Author: Facing AI

Same night, two earnings reports, two different emotions.

Meta's stock price surged after hours following the release of its earnings report.

Almost at the same time, Microsoft was declining.

The figures on paper are not that different; what truly creates the gap is the market's attitude toward the "future."

01. Zuckerberg really has everyone hanging on his every word.

Meta's latest earnings report is really impressive.

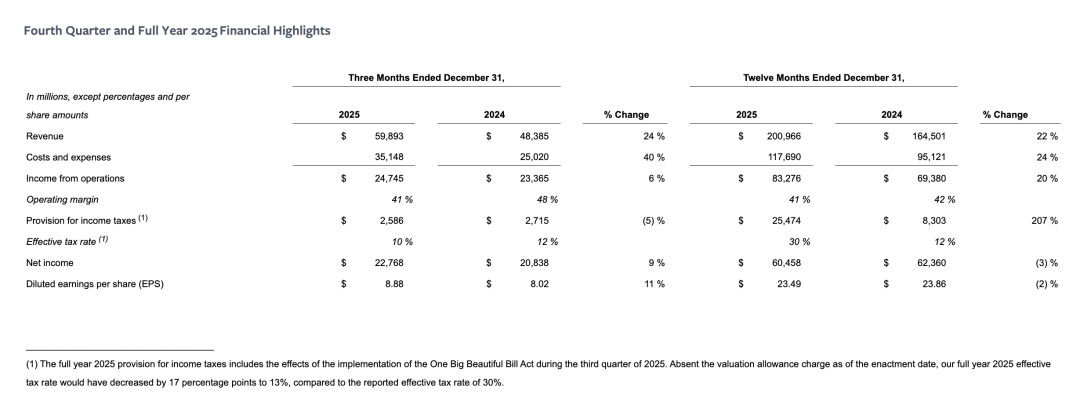

Q4 of the 2025 fiscal year, Meta:

Revenue reached $59.893 billion, representing a 24% year-over-year increase, significantly exceeding Wall Street's expectations.

· Net profit of $22.768 billion, representing a 6% increase compared to the previous year.

· Diluted earnings per share of $8.88, representing an 11% increase from the previous year.

The majority of the revenue still comes from advertising. In the fourth quarter, Meta's advertising revenue was $58.137 billion, accounting for 97% of total revenue. Although revenue from other businesses is smaller, it grew by 54% year-over-year.

From an operational perspective, the average daily active users (DAP) of the Meta app family reached 3.58 billion, representing a 7% year-over-year growth.

In the fourth quarter, the ad impressions on the app family grew by 18% year-over-year, and the average price per ad increased by 6% year-over-year. In 2025, these growth rates are expected to be 12% and 9% annually, respectively.

Meta has always credited the positive changes in its advertising business to the boost from AI, as AI helps improve both the volume and pricing of advertisements.

For the entire year of 2025, Meta's total revenue was $200.966 billion, representing a 22% increase compared to $164.501 billion in 2024; its net profit was $60.458 billion, a 3% decrease compared to $62.360 billion in 2024.

However, since the AI industry has taken off, market reactions to the earnings reports of major companies have never solely depended on the performance results. Investors are always more concerned about: What's next?

In recent years, the constant question hanging over Meta has been its extravagant spending. For AI, Zuckerberg is going all out.

This has not changed if you look at the numbers alone.

Meta has once again raised its spending forecast, with capital expenditures expected to range between $115 billion and $135 billion in 2026.

Over the past six months, Meta has actively restructured its AI business and established a Superintelligence Lab.

At the earnings call, Zuckerberg stated that the company plans to release its latest AI model within the next few months.

"We will demonstrate our current rapid growth momentum," he said, adding that Meta hopes to "push the boundaries" through its AI research and development efforts.

Zuckerberg's demonstration was like: everything is ready, we're about to start shipping products in full force!

And the market has chosen to believe—or rather, has chosen to bet—that Meta can truly rise up this time.

While the earnings call was taking place, Meta's stock rose after hours by more than 10% at one point.

02 Is Microsoft No Longer Fierce?

In stark contrast to Meta is Microsoft.

For Microsoft, all eyes will be on its Azure cloud computing business, which is experiencing strong demand from companies developing and operating artificial intelligence services.

In the first fiscal quarter ended September, Microsoft stated that demand for Azure services "significantly" exceeded its capacity. Revenue growth for the division is expected to increase in the second quarter.

In fact, the most recent second fiscal quarter showed Azure cloud business revenue growth of 38%, slightly slower than the previous quarter. Microsoft's overall revenue growth also slowed, dropping from 18% in the previous quarter to 17%.

Investors are also closely watching for signs of growth in Microsoft's Copilot product line, which is the company's primary channel for selling artificial intelligence software tools to office workers.

As Anthropic received positive reviews for its new AI tool, Claude Cowork, launched at the beginning of this month, shareholders are becoming increasingly concerned that Microsoft's related business might be "cut off at the pass."

After-hours trading on the U.S. stock market saw Microsoft's stock price drop by more than 8% at one point.

Microsoft was one of the first major companies to successfully "bet" on and boldly enter this wave of AI, making a significant impact. The company has heavily invested in OpenAI and is closely aligned with it. Last July, Microsoft's market value briefly exceeded $4 trillion.

However, entering early also brings its own troubles—entering early means facing evaluation and scrutiny earlier. While Meta is still experimenting and searching for the right path, investors have long been eagerly waiting to see when Microsoft's seemingly firm and confident AI investments will generate revenue that matches their scale.

And when such contributions are delayed or insufficient, the patience of the market is also being tested.

Regarding the slowdown in Azure's growth, Microsoft also emphasized its defense during the earnings call.

CFO Amy Hood said, "If I allocated all the GPUs that were launched in the first and second quarters entirely to Azure, our KPI (growth rate) would have already exceeded 40%."

Hood stated that the issue Microsoft is currently facing is not that Azure cloud services are unsellable. On the contrary, demand is extremely strong, but supply is insufficient. Microsoft's computing power must be allocated not only to Azure but also to AI products like Microsoft 365 Copilot and GitHub Copilot, making distribution challenging.

She even revealed that currently, the majority of Microsoft's huge expenditures are allocated to GPUs/CPU, indicating how tight computing resources are at present.

In addition, Microsoft CEO Satya Nadella directly refuted rumors during the earnings call, countering speculation that the usage of Microsoft's AI tools had declined under competitive pressure.

Nadella revealed that the daily active users of Microsoft 365 Copilot have increased tenfold, the proportion of paying users has grown by 160% year-over-year, and the total number of paying users has reached 15 million.

03 Future, Future, and Future Again

Although ChatGPT is about to turn four this year, major companies generally emphasize that we are still in the "early stages" of AI industry development.

For the future, the giants also generally express optimism.

Zuckerberg has clearly positioned AI smart glasses as the next-generation core computing device, comparing this turning point to the historical moment when smartphones replaced feature phones.

Next, Meta's crucial leap forward will be to gradually restructure its advertising-centric business model into an entirely new revenue system centered around "personal superintelligence."

In contrast, Microsoft's vision for the future is clearly more oriented toward "engineering" and "systems."

In Nadella's narrative, AI is not a single breakthrough hit, but rather a comprehensive enhancement integrated into the operating system, office software, development tools, and cloud infrastructure. Copilot doesn't need to immediately prove how much money it can generate; as long as it continuously improves the stickiness and ARPU (average revenue per user) of Microsoft 365, GitHub, and Azure, commercialization will naturally unfold.

The problem is that the market's patience for "the future" is not evenly distributed.

Meta is still in a stage "where it's allowed to spend money freely": its advertising business remains solid and its cash flow is ample, while its investment in AI is more like a bet on the next major platform;

And Microsoft has already found itself in a position "where it must deliver results"—as the company that bet earliest, invested most deeply, and built the most complete narrative, it is only natural that it is the first to be expected to show quantifiable returns.

Therefore, the same phrase "we are still in the early stages" carries different meanings when applied to the two companies.

Ultimately, the issue isn't whether AI is capable or not, but rather whose side time is on.

Meta still has room for storytelling, while Microsoft has already reached the point where it needs to turn the story into financial results.