Naval Ravikant, Silicon Valley’s most famous angel investor, has just launched a new fund. Unlike his previous investments in over 400 companies—including Uber, Twitter, and Notion—this time, you can invest too.

You don’t need to be a millionaire, you don’t need connections, and you don’t need to be an accredited investor under U.S. securities law. With just $500, you can invest in shares of OpenAI, Anthropic, xAI, and SpaceX all at once.

The fund is named USVC (United States Venture Capital), built by AngelList, with Naval himself serving as chair of the investment committee. After its launch last night, AngelList’s announcement tweet garnered 2.75 million views, and Naval’s long tweet received 2.25 million views. They’ve set a bold tagline for the fund: “The Endowment of the American People.”

It sounds like a complete financial democratization. But when you look beneath the surface, the reality is much more complex than the slogan suggests.

Buy a top Silicon Valley portfolio for $500

The long tweet announcing the launch was written personally by Naval, in his classic style—short sentences, aphorisms, and historical analogies.

He began with the Age of Exploration in the 1500s, then contrasted the median age of U.S. companies at IPO in 1980 (six years) with today’s median age of public companies (13 years), implying that the growth opportunities retail investors once accessed through public markets are now largely locked away in private markets.

The tweet ends with a somewhat fatalistic maxim: “In the future, either you tell the computer what to do, or the computer tells you what to do. You don’t want to be on the wrong side of that trade.” The narrative is beautifully crafted, like Silicon Valley’s last serious pitch ad.

For decades, a hard rule in the U.S. private market has been that if you want to invest in private companies, you must first prove you are an “accredited investor”—a barrier that has excluded most ordinary people from venture capital.

USVC bypasses this restriction by registering directly as a closed-end fund under the Investment Company Act of 1940—the same law that governs U.S. mutual funds and ETFs. Once registered, the fund is subject to standardized audits and regular financial disclosures, but in return, it can be open to all investors without requiring accredited investor verification, and it issues IRS Form 1099 annually, which is far more favorable for individual investors than the K-1 forms typically issued by private funds.

The slogan for USVC repeatedly mentions a figure: $125 billion. This is the total assets currently hosted on the AngelList platform. Since its co-founding by Naval in 2010, AngelList has gradually become a foundational infrastructure for private investment in the United States, hosting more than 4,500 fund managers, managing over 25,000 funds, and supporting more than 13,000 active startups.

USVC's GP Ankur Nagpal described this in a tweet thread as "our unfair advantage," meaning that USVC's stock selection capability does not come from the judgment of Naval or Ankur alone, but rather from using AngelList’s data streams and manager network as a filter.

Ankur Nagpal is part of the day-to-day management at USVC, is the founder of the online education platform Teachable, and currently serves as a GP at USVC and as a founding GP of Vibe Capital, an emerging fund within AngelList. Naval’s role at USVC is Chair of the Investment Committee, responsible for shaping investment strategy but not involved in day-to-day decisions.

Several familiar faces from Silicon Valley were seated on the advisory panel: Cyan Banister, former partner at Founders Fund; Arielle Zuckerberg, who made investments at hedge fund Coatue and Kleiner Perkins; and Jeff Fagnan, founder of Accomplice, an early investor in Carbon Black, PillPack, and Whoop.

This list itself is a signal from USVC to retail investors: we are not a temporary retail investment product—we are backed by an entire mature venture capital ecosystem.

Lift the lid—what's inside USVC?

USVC is structurally different from the ETFs and mutual funds we commonly encounter. It is a perpetual closed-end fund with no fixed term, and its shares are not traded on secondary markets.

Compared to traditional VC funds, it has no 10- to 15-year lock-up period. Compared to ETFs, its shares are not listed on any exchange, and its price does not fluctuate with secondary market sentiment but instead tracks the fair value of the underlying companies.

This structure delivers a “plausibly reasonable” return curve—it won’t be swung daily by secondary market sentiment like publicly traded ETFs, nor will it lock your capital away for a decade like traditional VC funds.

According to the official website, after raising funds, USVC's investment strategy is divided into three pathways:

First, invest in other fund managers. USVC will act as a limited partner, investing capital in emerging fund managers on the AngelList platform whom it believes in. This is USVC’s primary pathway to gaining exposure to early-stage investments.

Second, add to the growth round. When one of the companies in the portfolio succeeds, USVC aims to increase its investment in subsequent rounds to prevent its ownership stake from being diluted as the company raises additional funding.

Article 3: Secondary Shares. Purchase shares in private companies that have already made progress, directly from existing shareholders via the AngelList network.

These three paths carry an implicit meaning: USVC is essentially more like a fund of funds (FOF) than a direct investment fund. Most of its capital does not go directly onto the shareholder registers of OpenAI or Anthropic, but instead first goes to other fund managers, who then make the investments.

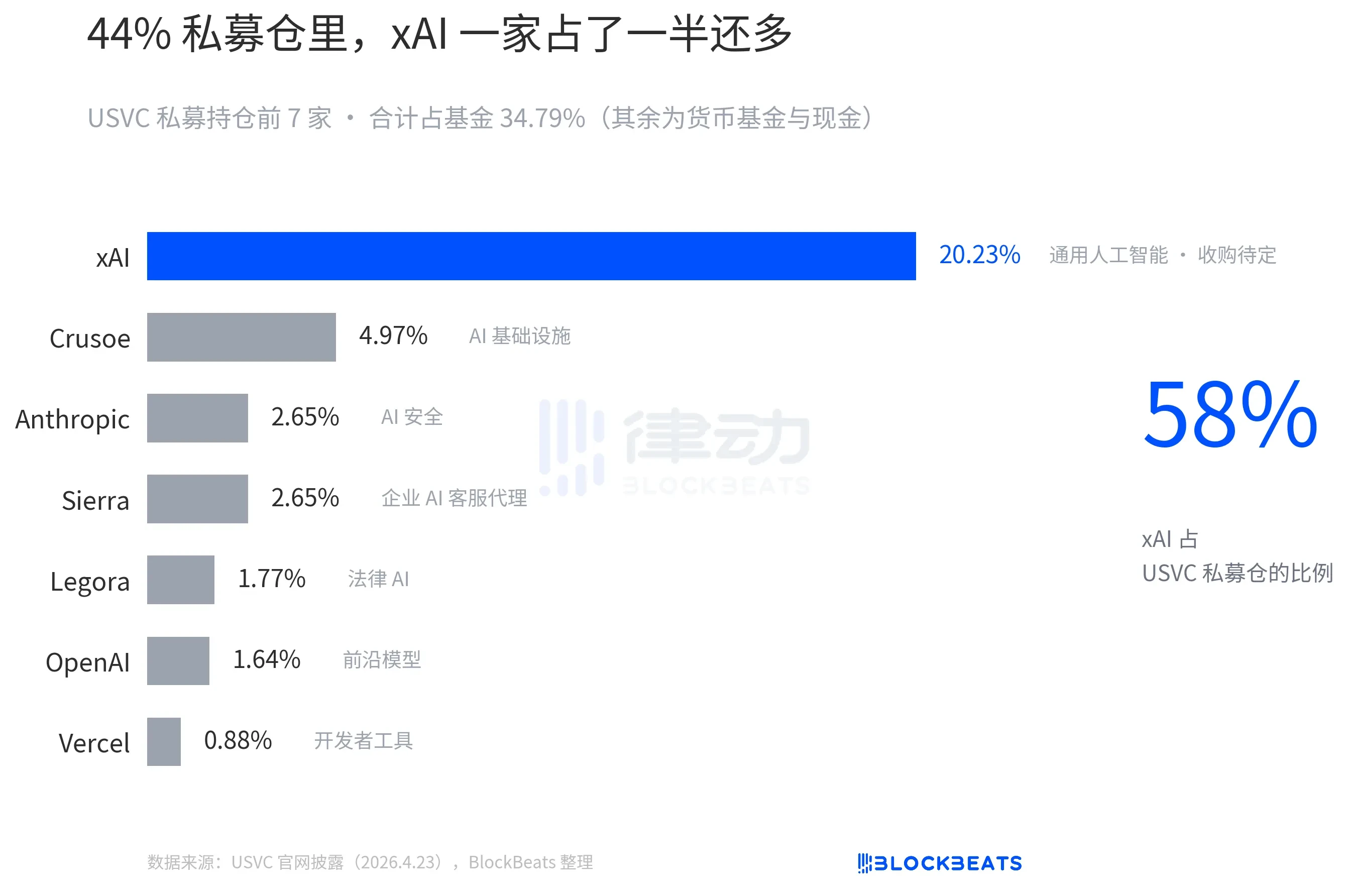

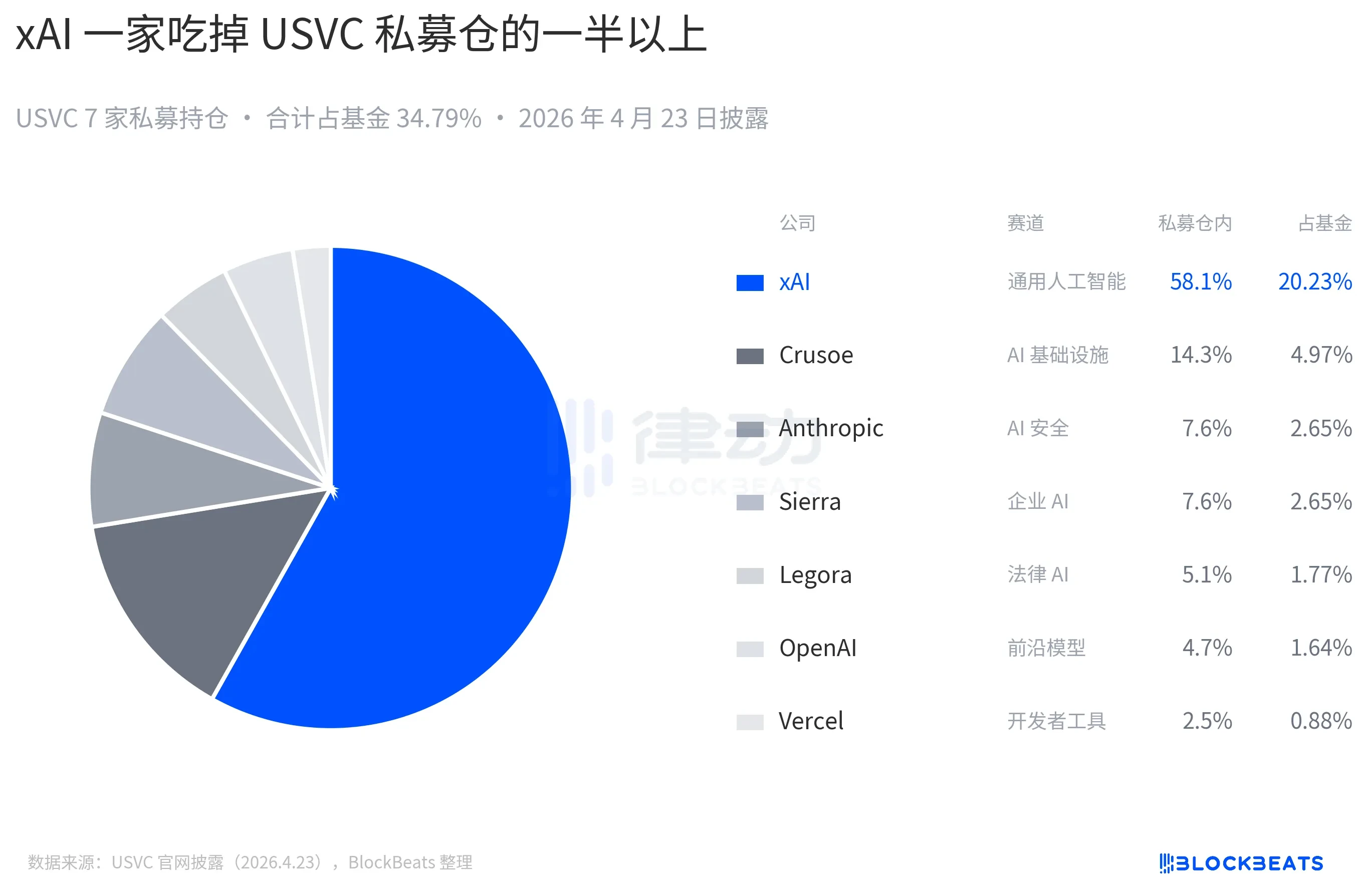

The current holdings disclosed on the USVC website include OpenAI and Anthropic, but the largest allocation is xAI:

The shares of USVC are not listed on any national securities exchange, so you might wonder how USVC returns money to investors.

The answer is a quarterly repurchase offer: the fund has the right to initiate a repurchase once per quarter, with a cap of 5% of the fund’s net asset value. However, this is at the board’s “discretion,” not a contractual obligation. It represents a middle ground—worse than an ETF but better than traditional venture capital. For readers, if you ever need cash urgently, USVC shares are essentially illiquid.

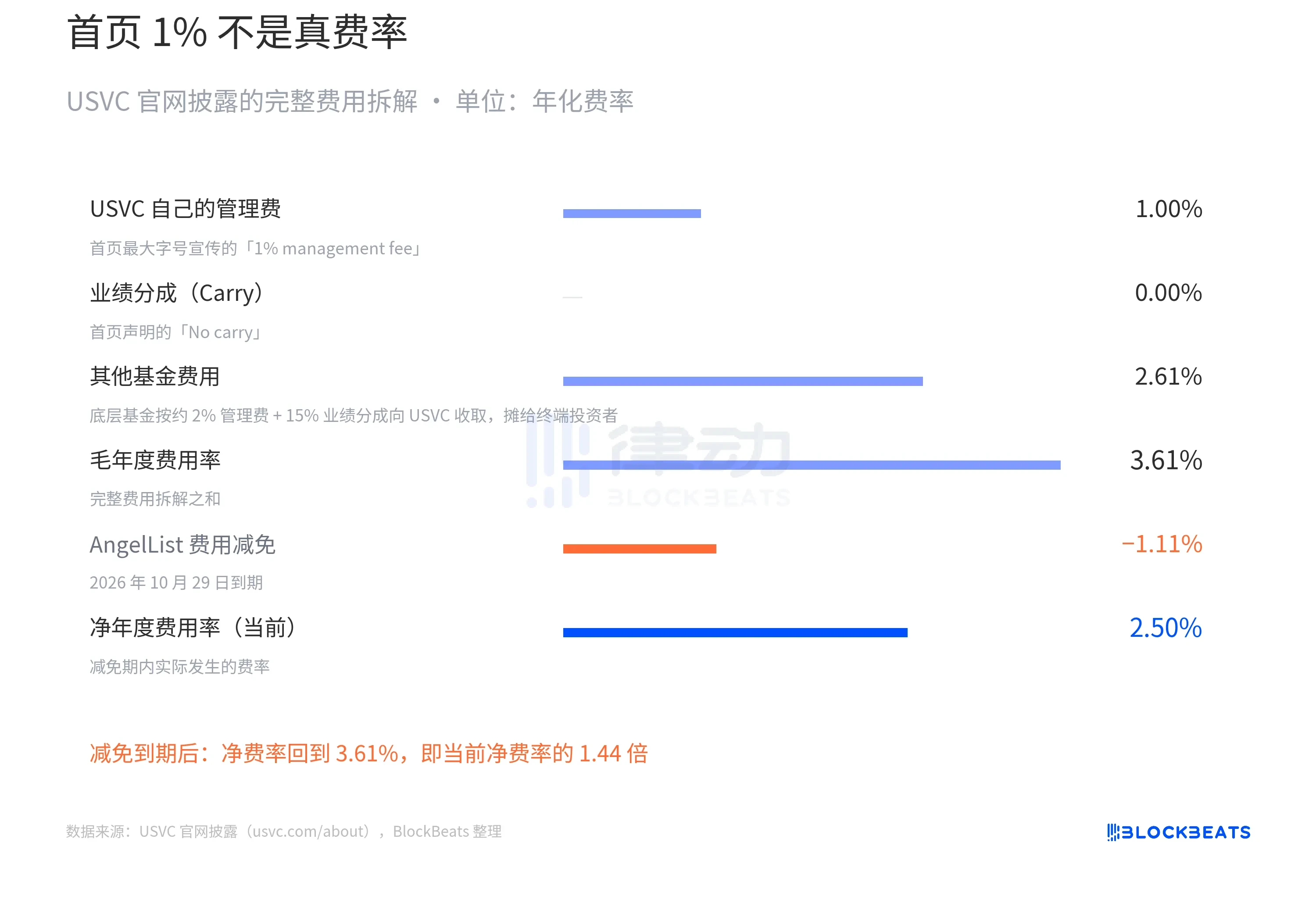

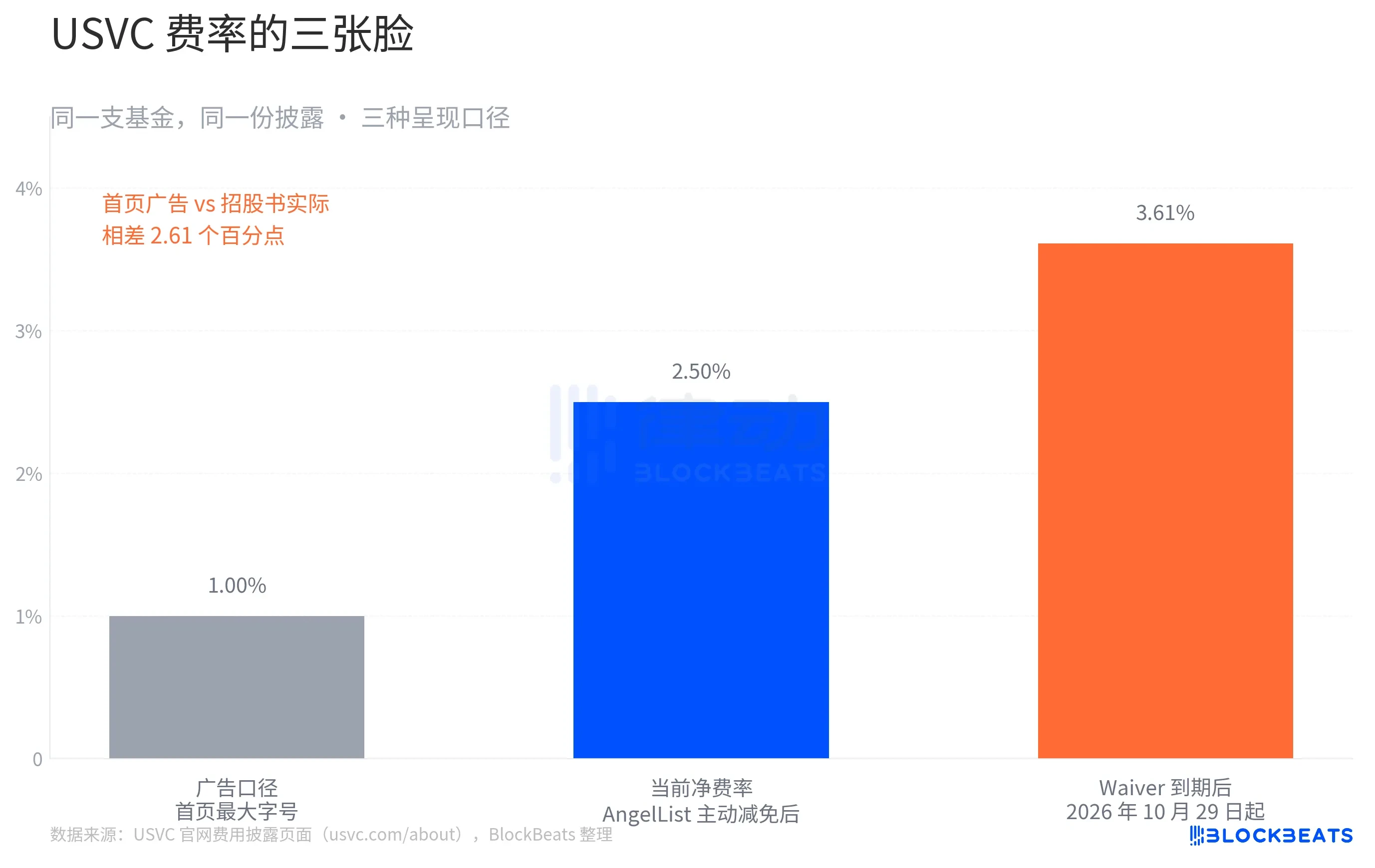

The most noteworthy aspect of the entire USVC story is its fee structure.

At the top of the official website homepage, USVC displays in the largest font size: “1% management fee, no performance carry.” It then casually contrasts this with the traditional VC model of a 2% management fee.

This is the advertising face of USVC. Turn to the fee schedule at the bottom of the same page, and the story changes. The full fee breakdown disclosed by USVC is as follows:

Other fund fees of 2.61% refer to the first of the three pathways mentioned earlier for USVC: investing capital in other emerging fund managers, who charge USVC a 2% management fee and a 20% performance fee. These fees are borne by USVC as a limited partner and ultimately passed on to end investors.

Therefore, the net fee for USVC is actually 2.50%. This is not the final structure. The official website also includes a key limitation: AngelList has agreed to waive a portion of the fees and cover some operational expenses, with the waiver lasting at least until October 29, 2026. However, once the waiver expires, the fee will immediately rise to 3.61%.

Assuming the underlying portfolio of USVC generates an annual gross return of 12%, matching the median performance of top-tier VCs over the past decade. During the waiver period, the net fee is 2.50%, resulting in an investor net return of approximately 9.5%. After the waiver expires, the net fee reverts to 3.61%, yielding an investor net return of approximately 8.4%.

After 10 years of compound interest, $10,000 becomes $24,800 and $22,400 respectively. The difference of $2,400 equals 24% of the initial principal.

This is not a fabricated story. All the numbers are clearly stated on USVC’s official website compliance disclosure page. However, for a fund that champions “financial inclusion,” this disparity is worth highlighting.

Behind the narrative, is this really "mass investment"?

Aakash Gupta, a well-known analyst in Silicon Valley’s product circle, directly reviewed the documents USVC filed with the SEC. He found that, as of December 31, 2025, the total size of the USVC fund was only $8.3 million. Of this $8.3 million, 56% (approximately $4.65 million) was held in a government money market fund yielding 3.66%.

This group of numbers stands in stark contrast to the lineup of seven star companies featured on the official website’s homepage. You see OpenAI, Anthropic, xAI, SpaceX, and might assume your $500 would be allocated roughly equally among these firms. But in reality, the entire fund’s total size under SEC reporting is less than $10 million, with more than half held in short-term Treasury bills.

This can certainly be reasonably explained: the fund was just established, and deploying cash takes time. Ankur later mentioned in a tweet that "there is another batch of promising new projects in the pipeline."

Some community perspectives have criticized USVC as Naval’s new “liquidity exit art,” arguing that USVC is not an entry mechanism but rather a distribution system for positions that have already appreciated significantly.

Over the past decade, private valuations have already captured their major gains: OpenAI rose from $86 billion to $500 billion in three years, and xAI increased from $24 billion to over $200 billion in 18 months. Meanwhile, public markets have already provided several precedents suggesting private valuations may be inflated—Figma dropped below 50% of its private valuation within two weeks of its IPO, and Klarna fell from a private valuation of $46 billion to just $6.7 billion at listing. In this context, packaging and selling these positions to retail investors feels more like a “distribution.”

A quarterly buyback cap of 5% appears favorable under normal market conditions. However, suppose a significant market correction occurs in 2027, causing the valuations of the underlying private companies in USVC to decline and secondary share trading to contract. In such a scenario, the board’s rational choice would be to forgo buybacks this quarter rather than sell underlying assets at depressed prices to meet the buyback requirement.

Silicon Valley developer and investor Kenn Ejima directly commented that USVC is a fund with a limited window of opportunity, the length of which depends on how long Naval remains as chair of the investment committee.

The term “democratization” has appeared several times in the financial history of the past century. A question repeatedly asked is: “Is it opportunity or risk that is being democratized?” But this time, the question you might need to ask is: “Are you buying a fund, or are you buying Naval’s attention from those years?”