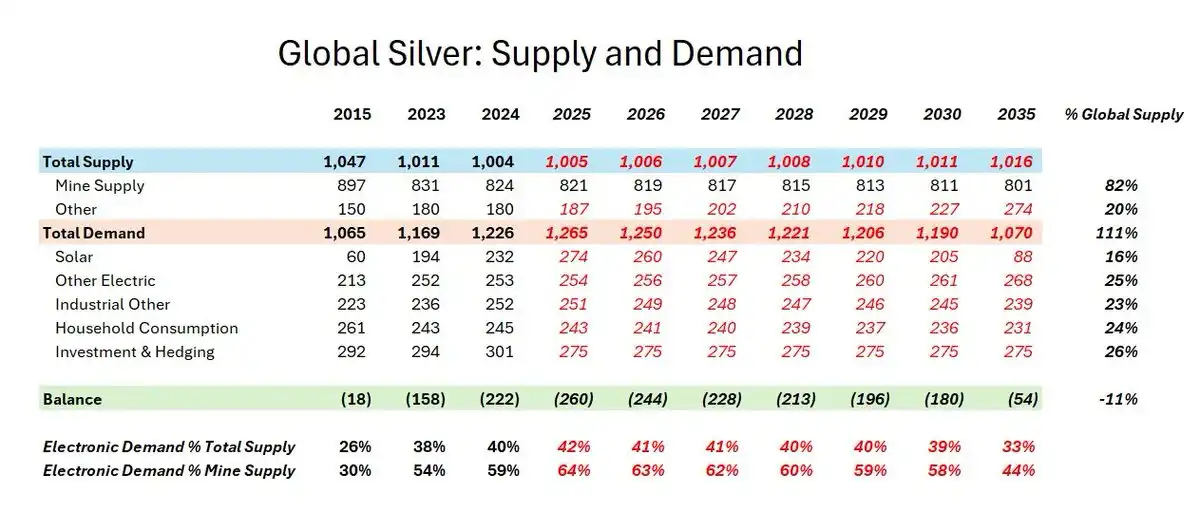

Let's review why we entered this trade—to find assets that could appreciate due to capital outflows from China. Including recycling, the global annual silver supply is only about 100 million ounces. At $100 per ounce, this represents a multi-billion-dollar market. Meanwhile, China's "printing press" adds about $3 trillion in new bank deposits each year. Now that the secret of real estate no longer being a safe store of wealth is widely known, even a small shift in saving behavior could be enough to disrupt the silver market.

This is exactly what you see right now.

If you are a wealthy Chinese family, would you prefer to put more money into a zombie banking system with trillions of hidden losses, or would you rather buy physical silver at high prices and risk a 30% drawdown? When your other option is depositing money in technically insolvent banks, the answer is obvious.

Chinese property bonds were sold off again. Stocks in our "Worst Chinese Banks" basket are also turning negative.

Funds from India and the Middle East are also flowing in. If you were an Indian oligarch, would you want to hold wealth in a currency that has depreciated more than 20% against the US dollar since 2020?

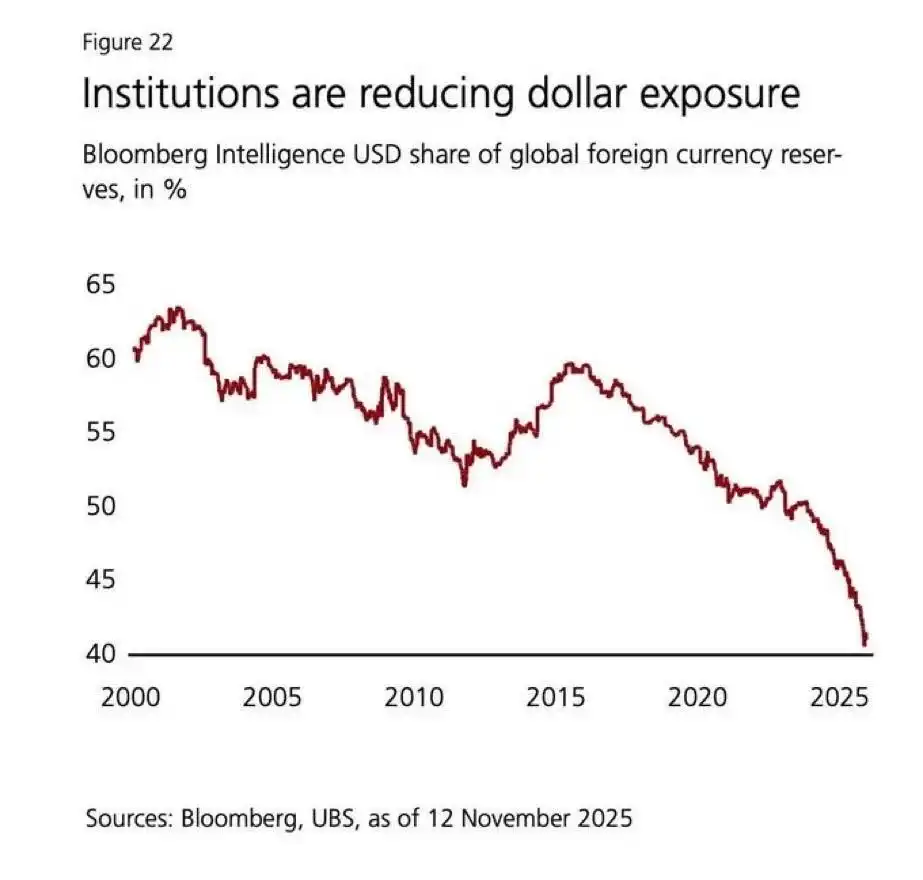

European institutions are finally waking up. If you are a European pension fund with 40% of your assets allocated to U.S. bonds and stocks (many of which are illiquid and overvalued—such as private equity, venture capital, and private credit), you have been underweight in metals for years. Now, you have both political reasons to diversify, and your investors are questioning why you missed this move.

Official purchases seem inevitable. Asian demand appears insatiable. The rebalancing trades that suppressed retail demand at the end of last year are now a thing of the past. ETF inflows remain strong, though still below historical highs.

At this moment, the question seems no longer whether the government will establish a silver strategic reserve, but rather when it will begin.

Why Are We Still Long?

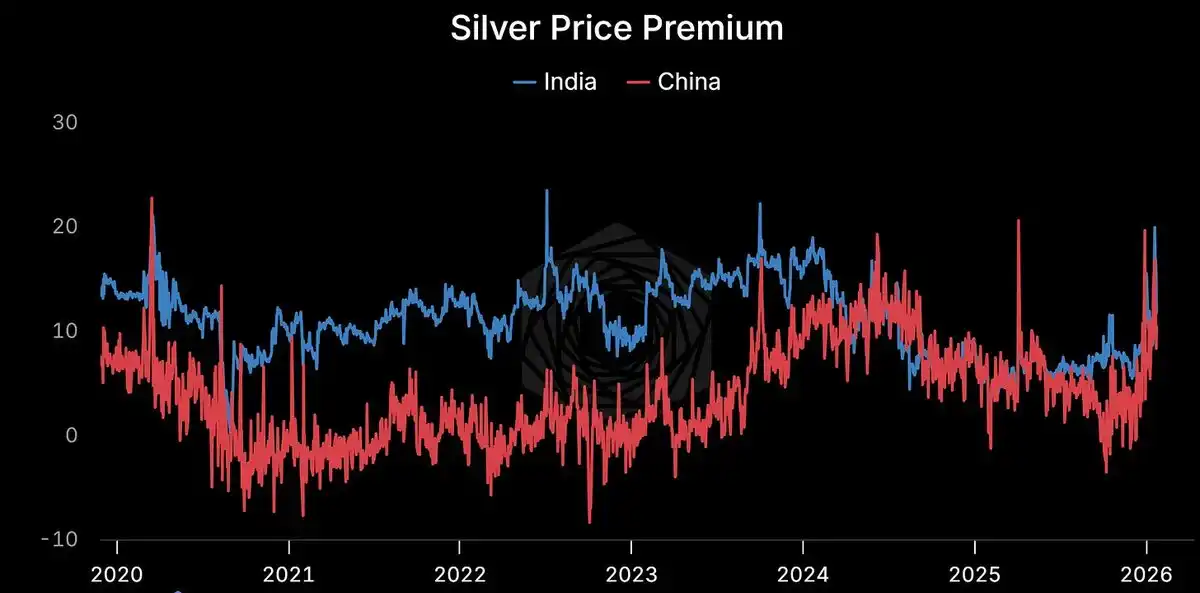

The premium continues to exist.

Shanghai: $114/ounce. COMEX: $103/ounce. Premium exceeds 10%. Persistent. Structural.

When physical commodity prices deviate so greatly from paper prices, one side must be wrong. History tells us it's usually not the physical commodities.

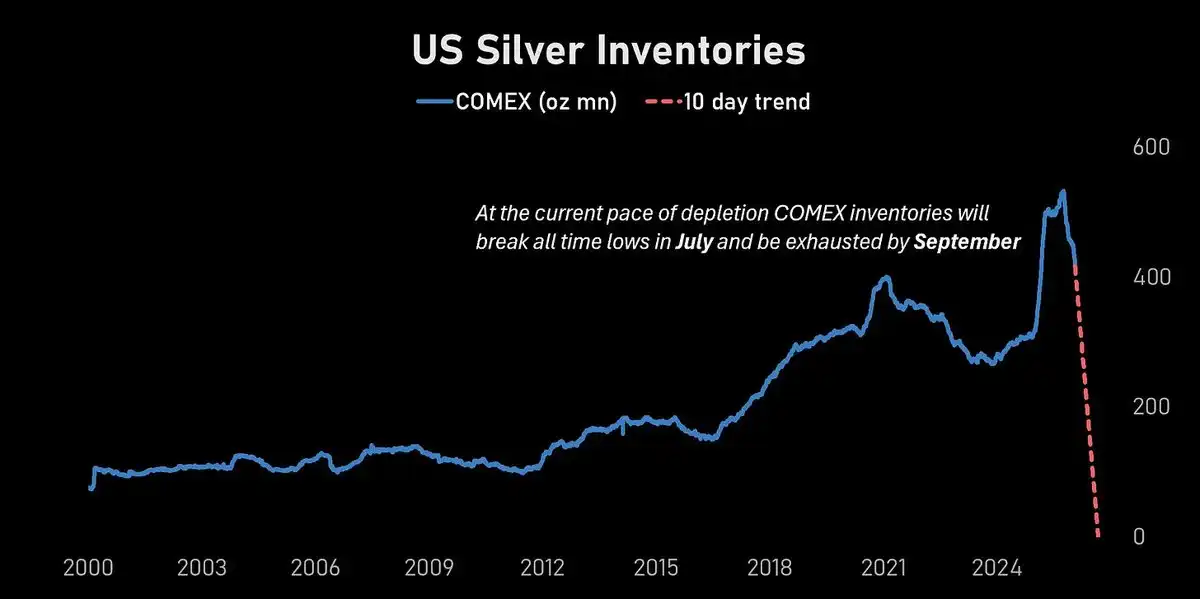

COMEX inventory is plummeting.

At the current rate of consumption, COMEX inventory will reach a historical low in July and will be functionally depleted before September.

In a market with an annualized volatility rate of 70%, it's hard to see that far ahead. But the direction is clear.

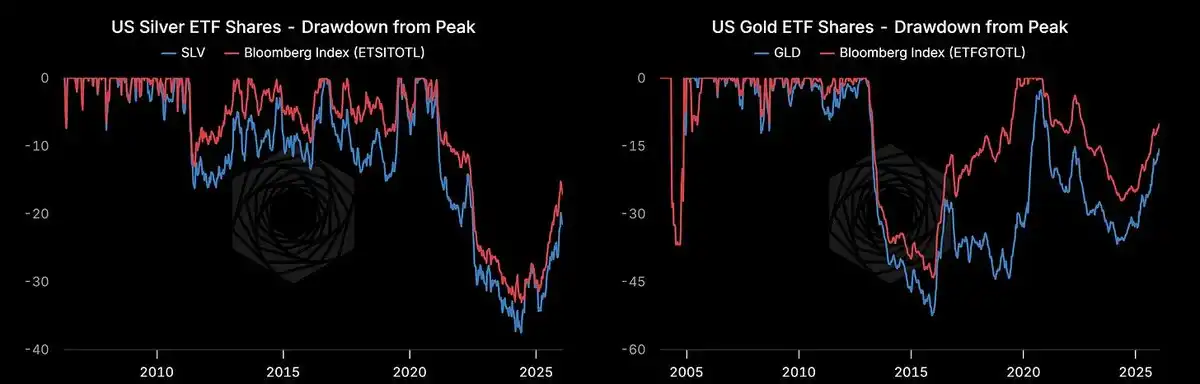

There is still room for ETF fund flows.

Shares of the U.S. silver ETF are rising but are still about 20% below their 2021 peak. We have not yet reached a speculative frenzy.

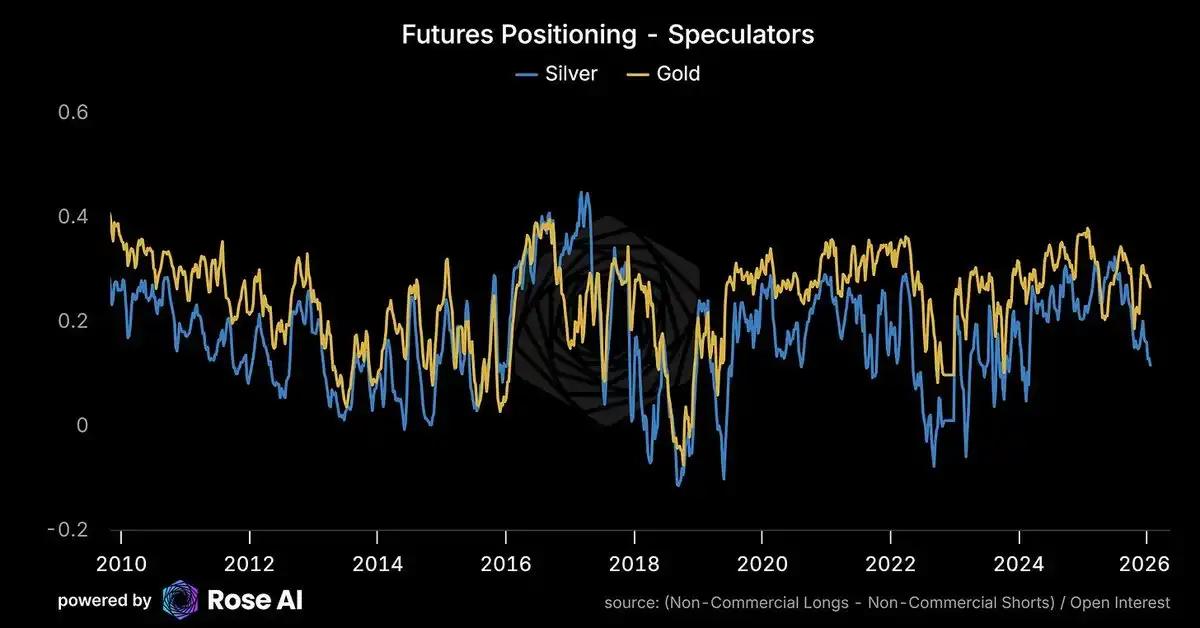

Speculative positions are not crowded.

Western speculators actually reduced their long positions and attracted short positions as prices broke through historical highs. The positioning is not extreme.

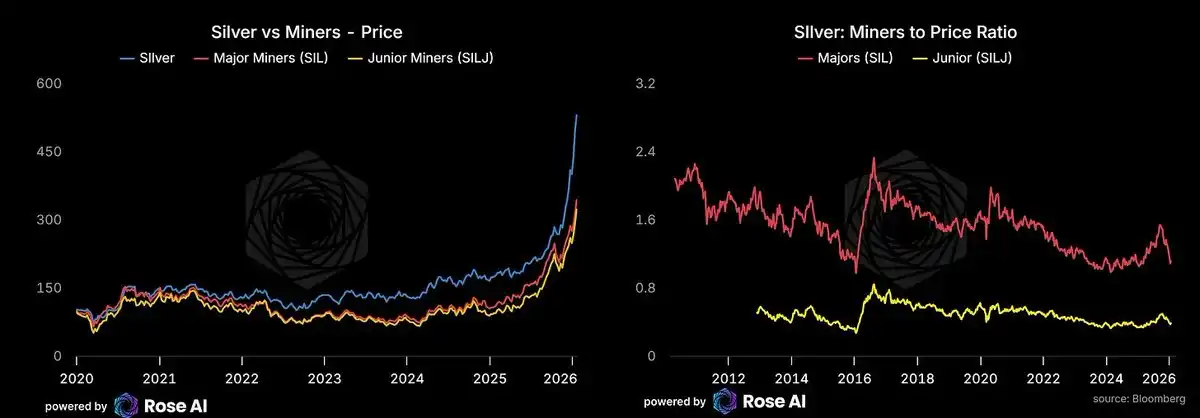

Mining stocks underperformed.

Mining stocks are catching up but still underperforming the commodities they represent. If energy prices remain low (keep an eye on the Strait of Hormuz), mining stocks could experience a catch-up rally. We take long positions in junior miners through equities rather than options—mining stock options have volatility that appears expensive relative to realized volatility.

AI Acceleration Accelerates

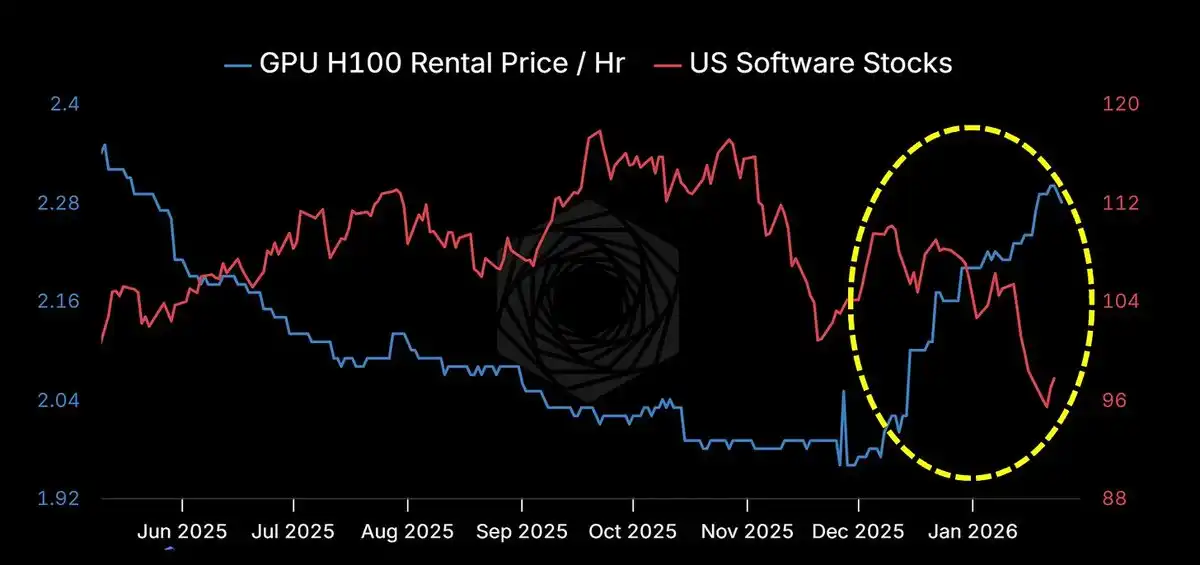

Claude Code and its imitators/branches (Codex, Ralph Wiggins, Clawdbot) are revealing the true face of "agents." The focus isn't on complex workflows, but on crossing the trust threshold: you grant the machine full access to your computer, files, and applications. Hackers and enthusiasts are scrambling to buy Mac Minis. I've built an agent framework (hope to release it this month). Memory modules are sold out. Rental prices have skyrocketed, while traditional SaaS businesses are declining. Perhaps software ate the world, and then GPUs ate the software.

The manifestation of cash flow will take time, but the era of machines has arrived. More machines mean more data centers. More data centers mean greater electricity demand. Greater electricity demand means more solar power.

More solar means more silver.

Potential Risks

A stronger US dollar is a recent risk.

The recent rise has been exacerbated by a weak dollar. If the U.S. economy continues to grow strongly, the substantial expectations of rate cuts implied by the two-year yield curve could be removed, thereby pushing up the dollar. The dollar's weakness over the past few days has undoubtedly intensified this recent upward move.

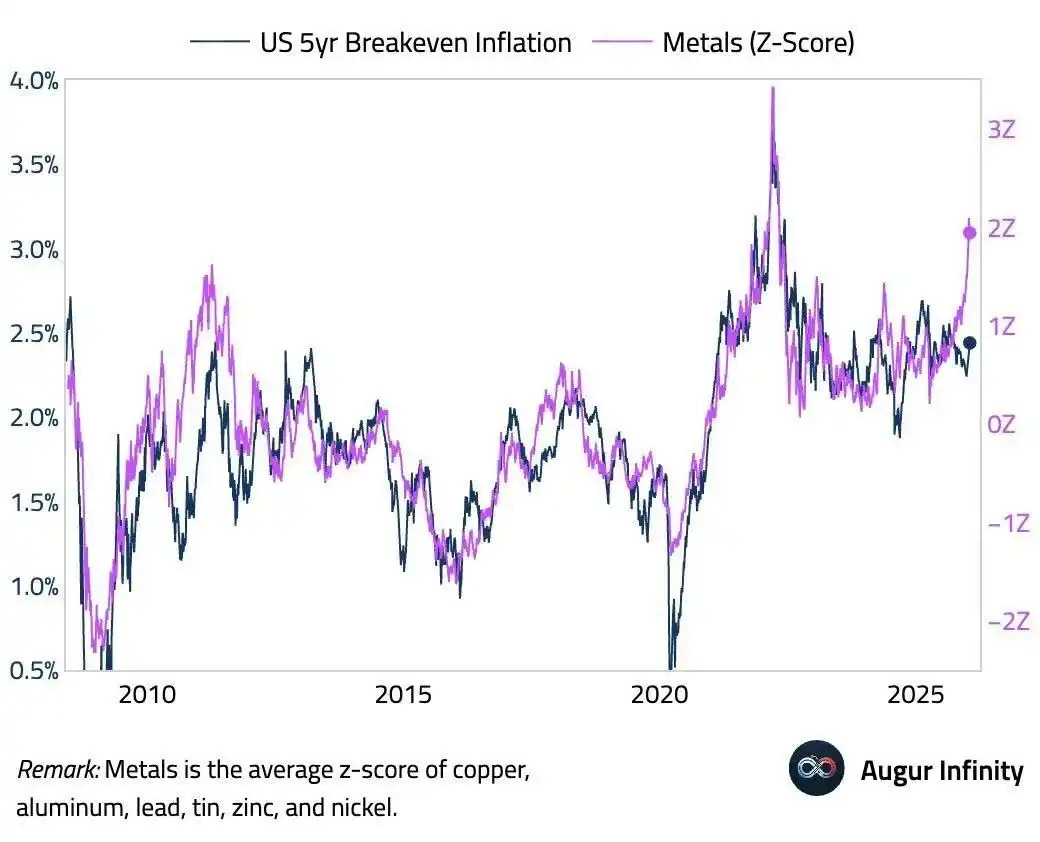

Stronger U.S. dollar + high prices = panic selling by weak holders. Those speculators who chased higher prices above $100 are different from Chinese households who have been accumulating since $30. Weak holders will cut their losses during sharp reversals. If the chart below is correct, we are currently seeing a divergence between metal prices and break-even inflation reaching extreme levels. This may be realigned through higher interest rates/dollar strength and lower metal prices.

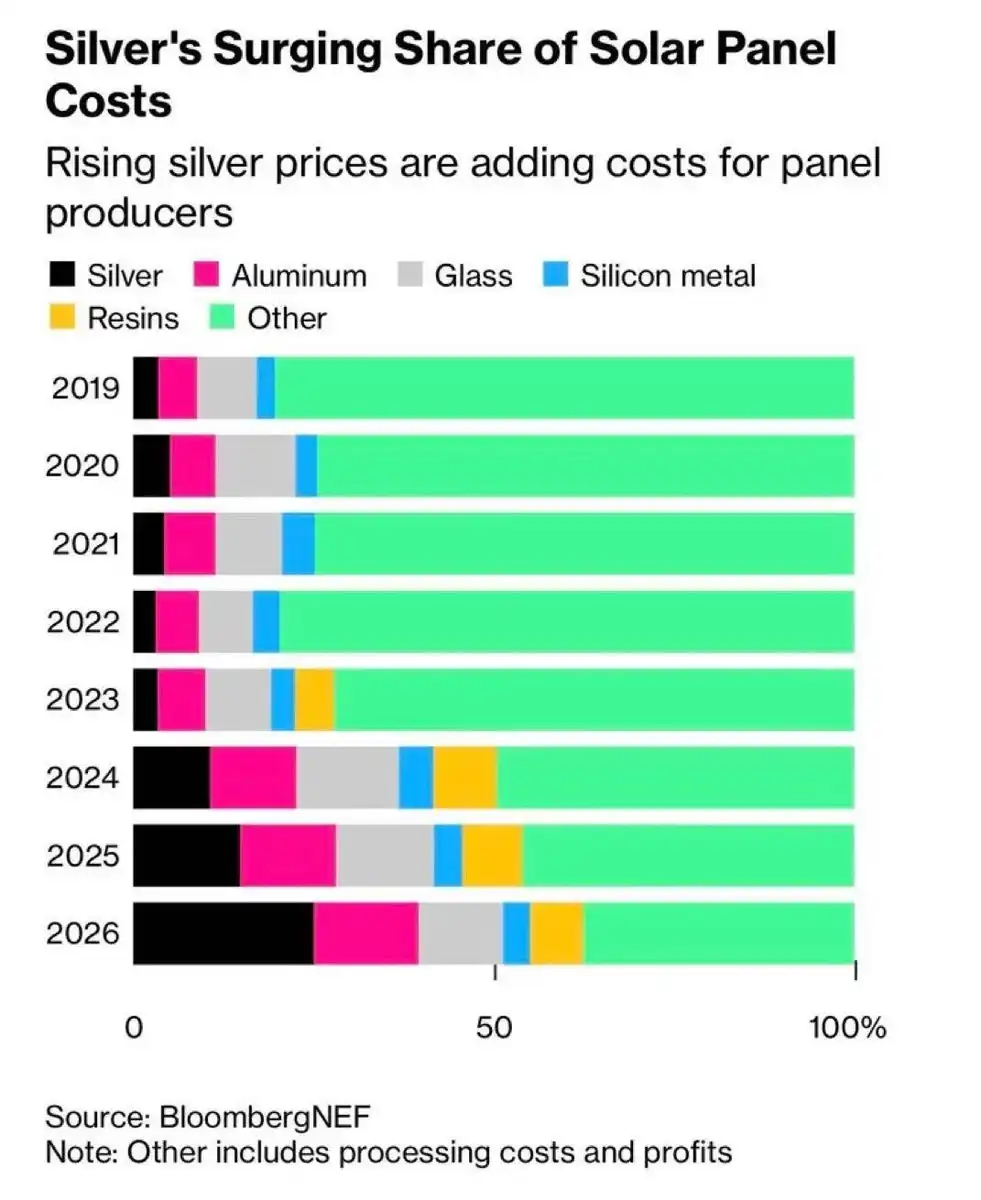

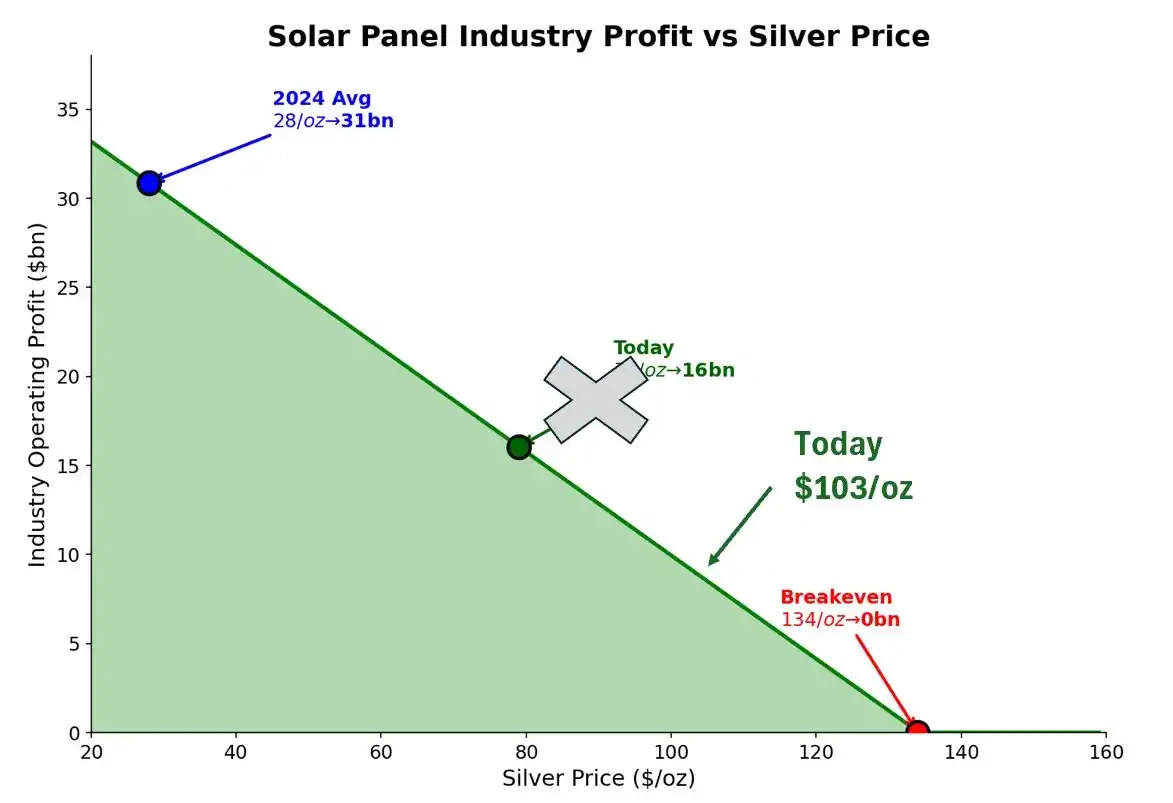

Silver prices are beginning to erode the profit margins of the solar industry.

At a price of $1,030 per ounce, this margin of error is no longer negligible for panel manufacturers. We are approaching a painful threshold.

At $28 per ounce (the 2024 average price), the industry's profit was $31 billion. At today's price of $103, profits could shrink to between $8 and $10 billion. The breakeven point is at $134 per ounce—just 30% above the current price. In a market with annualized volatility of 70%, this is not a comfortable margin of safety.

Copper substitution is accelerating.

The current price is $22 lower than $125 (at which price point the payback period for copper substitution investment drops below one year). At that time, the issue of conversion will be discussed at every board meeting.

Economics is shouting, "Switch immediately." But physics tells us it will take at least several more years to achieve a 50% transition. This is the time window.

Where does the marginal supply come from?

Not miners—supply is rigid and takes years. Not bullion producers—this is a physical market, you can't "mint" metal like issuing overpriced stocks. That leaves only recycling and melting down jewelry. If anyone knows a good silver recycling company, please contact me.

Our Focus

Signal:

Shanghai's premium persists = structural demand, not noise

COMEX inventory drawdown speed = If accelerated, the risk of a near-month contract squeeze increases.

USD direction = A stronger U.S. economy boosts the USD index, leading to the liquidation of weak positions.

Mining stocks catching up = When mining stocks start outperforming the spot price, retail investors are entering the market.

Official Statement: The first central bank to announce the establishment of a silver reserve will trigger a buying frenzy.

Framework:

Focus on the flow of funds, not the price.

If the physical demand from the East continues to buy in, while Western speculators flee due to a stronger U.S. dollar, it's a sign of accumulation. Buy on dips.

If the China premium collapses while COMEX inventory stabilizes, the short squeeze is unwinding. Take profits.

Trading Strategy

The price is already high. There is still demand for upward volatility.

When the spot price broke through the middle strike price, we closed half of the butterfly spread. This structure was specifically designed for this market move, and we have already realized profits.

Remaining Position:

Go long on gold through stocks and bullish vertical spreads

Go long on silver through stock, bullish calendar spreads, and butterfly arbitrage after rolling over positions

Go long on junior miners through stocks (not options — too expensive)

Hedge metal risk exposure by using UUP to gain multiple dollars.

Using put options and short selling SPY, HYG, TLT

We are long the COMEX near-month (March) contract and short the June contract—betting on declining inventory. Rollover may be needed.

Net Exposure: Maintain a long position, but through options. As the spot price rises, adjust the strike price upward. Wait for official and institutional buyers to catch up with the price trend.

Key Conclusions

As prices rise in a parabolic manner, we are gradually reducing our delta risk exposure. However, we will continue doing so until we observe any of the following combinations:

a) China Actively Addresses Real Estate Debt Crisis

b) The United States turning to fiscal responsibility

c) A more peaceful world (Ukraine, Taiwan, Iran)

d) Non-Western elites reach some kind of agreement with the United States

...We will remain long. Although some downside protection will be configured.

The factors that brought us here—capital flight, currency depreciation, solar demand, and supply constraints—have not changed. In fact, they are accelerating.

$103 for silver is not the end. It may not even be the midpoint.

We are beginning to see these same dynamics spreading to other metals. Particularly copper is receiving significant attention from investors who missed the silver rally and are now making rough estimates. The situation is not as dramatic as with silver—it lacks the same monetary/Veblen characteristics—but the story of AI-driven power demand is real, and similar supply constraints exist. We are also long on copper. We'll elaborate on this later.

The silver moon hangs in the sky, everyone.

"Hello, I amOriginal article link"」" is a

Click to learn about BlockBeats' job openings.

Welcome to join the official Lulin BlockBeats community:

Telegram Subscription Group:https://t.me/theblockbeats

Telegram discussion group:https://t.me/BlockBeats_App

Official Twitter account:https://twitter.com/BlockBeatsAsia