In March 2026, Mastercard announced it would acquire the stablecoin payment company BVNK for up to $1.8 billion, with the transaction expected to be completed by the end of the year.

If you look only at the financial data, this transaction is not cheap. BVNK processed $30 billion in stablecoin payments in 2025, yet generated only $40 million in annual revenue—making it difficult to justify the valuation using traditional revenue multiples.

Mastercard is clearly not interested in BVNK’s current level of profits.

What it bought was BVNK’s position in the next-generation payment network. As stablecoins begin to evolve from mere trading instruments within the crypto market into real-world tools for cross-border payments, corporate settlements, and global fund orchestration, what becomes truly scarce is no longer just “who can issue a new stablecoin,” but who can effectively connect fiat bank accounts, payment providers, merchant needs, and on-chain settlement rails.

Whoever controls this connecting bridge has a greater chance of gaining early control over the global payment system’s “Strait of Hormuz” during the transition from legacy payment networks to new ones.

Why BVNK? Why now?

To understand the significance of this acquisition, first look at what BVNK actually does.

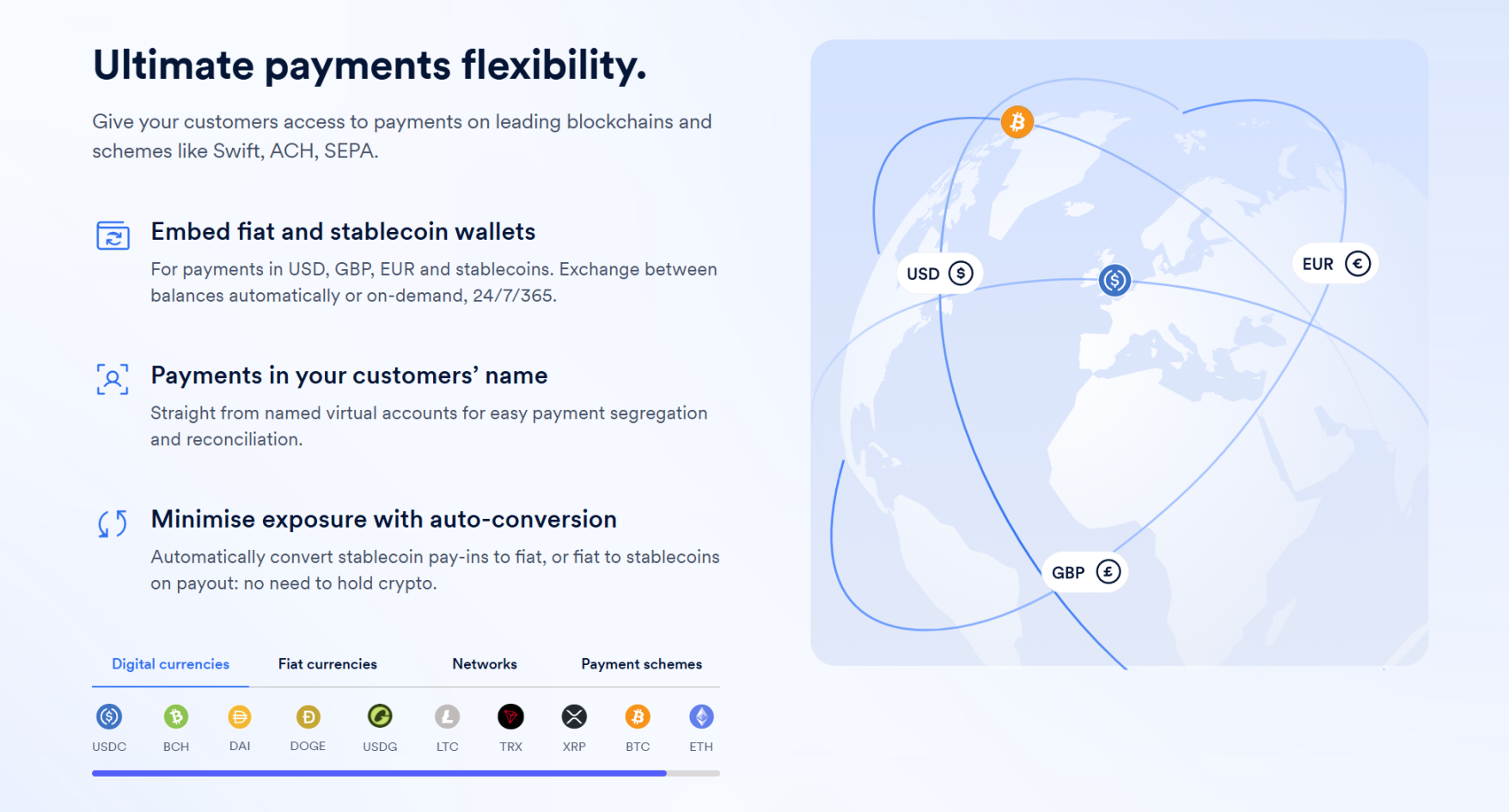

Strictly speaking, BVNK is not a typical crypto company; its most core asset lies not in issuing stablecoins or offering crypto products to retail users, but in embedding on-chain settlement capabilities into real-world payment networks.

In other words, it acts more like a bridge, with one end connected to the fiat payment world and the other end linked to the on-chain stablecoin ecosystem.

This also defines its customer profile as fintech companies, payment service providers (PSPs), and cross-border payment firms such as Worldpay, Deel, and Flywire—organizations that already have substantial real-world global payment and collection needs and require faster, lower-cost fund transfers. However, they often lack the capability to directly integrate with on-chain stablecoin infrastructure—whether in terms of wallet systems, on-chain routing, receiving and sending stablecoins, exchange processes, compliance and risk controls, or system integration—all of which most enterprises prefer not to build and maintain themselves.

What BVNK does is encapsulate this complexity, offering a comprehensive solution centered on stablecoin payments and integrating these capabilities into businesses' existing payment workflows—essentially selling the interface capabilities that enable enterprises to use stablecoin rails.

Source: BVNK

And this is precisely what Mastercard most wants.

Many people discussing stablecoin payments tend to focus on surface-level advantages like "faster" or "cheaper," but for Mastercard, Visa, banks, and cross-border payment networks, the real challenge posed by stablecoins is not merely the emergence of a faster, cheaper payment method—it’s the possibility that payment networks themselves may begin to migrate.

In the past, the majority of global cross-border payments relied on correspondent banking networks—a global funds transfer system composed of layered bank account relationships, clearing channels, and local financial institutions. While this system benefits from maturity and broad coverage, it suffers from long pathways, numerous intermediaries, slow settlement times, and high fees, as nearly every layer in the cross-border chain extracts its own profit.

For traditional banks and payment institutions, this "slow and expensive" nature is precisely the source of profit, as greater complexity in the payment chain naturally generates fees, foreign exchange spreads, liquidity holding costs, clearing service charges, and a range of additional revenues tied to corporate treasury management.

In other words, traditional cross-border payment systems have never just profited from the money being transferred—they’ve profited from the entire ecosystem of financial control surrounding those transfers. This is the truly sensitive aspect of the competition. Once stablecoins begin entering real-world commercial payment scenarios, the most critical value components of the old system will face a complete reshuffling.

The positions once firmly held by banks, card networks, and traditional payment systems now require rethinking: who will connect merchants to funds, who will organize cross-border settlement, and who will control payment access points and liquidity exits?

From this perspective, the impact of stablecoins on card networks is actually devastating. After all, the business models of companies like Mastercard are built on their control over the connection between global merchants and issuing systems, as well as their position as an indispensable node in payment flows across regions, currencies, and institutions.

Therefore, Mastercard’s acquisition of BVNK is essentially purchasing a "bridge" connecting the old world to the new轨道—what it seeks is not immediate profit, but rather preemptive control over the critical "Strait of Hormuz" before stablecoin payments become mainstream, completely eliminating the possibility of bypassing card networks.

This is also why Mastercard itself admitted on its investor call that building similar blockchain financial capabilities would take “a considerable amount of time.”

In other words, buying is faster than building.

Source: BVNK Blog

Ultimately, from a traditional M&A perspective—looking only at metrics like revenue multiples, profit margins, and maturity—BVNK would be hard to justify at this price. But if viewed as a strategic move to secure an early position in the future payments landscape, everything falls into place.

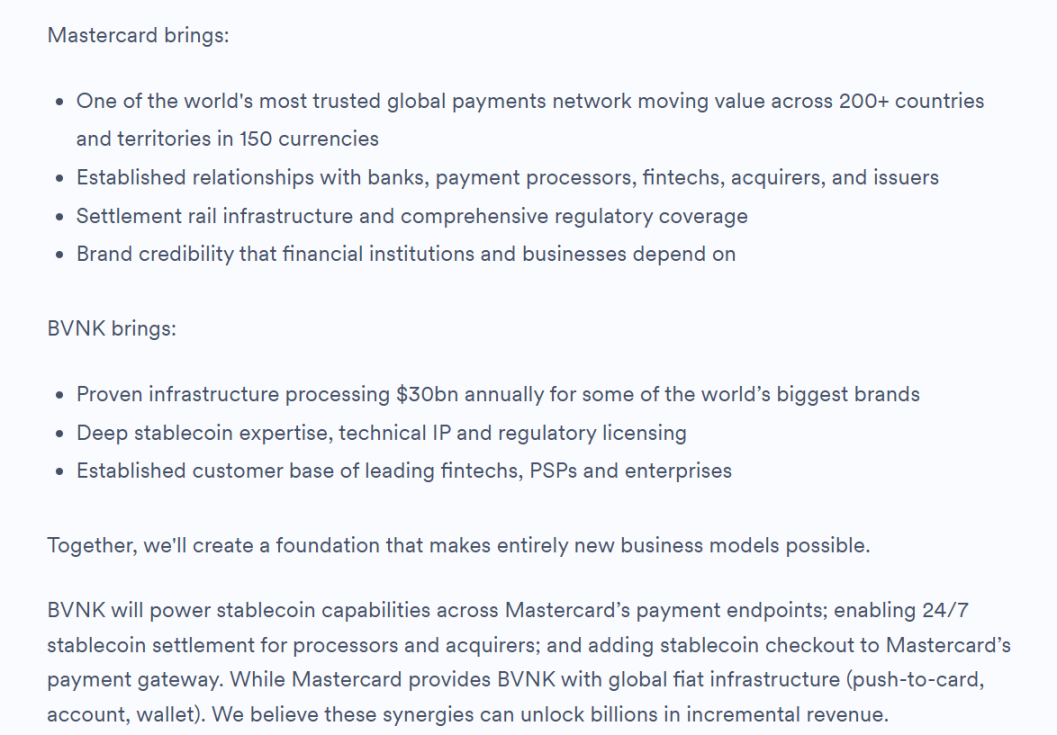

BVNK also clearly stated in its latest official blog that future collaboration efforts will include BVNK providing stablecoin capabilities to Mastercard’s payment endpoints, enabling 24/7 stablecoin settlement for processors and acquirers, and integrating stablecoin checkout capabilities into Mastercard’s payment gateway—directly stating that these synergies are expected to generate billions of dollars in new revenue.

II. The Battle Over "Clearing and Network Control" by Payment Giants

Interestingly, Mastercard was not the first to enter this race—in fact, it was one of the last to act.

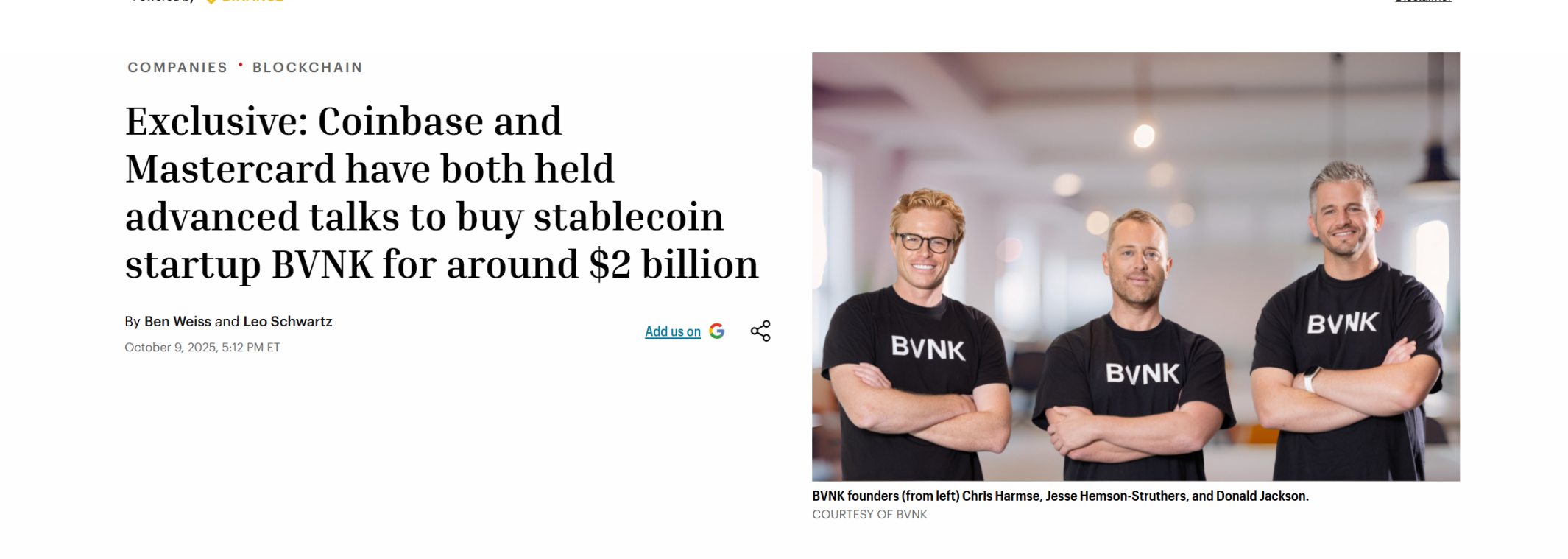

Even before the acquisition was finalized, in early October 2025, Coinbase initiated acquisition negotiations with BVNK, with a proposed transaction range of $1.5 to $2.5 billion. According to multiple sources, Coinbase initially held a leading position in the bidding process and even signed an exclusivity agreement with BVNK.

However, the two parties ultimately announced the breakdown of negotiations that month, creating an opening for Mastercard’s subsequent successful entry.

Source: Fortune

An interesting comparison: In October 2024, global payment giant Stripe acquired Bridge, a stablecoin API provider, for $1.1 billion, setting the record for the largest crypto acquisition at the time; today, one and a half years later, Mastercard paid $700 million more than Stripe, surpassing that record.

Meanwhile, at the beginning of this month, Visa expanded its partnership with Bridge, planning to roll out stablecoin-linked cards to more than 100 countries.

All are giants in payment networks, all acquiring stablecoin payment providers. When viewed on the same map, it becomes clear that from Stripe’s acquisitions to Mastercard’s moves, and even Visa and PayPal’s earlier launch of PYUSD, this is not an isolated bet by any single company—but a synchronized industry-wide positioning effort.

The impact of stablecoins extends far beyond payment experiences—it challenges deeper profit and power structures within the traditional financial system, compelling global payment giants to proactively connect on-chain accounts, stablecoin assets, and merchant payment endpoints, bypassing or avoiding others bypassing the issuing banks and card networks in traditional payment pathways.

This is why companies like Bridge and BVNK have suddenly become scarce—they truly hold value at a critical intersection, connecting on-chain accounts and stablecoin assets on one side, and merchants, enterprises, payment service providers, and fiat settlement networks on the other.

In other words, the industry has long moved beyond the initial stage of “who issues stablecoins” and entered the second half, where the focus is on “who can truly build a functioning network around stablecoins.”

At the same time, the value of this "stablecoin network" is also likely to be further amplified in the AI era.

A long-underestimated trend is that the entities initiating payments in the future may no longer be exclusively humans, but increasingly agents, robots, and automated systems. Traditional card networks excel at organizing payments around human consumption, acquiring, issuing, and card-based account systems. However, as AI agents become more widespread, the demand for small-scale, high-frequency, automated settlements between machines may not naturally align with card networks, which were designed for the consumer finance era.

In contrast, on-chain payments and stablecoin rails better align with these new demands, as stablecoins inherently enable 24/7 operation, programmability, support for high-frequency microtransactions, global unified settlement, and eliminate the need for complex intermediary authorization. In other words, stablecoins are not just competing for today’s existing cross-border payment volume—they are likely targeting an even larger future incremental payment market.

Traditional giants are also investing heavily in this emerging field; for example, Visa Crypto Labs has launched its first experimental product, Visa CLI, enabling AI agents to securely pay for required fees when writing code, without needing API keys for programmatic card payments.

Source: 𝕏

Ultimately, stablecoin payments are not just a patch to the old system—they aim to redraw the map of the next-generation global payment network.

Continuing with this logic, what will be more worth monitoring in the future may not just be those single-point business roles that most resemble stablecoin issuers, but rather those participants positioned at the intersection of trading, compliance, institutional liquidity, and payment network expansion—entities with a greater potential to evolve into platform-level nodes in the stablecoin era. They may not be the hottest in the short term, but they are often closer to the core of long-term competition.

Behind this judgment, a larger reality is taking shape.

Three: One Map, Two Solutions—New Perspectives Beyond the Solutions

Objectively, Mastercard’s acquisition of BVNK also fills a critical gap in market understanding: the value of stablecoins lies not only in issuance but also in connectivity; not just in compliance credentials, but in the ability to organize liquidity and payment networks.

This is also the fundamental reason why giants like Stripe and Mastercard continue making acquisitions—they are not just buying specific stablecoin technology, but the potential to build a network around it. After all, only when on-chain accounts, stablecoin liquidity, merchant use cases, fiat settlement, and regulatory compliance are truly integrated will stablecoin payments evolve from a “new tool” into a “new network.”

However, one thing to note is that giants like Mastercard and Stripe have essentially taken a path of transitioning from traditional finance, acquiring on-chain capabilities through acquisitions and leveraging their existing distribution networks to scale stablecoins. While this path is clear, it requires breaking free from the weight of a long-standing legacy and redefining their relationship with the blockchain.

This also means that, in addition to actively migrating from the traditional financial system toward stablecoins, there is another solution with the same goal but a different starting point.

Yes, those compliant platforms that were born natively on-chain are reversing the flow—spreading TradFi from stablecoins. They don’t need to switch tracks because they’ve always been on them.

Taking Hong Kong, one of the regions with the fastest progress in global crypto regulation, as an example, over the past several years, multiple licensed and compliant platforms such as OSL and HashKey have emerged. Unlike traditional payment platforms that treat stablecoins as a new service to integrate, these native compliant platforms, which have grown out of digital assets and on-chain liquidity ecosystems, are inherently better positioned at the core pillars of the stablecoin era: trading, custody, liquidity, regulatory compliance, and the ability to extend into payment use cases.

As Hong Kong’s regulatory framework for stablecoins continues to advance, licensed platforms have begun to put this potential into practice. For example, OSL clearly transitioned last year toward becoming a payment and settlement infrastructure provider for stablecoins; in January this year, it completed the acquisition of global Web3 payment service provider Banxa, and in February launched USDGO, an enterprise-grade USD stablecoin compliant with U.S. federal regulations and eligible for compliant distribution in Hong Kong, with a focus on e-commerce, bulk trade, and interactive entertainment sectors.

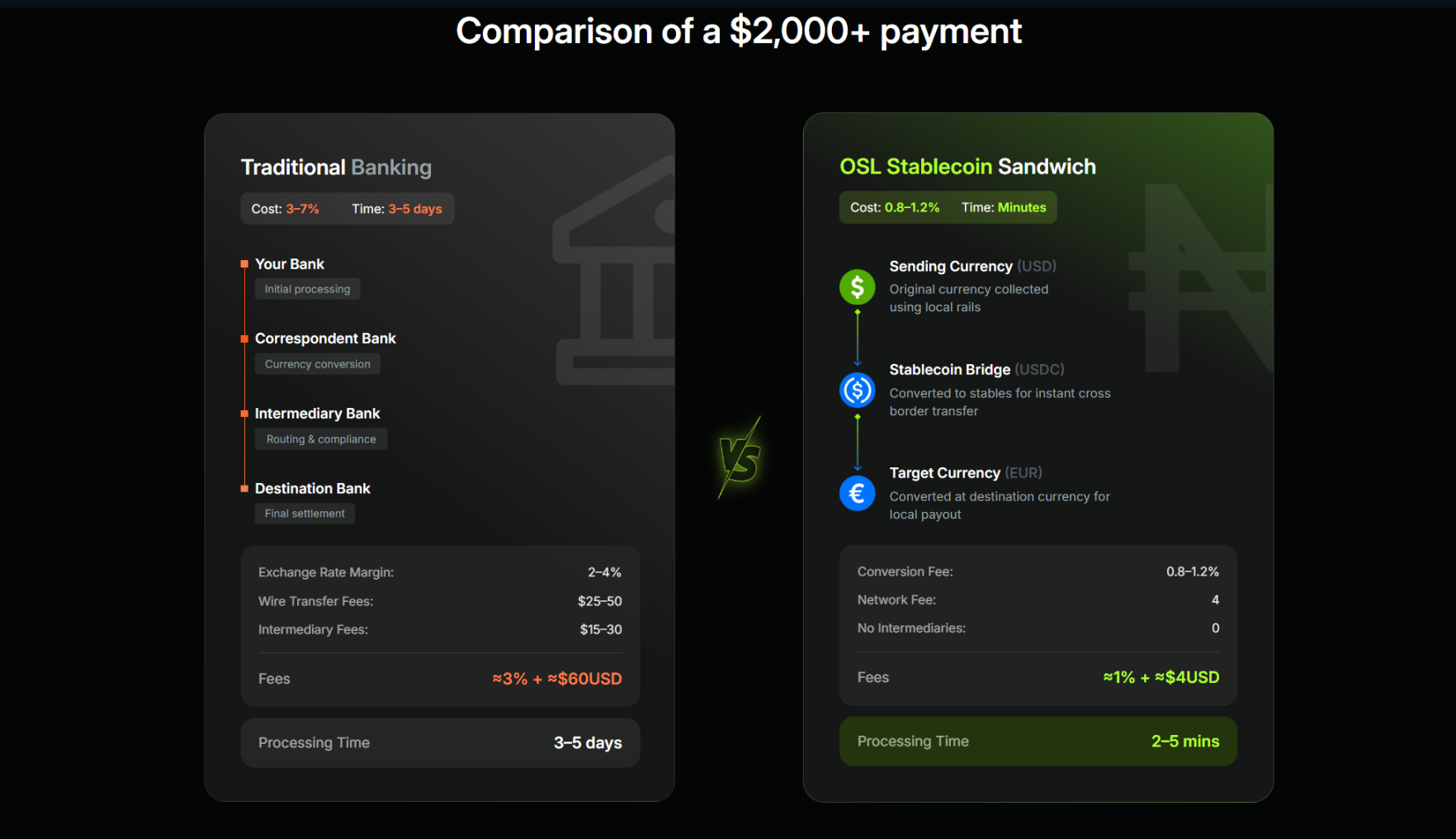

This is a classic implementation pathway combining TradFi and digital finance: enterprises use USDGO for cross-border settlements. When combined with OSL BizPay’s all-in-one stablecoin payment and settlement capabilities, it enables seamless conversion and circulation between fiat and stablecoins. Leveraging its licensed and compliant network across multiple markets, this end-to-end flow can facilitate fiat on-ramping, on-chain stablecoin settlement, account management and fund aggregation, treasury optimization, and fiat off-ramping—all without relying on the traditional SWIFT system—while fully meeting compliance, regulatory, and audit traceability requirements.

This presents an interesting contrast to Stripe’s acquisition of Bridge and Mastercard’s acquisition of BVNK: both are heading toward the same destination—“on-chain accounts + stablecoins + a global payment network”—but one path involves actively switching tracks from an existing ecosystem, while the other relies on existing infrastructure, waiting for increased traffic, use cases, and regulatory conditions to naturally scale.

Two solutions, each with its own logic and time window.

Source: OSL

Precisely because of this, the upcoming announcement of the results of Hong Kong’s first round of stablecoin issuer license approvals, which coincides almost exactly with Mastercard’s acquisition of BVNK, is particularly noteworthy.

The long-term value of stablecoins to the global financial system ultimately depends on how many real, functioning networks enable funds to move faster, cheaper, and more reliably, making them truly usable by businesses and individuals.

Therefore, what’s truly worth watching in the next phase is which players can turn the “entry point” into “traffic,” the “traffic” into a “network,” and the “network” into a new global payment infrastructure.

In conclusion

Ultimately, Mastercard spent $1.8 billion not on a business, but on a position.

Viewed within a larger framework, it becomes clearer that the global payment network is irreversibly shifting toward stablecoins, with varying speeds and paths, but ultimately competing in the same endeavor:

Who can truly connect on-chain accounts, liquidity, payment scenarios, and compliance frameworks into a unified network?

And this is precisely the question most worth continuing to explore in the next phase, especially as stablecoins cease to be mere on-chain proxies for the dollar and begin to retroactively penetrate the traditional financial system.

The real change may have just begun.