RV doesn't just grow — it accelerates, and understanding why is what separates a structural read of MVRV from a superficial one.

RV accelerates with each cycle through a simple mechanism. When large volumes trade near a cycle top, the realized price of the UTXOs involved resets to near-top levels. STH (short-term holder) UTXOs are created at recent prices — a flood of them near cycle highs pulls the system-wide realized price sharply higher. Since each cycle reaches a higher ATH, the cost basis of newly created STH UTXOs climbs with it. Even with 10-year-old LTH (long-term holder) UTXOs dormant at $200, the STH UTXOs created at $60K–$100K dominate the average realized price. Result: RV accelerates each cycle as ATH-level prices get imprinted onto new UTXOs, while MV decelerates as market cap grows.

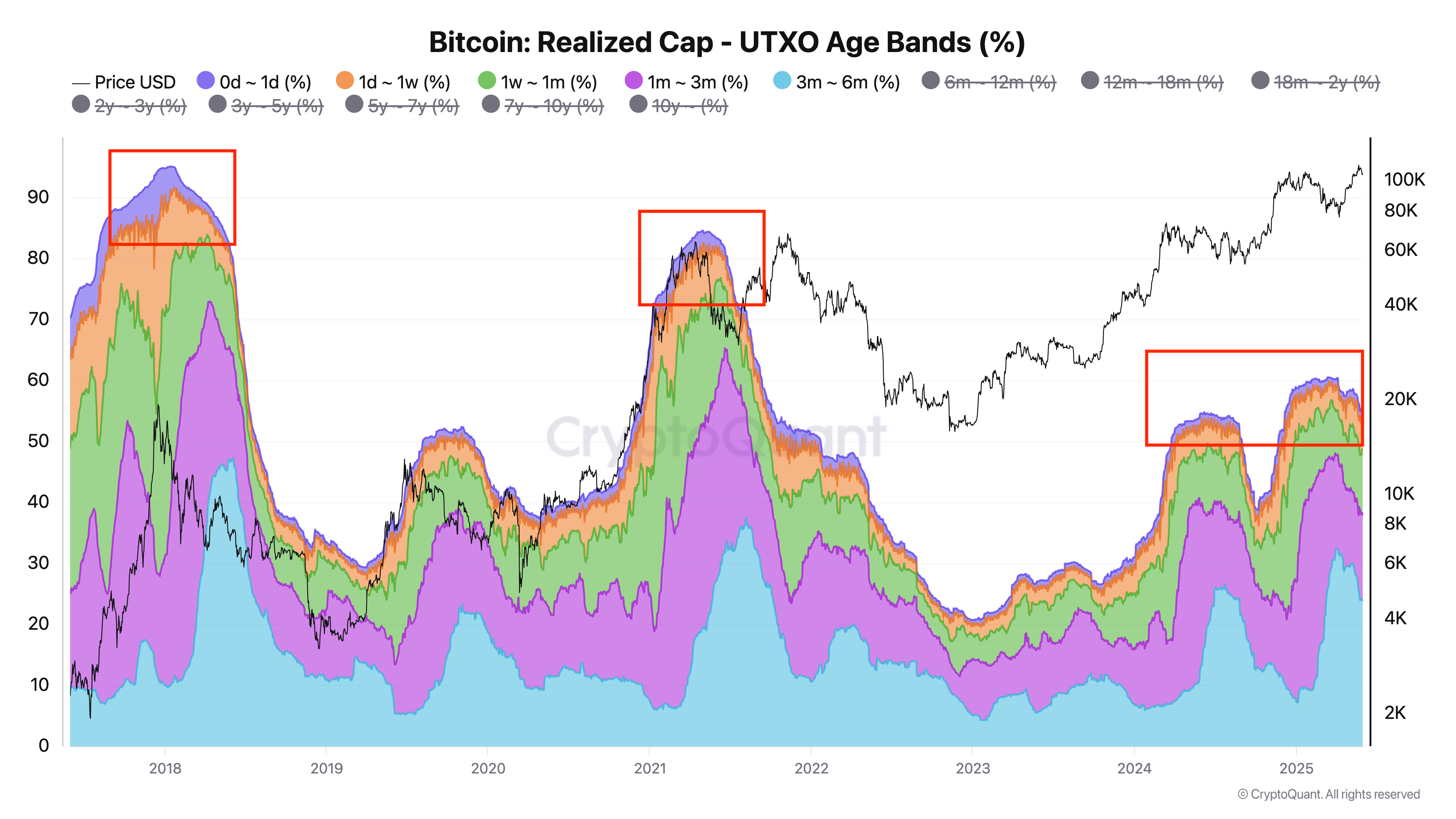

MV deceleration and RV acceleration together explain why peaks fall at a roughly steady pace — but not why they now fall below the trendline. An additional variable is at work. The share of participants treating BTC as a long-term asset has been structurally growing. The share of BTC supply held by STH (Realized Cap basis):

- 2017 peak: ~90%

- 2021 peak: ~80%

- 2024 peak: ~50%

That supply sits inside RV with high cost bases, compressing the room MVRV has to expand.

On top of that, the time spent meaningfully above the prior ATH has shrunk. After hitting $73K in early 2024 (about 6% above the 2021 ATH), BTC ranged near that level for six months — giving RV ample time to catch up. The window for MV and RV to diverge was extremely short.

The MVRV ceiling isn't just lower each cycle — it's now falling below what even an extrapolated trendline would predict.

That structural shift has direct implications for how fixed thresholds should be treated — which is next.