Original author: Jared Mitovich, the Wall Street Journal

Compiled by: Peggy, BlockBeats

Editor's Note: AI trading is shifting from "model narratives" to "hardware bottlenecks."

Over the past year, discussions around AI in the market have focused more on large model companies, cloud providers' capital expenditures, and whether AI applications can generate real revenue. But this round of U.S. stock market gains shows that investors are repricing the more fundamental and scarcer segments of the AI infrastructure chain: storage, semiconductor manufacturing, and high-performance chip supply.

The surge in the memory chip sector fundamentally reflects that the AI industry has entered a more tangible phase of expansion. Training data, model parameters, inference workloads, and data center expansions all require higher-performance, higher-capacity storage and computing hardware. For end-tech giants like Apple, rising storage prices mean increased cost pressure; but for chipmakers such as Micron, SanDisk, Intel, and Samsung, this marks the beginning of a new profit cycle.

It is worth noting that the market is not solely driven by optimism. The Wells Fargo sentiment indicator has triggered a "sell" signal for the first time since 2021, suggesting that the current rally has become somewhat overheated. AI remains the dominant theme, but investor focus is shifting: it is no longer about who tells the grandest AI story, but who truly controls the supply bottlenecks and can convert capital expenditures into revenue and profits.

Meanwhile, the Middle East situation, oil price fluctuations, and Fed interest rate expectations continue to unsettle markets. In other words, the new highs in U.S. stocks are not driven solely by AI hype, but rather by a combination of robust AI infrastructure demand, easing geopolitical risks, and favorable liquidity expectations.

The AI bull market is becoming more "physical." As compute power, storage, energy, and supply chains become real constraints, the market is no longer rewarding just companies that tell stories, but manufacturers that provide critical infrastructure.

The following is the original text:

John G Mabanglo / EPA / Shutterstock

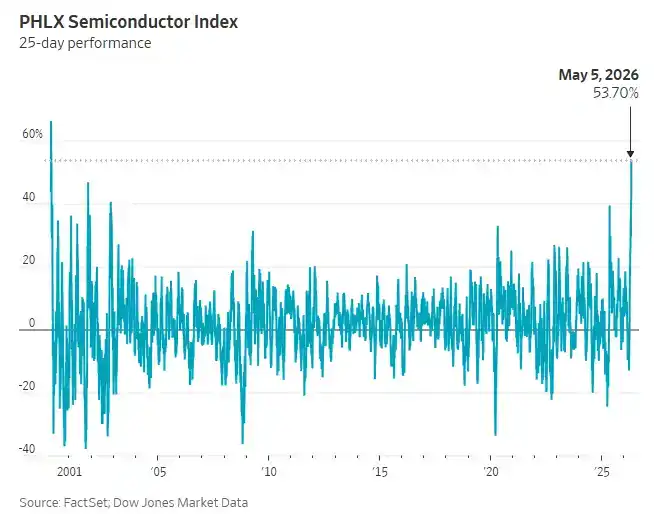

On Tuesday, investors flooded into the memory chip sector, pushing the Nasdaq Composite and S&P 500 to new highs and further cementing the PHLX Semiconductor Index’s best rally since the dot-com bubble.

Since the end of March, the semiconductor index has risen 54%, achieving its best performance over a 25-trading-day period since March 2000. As demand surges for specialized chips driven by artificial intelligence, chip manufacturers are ramping up production to meet market needs.

Rising storage prices are increasing costs for tech giants like Apple, but they represent a major boon for the entire chip manufacturing industry. Tuesday’s surge propelled Intel’s stock up 13%, lifting its market capitalization to approximately $544 billion, surpassing Oracle and Johnson & Johnson. SanDisk, Micron, and Qualcomm all rose over 10%, helping the Nasdaq Composite, which has a heavy weighting in tech stocks, climb 1%.

Ohsung Kwon, Chief Equity Strategist at Woori Securities, said that companies designing, producing, or selling the computing chips required for high-intensity AI tasks are the biggest beneficiaries of the current large-scale AI infrastructure build-out. “This is the real bottleneck,” he said.

Kwon said that AI trading has entered a healthier cycle: investors' focus is shifting from capital expenditures to whether this technology can achieve commercial monetization. This shift in focus is also reflected in the recent earnings reports of tech giants like Amazon and Google—traders are more concerned about whether these companies' massive investments in AI have truly translated into revenue.

Despite the ongoing AI boom, Wells Fargo's sentiment indicator has triggered a "sell" signal for the first time since November 2021. Kwon has described the recent market rally as a "sugar rush" euphoria, suggesting that investors should begin implementing protective measures for their portfolios.

Reports suggest that Apple is considering having Intel and Samsung produce its main chips in the U.S., boosting investor optimism and driving Intel’s stock higher. Samsung’s stock also rose about 5% in the Korean market.

Among major U.S. stock indices, the Nasdaq led gains, with the S&P 500 rising 0.8% and the Dow Jones Industrial Average climbing 0.7%, or 356 points. All 11 sectors of the S&P 500 advanced on the day, with materials and technology leading the gains; the small-cap Russell 2000 index rose 1.8%, setting a new record high. The financial services sector opened lower after Coinbase and PayPal announced layoffs, but later recovered losses and closed nearly flat.

On Tuesday, investors grew more hopeful that the U.S. and Iran could avoid a full-scale resurgence of hostilities following the escalation in the Persian Gulf on Monday.

Near-month Brent crude futures fell 4% to $109.87 per barrel. On Monday, the most actively traded crude contract closed at its highest level in nearly four years following Iran’s attacks on a key oil terminal in the UAE and vessels in the Strait of Hormuz. However, U.S. Defense Secretary Pete Hegseth downplayed the impact of these attacks on Tuesday, stating that the ceasefire agreement with Tehran, which has been in place for four weeks, remains valid.

Bill Northey, Senior Investment Director at Bank of America Asset Management Group, said: "At this point, it appears that the situation has not escalated significantly, and the market has taken a sigh of relief."

He added that although hostilities in the Middle East appeared to ease on Tuesday, the conflict continues to impact future U.S. economic data and the Fed’s interest rate decisions. For example, if the Strait of Hormuz could be safely and fully reopened, it would dampen market expectations of higher inflation and push down 10-year U.S. Treasury yields.

Northey said: "Our baseline judgment is that this volatility is likely to continue."