Article by Tanay Ved

Compiled by: Chopper, Foresight News

TL;DR

- Amid macroeconomic and geopolitical volatility, the crypto market has continued to face pressure, but improving ETF demand this quarter has provided support for Bitcoin’s current price level.

- On-chain trading platforms and asset tokenization are further driving traditional assets into a 7×24-hour trading market; perpetual contracts on stocks and indices launched by platforms like Hyperliquid, along with newly added stock perpetual products on major exchanges, are steadily increasing open interest.

- The total supply of stablecoins has stabilized around $300 billion, with the adjusted transaction volume rising to approximately $21.5 trillion in the first quarter of 2026; regulatory policies related to stablecoin yields and issuance are gradually becoming clearer, continuing to influence industry development.

The first quarter of 2026 has come to a close, marking a key moment to review the developments and core themes in the crypto market. This quarter, geopolitical and macroeconomic uncertainties intertwined, resulting in an overall risk-off, highly volatile market environment. Despite challenges facing the crypto market—with total market capitalization declining by approximately 22%—tokenized stocks and on-chain trading of traditional assets emerged as industry highlights, while infrastructure saw substantial progress. This article reviews the first quarter of 2026 and analyzes the trends and core themes that shaped the market during this period.

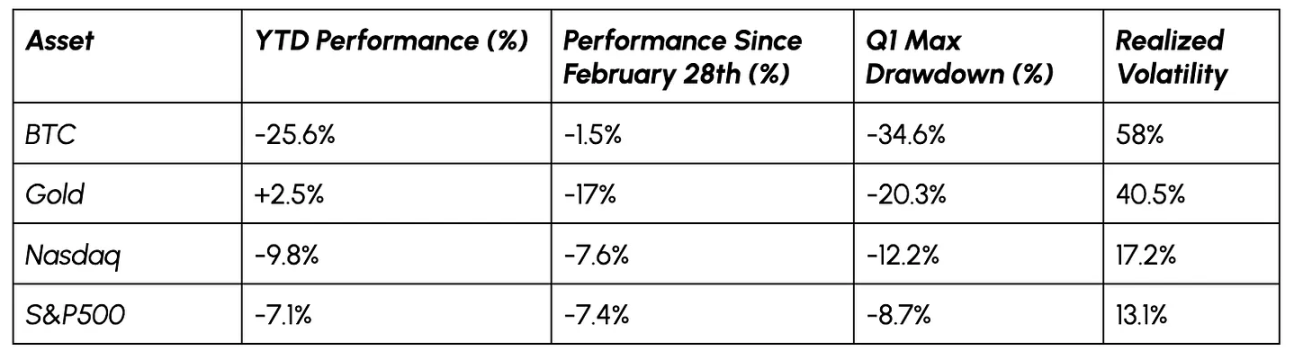

Market Performance

Bitcoin's price dropped over 30% in February from around $95,000, resulting in a 22% decline year-to-date. In addition to macroeconomic pressures, broad selling of risk assets and liquidations in the derivatives market intensified the downturn, reigniting discussions about Bitcoin's safe-haven properties and its role as a store of value.

However, since the outbreak of the conflict in Iran on February 28, Bitcoin has shown greater strength compared to stocks and gold, indicating some resilience and signs of renewed demand.

Data sources: Coin Metrics and Google Finance

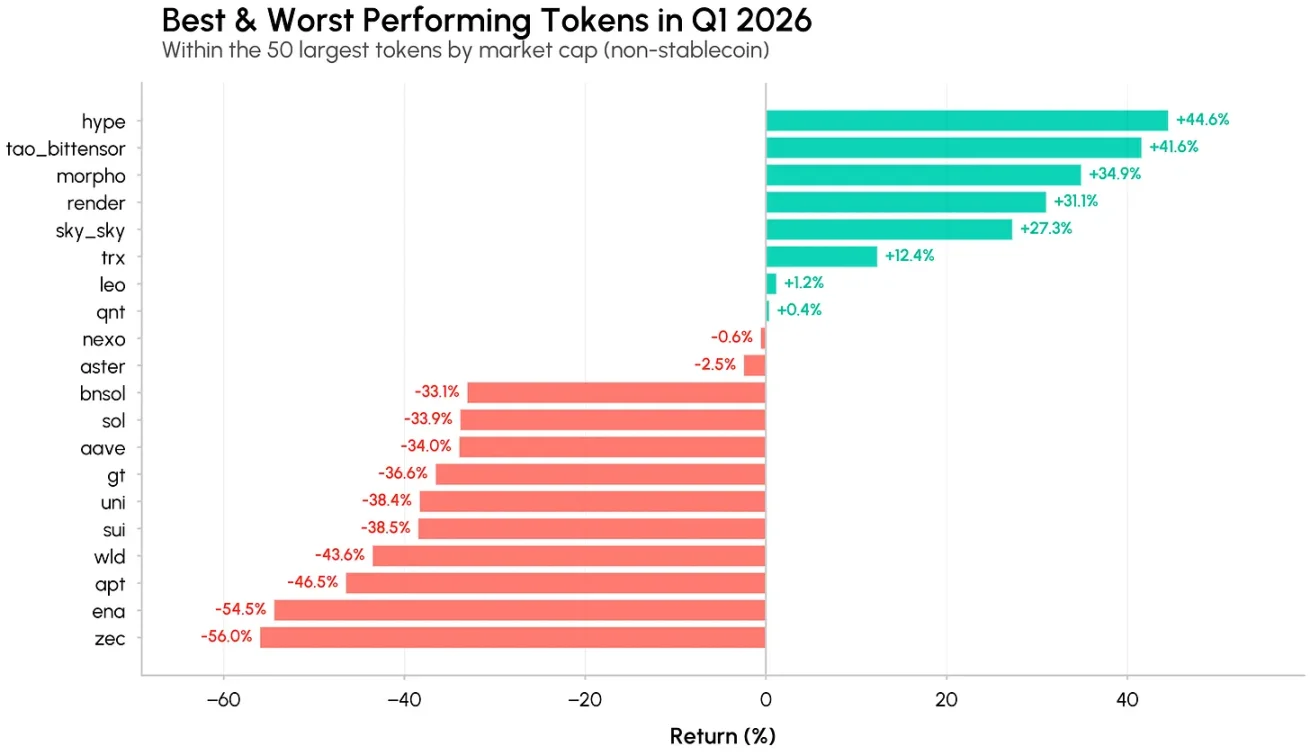

Internal performance among crypto assets has diverged significantly, with only a few altcoins featuring strong narratives and real usage growth outperforming the market.

Top-performing tokens include Hyperliquid (HYPE), Bittensor (TAO), and Morpho (MORPHO), all posting quarterly gains exceeding 30%. Hyperliquid has benefited from the growth of its HIP-3 markets, particularly in commodities and stock indices, expanding its business beyond crypto assets into broader asset classes; Bittensor and Morpho have leveraged growth in AI infrastructure and decentralized finance lending, respectively, as institutional interest in decentralized AI and treasury management continues to rise.

Data source: Coin Metrics

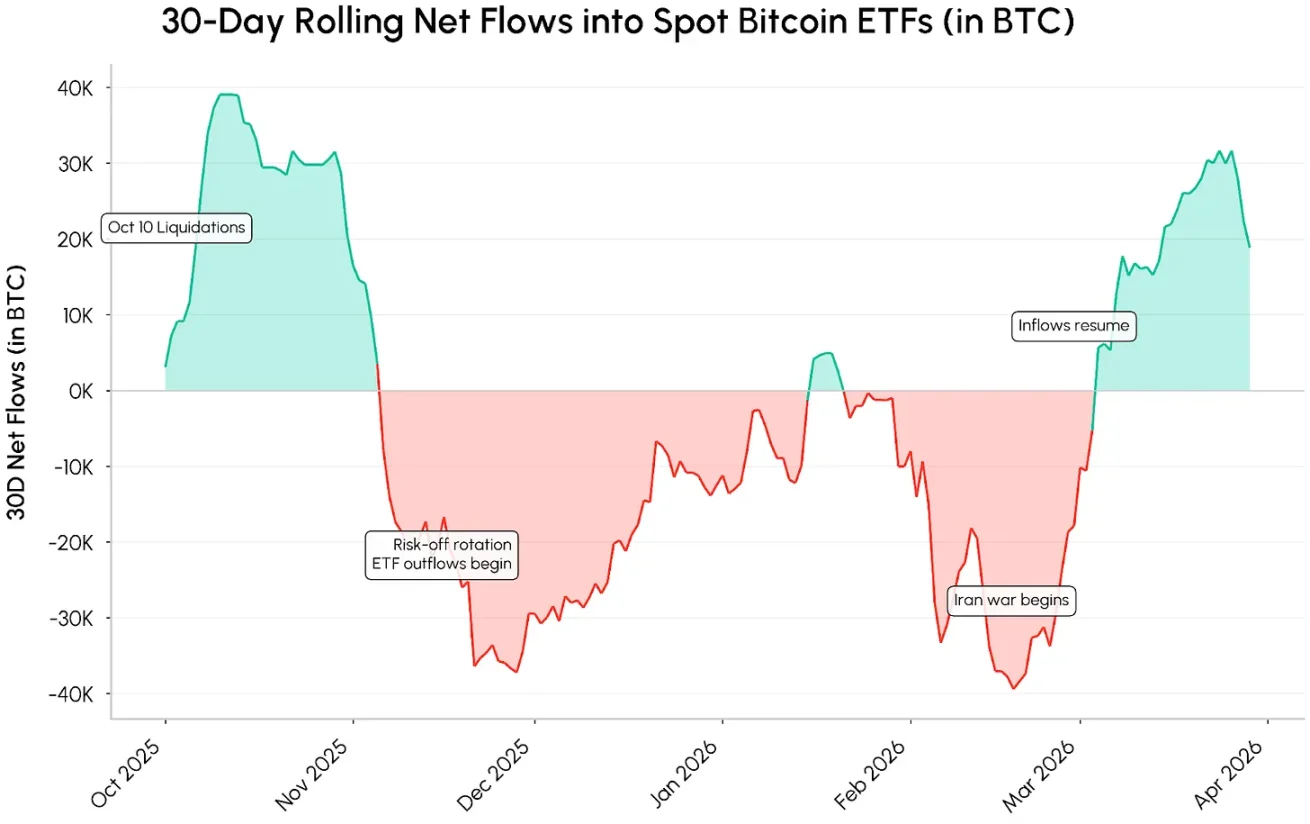

Demand for Bitcoin is gradually stabilizing

The risk-off sentiment at the beginning of the quarter reversed in March. Despite lingering signs of market weakness, demand for Bitcoin spot ETFs improved significantly, reversing the continuous outflows that had persisted since November 2025. Rolling 30-day data shows net inflows into ETFs exceeding 30,000 Bitcoin, supporting Bitcoin’s consolidation near $70,000.

Data source: Coin Metrics Network

The sustainability and acceleration of this demand largely depend on the macroeconomic environment and policy direction. Relief in geopolitical risks, slowing inflation, returning expectations of rate cuts, and continued growth in demand for ETFs and cryptocurrency treasury allocations (including institutional initiatives such as the $42 billion Bitcoin fundraising plan by Strategy) are all expected to further reinforce capital inflows.

24/7 on-chain markets and tokenized stocks

Hyperliquid and the traditional assets sector

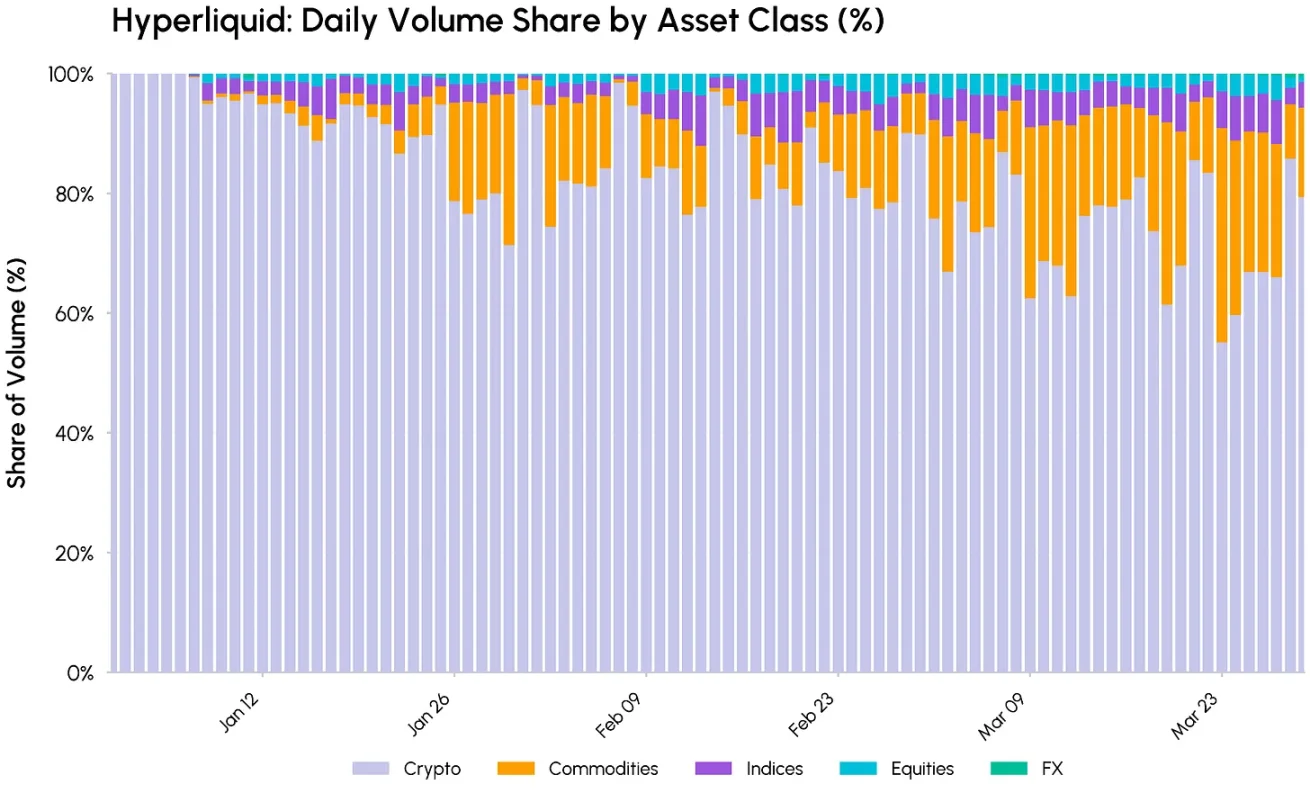

One of the key trends this year is the accelerated convergence between traditional financial markets and on-chain infrastructure through asset tokenization and round-the-clock trading. The growth of perpetual contracts on traditional assets is the most direct manifestation of this trend.

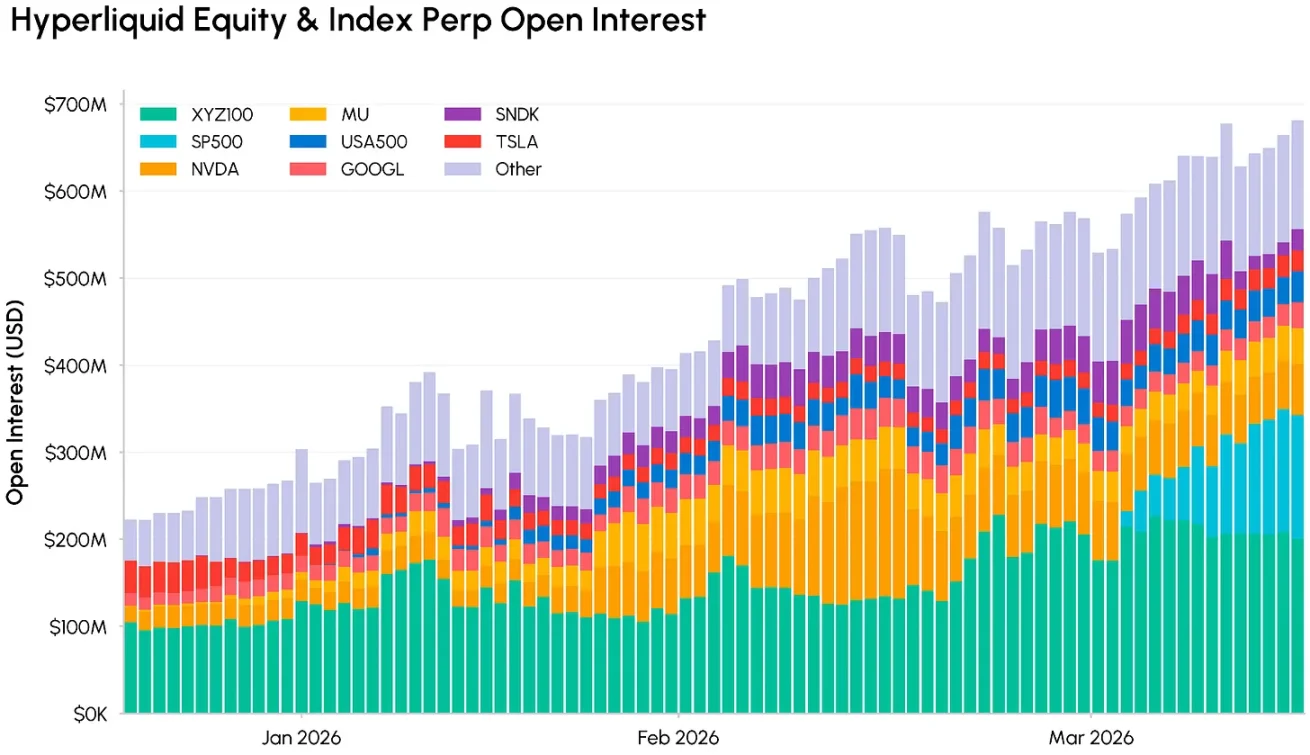

After launching HIP-3 markets covering stocks, indices, commodities, and other asset classes, Hyperliquid saw the share of non-crypto asset trading volume rise significantly to approximately 45% this quarter. Amid geopolitical tensions, traders sought round-the-clock exposure to assets such as metals and crude oil, driving substantial growth in overall platform trading volume and open interest; open interest in HIP-3 traditional assets accounted for about 28% of the platform’s total.

Data source: Coin Metrics

The Rise of Stock Perpetual Contracts

In this niche, as trading platforms expand their offerings, mainstream stocks and indices have become the fastest-growing category. Kraken launched xStocks stock perpetuals in February, while Coinbase International introduced stock perpetual products, providing investors with leveraged exposure to U.S. equities. Meanwhile, [XYZ], the largest deployer of Hyperliquid’s HIP-3, partnered with S&P Dow Jones Indices to launch the first official S&P 500 perpetual contract, further enriching the global market for stock exposure trading.

Data source: Coin Metrics

Open interest for Hyperliquid's stock and index perpetual contracts has been steadily rising, with core indices such as XYZ100 (Nasdaq 100) and the S&P 500 now among the platform's most heavily traded products, and individual stocks like NVIDIA (NVDA) and Micron Technology (MU) also generating significant liquidity.

Meanwhile, tokenized stocks and funds are growing in tandem, from the xStocks framework to tokenized money market funds and equity funds issued by institutions such as Ondo on Ethereum and Solana.

The growth of tokenized stocks and real-world asset (RWA) perpetual contracts underscores a trend: on-chain platforms are increasingly becoming a 24/7 extension of traditional markets, rather than merely crypto-native trading venues.

Stablecoins: Stable supply with growing practicality

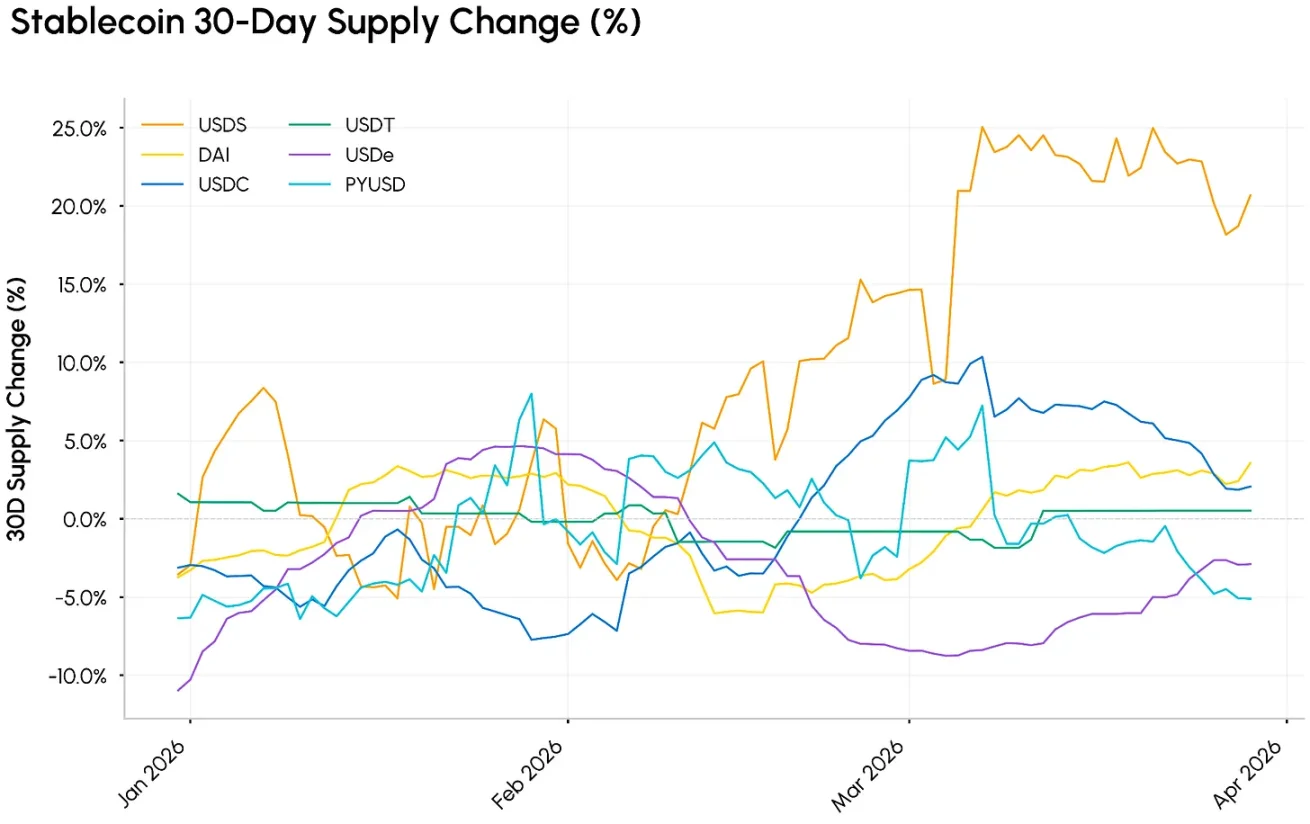

Stablecoins continue to serve as the foundational pillar of on-chain liquidity. Despite the overall market decline, the total supply of stablecoins remained stable around $300 billion in the first quarter of 2026, with a slight rebound in supply growth on February 30.

The most prominent growth among stablecoins is USDS, a USD-pegged stablecoin issued by Sky Protocol (formerly MakerDAO), collateralized by both crypto and real-world assets, with its supply increasing 43% to approximately $8 billion; USDC, issued by Circle, has a market size of $77 billion, while USDT remains stable at around $184 billion.

Data source: Coin Metrics

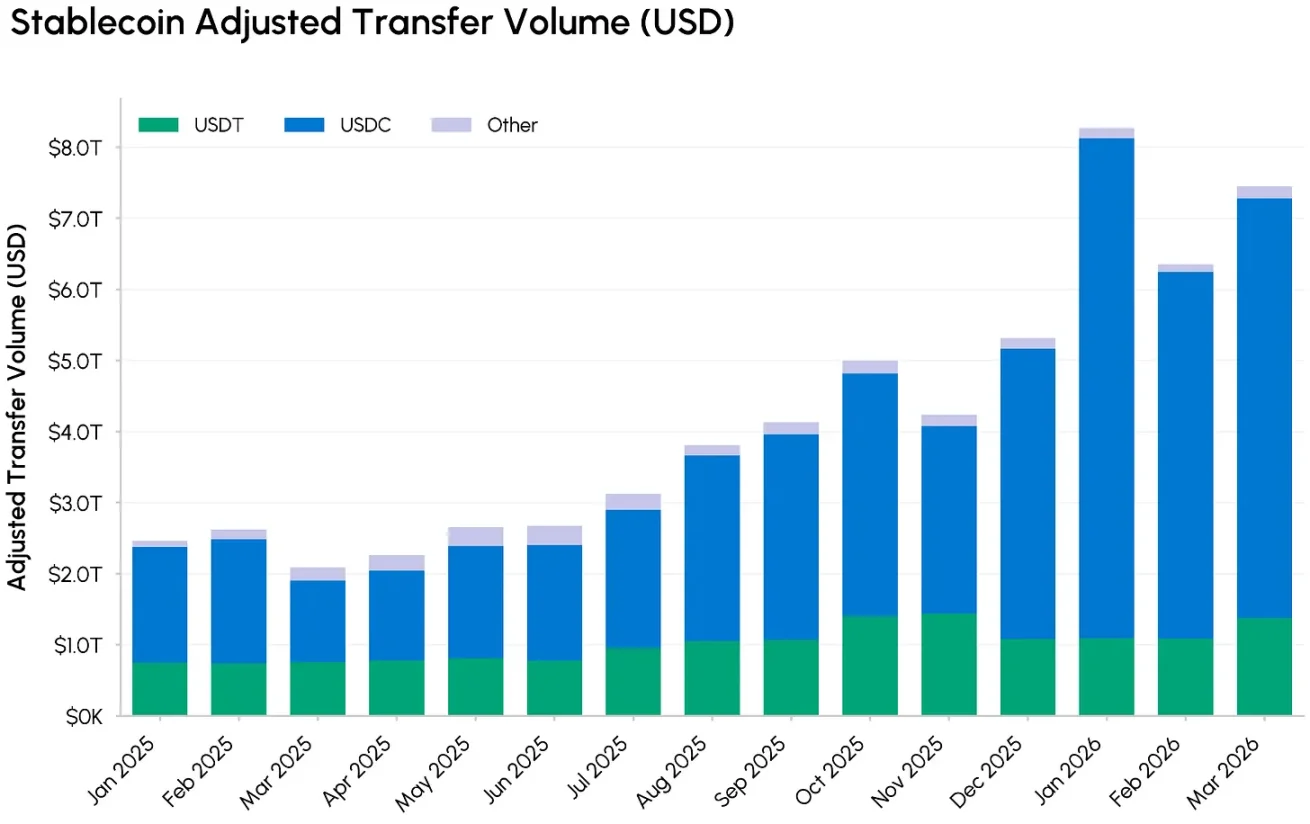

While supply remains stable, the velocity and scale of stablecoin usage have significantly increased. The adjusted total stablecoin transfer volume in Q1 reached $21.5 trillion, approximately three times that of the same period in 2025. Over 80% of this volume came from USDC, whose share of transaction usage continues to expand relative to USDT. This activity is primarily driven by USDC on the Base chain, which alone accounted for $13 trillion in Q1 transfers.

As we analyzed in our recent report, a large portion of this capital flow stems from DeFi infrastructure activities such as liquidity provider rebalancing and flash loans, rather than end-user payments or settlements, although the latter scenarios are also growing simultaneously.

Data source: Coin Metrics

In the future, the direction of the stablecoin industry may depend on yield mechanisms and issuance rules. The latest draft of the CLARITY Act proposes prohibiting passive yield on stablecoin balances, while permitting activity-based rewards tied to payments or platform usage. This provision could transform the business models of core participants.

For Coinbase, where stablecoin income already accounts for more than 25% of total revenue, limiting USDC yields could weaken its ability to attract and retain funds; Circle, by contrast, would be less affected, and its payment and transaction-related revenues could benefit if high interest rates persist and regulatory frameworks become clearer. As the bill progresses, its impact on DeFi lending, yield-bearing stablecoins, and tokenized treasuries warrants continued attention.

The U.S. SEC releases a framework for classifying digital assets

This quarter, important regulatory clarity emerged. The U.S. SEC and the Commodity Futures Trading Commission (CFTC) jointly released an interpretive document, introducing a five-category framework for digital assets and clarifying the classification of each type under existing securities and commodities regulations:

- Digital goods: Native tokens of core networks, whose value primarily depends on the functionality of the cryptographic system and market supply and demand (such as major public chain tokens), classified as commodities rather than securities.

- Digital collectibles and tools: NFTs, in-game assets, gas fee tokens, and access tokens generally do not fall under securities regulations unless they are fractionalized or primarily marketed as investment products.

- Payment stablecoins: Fiat-backed and real-world asset-collateralized payment stablecoins are considered monetary instruments, but variants with yield features or non-compliant designs still require securities classification review.

- Digital securities: instruments such as tokenized stocks, bonds, and credit-related real-world assets, all of which fall entirely within the securities category, regardless of whether they are on-chain or not.

- Staking, mining, and wrapping: Native staking, mining, airdrops, and wrapping activities are not securities transactions; however, pooled staking, yield wrapping/structured tokens may be classified as investment contracts if they make yield promises to investors.

To gain deeper insights into the new token classification framework, the progress of CLARITY Act negotiations, and global regulatory developments, refer to Talos’s latest report, Regulatory Review.

Conclusion

Although cryptocurrency prices remain significantly influenced by macroeconomic and geopolitical factors, the underlying infrastructure of the industry continues to evolve. Bitcoin is gradually gaining support at current price levels, while on-chain platforms are further expanding into 24/7 trading markets for equities, commodities, and real-world assets. Meanwhile, traditional giants such as the NYSE and Nasdaq are actively investing in tokenization, driving the modernization of equity trading systems. The progress of the CLARITY Act and regulatory policies related to stablecoin yields will become key industry variables; if the macroeconomic environment improves, risk appetite for cryptocurrency assets is expected to gradually recover.