On March 24, OpenAI announced the shutdown of Sora, its video generation tool that had been live for less than six months, and terminated its $1 billion content licensing agreement with Disney (according to Variety and Bloomberg). Data shows that Sora generated $367,000 in monthly revenue, with daily operating costs of $15 million, resulting in a revenue-to-cost coverage ratio of just 0.08%.

The day before, according to documents obtained by CNBC, Microsoft was listed as the top risk factor in OpenAI’s IPO preparation filings sent to investors. Three weeks prior, according to Awesome Agents, ChatGPT’s built-in e-commerce feature, Instant Checkout, was quietly shut down due to near-zero conversion rates.

A company valued at $730 billion, instead of showcasing a growth story as it races toward its IPO, is cutting product lines, shedding partners, and distancing itself from its largest shareholder. This doesn’t look like a contraction—it looks like a deliberate narrative cleanup.

Sora: Technically stunning, a commercial disaster

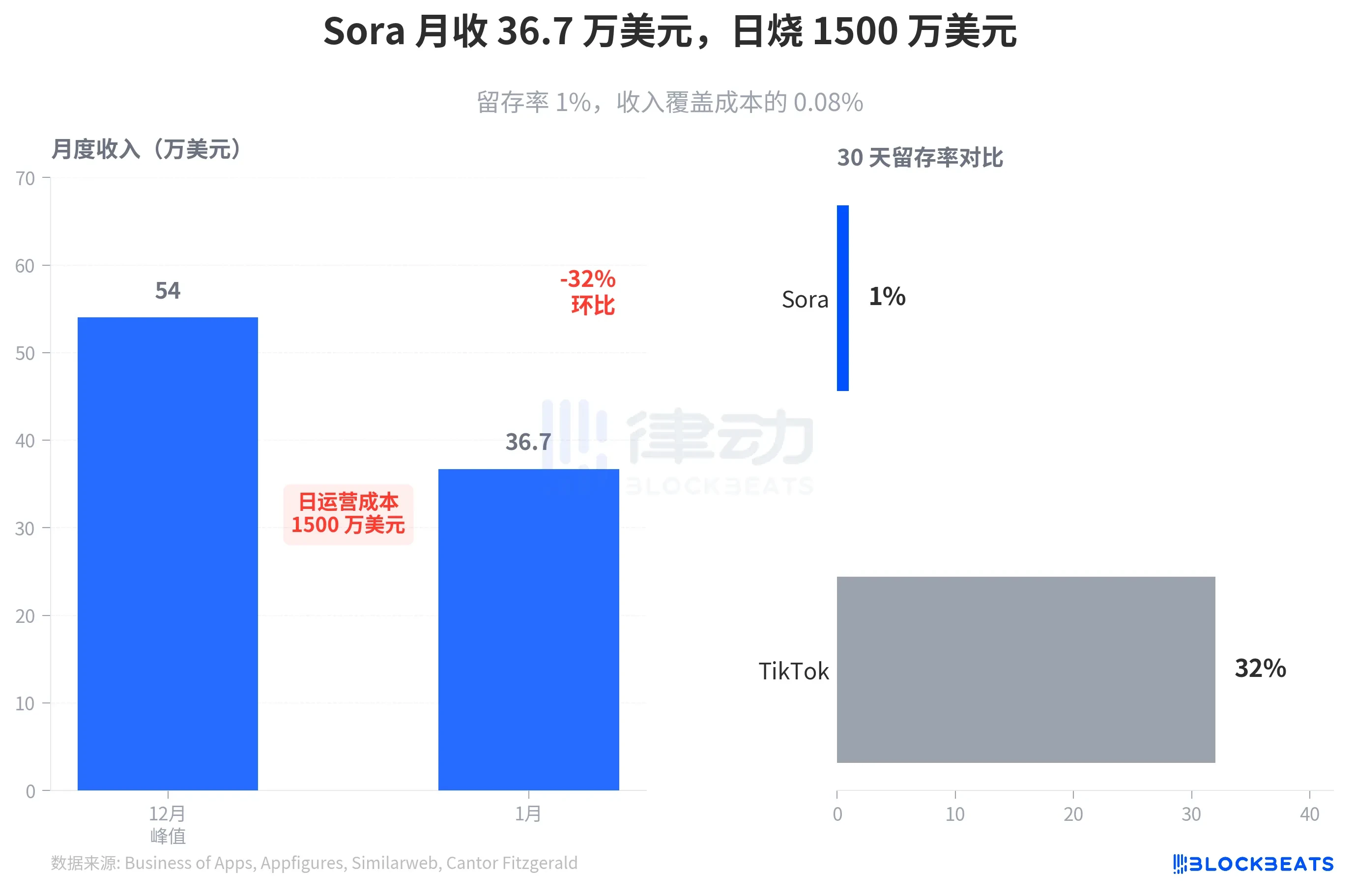

When Sora launched in October last year, it became a phenomenon on the App Store, surpassing 1 million downloads within five days and reaching over 3 million total downloads. However, according to data from third-party tracking platforms Appfigures and Similarweb, its 30-day retention rate was only about 1%, compared to TikTok’s 32% during the same period.

According to Appfigures data, downloads in January decreased by 45% month-over-month to approximately 1.2 million. Revenue in January was $367,000, a 32% decline from the December peak of $540,000. According to Cantor Fitzgerald analyst Deepak Mathivanan, Sora peaked at generating 11.3 million videos per day, with an estimated generation cost of $1.30 per video, resulting in daily operating costs of approximately $15 million and an annualized burn rate of about $5.4 billion.

For OpenAI, the problem with Sora isn't inadequate technology—it's an unsustainable business model. Spending $540 million annually to generate less than $5 million in revenue is toxic in any IPO prospectus.

The cancellation of Sora comes at the cost of Disney’s $1 billion investment agreement being voided. According to Variety, the three-year agreement originally granted OpenAI the rights to use more than 200 characters from Marvel, Pixar, and Star Wars to train and generate content, excluding characters associated with live-action actors’ likenesses and voices. According to Bloomberg, the funds have not yet been disbursed.

De-Microsofting: A 16-Month Systematic Engineering Project

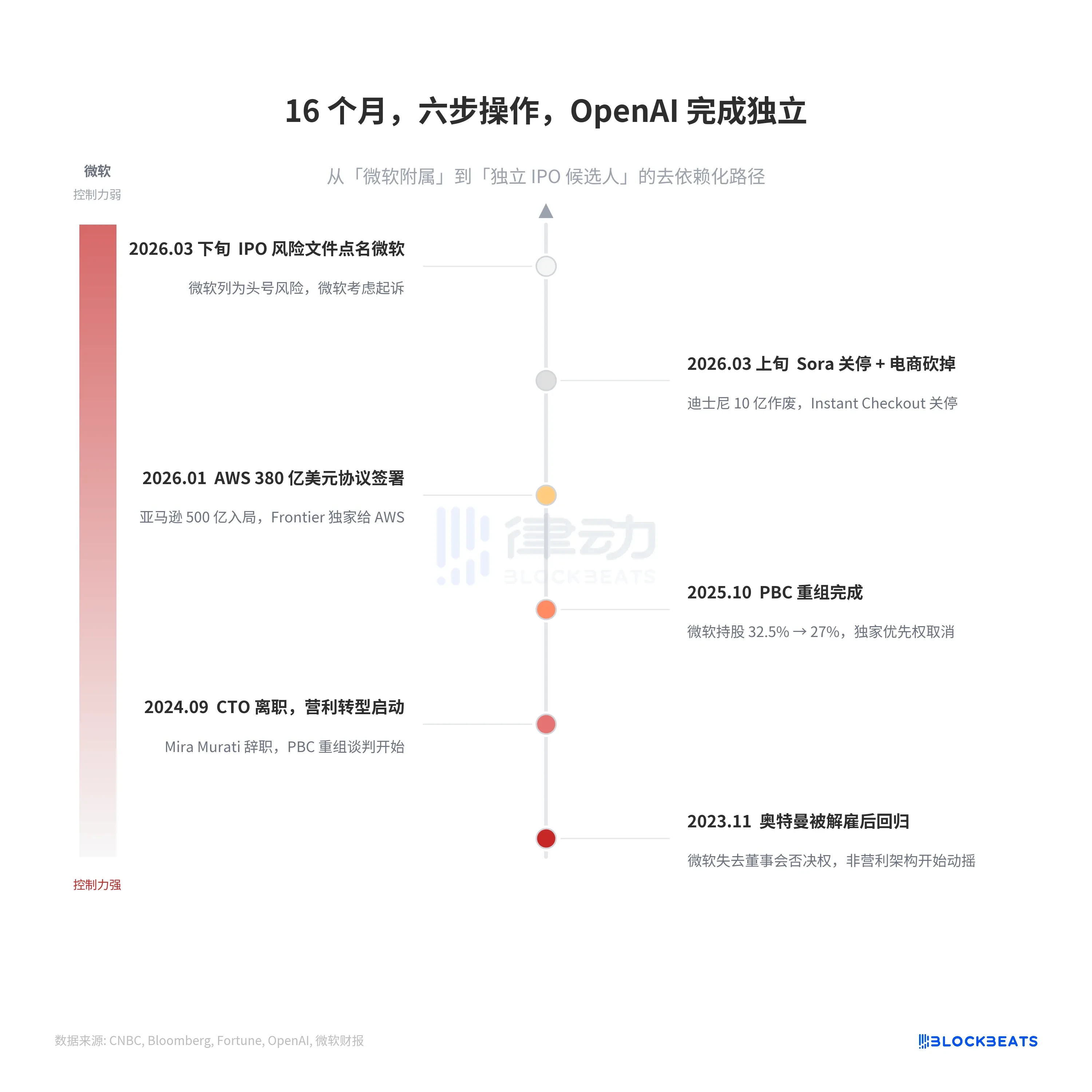

Viewing the Sora and Disney agreements as isolated events overlooks a more important clue. Starting with Altman’s firing and subsequent return in November 2023, OpenAI executed six strategic moves over 16 months to systematically downgrade Microsoft from a controller to a minority shareholder.

The PBC restructuring in October 2025 was a pivotal turning point. According to Fortune, Microsoft’s equity stake was diluted from 32.5% to 27%, and its exclusive cloud priority was simultaneously terminated. Six days after the restructuring was completed, OpenAI signed a $38 billion cloud computing agreement with Amazon, with all deployments expected to be completed by the end of 2026, as reported by ESM China. Amazon’s total commitment amounts to $50 billion, with $15 billion paid upfront and the remaining $35 billion tied to milestones such as the IPO进程.

More critically, the cloud architecture is split: Microsoft Azure retains OpenAI’s stateless API calls—the foundational inference services for ChatGPT and the API—while Frontier, OpenAI’s stateful enterprise-grade agent platform, is exclusively deployed on AWS. According to Windows Central, Microsoft believes this violates the original exclusivity clause and is considering legal action.

According to Next Platform’s analysis, approximately $281.3 billion of Microsoft’s $625 billion revenue backlog stems from OpenAI’s committed Azure purchases, accounting for 45%. Microsoft’s estimated capital expenditure for fiscal year 2026 is between $100 billion and $125 billion, while AI-related revenue is projected to annualize at only about $13 billion. This creates a counterintuitive situation: as OpenAI忙于“de-Microsofting,” Microsoft’s financial dependence on OpenAI may be growing even deeper.

E-commerce zero conversion and narrative focus

The shutdown of ChatGPT Instant Checkout received little attention, but it follows the same logic as the shutdown of Sora. The feature, launched in September last year, had promised integration with over one million Shopify merchants but was actually integrated with only about twelve. According to Awesome Agents, by the time of its shutdown, the purchase conversion rate was nearly zero, and a state sales tax collection system was never established.

After the shutdown announcement, public market data shows that Expedia's stock rose 13.69%, Booking's stock increased by 8.46%, and Shopify's stock gained 3.96%. The market's interpretation is clear: OpenAI's exit from e-commerce is a positive development for existing players.

The simultaneous contraction of three product lines points to a shared goal: focusing the IPO valuation narrative on the core AI model. According to disclosures from OpenAI’s CFO Sarah Friar and official OpenAI data, figures such as $20 billion in annual revenue, 800 million weekly active users, and 1 million enterprise customers are sufficient to support a clean growth story. The $5.4 billion annualized cost of Sora, zero conversion from e-commerce, legal risks from the Disney agreement, and uncertainties surrounding the Microsoft relationship—all of these are noise in an IPO prospectus.

The "streamlining" before an IPO is not unique to OpenAI.

In 2020, Uber sold its autonomous driving division, ATG, to Aurora for $4 billion in exchange for a 26% equity stake. ATG had an annual R&D expenditure of $457 million. After eliminating ATG, Uber achieved its first profit since its IPO. Similarly, WeWork also cut non-core businesses before its 2019 IPO, but acted too late—its valuation plummeted from $47 billion to $8 billion, leading to IPO failure and bankruptcy in 2023.

OpenAI’s operations are more similar to Uber’s: proactively eliminating high-cost, low-return business lines and cleaning up its financial structure before going public. The difference lies in scale. Uber’s ATG division burned $457 million annually; OpenAI’s Sora project burns $5.4 billion annually—an order of magnitude larger. Add to that Disney’s $1 billion write-off, the dissolution of its e-commerce team, and the public downgrade of its relationship with Microsoft, and OpenAI is undergoing the largest business-line purge in tech history as it races toward its IPO.

Altman is telling the growth story through subtraction.