Written by: Delphi Digital

Compiled by AididiaoJP, Foresight News

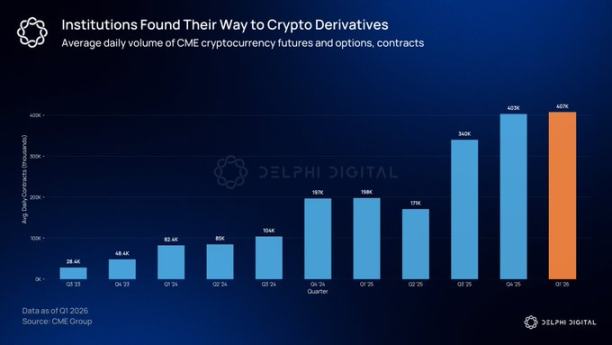

The cryptocurrency options market is far larger than most people realize. Trading volume for cryptocurrency derivatives on the Chicago Mercantile Exchange (CME) increased by 46% compared to last year’s record high. Institutional investors require clear risk management tools to hedge large positions, and options are the only cryptocurrency instrument that provides this functionality.

Market landscape reshaped

In mid-2025, the total open interest in Bitcoin options reached $65 billion, surpassing futures open interest for the first time. While futures are leveraged instruments, options allow funds to set a maximum loss on their $500 million Bitcoin position by paying a premium. This turning point indicates that instruments with defined risk profiles are gradually replacing pure leverage tools.

This growth has been concentrated primarily on two platforms. Deribit has long been the dominant platform for cryptocurrency options trading, and after being acquired by Coinbase for $2.9 billion in 2025, it gained institutional-level validation. Meanwhile, IBIT options, launched at the end of 2024, have brought traditional financial capital into this space. While the options market is expanding rapidly, the vast majority of trades still require intermediaries.

On-chain options are still in their early stages.

The market share of decentralized derivatives has risen from 2% to over 10% within two years. Hyperliquid has demonstrated that decentralized exchanges (DEXs) can match centralized exchanges in speed and transparency. However, no comparable representative project has yet emerged in on-chain options.

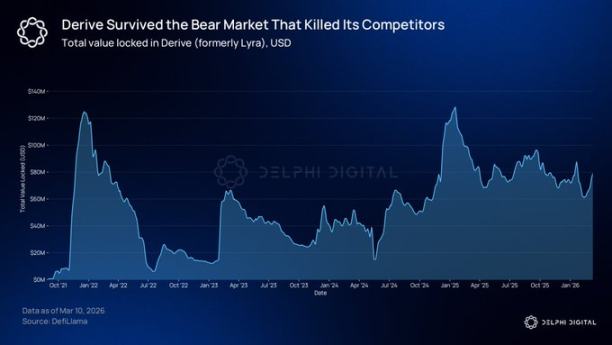

@DeriveXYZ remains the leading on-chain options protocol, with notional options trading volume exceeding $700 million over the past 30 days. Originally launched in August 2021 as Lyra as an options automated market maker (AMM), the protocol underwent a full rebuild after the bear market and now features a gas-free central limit order book built on its own OP Stack Layer 2.

This restructuring has completely transformed the pricing mechanism. Market makers now quote directly on the order book, narrowing spreads, improving pricing accuracy, and enabling larger trade sizes. Traders benefit from zero gas fees and sub-second execution speeds.

Its portfolio margining system has also attracted institutional attention. The system evaluates overall position risk through scenario analysis. For example, if a trader holds both a long position in a call option and a short position in a put option on the same underlying asset, the system does not require margin to be collected separately for each leg.

The collateral required for a hedged position is lower than the simple sum of individual positions, which is the standard logic used by traditional financial derivatives trading desks. Derive also offers perpetual contracts and lending services on the same Layer 2, with cross-product margining supported.

@KyanExchange is moving toward the same goal in different ways. The platform combines an order book matching engine with on-chain portfolio margining, enabling multi-leg operations to be executed in a single atomic trade. Traders can deploy a iron condor strategy with just a few clicks.

Kyan’s liquidation mechanism also differs from most DeFi protocols. When the margin threshold is breached, the platform does not liquidate the entire account; instead, it executes a partial close, liquidating only the minimum position required to restore the account to its margin requirements. Kyan is currently in the Arbitrum test phase, with mainnet launch imminent.

Who needs options?

Asset management companies building structured products urgently require the clearly defined risk-return profiles offered by options. For example, JPMorgan’s Stock Yield Enhancements ETF, which is constructed using a covered call strategy, is one of the largest actively managed funds globally. The total assets under management of derivative-based income products have exceeded $100 billion. As more institutional capital flows on-chain, corresponding hedging demand will also migrate accordingly.

An increasing number of institutional investors currently hold or plan to allocate to digital assets in the near term. Open interest in IBIT options has surpassed that of the gold ETF GLD. In 2025, CME processed notional trading volume of $3 trillion in cryptocurrency derivatives.

The timing is ripening

Most early on-chain options protocols failed to survive, primarily due to regulatory uncertainty. For example, Opyn was penalized by the CFTC for operating an unlicensed derivatives exchange. At the time, teams developing these products could not predict whether their offerings would be deemed illegal in the next quarter.

This situation is improving. In September 2025, the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly issued a statement permitting regulated exchanges to offer spot trading of crypto assets. The CLARITY Act has passed the House of Representatives and proposes to place the spot market for digital commodities under CFTC oversight. The Senate version is still under negotiation and currently stalled. CME Group will launch 24/7 crypto options trading on May 29. While this does not guarantee that on-chain protocols will inevitably prevail, the overall environment has undergone a substantive shift.