Author: Chloe, ChainCatcher

On March 23, Polymarket officially announced an updated Market Integrity Policy, applicable simultaneously to its DeFi platform and its U.S. exchange regulated by the CFTC. The new rules explicitly prohibit three categories of insider trading and strengthen the framework for combating market manipulation. This policy adjustment did not arise in a vacuum; it is the result of a series of controversies and public pressure, as well as Polymarket’s proactive compliance effort ahead of intensified regulatory scrutiny from U.S. financial authorities.

However, the new regulations affect not only genuine insider players—do they more directly threaten the interests of the large group of users seeking free rewards, or the professional arbitrageurs who truly provide liquidity?

The historical pressure behind the rule upgrade: from the Venezuelan coup to the Iranian war

Look back at the public opinion and regulatory pressures Polymarket has endured over the past several months. In early January 2026, an anonymous user spent $32,537 on Polymarket to bet that Maduro would step down before January 31. Immediately after Trump announced on Truth Social at 4:21 AM that Maduro had been arrested, the user received a return of $436,000, achieving a return on investment of more than 13 times.

The investigation found that the account was only created in December 2025, with all bets precisely targeting Venezuela’s political situation, placed just hours before the events unfolded. Dennis Kelleher, co-founder of Better Markets, noted that this transaction exhibits all the hallmarks of insider trading: a newly created account, large sums of money, precise timing of predictions, and all occurring within an unregulated and opaque market.

Coincidentally, around the same time, suspicious trades appeared on Polymarket targeting the timing of U.S. military action against Iran, with certain accounts precisely establishing positions just before the U.S. military strike, earning hundreds of thousands of dollars.

Notably, Polymarket CEO Shayne Coplan once made a thought-provoking statement in an interview with CBS News: "It's a good thing that insiders have an advantage in the market."

However, in March 2026, Senator Adam Schiff and Senator John Curtis introduced bipartisan legislation aimed at banning trading contracts that resemble “sports or casino games.” In the same month, the Commodity Futures Trading Commission (CFTC) issued guidance requiring prediction market platforms to implement specific measures to prevent insider trading and encouraging exchanges to proactively consult with regulators when designing event contracts to identify risks of manipulation or price distortion.

Regulatory pressure has already taken shape, and Polymarket’s policy upgrade is a proactive response to this crackdown.

New Regulations Analyzed: Three Prohibitions and a Multi-Layered Monitoring Framework

Polymarket officially released updated Market Integrity Rules on March 23, 2026, clearly defining three red lines: first, trading based on stolen confidential information; second, trading based on illegal sources of information; third, trading by individuals who influence the outcome.

At the level of market manipulation, regulations explicitly prohibit behaviors such as spoofing, wash trading, and fictitious transactions. In response to these prohibitions, ChainXue Society, in an interview with ChainCatcher, stated that the boundary between wash trading and legitimate trading lies in whether real value is generated and whether trading costs are borne. Wash trading involves the same individuals transferring assets between their own accounts purely for data manipulation, while legitimate arbitrage or market making involves placing limit orders at different prices and assuming position risk, with each transaction executed against genuine market participants and subject to scrutiny.

On the architectural level, Polymarket employs a "multi-layered monitoring" design. On the DeFi platform side, all transactions are recorded on the Polygon chain and are publicly accessible to anyone; the platform collaborates with world-class monitoring technology firms to detect on-chain anomalies. Upon identifying suspicious activity, available sanctions include freezing wallet addresses and referring users to law enforcement authorities.

On Polymarket US (a CFTC-regulated exchange), monitoring is conducted in three layers: external monitoring technology partners, a real-time monitoring desk, and a regulatory services agreement with the National Futures Association (NFA), which has the authority to directly investigate and sanction violators through measures such as suspension of privileges, account termination, monetary fines, or referral to regulatory authorities.

The interests of "grabbings" users and the challenges faced by related studios?

Polymarket’s move is a blow to “insider players,” but may spark different reactions among arbitrage users and related studios. In response to the new rules, the reactions of major market participants are telling. ChainXi Society, which has already achieved over $200 million in trading volume on Polymarket, told ChainCatcher that the new regulations were expected—and even long anticipated. They view this not as an attack, but as a sign of market maturation. Even when the platform first began charging fees, professional teams anticipated that full-market fees and stricter regulation would eventually follow.

For general volume-farming airdrop users, past practices of relying on massive on-chain transaction records and wash trading with dual accounts in a single market are now directly conflicting with new regulations. Some participants have even evolved to operate matrices of 100 wallets or hedge between Polymarket and Kalshi, but upgraded monitoring systems have significantly increased the risks associated with these activities.

ChainXueShe believes that truly high-quality strategies should not be about "plucking hairs" but about genuine arbitrage. Arbitrage itself is the process of identifying price discrepancies and correcting market inefficiencies—healthy behaviors essential for market prediction. As gray-market activities are squeezed out, the market will become cleaner, and professional arbitrageurs may even see higher returns.

The liquidity paradox: Are volume-faking users parasites or infrastructure?

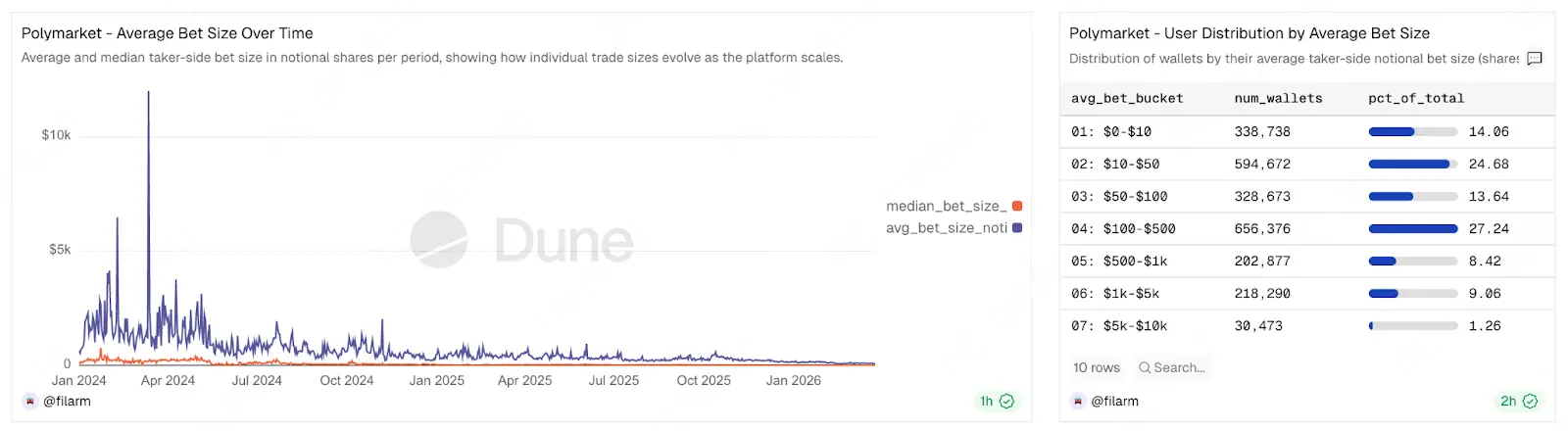

Additionally, behind this wave of regulation lies an unavoidable contradiction for Polymarket: Polymarket’s liquidity is not naturally occurring. On-chain data shows that 80% of users on the platform place single bets of less than $500, and the average single bet amount over the past month has been approximately $100. Thus, market depth is primarily supported by a very small number of large traders and liquidity providers.

It is worth exploring whether the group of airdrop farmers employing "legitimate strategies" (such as providing two-sided liquidity and cross-platform arbitrage) are, objectively speaking, fulfilling the role of informal market makers.

They narrowed the bid-ask spread and enhanced market capacity, enabling ordinary users to enter positions at more reasonable prices. On the business side, after returning to the U.S. market, Polymarket urgently needs a massive volume of real trading activity and deep market data to demonstrate market efficacy to the CFTC (Commodity Futures Trading Commission), which is critical for obtaining further regulatory approvals.

If the new rules are too aggressive and drive away these arbitrage users, a short-term liquidity crunch is almost inevitable, especially in niche long-tail markets where these users are often the only source of counterparty liquidity.

In response, ChainStudy Society stated that platforms should recognize the contributions of users who provide genuine liquidity. For example, with a multi-account system, if a user consistently contributes millions of dollars in daily trading volume entirely through maker limit orders, this is precisely the behavior the platform’s mechanism is designed to encourage. Especially during periods of low volatility and poor liquidity, such orders add depth to the order book, enabling ordinary users to execute trades. This behavior essentially involves exchanging capital and time for rebates while serving the market.

Under regulatory compliance, do related studios also need strategic transformation?

Polymarket's compliance process is not a fleeting market fluctuation, but a signal of the platform's strategic shift.

From acquiring the licensed exchange QCX to signing an agreement with the NFA, all of these developments indicate that prediction markets are moving closer to traditional financial regulation. On this highly transparent and regulated path, the room for traditional “low-quality volume manipulation” will continue to shrink. ChainXue Society believes that the new regulations are actually favorable for professional teams, who will adopt three strategies going forward: first, increase liquidity provision to earn more maker rebates; second, actively engage with platforms to explore deeper market-making solutions; third, continuously optimize strategies to enhance returns within a compliant framework.

Overall, for studios that view Polymarket as a core source of profit, it is now a critical juncture to shift strategic focus from “quantity” to “quality.” Rather than manipulating 100 wallets to engage in low-quality wash trading and risking precise detection and mass bans by monitoring systems, it is wiser to abandon the multi-wallet matrix and instead cultivate a small number of high-quality accounts. Engaging in deep trading based on genuine market research, or focusing exclusively on liquidity provision within the platform’s guidelines, not only effectively mitigates the risk of bans but also increases the likelihood of receiving a more favorable token airdrop allocation by contributing genuine value in the final weighted airdrop calculation.