Netflix's (NFLX.M) Q4 2025 earnings report presents a highly divided narrative.

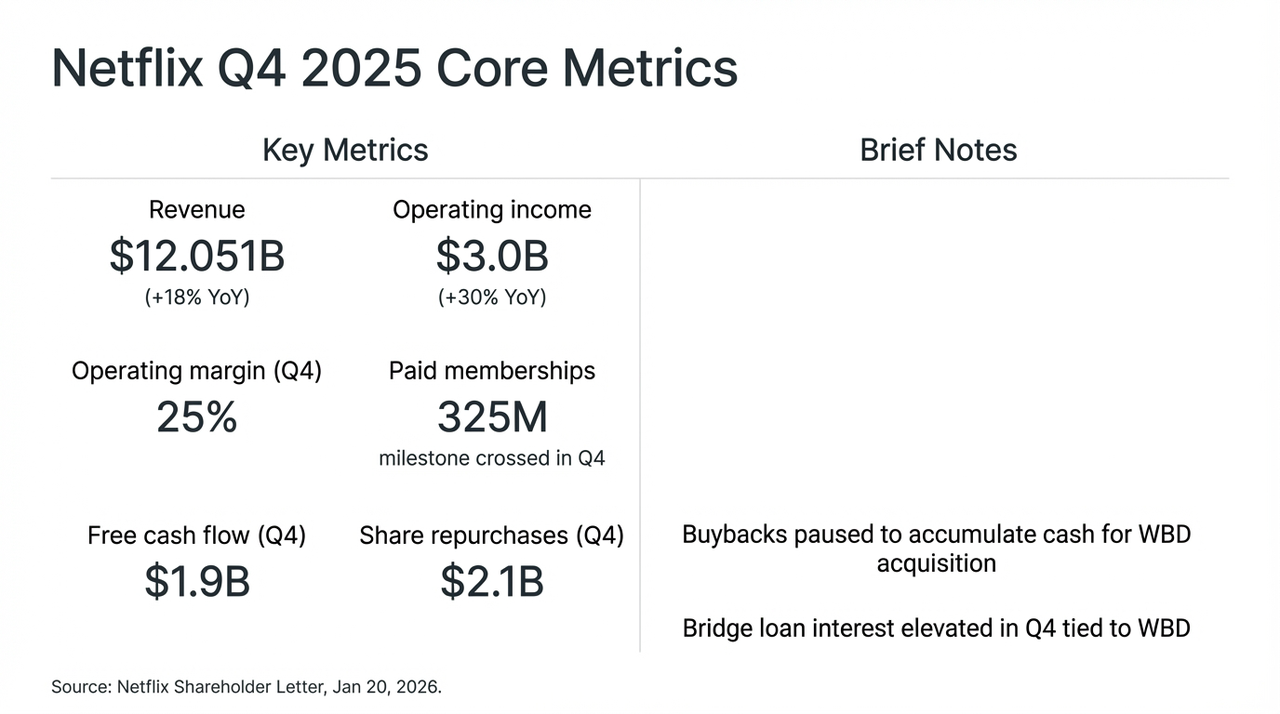

It's worth noting that, driven by the phenomenon series Stranger Things in its final season, Netflix delivered an almost flawless performance this quarter: revenue increased by 18% year-over-year to $12 billion, the number of global paid subscribers surpassed 250 million, and free cash flow (FCF) for the quarter reached $1.9 billion.

However, the market did not respond favorably. After the earnings report was released, investors' attention quickly shifted from the impressive growth figures to a controversial decision—Suspend stock buybacks and fully allocate liquidity for the acquisition of Warner Bros. Discovery (WBD).

This aggressive strategic shift of "trading growth for space" directly triggered significant after-hours stock price fluctuations for Netflix. We also attempt to look beyond this 72 billion-dollar acquisition plan (59 billion of which is financed through bridge loans) to dissect this high-stakes transformation aimed at claiming the title of "streaming king."

Netflix Q4 Key Financial Metrics and Impact of the WBD Merger

I. Financial Reports Beneath the Surface: Price Increases and Advertising as "Dual-Driven Forces"

Frankly speaking, looking at the numbers alone in the Q4 financial report, it's almost "flawless," once again strongly demonstrating Netflix's unshakable dominance in the global streaming market.

However, the unusual restraint shown by the capital market stems primarily from Netflix's decision to halt share repurchases and to acquire WBD entirely with cash, forcing the market to reassess Netflix's growth strategy and capital structure risks. To put it plainly, in the long-standing power struggle between Silicon Valley and Hollywood, Netflix appears to have chosen the most aggressive path: sacrificing free cash flow to launch a final sprint toward becoming the crowned king of streaming.

This is also the real shift beneath the surface of the financial report—the core issue for Netflix has long shifted from whether growth exists to how to continue growing.

Looking back at the statements made by Netflix's management during this earnings call, this shift has become evident—setting aside the noise from mergers and acquisitions,Netflix's own growth logic is actually at a critical stage of transitioning from "user scale-driven" to "ARM (Average Revenue per User)-driven."

For example, although its annual advertising revenue has exceeded $1.5 billion (an increase of over 2.5 times year-on-year), the ceiling effect in mature markets is becoming evident, causing actual business performance to fall significantly short of some institutions' previously aggressive forecasts (of $20-30 billion). More importantly, this growth is primarily driven by price increases in North America and Western Europe, as well as the short-term tailwind from cracking down on password sharing.

The management also admitted that the programmatic advertising system is still in the testing and early growth phase. In the short term, the advertising layer mainly serves as a low-cost customer acquisition tool rather than a true profit engine.

Against this backdrop, Netflix's revenue growth guidance of 12%–14% for 2026, which is significantly lower than the pace of previous years, has been viewed by many analysts as...Netflix has entered a "low-growth era" where it relies more on refined operations rather than expansive, rapid growth.

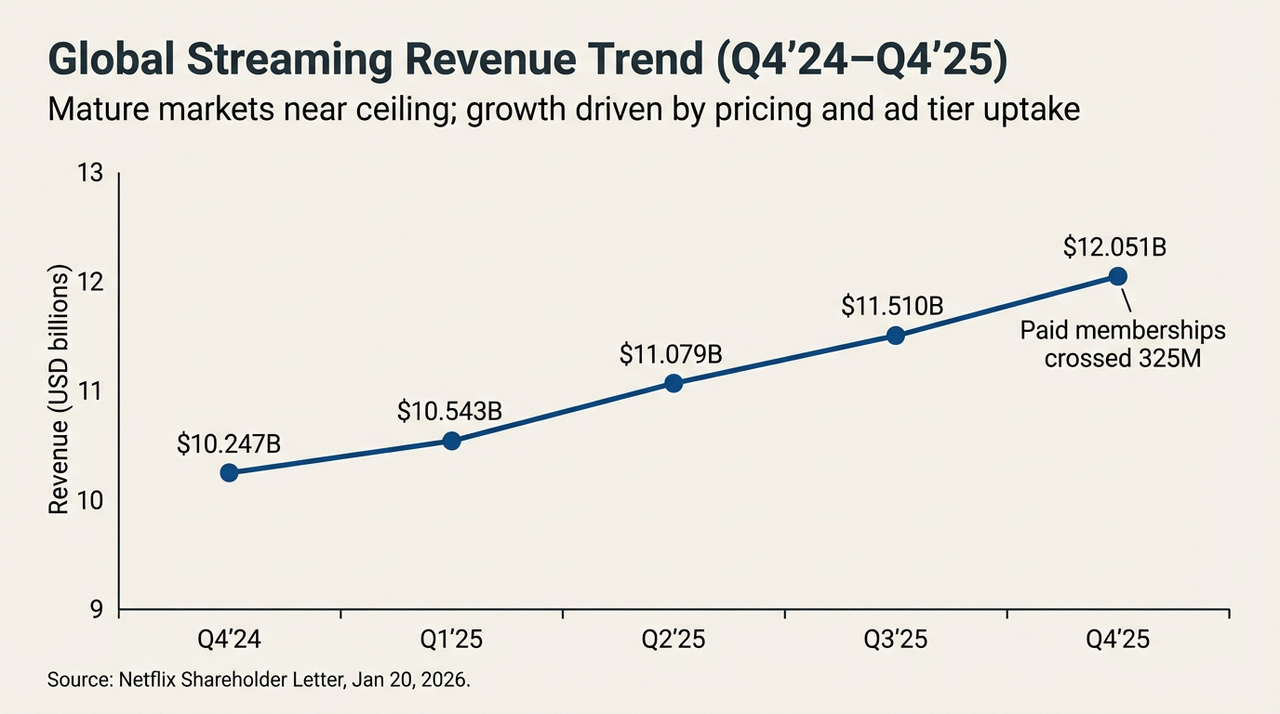

Global Streaming Revenue Trends (Q4'24-Q4'25)

From another perspective, as it becomes increasingly difficult to rely on refined ARM management to sustain the double-digit "growth myth," the marginal benefits of achieving valuation breakthroughs through internal forces are diminishing.Since the internal engine can no longer support greater ambitions, seeking an "external driving force" capable of reshaping the competitive landscape is no longer an option, but a necessity.

This might just be the deep underlying catalyst for why Netflix has chosen to heavily bet on WBD at this moment.

II. Acquisition of WBD: A Turning Point in the Growth Story

Although the fundamentals remain strong, it is Netflix's "heavy-industry-style" merger arrangement with WBD that has truly shifted market sentiment toward caution.

"Could this be a poisoned candy?" This is likely the most central question lingering in the minds of all investors regarding Netflix's merger with WBD at this moment.

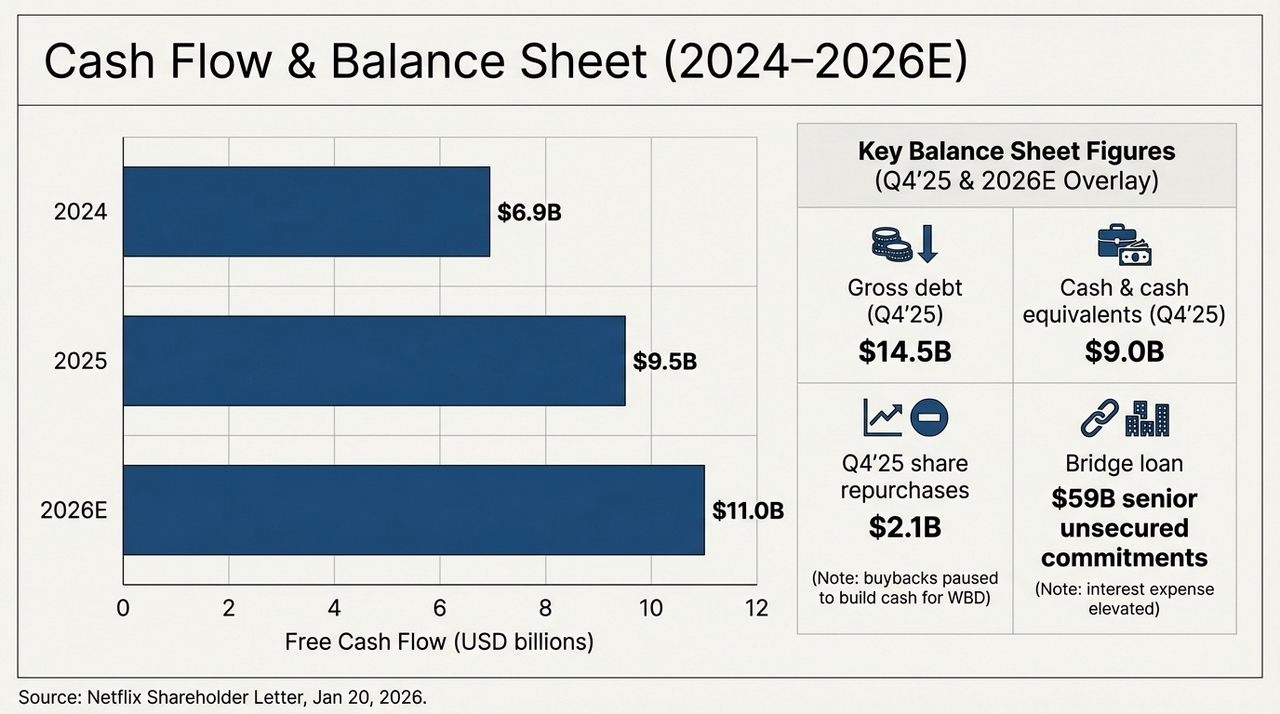

Objectively,The WBD acquisition has instantly pulled Netflix back into the heavy asset quagmire of traditional media, moving it away from its previous light-asset technology company model.To complete this all-cash deal at $27.75 per share, Netflix took on a senior unsecured bridge loan commitment of up to $59 billion. The immediate consequence of this decision was a dramatic "stress test" on its balance sheet.

The following chart clearly illustrates the evolution of the company's cash flow and debt structure over the next two years. As of Q4 2025, Netflix's confirmed gross debt will reach $14.5 billion, while its cash and cash equivalents on the balance sheet will amount to only $9 billion. This means that even before officially acquiring WBD, the company's net debt will already reach $5.5 billion. With the addition of a $59 billion bridge loan, Netflix's total debt will surge to more than four times its previous level.

Cash Flow and Balance Sheet Outlook (2024-2026E)

Meanwhile, Netflix's free cash flow is actually on a steady upward trajectory: approximately $6.9 billion in 2024, rising to about $9.5 billion in 2025, and expected to reach around $11 billion in 2026 (guidance). Looking at this trend alone, Netflix remains one of the few global streaming platforms capable of consistently and at scale generating cash.

But the problem is that,Even if Netflix uses all of its projected $11 billion in FCF in 2026 purely for debt repayment, it would still take more than five years to fully pay off the bridge loan.More concerning is that the content amortization ratio is currently maintained at around 1.1x, but with the inclusion of HBO's and Warner Bros.'s extensive film library, future amortization pressure will significantly increase.

This "cash flow sacrifice" essentially amounts to a bet that the marginal ARM (Annual Recurring Margins) increments generated by top-tier assets under WBD, such as HBO and the DC Universe, will cover the costs of interest expenses and depreciation/amortization.

This also means that before WBD's assets are fully integrated and begin to enhance content supply and user retention, Netflix must endure a relatively long transitional period where cash flow is prioritized to service its debt. If the integration efficiency falls short of expectations, this substantial loan will shift from being a "booster" for growth to a "black hole" dragging down its valuation.

III. IP Alchemy: Can Copyright Magic Overcome the Gravity of Debt?

Why is Netflix willing to endure criticism to "go all-in"?

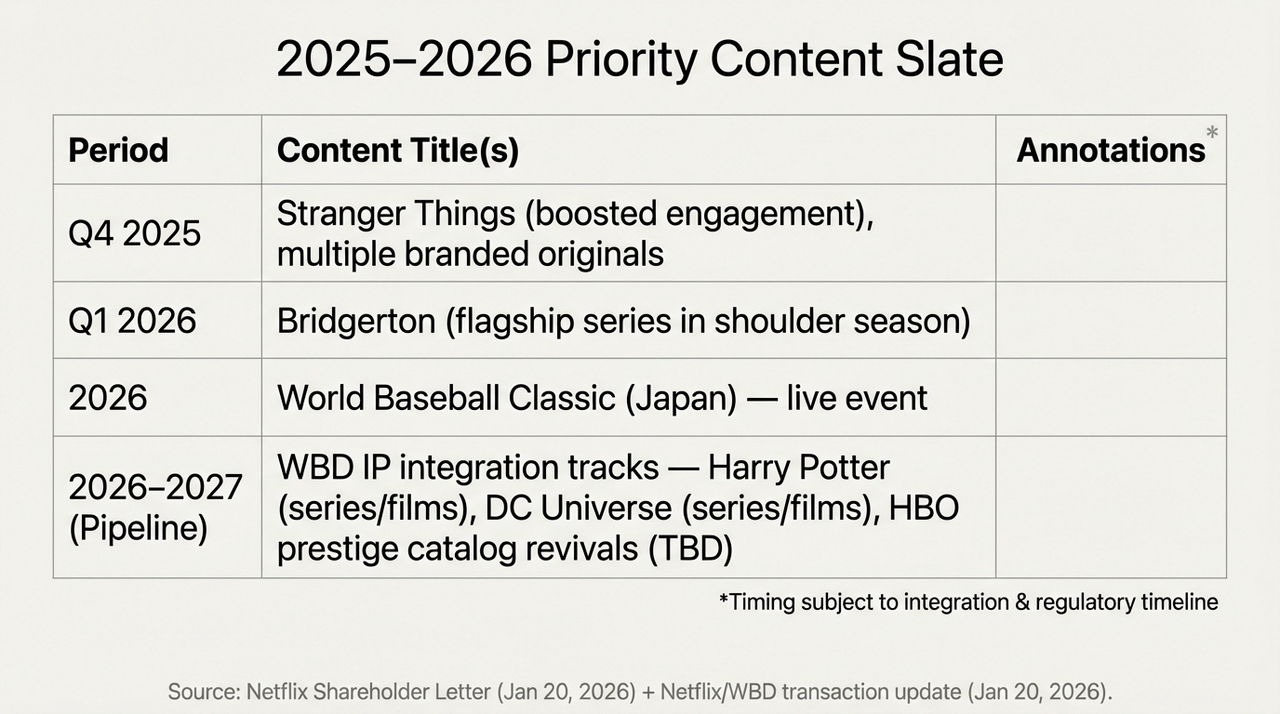

The answers lie within WBD's "dusty" assets. As is well known, from the studios in Burbank to the production facilities in London, WBD possesses a treasure trove of content that streaming platforms dream of—such as the magical world of Harry Potter, the superhero capes of the DC Universe, and HBO's irreplaceable premium library.

These are areas where Netflix has long been relatively weak, yet desperately needs to strengthen its "content moat." Therefore, for Netflix, this represents the final piece of the puzzle in building its "all-in-one streaming empire," as well as its trump card for placing a big bet in the second half. At the end of the day,The true significance of this merger and acquisition does not lie in short-term financial performance, but in the long-term change in the competitive structure:

- On one hand, WBD's intellectual property (IP) can significantly enhance Netflix's stable content supply, reducing reliance on a single hit.

- On the other hand, global distribution networks and mature recommendation systems also provide these IPs with unprecedented commercialization opportunities;

The issue is simply that the payback period for this path is clearly longer than the pace currently preferred by capital markets. After all, with a P/E ratio around 26 times, Netflix is standing at a delicate position:

For optimists, stock price fluctuations offer a "discount ticket"—once WBD's intellectual property successfully integrates into Netflix's content ecosystem, a new growth flywheel may restart. However, for the cautious, the hundreds of billions in merger financing, the suspension of share repurchases, and the downward revision of growth guidance all signal that the company is entering a new phase where both risks and rewards are amplified.

This is also the root of the market's divergence.

2025-2026 Key Content Schedule and WBD IP Integration Plan

In other words, this has turned into a repricing of Netflix's future positioning. The unprecedented "IP alchemy" that Netflix is undertaking comes at a significant cost—before free cash flow (FCF) ramps up by 2026, every dollar of revenue will be prioritized to pay down interest, plunging the company into a "precipice."

But the final answer, obviously, still needs time to reveal.

Final Words

Ultimately, the stock price decline following the Q4 earnings report resembles a fierce battle between bulls and bears over the "streaming king" narrative.

In any case, Netflix is no longer just the app that keeps you entertained during a boring weekend; it is becoming a financially burdened giant.

Perhaps in 2026, when Harry Potter emerges from the fog of debt onto Netflix's homepage, we will finally know whether this alchemy was a success or if it backfired on its creators.

Disclaimer: The content of this article is a macro-level analysis and market commentary based on publicly available information, and does not constitute any specific investment advice.