Original author: Radigan Carter

Shenchao TechFlow

Introduction: The very context in which this analysis was written speaks volumes—the author developed this four-stage market framework while evacuating family members in Oman and dealing with missile attacks.

He does not attempt to predict outcomes, but instead deduces the most likely intermediate path: six weeks is the critical point for inflation transmission, July–August is the buying window, and in September, the Fed will be forced to cut rates.

This is one of the most information-dense and credible analyses of the Iranian war market to date.

The full text is as follows:

Over the past week, I intermittently completed this analysis amid evacuating my wife and responding to attacks in Oman. This is my current thinking on how this war may impact markets over the next six to twelve months. I am not making predictions—rather, I aim to outline the most likely middle-path scenario so we can adapt as events unfold.

My goal has always been, like Thucydides: to bear my own risks, seek understanding, and speak the truth clearly. When great powers collide once again, and we all feel the weight of uncertainty, my only concern is: as an individual investor, what should I do to protect my family?

I see four stages ahead.

Phase One

Denial. This is where we are now. We’re seeing volatility centered around the president’s statements—when he speaks, the market moves. Everyone is desperately trying to believe this new war in the Middle East will be brief. Powell has been assuring everyone this isn’t stagflation, all while watching Israel bomb the South Pars gas field, wishing he could throw his phone across the room.

Phase Two

If the war continues, the six-week trigger point in mid-April will activate this phase. By the sixth week, the oil price shock caused by strikes on energy infrastructure will spread to freight, food, and consumer goods. CPI data begins to cause panic. Tech stocks start to suffer real pain as valuation multiples begin to contract.

Tech stock valuations should decline—higher energy prices are driving hotter CPI data, which will eliminate any remaining expectations of Fed rate cuts. Powell has already begun quelling these hopes, and the April and May data will finish the job. This situation won’t change as long as Israel holds veto power over our foreign policy. Israel is bombing South Pars, while the U.S. is allowing Russia and Iran to sell oil on global markets in an attempt to stabilize energy prices.

When Powell extinguishes the last hope for rate cuts this year, the market will erupt in fury. And unlike every sell-off over the past 15 years, I’m not sure I can simply buy the dip and wait for the Fed to rescue me. The inflation we’ll see will be supply-driven—coming from bombings of gas fields and LNG terminals.

The Federal Reserve has a bunch of useless economics PhDs and a computer for printing money. It doesn’t have a team of petroleum engineers or LNG processing facilities in its basement. The Fed cannot solve this problem with monetary policy. Therefore, tech stock valuations priced on expectations of rate cuts will be repriced under the assumption that rates remain at current levels—before summer arrives, everyone will suffer once it becomes clear there’s no easy way out.

Stage Three

As summer arrives, targeting July to August, companies begin releasing earnings reports, and the damage we’ve observed firsthand starts to show up in real numbers: corporate profits fall short of expectations, and unemployment rises. Amid this war, the process of AI replacing workers will accelerate behind the scenes, as companies seek to cut costs in response to higher energy inputs. Politicians will begin to panic ahead of the November midterm elections.

The third stage is the buying opportunity I’m looking forward to.

The high-quality assets on my shopping list are likely to appear at meaningful discounts—when everyone is already tired of it all, angry about rising costs and declining job security, and demanding action before the fall and midterm elections. This will happen. We’ve moved from cost-cutting to massive spending akin to the Afghanistan war. Less than three weeks into the war, costs have already skyrocketed with no sign of slowing, and hundreds of billions are just the beginning. The Fed will eventually concede, politicians will ramp up fiscal support, and we’ll add over another trillion in debt to fund Israel’s war. Just stay patient.

Stage Four

From late 2026 to 2027, the Federal Reserve compromises and begins cutting interest rates, causing everything purchased in the third phase to start paying off. I believe that as we emerge from this crisis in the fourth phase, there will be heightened focus on energy independence and energy abundance. Both parties in Congress will sing the same tune. No one wants to be labeled as "obstructing solutions to this pain," as people have directly witnessed how disruptions in energy markets in one region lead to cost increases everywhere. This also provides them with justification and cover to cut interest rates, increase spending, and create jobs.

The war in Iran will underscore the necessity of controlling input factors, and I expect this to be beneficial for assets within U.S. jurisdiction or at least the Western Hemisphere. Against this backdrop, AI will only accelerate. Companies facing margin pressures and rising energy and input costs will use AI to cut labor expenses wherever possible. These are not typically considered AI or tech companies, but productivity gains will begin to reflect in their margins from 2027 onward. Emerging from this conflict, the story of AI won’t just be about companies building AI, but about those adopting AI to survive. This is the structural shift I’ll be looking for this summer.

How did this war begin?

The war has now been going on for nearly three weeks, and I still believe most people have underestimated the duration of this conflict. This is not because I am predicting the worst-case scenario—I am trying to focus on the most likely middle path—but because the theological framework driving Iran’s decision-making does not respond to the incentive structures assumed by Western politicians and commentators.

Shi’a tradition is built upon the story of Husayn ibn Ali, the third Shi’a Imam, who knew he would die in the Battle of Karbala in 680 CE. Despite facing thousands of enemies with only 72 companions, he still marched toward his death. In Shi’a theology, resisting injustice is an obligation, even when victory is impossible by conventional standards. Defeat and death are not failures—it is surrender to overwhelming injustice that constitutes failure.

The way Israel and the United States launched this war resembles a meticulous reenactment of the origin story of Shia Islam—diplomacy treated as a tool of deception, launching an attack at the very moment Oman’s foreign minister announced a diplomatic breakthrough, assassinating Khamenei and his family, just as Hussein was massacred after being promised safe passage.

That’s why Iranians won’t bow down, no matter how many targeted killings Israel carries out—against men who live peacefully with their families and civilians in residential areas. The Israelis know this, and they don’t care. Israel will bomb Tehran until it looks like Gaza, setting the entire Middle East ablaze. They are indifferent to chaos. What about the United States? I know I can’t.

Shiite theology reframes suffering as affirmation of walking the path of justice. This can be traced back to the 7th century, when Arab tribes emerged from the Arabian Peninsula and began conquering parts of the Roman and Persian territories. The Persians, an ancient civilization, viewed their conquest by the Arabs as an injustice, so Shiite theology found a natural home within Persian identity.

It is absurd to believe that Israel and the United States can assassinate their leaders, launch a few missiles, and expect them to submit to foreign powers—when their entire history has been built on resisting foreign domination for thousands of years. We remain tragically ignorant of who we want to go to war with, having learned nothing from the failures of the global war on terror and the war in Ukraine, yet we have handed the veto over foreign policy to psychopaths.

Current situation

It is day 20, and the conflict has crossed the threshold of energy cost penetration into the supply chain in phase two.

Yesterday, Israel attacked Iran’s South Pars gas field, the world’s largest natural gas field. Iran retaliated, severely damaging Qatar’s Ras Laffan LNG facility, which is likewise the largest in the world. QatarEnergy has declared force majeure on natural gas exports and halted LNG liquefaction production. Qatar accounts for approximately 20% of global LNG trade, with over 80% of its shipments destined for Japan, South Korea, China, and Taiwan. These supplies are now offline, and restoration may take years. Additionally, the Bazan Refinery in Haifa, Israel—which supplies 65% of Israel’s diesel and 59% of its gasoline—was also struck, along with other energy infrastructure in the Gulf region.

In Qatar, I worked for five years in Ras Laffan Industrial City, performing pre-commissioning on LNG facilities. Qatar Energy (known as QatarGas during my tenure) is vertically integrated, owning every stage from offshore gas fields to LNG processing plants, export terminals, and its fleet of LNG tankers.

These LNG processing facilities are massive. When they were built two decades ago, 250,000 workers reported to work each morning in the sweltering heat of this industrial city, where the under-construction facilities resembled a forest of cranes. Starting up these facilities—especially after damage, repair, inspection, and systematic recommissioning—is not a quick process. These natural gas processing plants are like small cities, costing tens of billions, with incredibly complex systems, some components custom-ordered with lead times measured in years.

Once missiles and Shahed-136 suicide drones enter these facilities, causing primary and secondary fragmentation damage, along with fire and blast waves, you must thoroughly inspect these systems before restarting them in stages. Some systems operate under extremely high pressure; overlooking even a single point of damage could lead to catastrophic failure.

If a custom long-cycle component is damaged, you may have to wait months or longer—for a new container to be manufactured in China or Korea, transported, unloaded at the port, and then escorted to its destination by Mammoet’s heavy-lift team.

I had hoped that the damage to Ras Lafan was not as severe and could be repaired within months rather than years. Unfortunately, it appears this is not the case.

This will immediately trigger ripple effects across other industries. Qatar’s offshore natural gas has a high sulfur content, and Qatar Energy, like using an entire cow efficiently, separates liquid hot sulfur from the gas, produces sulfur pellets, and ships them out via bulk carriers for use in manufacturing fertilizers, chemical products, cement, and refinery products. Once LNG production begins, it sets off a cascade of secondary and tertiary effects—some of which I currently cannot fully determine. The only certainty is that if this situation persists long enough, the global economy will begin to encounter problems in unexpected ways.

As Charles Gave said, the economy is the transformation of energy. As the energy sources the world relies on go offline and remain offline, countries will scramble to secure alternative energy imports. The offline status of Middle Eastern energy producers has led to rising global energy prices. This may benefit U.S. energy exporters, but over time, higher energy costs will be passed on to consumers, and businesses unable to afford energy at higher prices will shut down production and lay off workers.

Chart: Toward an Inflationary Collapse

Hormuz crisis

Beyond targeting energy infrastructure, the conflict continues to spread regionally. Israel is invading southern Lebanon, resulting in approximately 1,000 deaths and nearly a million people displaced. The Popular Mobilization Forces in Iraq—Iran-backed Shia militias that played a crucial role in the fight against ISIS in 2016—have now entered the conflict, attacking U.S. facilities in Iraq, Saudi Arabia, Kuwait, and Jordan. This has forced the United States to withdraw and redeploy personnel from the region, further undermining the U.S. military’s ability to sustain operations there.

I have sailed through the Strait of Hormuz multiple times and previously wrote an article about the strait.

Since the start of the war, more than 20 vessels have been targeted. The Islamic Revolutionary Guard Corps has launched 50 operations against U.S. bases in the region. My understanding is that, from Adana in southern Turkey, southward through Israel, and eastward across Lebanon, Syria, Iraq, the Arabian Peninsula, the Persian Gulf, and the Arabian Sea, the entire region is under Iran’s firepower control.

If the Houthi militia in Yemen is also included, then when the Houthis begin targeting Red Sea shipping, global maritime and energy trade will be split in two. Historical parallels include: the Ottoman Empire closing the Silk Road, the global economic shock triggered by the outbreak of World War I in the summer of 1914, and the 1956 Suez Crisis, which signaled to the world the end of the British Empire. This is why I believe that, after emerging from this crisis in its fourth phase, investors will reassess their portfolios and seriously consider the issues revealed by this war. Many may conclude: while profits are good, is the asset secure, and in which jurisdiction is it located? Assets located in jurisdictions that are considered safer—those not requiring passage through vulnerable chokepoints—may command a premium. The outcome of this conflict is of immense significance.

Climbing the upgrade tiers

Someone asked, since Iran has fire control over the strait, why doesn’t the U.S. begin targeting life-sustaining infrastructure? Given that targeted killings, regional escalation of conflict, and current strikes on energy producers have already occurred, further escalation is not something to be taken lightly—no matter how White House interns try to frame this war as a video game and release disgraceful propaganda videos.

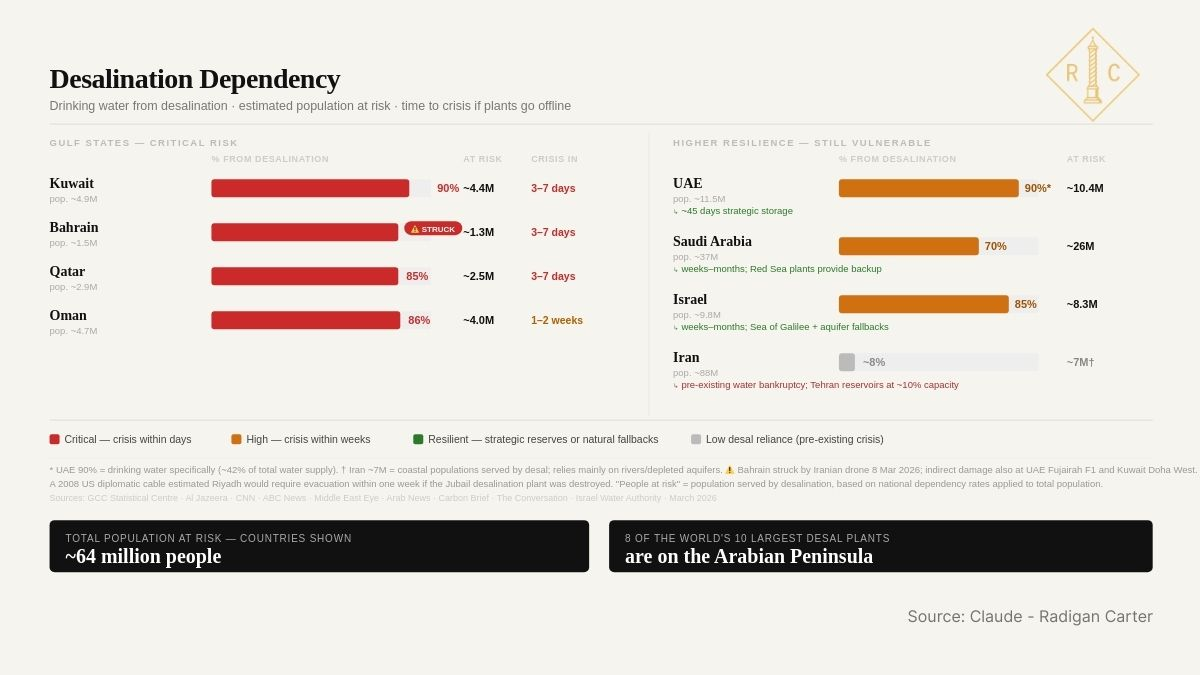

Unfortunately, we are already targeting life-sustaining infrastructure. On day 7 of the conflict, the United States struck a seawater desalination plant on Iran’s Qeshm Island—a strategic location guarding the Strait of Hormuz. Due to Iran’s geology, the island contains numerous natural caves, which the Islamic Revolutionary Guard Corps have spent decades improving and reinforcing as underground facilities.

The next day, Iran responded with an equal escalation, deploying attack drones to strike a seawater desalination plant in Bahrain. Kuwait and the UAE have also reported missile-related damage to their desalination facilities. The loss of desalination plants poses an existential threat to Gulf nations and Israel. With summer temperatures reaching 46°C, disruptions to drinking water and electricity could trigger a humanitarian crisis, posing a real risk of loss of life.

Over 90% of desalinated water in the Gulf region comes from just 56 plants. In Kuwait and Bahrain, desalinated water accounts for approximately 90% of the nation’s water supply. In Oman, where I am from, the figure is 86%; in Israel, it is 80%; in Saudi Arabia, 70%; and in the UAE, 42%.

If the United States and Israel continue targeting life-sustaining infrastructure, Iran will retaliate. As air defense interception capabilities become increasingly depleted, striking these facilities will grow easier—exposing a critical asymmetrical vulnerability for Gulf nations and Israel. Approximately 64 million people in the region could be affected, triggering a humanitarian and refugee crisis that would dwarf the Syrian civil war, with profound implications for Europe and Turkey.

Oil built modern the Middle East, but desalination keeps it alive. In this conflict, Iran holds the upper hand in both. The U.S. needs a steady flow of energy from the Persian Gulf to maintain global market stability, and the region cannot afford to lose its desalination plants. Israel can continue climbing the escalation ladder, but it will eventually reach the top—whereupon Iran will target its desalination facilities.

Phase Two: Logic of the Six-Week Trigger Point

Everything that has happened so far belongs to Phase One—our current position, why neither side can back down, and why the conflict is likely to persist. But tomorrow, Trump might announce a glorious victory on Truth Social, declaring the war over and claiming he has secured an incredible deal—even if the details aren’t true.

Whether the Strait of Hormuz remains under Iranian control doesn’t matter, and whether the U.S. has experienced its own Suez moment doesn’t matter either—those have longer-term implications, but that’s another issue. In this context, what matters is whether higher energy costs can be absorbed before they ripple through the rest of the supply chain; otherwise, this entire analysis falls apart.

While thinking, I asked myself: At what point had higher energy prices already been flowing through the system, regardless of what was said or what agreements were announced?

Six weeks—that’s the trigger point I’ve identified. By the sixth week, the denial phase ends. Nothing will be okay anymore; this war is not a 20-minute minor adventure. The inflation data from late April and May will reflect the substantial damage already done.

Chart: Every new conservative is talking about the Middle East

I arrived at the six-week trigger point this way:

During the first to second week, we observed refined product price adjustments, with gasoline and diesel at gas stations being repriced. Shortages began to emerge in more vulnerable countries. Oil prices rose by approximately 40% compared to pre-war levels.

Weeks three to four, which is the stage we are currently in. Shipping and logistics costs are beginning to adjust as carriers repricing based on new fuel costs. The February PPI data came in at 0.7%, above the expected 0.3%, serving as an early signal of this phase; April inflation data will likely be worse as costs continue to permeate the system.

During weeks five through eight, the increased shipping and logistics costs from the first two weeks flowed into consumer goods as costs were passed on to consumers. Food, building materials, and manufactured goods were all repriced, as the overall inflation in fuel and shipping costs from the previous month reached the consumer level.

By the sixth week, higher costs have been passed on to consumers, and it no longer matters whether the conflict ends—the elevated prices have already taken hold, especially after energy producers shut down; now, it’s just a matter of patiently waiting for the third and fourth stages to unfold over the summer and fall.

Six weeks ago, a ceasefire could have mitigated most of the damage, as contracts had not yet fully rolled over, companies could have reverted to previous pricing, and the Fed could have cut interest rates—everything would have been fine, at least in theory. However, my assessment may be off due to the impact on energy infrastructure and the foreseeable offline status of supplies such as Qatari natural gas.

Six weeks from now, even if a ceasefire is reached, nothing can undo what is already in motion. Rerating has already occurred, and the CPI data for May and June will reflect the damage, regardless of what happens in Iran.

CPI data will enable Powell—currently saying he is not concerned about stagflation—to extinguish the last remaining hopes for rate cuts this year, keeping interest rates at current levels. This will lead to shrinking tech profit margins, and the market won’t be happy. As this war drags on, no one will be happy.

Phase Three: The Long Summer and AI

This summer, my plan is to head to the beach and the gym, to cultivate patience, and by late summer, to take a serious look at where things stand. By August, we should start seeing corporate earnings reports reflect the damage we’re currently observing on the ground. Meanwhile, AI continues to accelerate behind the scenes as companies strive to cut costs amid increasing pressure on energy expenditures.

The company has been deploying AI instead of hiring, and now we’re adding an inflationary energy shock on top of that. You don’t need to be a rocket scientist to realize: when a company faces margin compression from $95 oil and needs to cut costs, it will use AI tools to replace employees wherever possible. This is no longer about innovation—it’s about survival.

AI adoption will accelerate during downturns, as it becomes an obvious way to reduce costs.

The cruel paradox is that this works extremely well for individual companies while simultaneously destroying overall demand. It will eliminate the income that workers would have spent, and I’m uncertain about the impact on creditors—those who previously believed they held gold-standard investments.

It’s also unclear how this will affect their colleagues—who are no longer certain about their own prospects and are cutting back on non-essential spending, especially as rising energy costs drive up the price of goods.

So if we see price increases stemming from energy shocks, coupled with employment deteriorating faster than any historical model predicted—because AI substitution is叠加 and amplifying cyclical downturns—I wouldn't be surprised.

This is the most important point regarding the timeline.

The Fed’s employment mandate will be triggered earlier than anyone expects—not just because of the war, but also because AI structurally amplifies underlying unemployment. This compresses the entire timeline, pointing toward a rate cut in September.

The Federal Reserve will face a dilemma: inflation it cannot combat and worsening employment that is about to get worse. They will hold steady throughout the summer and cut rates in September due to pressure from the midterm elections.

AI and technology stock prices will decline in this environment due to multiple contraction and slowing corporate revenues. But the narrative will actually grow stronger: companies that adopt AI will survive the downturn, while those that don’t will fail. Thus, when stocks are cheapest, the long-term argument becomes most compelling. That’s why I want to remain patient and buy technology and research companies in the third stage—those that will leverage AI to emerge from the crisis.

After phase four, people will look back and say: “Of course I should have bought that copper mining company—it was crushed at the time because no sulfur was flowing from Hormuz, but they turned 30-ton dump trucks into autonomous vehicles, and now they’re printing money because both parties in Congress believe in energy independence!”

Midterm elections

The Federal Reserve, the White House, and Congress each have different mandates, but they all face the same deadline—November. No governing body wants to confront voters amid stagflation without a policy response. No Federal Reserve chair wants to be seen as standing idly by as the economy deteriorates.

This consistency breaks the deadlock. The Federal Reserve will signal a September rate cut at the August Jackson Hole meeting, allowing every politician to campaign by saying, "We took action."

The market typically reacts 4 to 6 weeks in advance, meaning July to August is when I would seriously consider beginning to build my position—if the six-week threshold is triggered and the war continues. Meanwhile, AI-driven job market deterioration has actually accelerated this timeline. It has provided the Fed with political cover to cut interest rates even as inflationary pressures persist, by framing it as an employment emergency rather than a policy concession.

Outlook for 2027

The theme of energy independence emerging from this crisis will be massive and bipartisan, akin to defense spending during the global war on terror, but focused on energy. After higher energy prices and associated costs impact consumers, energy independence will become the dominant political narrative, transcending partisan divides by 2026 to 2027.

In this conflict, the bombardment of South Pars, Qatar’s LNG terminals, and Saudi refineries has made the vulnerabilities undeniable. Every politician is campaigning on “never again relying on the Middle East.” Both parties in Congress will push for increased infrastructure spending, expanded drilling, regulatory reforms, nuclear energy, and clean energy.

I constantly remind myself of the most important thing: I’m not trying to predict; I’m simply adapting. If a genuine peace agreement emerges—not just a tweet from Trump declaring it over, but an actual cessation of hostilities, the reopening of the Strait of Hormuz, the insurance market re-entering, and Iran having a negotiating partner capable of delivering compliance—then I will shift.

But to be honest, with Larijani killed and Israel continuously assassinating anyone we could negotiate with, that hope is fading every day.

This is my current thinking framework—not a prediction, but a flexible structure that can adapt as events unfold.