Oil Is the War

Original author: Garrett

Peggy, BlockBeats

Editor’s Note: While the market still views oil price fluctuations as a “dependent variable” of war, this article argues that what truly needs to be understood is how war itself is being priced through oil.

As the Strait of Hormuz remains disrupted, the global crude oil supply system is being forcibly restructured—Asian buyers are shifting en masse to U.S. crude, causing WTI to surpass Brent, signaling a structural shift in pricing mechanisms and trade flows. While short-term price differentials can be explained by contracts, the deeper issue is: “Who can still supply?”

The author further notes that the market’s key misjudgment is not in price, but in timing. The futures curve still implies an assumption that the conflict will end soon and supply will recover. However, a more likely scenario is a prolonged war of attrition. This means that elevated oil prices will no longer be a temporary shock, but rather evolve into a more persistent structural condition, with the price range potentially shifting upward to $120–$150.

Under this framework, crude oil is no longer just a commodity but has become the "upstream variable" for all assets. Its repricing will propagate layer by layer through interest rates, exchange rates, equity markets, and credit markets.

The market has priced in the occurrence of the war, but not its duration.

The following is the original text:

Trump gave Iran a 10-day deadline. That was already a week ago. Yesterday, he reminded everyone again: only 48 hours remain. Tehran’s response: no.

Five weeks ago, on February 28, when U.S. and Israeli fighter jets conducted airstrikes on Iran, market pricing still assumed a "surgical" air strike: two weeks, at most three; the Strait of Hormuz reopening; oil prices rising briefly before falling back, with everything returning to normal.

But our judgment at the time was: no.

From day one, our core thesis has been that this conflict will escalate first and only potentially de-escalate much later. The most likely path involves ground forces entering the fray, followed by a prolonged and attritional conflict. The duration of the disruption to the Strait of Hormuz will far exceed the assumptions markets are willing to incorporate into their models. We have laid out the full logic in our duration framework, Hormuz pricing model, and war scenario analysis.

The core judgment is simple: Iran doesn’t need to win; it only needs to raise the cost of war high enough to force Washington to seek an exit. And this “exit” will not be accompanied by the smooth reopening of the strait.

Five weeks later, each key part of this assessment is being gradually validated. The Strait of Hormuz remains closed. Brent crude is trading at around $110. The Pentagon is preparing for weeks of ground operations. Trump’s war objectives have shifted from “denuclearization” to “pushing the other side back to the Stone Age,” yet he still cannot clearly define what “victory” means.

The deployment of ground forces is the key upgrade trigger we've been monitoring. Marine and airborne units have already assembled in the theater—this moment is drawing near.

But more critical than the next airstrike or the next ultimatum is oil.

Oil is not a byproduct of this war—oil is the core of the war itself. Stock markets, bond markets, crypto markets, the Federal Reserve, and even your daily grocery expenses—all are downstream variables. Get the oil price right, and everything else follows; get it wrong, and all other decisions lose their meaning.

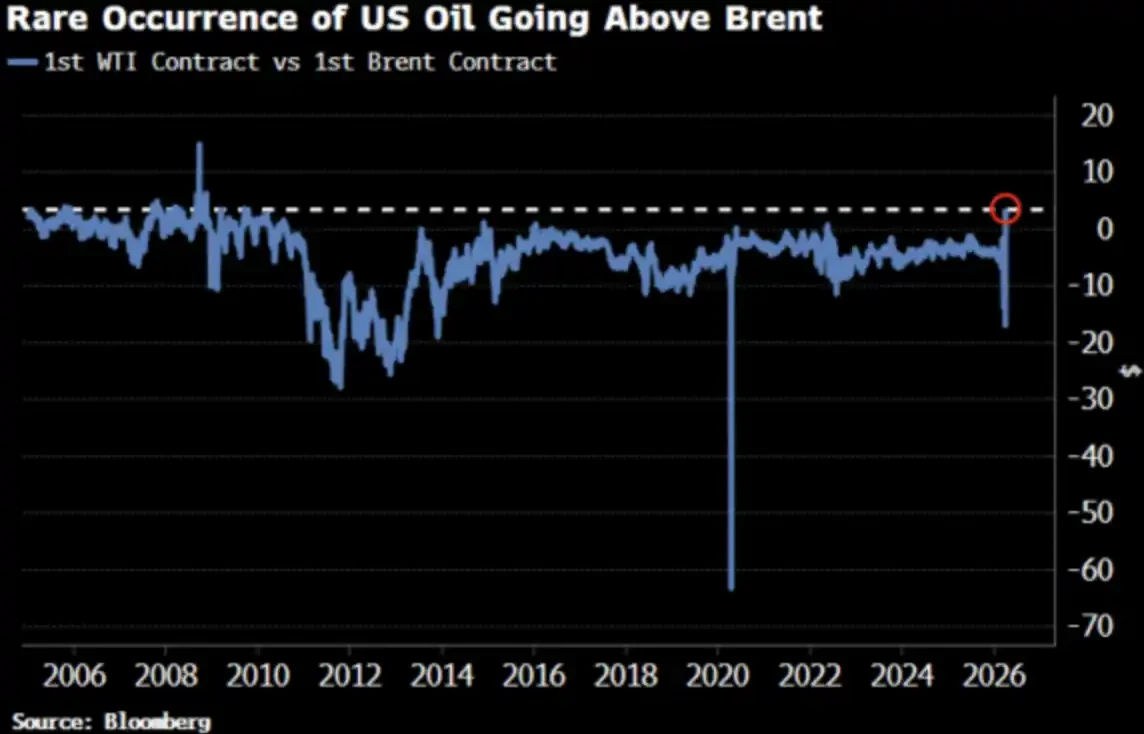

WTI crude oil prices have just risen above Brent for the first time since 2022, a shift that has drawn market attention.

Great, that's how it should be.

WTI above Brent: What everyone is asking

On April 2, WTI crude closed at $111.54, while Brent closed at $109.03. WTI traded at a $2.51 premium to Brent, the largest spread since 2009. Just two weeks prior, WTI was trading at a significant discount to Brent.

Everyone is asking: What happened? Here’s a brief version, and a more accurate one.

Brief version: Mismatch in contract duration

The front-month WTI contract corresponds to May delivery, while the front-month Brent contract has rolled to June. Under such tight supply conditions, "delivering a month earlier" means a higher price—WTI simply happens to have an earlier delivery date.

Adi Imsirovic, a petroleum trader based in Oxford with 35 years of trading experience, said buyers are willing to pay nearly $30 per barrel more for Brent crude to take delivery a month earlier, on top of historically high freight and insurance costs—a phenomenon he has never witnessed in his 35-year career.

This is an explanation at the "mechanism level"—it is correct, but incomplete.

Real version: The price curve is shifting overall.

The convergence of WTI and Brent is not merely an occasional mispricing in the front-month contracts. Bloomberg notes that this phenomenon is clearly visible across multiple contract months, spanning the entire forward curve—indicating that the entire price curve is being repriced.

What’s the reason? A shift in Asian demand. In late March, Asian refineries secured approximately 10 million barrels of U.S. crude for May shipments; the prior week, they purchased around 8 million barrels. Kpler expects U.S. crude exports to Asia to reach 1.7 million barrels per day in April, up from 1.3 million barrels per day in March. China, South Korea, Japan, and ExxonMobil’s refinery in Singapore are all buying U.S. crude—because it’s currently the “only cargo available.”

The Strait of Hormuz remains closed. Murban crude from Abu Dhabi—the closest substitute to WTI—has disappeared from the global market. WTI is becoming the global 'marginal pricing oil'.

This is not a panic buying spree, but a change in liquidity structure.

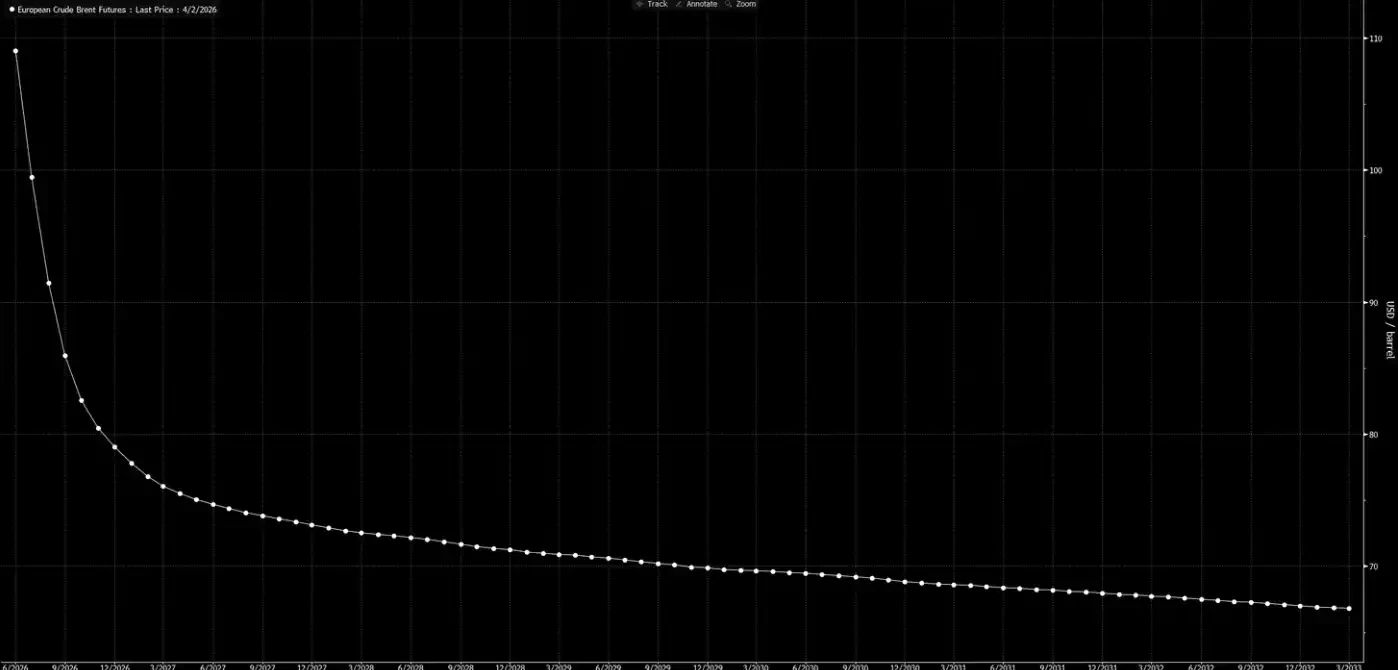

Now let’s look at the forward price curve.

This curve signals that this is only a temporary shock, and everything will return to normal before Christmas.

Our assessment is: This curve is dreaming.

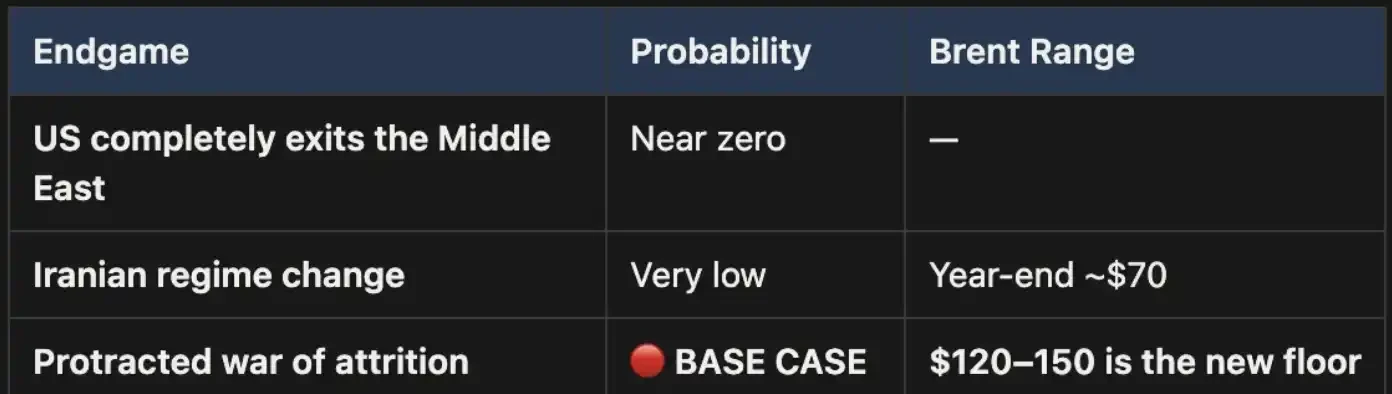

Three outcomes, one baseline path

We have previously presented this analytical framework in the Weekly Signal Playbook. So far, nothing has changed; if anything, the probability of the base case has further increased.

This war will ultimately end in only three ways:

The diagram lists three possible outcomes: one, the United States fully withdraws from the Middle East; two, a regime change in Iran (similar to Iraq in 2003); three, a prolonged attrition war.

Outcome one is politically almost impossible to achieve.

Outcome two is equally untenable: terrain conditions, troop requirements, and the evolutionary logic of guerrilla warfare all indicate that this path would be prohibitively costly and difficult to resolve. Iran’s land area is three times that of Iraq, its population nearly twice as large, not to mention the mountainous terrain that offers no room for invaders. This is not 2003.

Outcome three is the baseline scenario, with a significantly higher probability. If the conflict escalates into a prolonged war of attrition, the disruption of the Strait of Hormuz will persist, keeping oil prices elevated. This high level will be structural, not temporary. The current forward price curve clearly underprices this risk.

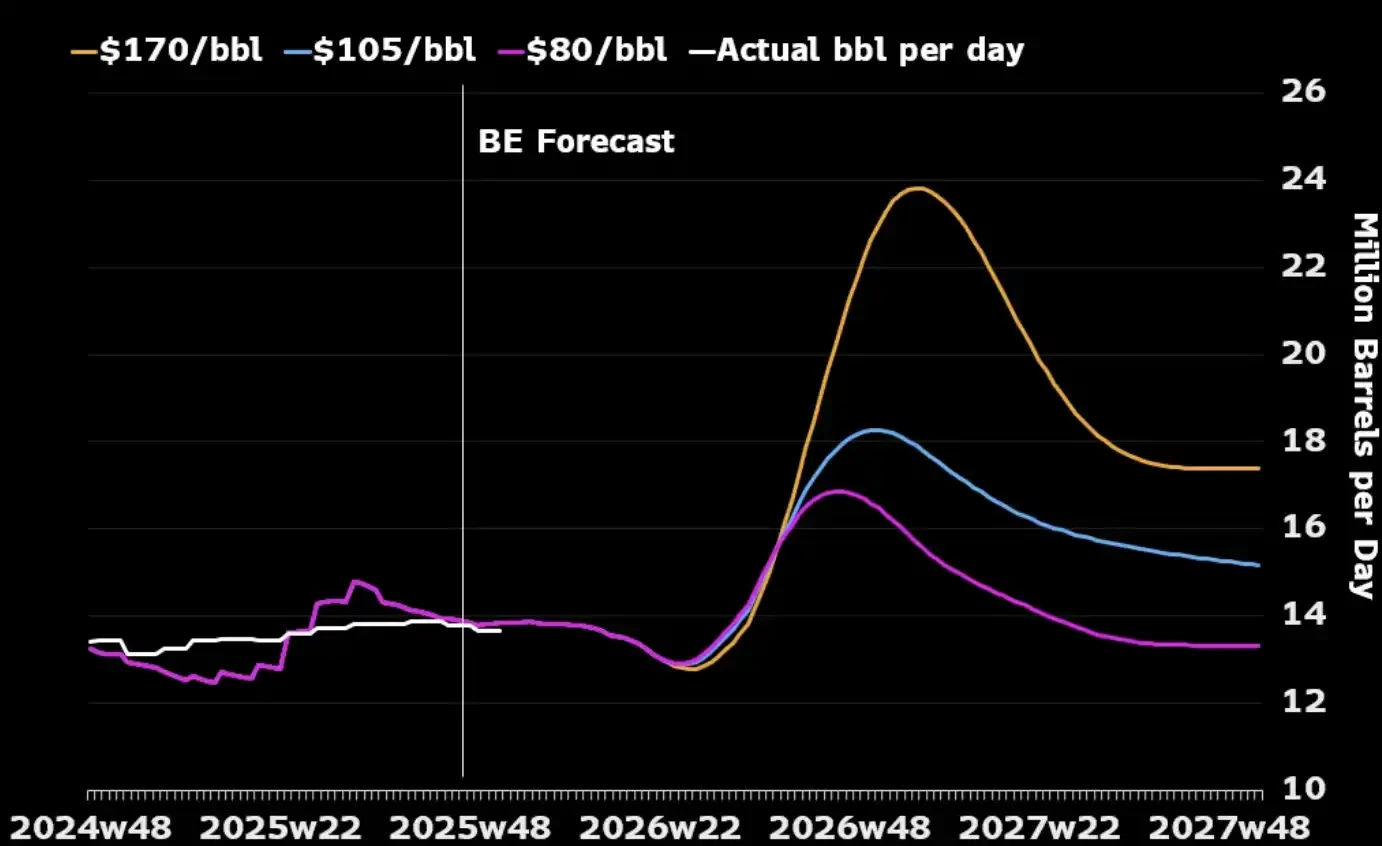

One point many overlook is that, from the perspective of the oil industry alone, a prolonged war might actually align with U.S. strategic interests. Oil production capacity in the Middle East would be disrupted during conflict, leaving global buyers with little choice but to turn to North American energy, as alternative sources have largely dwindled. Higher oil prices would also incentivize U.S. producers to increase output—deploying more drilling rigs and boosting investments in shale oil. As the chart below shows, historically, nearly every major spike in oil prices has been followed within 12 to 18 months by an uptick in U.S. production.

The only cost the U.S. truly needs to manage is domestic: how to prevent gasoline prices from remaining above $4 per gallon for too long and triggering political backlash. This is a "pain threshold," not a condition for ending the war.

The "arithmetic" of price

In the event of a closure of the Strait of Hormuz, $110 per barrel for Brent is not the ceiling, but merely the starting point. Under our base case scenario, as long as the strait remains closed, oil prices will remain in the range of $120 to $150 per barrel.

Each passing week depletes inventories. UBS data shows that global inventories fell to the five-year average by the end of March—before the latest round of upgrades. Macquarie estimates that if the war extends beyond June and the strait remains closed, there is a 40% chance oil prices could surge to $200.

The nearby spread (the spread between the two nearest Brent contracts) has widened to $8.59 per barrel. The market is paying a premium of approximately 8% for delivery a month earlier—a level of tightness not seen since 2008.

But in 2008, 15% of the global supply was not physically locked up.

Today, virtually all models, all price curves, and all Wall Street year-end forecasts are built on the same assumption: that this conflict will end, the Strait of Hormuz will reopen, oil prices will return to normal, and the world will go back to how it was.

Our judgment is: no.

The back end of the forward curve has not yet caught up with reality. The market has priced in the occurrence of war, but not its duration. Every pullback in crude oil before the Strait of Hormuz reopens is an opportunity. This is our core position, and we will not hedge it.

Oil is the first node. When "ground forces enter" and there is no quick victory—when the conflict escalates into the prolonged attrition war we predicted from day one—the repricing will not stop at crude oil itself, but will sequentially transmit to interest rates, exchange rates, equities, and credit markets. This is what’s coming next.