Original author: Bull Theory

Compiled by: Ken, Chaincatcher

From the number of allegations faced, Jane Street’s entire business model appears to be designed to artificially trigger market crashes to extract liquidity and profit from them.

This situation has not occurred just once, but multiple times.

The Indian stock market case is the clearest example of how Jane Street operates. They ran an algorithm similar to a "10 a.m. crash" in India, earning $4.23 billion, but were eventually exposed and temporarily banned by the Securities and Exchange Board of India.

Here's how it works.

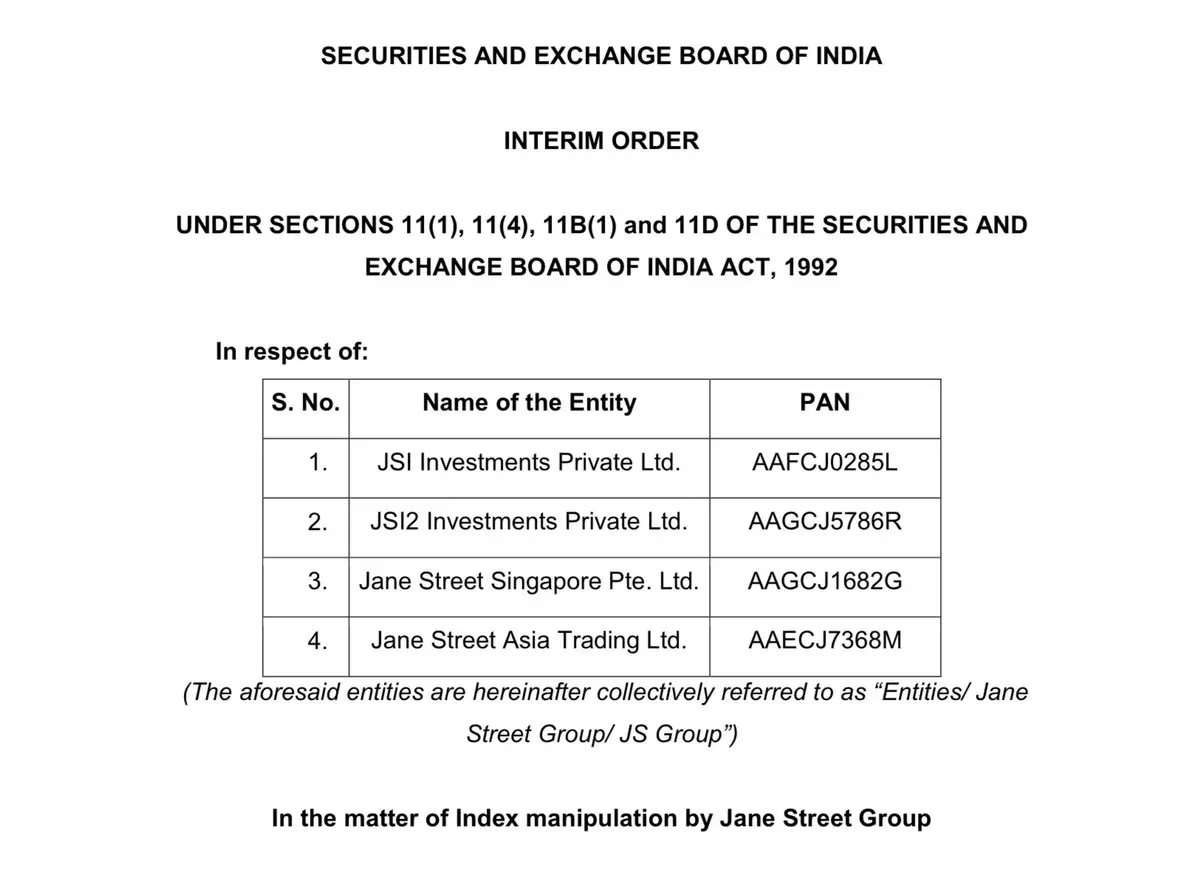

Indian script

Between January 2023 and March 2025, Jane Street generated approximately ₹365.02 billion in net profits through its operations in India. Of the 21 designated settlement dates, SEBI identified ₹48.4357 billion as suspected illegal proceeds. SEBI issued a 105-page interim order, followed by a trading ban. The disputed funds have been deposited into a third-party escrow account. Relevant appeals are currently ongoing.

What matters is not the ban itself, but the underlying mechanisms behind it.

Jane Street's operational architecture is as follows:

1. Jane Street Singapore Pte Ltd (FPI)

2. Jane Street Asia Trading Ltd (FPI, Hong Kong)

3. JSI Investments Pvt Ltd (Indian subsidiary)

4. JSI2 Investments Pvt Ltd (Indian subsidiary)

This separation of entities allows the publicly visible trading platform and the actual profit-generating operations to belong to different corporate entities.

How does expiration date manipulation work?

The settlement of index options is based on the final value of the index on the expiration date. Even minor fluctuations in the index on the expiration date can result in substantial gains on the options side.

The Securities and Exchange Board of India describes the strategy as operating as follows:

Morning session (approximately 9:15 AM to late morning)

This Indian entity is actively buying the constituent stocks and futures of Bank Nifty.

A large order has been placed.

On certain days, their trading volume accounts for a significant portion of the total market volume.

Buying blue-chip stocks pushed up the index. Meanwhile, offshore entities established large short option positions.

Sell a call option.

Buy a put option.

Net exposure is strongly bearish.

From the delta value, the size of the options position is several times that of the stock position, indicating that buying the stock is not the primary bet, but rather a preparatory step.

Afternoon session (late morning to close)

After building the options book, this Indian entity reversed its trading position, beginning to heavily sell the same stocks and futures.

Selling pressure has caused the index to decline. If the index closing price is near certain strike prices, out-of-the-money call options will become worthless, while put options will appreciate significantly.

The spot stocks incurred slight losses, while the options position generated substantial profits.

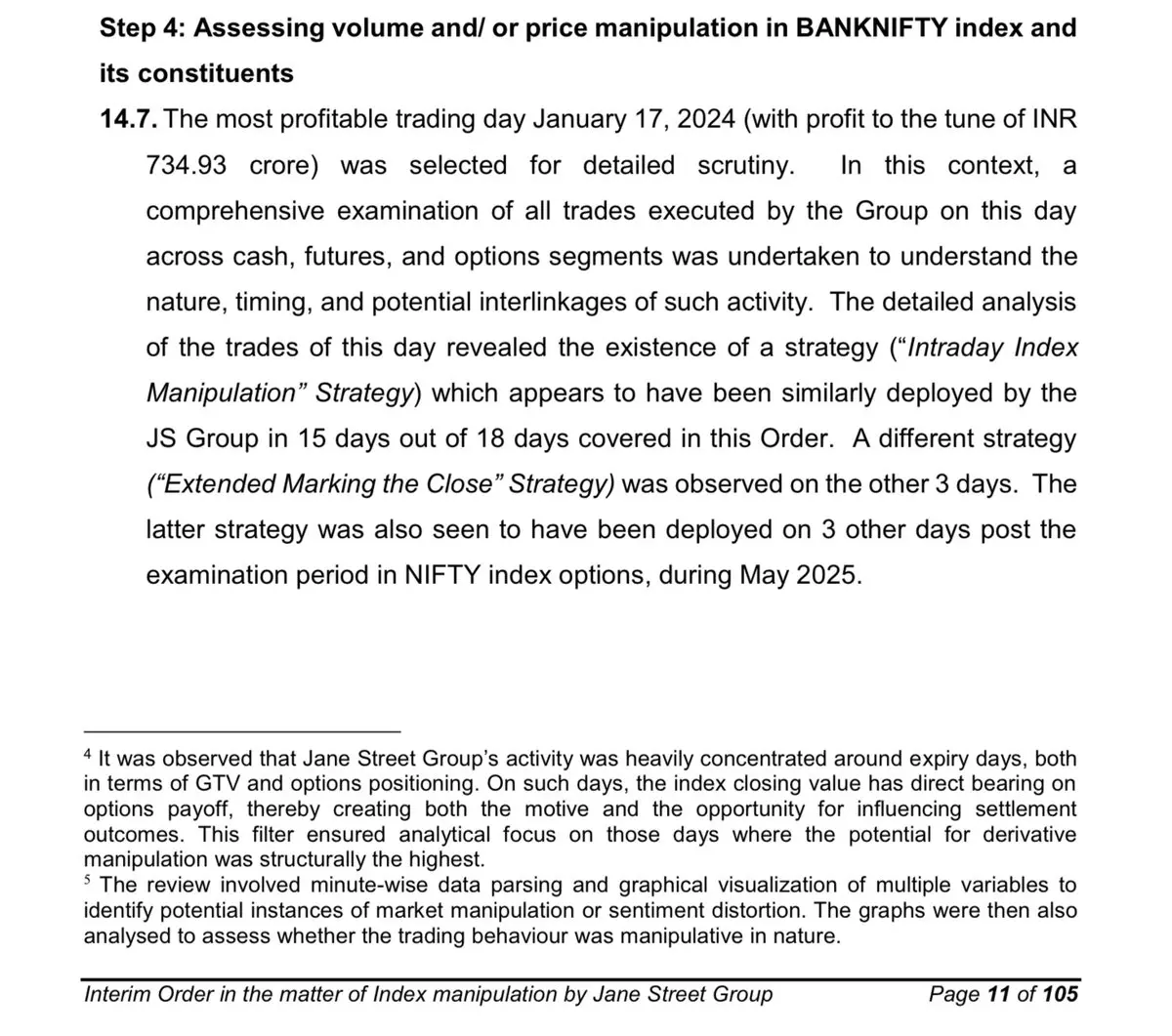

SEBI illustrates:

Morning buy orders reached 437 billion rupees.

Options delta exposure has significantly increased. Cash/futures loss of 6.16 billion INR.

Options profit: ₹73.493 billion.

Daily net profit: ₹67.333 billion.

Spot market activities affected the settlement levels, while the derivatives book captured the actual profits. This is India’s usual tactic: leveraging the funding advantage of the underlying asset to manipulate derivatives returns.

2) Manipulation script at 10:00 AM

Now let’s look at Bitcoin.

For months, selling pressure has repeatedly emerged around 10 a.m. Eastern Time. This time period is significant:

U.S. stock markets are open.

Increased liquidity.

Large orders can be executed efficiently.

The derivatives market is active.

Observed pattern:

Price dropped sharply. Leveraged long positions were liquidated, triggering a chain reaction of forced selling. Price then stabilized.

The cryptocurrency market has extremely high leverage. A drop of just 2% to 3% can wipe out a large number of long positions.

When the liquidation engine starts:

The exchange automatically sells the collateral.

Market order hits the order book.

The price continues to decline.

Trigger more liquidations.

If a large trading firm aggressively sells off during this window: it can initiate the first wave of decline. The liquidation mechanism amplifies this trend. The chain reaction completes the rest of the liquidation. After forced selling clears out positions, prices often rebound. This is structurally very similar to the India case: in India, indices were manipulated to influence options payouts. In cryptocurrency, spot price movements affect derivative liquidations and futures positions.

The movement of the underlying asset is the trigger, while the derivatives side is the true profit engine.

Another crucial detail: this 10 a.m. pattern ceased after the lawsuit against Terraform was filed on February 23, 2026.

Rather than facing selling pressure, Bitcoin has rebounded. Those liquidated were short sellers, not long holders. When a recurring mechanical pattern vanishes just as legal regulatory pressure emerges, market participants naturally take heightened notice.

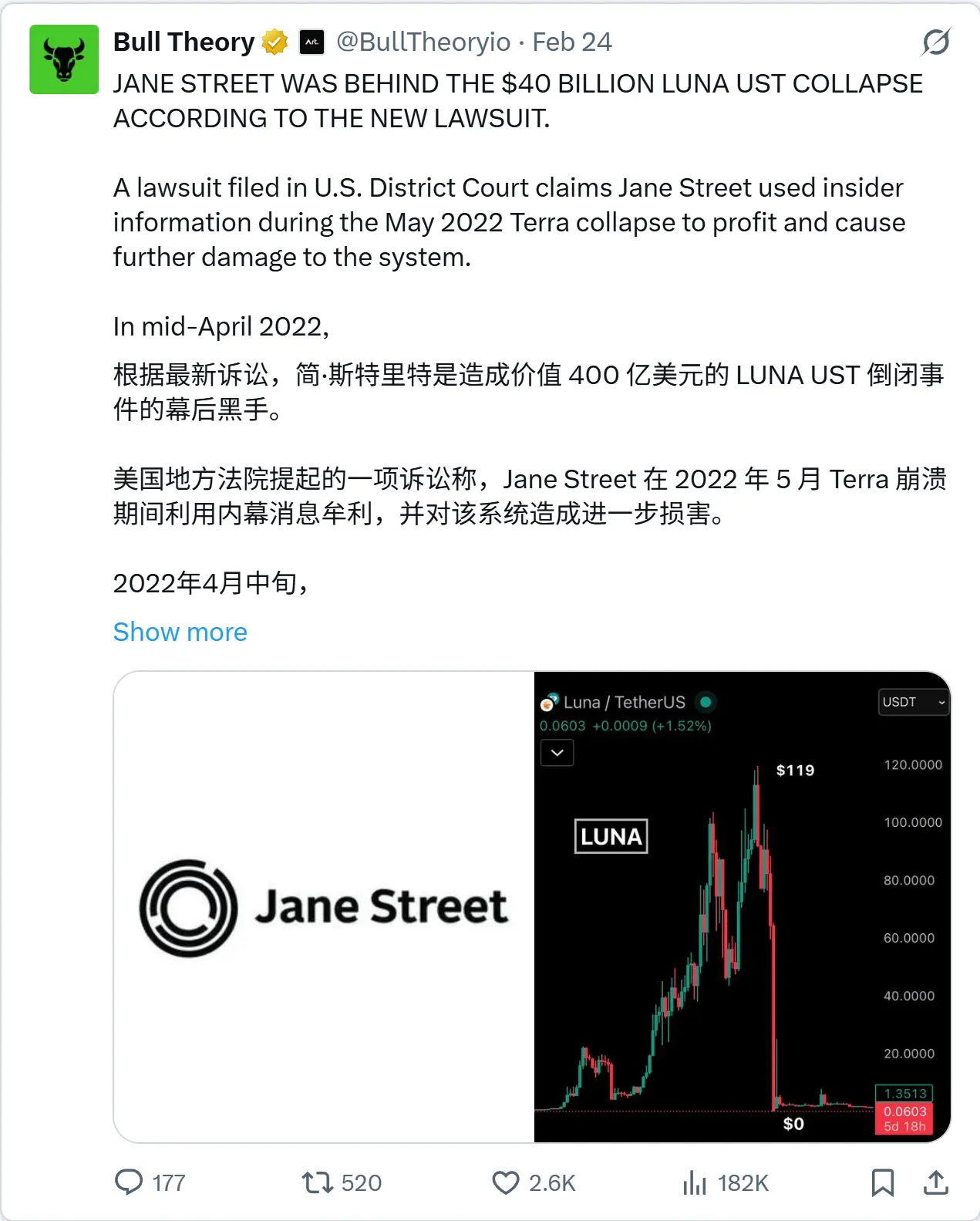

3) From a Bitcoin perspective, was the LUNA collapse used to force BTC lower?

In May 2022, Terra’s UST stablecoin collapsed from a $40 billion ecosystem to zero within just a few days. The peg mechanism was broken, panic spread rapidly, and the Bitcoin reserves intended to defend the system were forced to be deployed under extreme pressure.

In addition to the de-pegging event itself, the lawsuit raises another structural possibility.

Terraform Labs previously used its Bitcoin reserves to maintain UST's peg. These reserves had to be deployed immediately if UST became unstable.

This means that in an emergency, Bitcoin must be sold or pledged as collateral, and emergencies completely eliminate bargaining power.

Litigation allegations:

Jane Street knew that the liquidity in the Curve pool had been depleted.

In an extremely illiquid market, they executed a sale of $85 million in UST.

The pegged exchange rate collapsed rapidly.

During the crisis, Jane Street maintained direct contact with Do Kwon.

Reports indicate that the discussion included purchasing Bitcoin at a steep discount, with the amount potentially ranging between $200 million and $500 million.

If Terraform is forced to defend the peg, they must quickly mobilize their Bitcoin reserves. If someone anticipates this pressure coming, increasing short pressure on UST would accelerate that moment.

Applying greater pressure to the pegging mechanism means:

Accelerating the use of reserves

Undermine the other party's negotiating position

Get BTC at a discounted price

The resulting speculation is simple:

Was this crash merely a routine trading event, or was it exploited as leverage to acquire Bitcoin reserves at extremely low prices?

These are allegations in ongoing litigation. However, the sequence of events clearly reveals the underlying financial motives.

If you'd like a full analysis of the Terra event, we've published a detailed tweet.

4) Next is the ETF

Jane Street has become an authorized participant for several major Bitcoin ETFs. Authorized participants are at the core of the ETF creation and redemption mechanism.

They can:

Create ETF shares.

Redeem ETF shares.

Hedge using futures.

Sell options.

Perform arbitrage spread.

The publicly filed 13F documents only show long positions in ETFs. However, they do not show: short futures, swap contracts, sold options, or net hedged exposure. The disclosed long positions are not equivalent to net long exposure.

It could be:

Go long ETF stocks, short CME futures, short options, pair trading.

The public only sees the visible trading interface, while the complete derivatives ledger remains hidden in the background. Now, combine this with the recurring pattern of spot selling.

If the spot price is under pressure within a specific time window, while ETF exposure is increasing, the visible surface data fails to reveal the full strategy.

In India, stock trading is transparent, but options exposure is the real driver of profits. In ETFs, stock holdings are transparent, but derivative positions may not be disclosed. The structural similarity between the two lies in the opacity between visible and hidden trading.

5) Most importantly, their trading techniques are classified as confidential.

The Millennium Lawsuit—The $1 Billion Strategy That Was Sealed. The Millennium Lawsuit is no mere footnote; it strikes at the technical core of the entire architecture.

At the beginning of 2024, two senior traders left Jane Street:

Doug Schadewald — Senior Index Options Trader

Daniel Spottiswood — his direct subordinate

They joined Millennium Management. Shortly after, Jane Street sued Millennium in the U.S. District Court for the Southern District of New York, accusing it of stealing a highly valuable proprietary trading strategy.

During the court proceedings, a key detail was revealed: the strategy focused on Indian index options and generated approximately $1 billion in profits in 2023 alone.

This number changed the nature of the event. It is no longer a small arbitrage strategy, but a super-profitable engine.

What did this lawsuit reveal?

The lawsuit clarified three things:

This strategy is options-driven.

It operates in India's index derivatives market.

It offers extremely high profits and can be executed repeatedly.

However, almost everything about how it actually works has been hidden from the public. Large portions of court documents have been redacted. The public cannot see:

Algorithm that generates signals

Model for timing of execution

Strike Price Selection Framework

Delta Exposure Management

Cross-entity coordination process

Risk Control System

The only visible number is profit. The engine itself remains hidden.

The defense's argument:

Millennium Holdings argued that the structure of India's options market is public information and that the strategy is not proprietary.

The former trader claimed that the system is built on experience and expertise, not on hidden automated models. This raises a key point of disagreement:

If the advantage is merely structural, then anyone can replicate it.

If the advantage lies in execution—timing, coordination, position sizing, and layered derivatives positioning—then the system itself is the core asset. The execution system can be redeployed.

Why did this lawsuit trigger regulatory action?

This lawsuit produced an unexpected consequence: it revealed that a single trading strategy generates approximately $1 billion in profits annually in India.

This exposure triggered media coverage. Media coverage led to regulatory scrutiny. Regulatory scrutiny ultimately resulted in an SEBI investigation. SEBI's subsequent interim order described a maturity manipulation structure:

Spot trading influences index trends

A large options book captures substantial returns

The exposure of this $1 billion strategy made investigation unavoidable. The case was settled in December 2024. The terms of the settlement were not disclosed. No full trial was held, and no detailed strategy blueprint was released.

Its core operating mechanism remains sealed.

Why is it important to black out hidden content?

The importance of this redacted content lies in its structure. A $1 billion options strategy:

Operates across multiple entities

Dependent on derivative tiered structure

Fiercely defended in federal court

Its internal mechanisms have been erased from public view

It was the same company that later: faced SEBI allegations of expiration date manipulation; became entangled in litigation related to Terra; served as an authorized participant for a major Bitcoin ETF; and held substantial ETF positions without disclosing its derivatives hedging activities.

The internal trading system (i.e., the execution layer) is invisible in public documents; public reports only display positions.

They do not display execution logic. Court documents only show allegations. They do not display algorithm code. Regulatory orders only show outcomes. They do not reveal proprietary models.

When a company’s most profitable system is classified as top secret, and similar structural patterns repeatedly occur in other markets, rigorous scrutiny is only natural.

If a company can:

Manipulate the underlying market with massive capital. Layer on even larger derivatives exposure. Control influence at the settlement level. Coordinate operations across entities. Deeply understand the underlying mechanics of ETFs. And maintain strict confidentiality of execution systems.

Therefore, surface-level data can never reflect the full picture.

A company always at the center of every market manipulation incident?

Sam Bankman-Fried (SBF) worked at Jane Street for approximately three years before founding Alameda Research and later FTX. In April 2021, FTX invested $500 million in Anthropic, acquiring approximately 8% of the company.

In May 2022, Terra and UST collapsed. Alameda was reportedly severely impacted during the broader cryptocurrency market crash that followed. FTX subsequently filed for bankruptcy.

During the bankruptcy proceedings of FTX from 2023 to 2024, its shares in Anthropic were sold at an valuation of nearly $18 billion.

Jane Street was the second-largest buyer in this funding round, investing approximately $100 million to acquire shares. Therefore, the flow of funds forms a closed loop as follows:

A former Jane Street trader founded FTX.

FTX made an early investment in Anthropic.

FTX collapse

Anthropic shares are being liquidated

Jane Street acquired a portion of it, which is now worth $2.1 billion.

In 2024, Trump Media & Technology Group formally notified Nasdaq, alleging potential naked short selling and naming Jane Street as one of the firms responsible for the massive trading volume during its stock price decline. Although no formal legal charges were subsequently filed, the company was publicly named in this dispute.

Plus the following events:

India's SEBI issued a temporary ban, accusing it of manipulating expiration index futures and seizing approximately $570 million.

The Millennium lawsuit exposed a redacted Indian options strategy that generated approximately $1 billion in profits in one year.

Ongoing Terra lawsuit alleging insider trading related to the UST collapse

Jane Street serves as the primary authorized participant for the leading Bitcoin ETF.

Its position as one of the largest buyers of IBIT

The same company repeatedly appears across stocks, derivatives, cryptocurrencies, ETFs, and private AI equity funding rounds:

Market manipulation. Liquidity crisis. Regulatory scrutiny. Capital sell-off event.

None of these individual incidents can definitively establish collusion.

But the unsettling reality is:

Jane Street is often present whenever there is a major market crash or upheaval.

Is this merely a coincidental result of it being one of the world’s largest quantitative trading firms, with operations spanning all major asset classes?

Or is there a deeper structural issue here—does this company’s market positioning inherently allow it to profit massively from manipulation or crises?