Author: Shenchao TechFlow

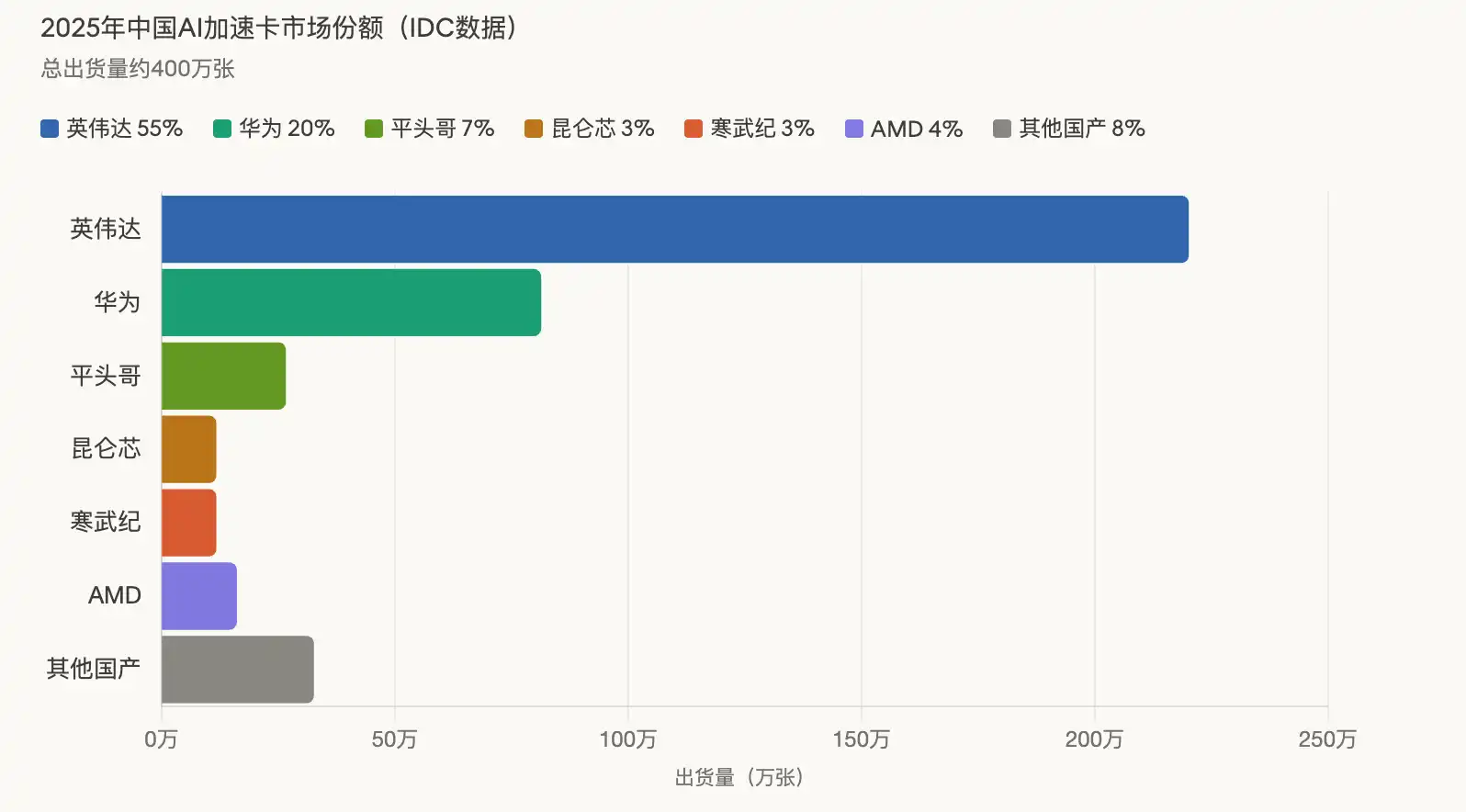

Shenchao Summary: IDC data shows that China's total shipment of AI accelerator cards in 2025 is expected to reach approximately 4 million units, with domestic manufacturers collectively delivering 1.65 million units, accounting for 41%. NVIDIA's market share has dropped from about 95% before sanctions to 55%.

Huawei leads the domestic chip market with 812,000 chips, and its newly released Atlas 350 accelerator card claims a推理 performance 2.87 times that of NVIDIA’s H20.

In November last year, Beijing ordered a full domestic replacement of state-owned data centers, accelerating the reshaping of the market landscape.

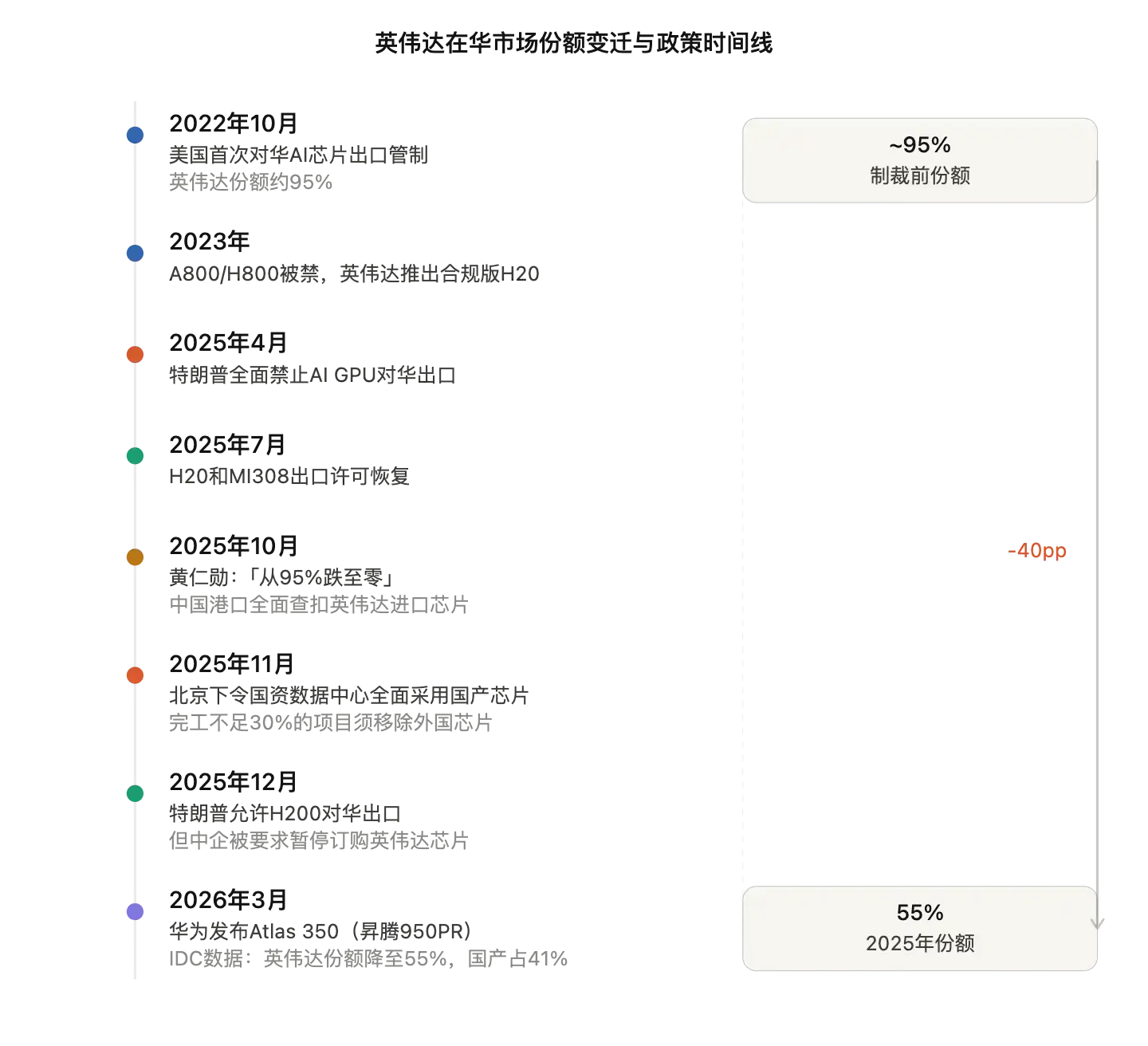

Three years ago, NVIDIA almost monopolized China’s AI chip market. Today, this landscape has been completely transformed.

According to Reuters, citing market research firm IDC, China’s total shipments of AI accelerator cards—specialized computing chips for AI servers—are expected to reach approximately 4 million units in 2025. NVIDIA remains the largest single supplier, shipping about 2.2 million units, or 55% of the market. However, this represents a significant decline of nearly 40 percentage points from its pre-sanction market share of around 95%. Meanwhile, domestic Chinese manufacturers collectively shipped about 1.65 million units, capturing 41% of the market. AMD ranks third with approximately 160,000 units shipped, accounting for 4%.

The rise of domestic manufacturers is both a passive outcome of U.S. export controls and an active result of the "domestic substitution" policy.

Huawei leads the domestic lineup, with the Atlas 350 competing against NVIDIA's H20.

Among China's domestic AI chip vendors, Huawei is the biggest winner.

IDC data shows that Huawei shipped approximately 812,000 AI chips in 2025, accounting for about 20% of the total market and nearly half of all domestic vendors' shipments. Alibaba’s chip design division, T-Head, ranked second with approximately 265,000 chips shipped. Baidu’s Kunlun芯 and Cambricon each shipped around 116,000 chips, tying for third place. Additionally, Hygon, MetaX, and Iluvatar CoreX accounted for 5%, 4%, and 3% of domestic vendors’ shipments, respectively.

Last month, Huawei unveiled its new AI accelerator card, the Atlas 350, powered by the in-house developed Ascend 950PR chip, at the China Partner Conference 2026 in Shenzhen. Zhang Dixuan, head of Huawei's Ascend Computing business, stated at the launch that the Atlas 350 delivers 1.56 PFLOPS of computing power under FP4 low-precision calculations—2.87 times the performance of NVIDIA’s China-specific H20. The card features 112GB of in-house developed high-bandwidth memory, HiBL 1.0, with a memory bandwidth of 1.4 TB/s and a power consumption of 600W.

However, this performance comparison suffers from a mismatch in metrics. NVIDIA’s Hopper architecture GPUs do not natively support FP4 precision, while the Atlas 350 is the first domestic accelerator card optimized for FP4; thus, a direct comparison at the same precision level is not valid. Huawei’s true competitive advantage lies in inference: the Atlas 350 is designed for inference workloads during AI model deployment, not for training large models.

Seven Huawei partners have already launched full-server products based on the Atlas 350, and iFlytek has also announced that its next-generation Spark large model will be adapted to the Ascend 910/950 computing foundation.

Dual drivers: export controls and domestic substitution policies

NVIDIA's shrinking market share in China is the result of escalating U.S. export controls and Beijing's domestic substitution policies acting in tandem.

The timeline is roughly as follows: In October 2022, the United States imposed restrictions on AI chip exports to China; thereafter, NVIDIA launched compliant, downgraded products such as the H20 and A800/H800. In April 2025, the Trump administration banned all AI GPU exports to China; in July of the same year, export licenses were reinstated for the H20 and AMD MI308; in October, NVIDIA CEO Jensen Huang stated publicly that NVIDIA’s market share in China’s advanced AI accelerator card market had “fallen from 95% to zero.” In December, Trump permitted NVIDIA to export the H200 to China, but Chinese companies were advised to suspend orders for NVIDIA chips.

Policy pressure on the other side is equally strong. According to a Reuters report from November 2025, Beijing issued guidelines to newly constructed data centers using state-owned capital, requiring them to adopt only domestically produced AI chips. Projects with completion progress below 30% are required to remove already installed foreign chips or cancel procurement plans.

According to Reuters data, Chinese AI data center projects have received over $100 billion in state capital investment since 2021, and most data centers in China have received some form of state capital support during construction, indicating the policy's extensive reach.

China Unicom's large data center in Qinghai has been reported by Reuters as a flagship example of this strategy: the project, valued at $390 million, is powered entirely by domestic AI chips such as those from Pingtouge.

The technical gap is real, but the inference side has reached the "sufficient" threshold.

The growing market share of domestic chips does not mean the technological gap has been eliminated.

Most industry analysts estimate that China’s domestic AI chips still lag behind NVIDIA by 5 to 10 years in data center training. When training large language models (LLMs) with trillions of parameters, NVIDIA’s high-end GPUs remain the preferred choice. The cluster of 50,000 Hopper-series GPUs used by DeepSeek to train its R1 model is a real-world example.

However, the situation on the inference side has changed. Industry observers believe that for 90% of commercial applications—including image recognition, chatbots, and autonomous driving—domestically produced chips have reached the “good enough” threshold, making a switch from NVIDIA to domestic solutions a viable business decision. Enhanced expectations of further sanctions have further accelerated this transition.

The real bottleneck lies in the software ecosystem. NVIDIA’s CUDA platform, after more than a decade of development, has become the de facto standard for AI development. Domestic chip manufacturers are investing heavily in compatibility: Moore Threads has announced that its C500 series will support CUDA compatibility; Huawei plans to fully open-source its CANN platform in 2025 to expand its developer ecosystem; and Cambricon and Moore Threads have each developed translation tools to convert CUDA code into their proprietary programming languages. The pace of ecosystem advancement will determine the upper limit of market share for domestic chips.

Domestic AI chip companies are aggressively pursuing capital markets.

The shift in market share is being realized simultaneously in the capital markets.

Since early 2026, China’s GPU sector has witnessed a wave of IPOs. Biren Technology and沐曦 have listed on the STAR Market, TianShu Intelligent Chip has debuted on the main board of the Hong Kong Stock Exchange, and Suan Yuan Technology’s application for a STAR Market listing has been accepted. Baidu has announced plans to spin off Kunlun芯 for an independent IPO, and according to informed sources, Alibaba is also considering a similar spin-off of Pingtouge.

In 2025, Huawei invested RMB 192.3 billion in R&D, accounting for 22% of its revenue, with a focus on chips, software, and manufacturing tools to further reduce dependence on U.S. technology. Xu Zhijun, Huawei’s Rotating Chairman, stated at MWC 2026 that Huawei will become “an alternative to ensure uninterrupted global AI computing power supply.” According to Reuters, Huawei’s new Ascend 950PR chip has generated ordering interest from major companies such as ByteDance and Alibaba, with a 2026 shipment target of approximately 750,000 units, and mass production is set to begin in the second half of the year.

For NVIDIA, even though the H200 has been approved for export to China, the foundation of trust has already been shaken. Beijing’s policy of self-reliance and control is no longer just a vision—it is already a reality embodied in every domestic chip operating in data centers. When the 2026 market share figures are released, whether the 55% figure rebounds or continues to decline will depend on whether Washington reverses its export policies again and how quickly domestic chips close the gap in training capabilities.