Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web3_golem)

On April 6, Polymarket announced a major platform upgrade within the next 2 to 3 weeks, including upgrading both CTF and CLOB to V2, and switching the platform's collateral from USDC.e to the native stablecoin Polymarket USD.

According to official documentation, Polymarket USD is 1:1 backed by USDC, and for most users, the transition from USDC.e to Polymarket USD is seamless—the frontend handles it automatically, requiring only a single confirmation click. For advanced users and API-only traders, the transition may involve a few additional steps, but it remains straightforward: they simply need to wrap their USDC or USDC.e into Polymarket USD using the wrap() function of the collateral access contract.

On the surface, Polymarket has simply switched its trading collateral in the background. As the platform grows, continuing to use USDC.e is indeed a risk. In February of this year, Circle and Polymarket announced plans to migrate the bridged USDC.e to native USDC; this is now simply a normal progression of their collaboration.

However, instead of directly introducing native USDC to replace USDC.e, Polymarket added another layer, aiming to keep USDC liquidity within its own pool—this layer is called Polymarket USD. Thus, the introduction of Polymarket USD is undoubtedly a “One more thing” (Odaily note: “One more thing” is a classic tradition at Apple events, now symbolizing a company’s grand finale or industry-disrupting move).

Polymarket holds the minting rights

The first layer of significance of this matter is that Polymarket can hold user funds.

Previously, funds deposited into Polymarket were converted into USDC.e. You can think of Polymarket as a large marketplace that only handles matching, pricing, and settlement—although money flows through it, it does not belong to Polymarket’s system, and Polymarket is not a vault.

But things are about to change: after replacing USDC.e with Polymarket USD, Polymarket can now reach into the funds that were previously just “passing through.” As Polymarket’s official statement notes, users won’t notice any difference in their daily experience, but the underlying on-chain settlement path has already been altered—this shift is equivalent to an exchange transitioning from relying on third-party clearing institutions to building its own clearing center.

Polymarket USD is 1:1 backed by USDC, meaning that for every Polymarket USD in circulation on the market, there is an equivalent amount of USDC in Polymarket’s reserve. Currently, every Yes/No share on Polymarket is backed by USDC.e, which moves on-chain when users place bets or settle outcomes. However, with Polymarket USD, while it still moves on-chain with user activity, the USDC in Polymarket’s reserve remains unaffected. As long as users do not redeem their tokens, these funds are effectively held by Polymarket.

Polymarket, having started as an application for a stablecoin, has now gained control over on-chain minting rights. Polymarket USD draws user assets from the “open sea” into Polymarket’s “internal lake.” Once funds begin to accumulate, Polymarket is no longer just a prediction trading platform—its business model no longer relies solely on transaction fees, as it can now engage in finance’s oldest game: making money out of money.

Increase Polymarket's revenue streams

The second layer of meaning is the expansion of Polymarket's business.

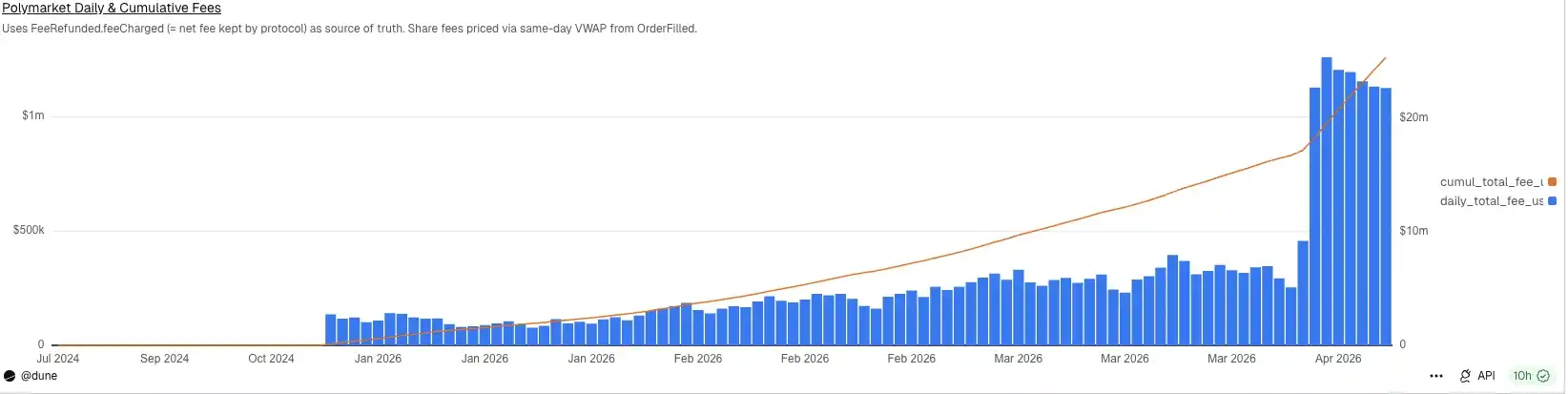

Currently, the business model of prediction markets is straightforward: collecting trading fees. After Polymarket adjusted its fee structure on March 30 (Odaily note: expanded the taker fee scope to include market categories such as Finance, Politics, Economics, Culture, and Weather, in addition to the existing Crypto and Sports categories), Polymarket's daily trading fee revenue has exceeded $1 million.

Polymarket daily fee revenue

While substantial, this is still not enough to satisfy Polymarket’s ambitions. Although prediction markets are currently the most sought-after sector, their business model has a relatively low ceiling, and the project’s moat is quite narrow (regulatory licensing), with low user retention. In a landscape where everyone is building prediction markets, what ensures that Polymarket won’t be surpassed by competitors in the future?

Now the answer it gives is: I don't just match trades—I can also put players' funds to work.

From a business perspective, the most attractive aspect of stablecoins over the years has never been fast payments or transfers, but rather the quiet, highly profitable money-printing machine behind them—the yield on reserve assets. In 2025, the vast majority of Circle’s revenue still comes from reserve income. Polymarket understood this model, which is why it launched Polymarket USD.

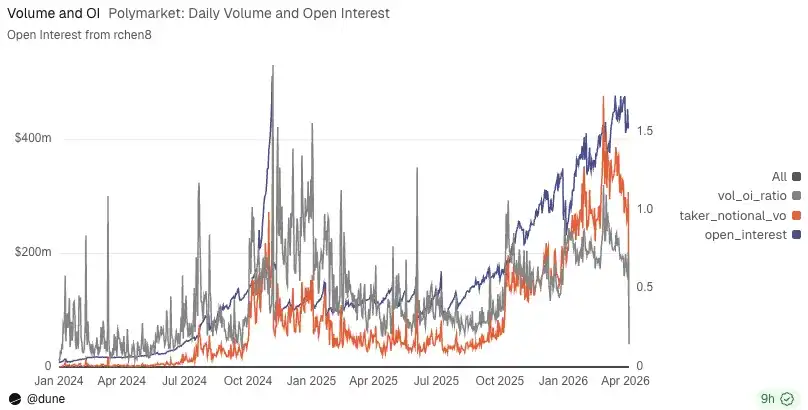

According to Dune data, the open interest on the Polymarket platform has exceeded $400 million. If all this money were converted into Polymarket USD, Polymarket could simply deposit the underlying USDC collateral into Circle’s institutional account or allocate it to U.S. Treasury protocols, earning an annual risk-free interest of 4%-5%—generating tens of millions of dollars in “interest tax” with no active effort.

DefiLlama founder 0xngmi even published a post directly stating that approximately $1.25 billion in user funds are held in Polymarket wallets; if these users retained this interest income, they would earn an additional $54 million annually at current rates. Polymarket could even participate in DeFi yield products with higher APYs, turning idle funds on its prediction platform into active leverage and returning the matured earnings to users, effectively providing them with a form of hedging.

Polymarket daily open interest and trading volume chart

Prediction markets naturally have two characteristics: capital stagnation and high-frequency reallocation driven by events. Users’ funds don’t instantly enter and exit like in a casino—they’re either already positioned or sitting idle in accounts, waiting for the next event or the next odds shift. This type of capital is ideally suited for financial repurposing, and for users, it offers a compelling justification: improving capital efficiency.

Of course, Polymarket hasn't publicly stated that it will definitely offer yield extraction or on-chain financial products after launching its stablecoin. But this path is almost inevitable—once Polymarket USD grows in scale, it will naturally have the opportunity to manage yields, expand collateral, and create in-platform financial products.

Earlier, the CLARITY Act faced opposition due to its potential ban on crypto companies offering interest-bearing stablecoins to users; if the outcome remains a prohibition, all the above speculation about Polymarket USD’s potential would vanish. However, on April 6, according to U.S. media reports, the core disagreement between U.S. crypto and banking sectors over stablecoin yield mechanisms may be nearing resolution. Although details have not been disclosed, overall expectations are turning optimistic, and the CLARITY Act may enter committee review by late April.

So, don't think Polymarket is far away from this.

Polymarket controls the distribution of USDC

The launch of a stablecoin by Polymarket has a third-layer significance: control over USDC distribution.

Today, Polymarket remains a major distribution channel for the USDC ecosystem: Circle provides native USDC, and Polymarket distributes it—both parties benefit harmoniously. As Polymarket continues its rapid growth, its platform’s accumulated USDC reserves will undoubtedly grow larger, potentially becoming a distribution channel as significant as Coinbase. When that time comes, the relationship between Polymarket and Circle may change.

A reality in the world of stablecoins is that issuance rights are as important as distribution rights, which is why Coinbase captures over half of Circle’s reserve income. Therefore, when Polymarket becomes a major distribution channel for USDC, it will inevitably gain bargaining power and be entitled to a significant share of the reserve earnings. Moreover, as Polymarket USD matures sufficiently, it could explore multi-reserve-backed stablecoins rather than relying solely on USDC.

This is why I believe Polymarket USD is not just a routine upgrade for Polymarket, but a redefinition of its identity. Polymarket will evolve from a platform that charges fees on event-based volatility into one that also organizes and settles transactions around the US dollar.

The former is casino logic, while the latter is banking logic.

Polymarket’s moat has thus grown even stronger. It still maintains its elegant narrative of “information as market” and “pricing facts ahead of time.” But quietly, it is shifting its business model toward something more significant—no longer content to be merely a surface-level traffic platform, no longer relying solely on odds to attract users, and no longer willing to let others keep the most profitable part of the value chain (asset reserve returns).